AMLR Solutions

AMLR Solutions AMLR Consultation

AMLR Consultation Onboarding

Onboarding Ongoing Monitoring

Ongoing Monitoring FRAML

FRAML KYC

KYC KYB

KYB KYI

KYI Age Assurance

Age Assurance Workforce IAM

Workforce IAM Candidate Verification

Candidate Verification Account Takeover

Account Takeover Bonus/ Promotion Abuse

Bonus/ Promotion Abuse Chargeback Fraud

Chargeback Fraud Deepfake

Deepfake Document Fraud

Document Fraud Fraud Networks

Fraud Networks Impersonation Fraud

Impersonation Fraud Money Mule Activity

Money Mule Activity Multi-Accounting

Multi-Accounting Party Fraud

Party Fraud Regulatory & Compliance Risks

Regulatory & Compliance Risks Synthetic Identity Fraud

Synthetic Identity Fraud Adult Content

Adult Content Banking

Banking Crypto

Crypto Fintech

Fintech Forex

Forex Compliance

Compliance Fraud prevention

Fraud prevention Trust & safety

Trust & safety Global expansion

Global expansion Compliance Officers

Compliance Officers Developers

Developers Fraud Analysts

Fraud Analysts Product Managers

Product Managers Advanced Journey Builder (AJB)

Advanced Journey Builder (AJB) Global Trust Platform

Global Trust Platform Customer Profiles

Customer Profiles Vendor Comparison

Vendor Comparison IDV Case Management

IDV Case Management AML Case Management

AML Case Management Regulatory Reporting

Regulatory Reporting Travel Rule Protocols

Travel Rule Protocols Agentic Rule Builder

Agentic Rule Builder AI Compliance Co-Pilot

AI Compliance Co-Pilot Fraud Analytics

Fraud Analytics Fraud Hub

Fraud Hub OCR

OCR Shufti AI

Shufti AI Bank Account Verification

Bank Account Verification Biometric Duplication

Biometric Duplication Database Checks

Database Checks Document Intelligence

Document Intelligence Government ID

Government ID Mobile Driver's License

Mobile Driver's License NFC

NFC Selfie Liveness

Selfie Liveness Brand Personalisation

Brand Personalisation Deployment Options

Deployment Options Identity Methods

Identity Methods IDV Modes

IDV Modes Multi-tenancy

Multi-tenancy On-Premise IDV

On-Premise IDV Secure Capture

Secure Capture

Enforcement of beneficial ownership rules has consistently lagged behind the rules themselves, leaving many institutions relying on ownership records that had not been independently verified in years.

That gap matters because a company’s registered shareholders are often not its real owners. Nominees sit between layers of holding entities. Subsidiaries operate in jurisdictions with minimal reporting requirements. The person whose name appears on incorporation documents may control nothing, while the actual decision-maker remains invisible to your compliance team.

This article covers what a business ownership structure actually contains, why verifying it is harder than most checklists suggest, and what good verification looks like in practice.

What is Ownership Structure

A business ownership structure describes who owns a company, who controls it, and how those two things relate to each other. In the simplest case, a small limited company has a direct match: one or two natural persons hold shares, those persons are named on company records, and a compliance check returns the relevant information in a matter of seconds.

The difficulty starts when ownership is indirect. A holding company owns 60% of an operating entity. That holding company is owned by a trust registered in a separate jurisdiction. The trust’s beneficiaries include another corporate vehicle. At each layer, the registered owner is a legal entity rather than a natural person, so reaching the human behind the structure requires active tracing, not a single registry lookup.

That tracing work depends on having the right ownership documentation in place from the outset.

The layers that create compliance blind spots

Nominee arrangements are one of the most common sources of opacity in a corporate ownership structure. A nominee director or shareholder holds a position on paper on behalf of the actual owner. The nominee’s name appears in official records. The actual controller does not. Without a declaration of trust or a separate nominee agreement, there is no automatic disclosure requirement in many jurisdictions.

Circular structures create a different problem. Entity A holds shares in Entity B, which holds shares in Entity A. Both entities meet the threshold for beneficial ownership reporting, but neither leads back to an identifiable natural person. These arrangements are not always designed to obscure control, but they consistently prevent automated registry lookups from reaching a resolution.

An EU-funded analysis of corporate ownership data from over 2.6 million firms across eight European countries found that firms with complex structures and owners from high-risk jurisdictions showed a materially higher likelihood of illicit activity. Structural complexity alone functions as a risk signal, regardless of underlying intent.

Challenges Linked to Complex Corporate Structures

Multi-layer ownership chains slow down verification considerably. Each additional entity in the chain means another registry lookup, another document request, and another round of screening before you can confirm who is actually in control. When layers span different jurisdictions, some with limited public registry access, that process rarely resolves quickly.

Automated tools help, but they depend on the quality of underlying registry data, which varies significantly by market. The result is that complex structures consistently produce longer onboarding timelines and higher rates of manual review than straightforward corporate clients.

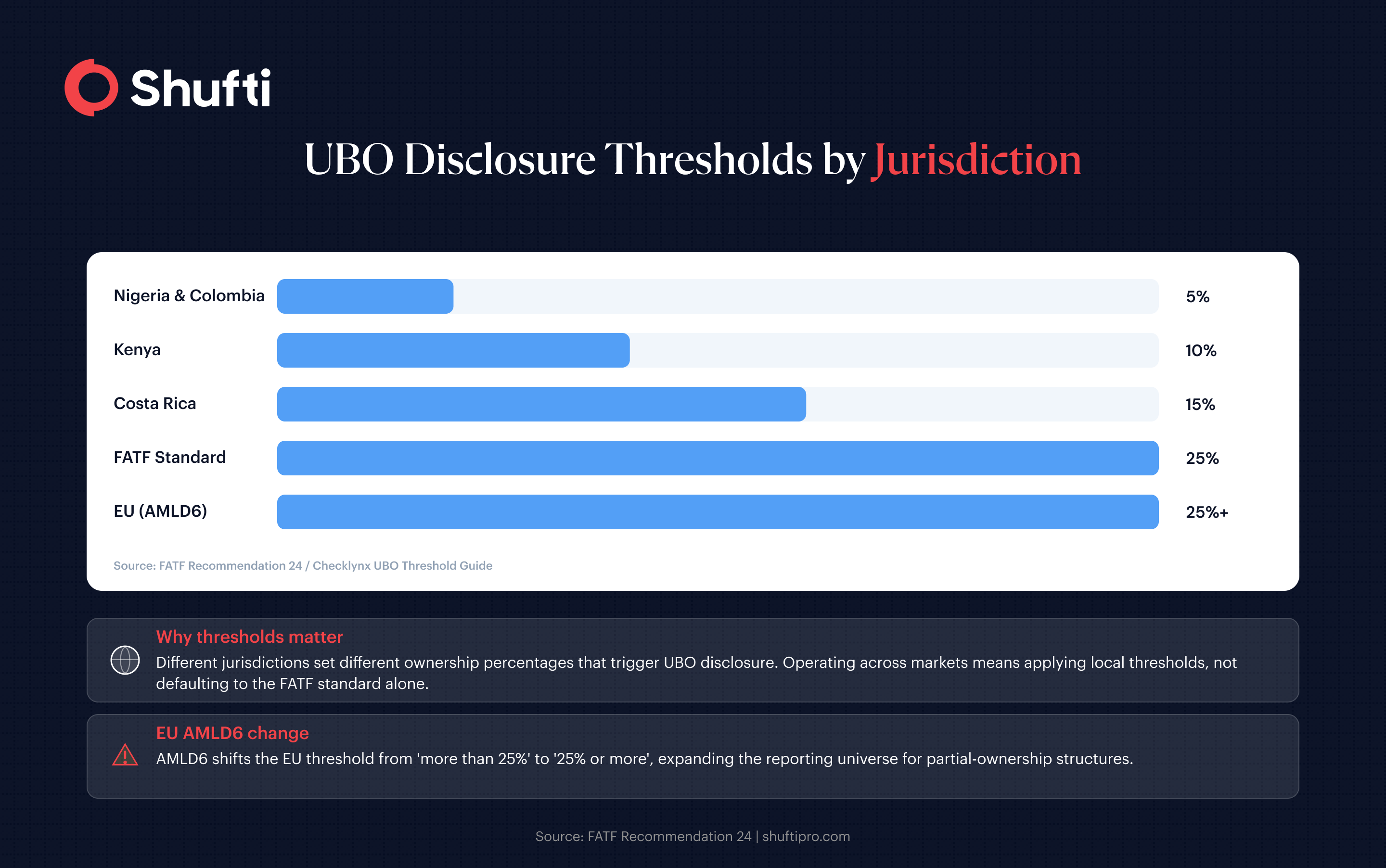

UBO thresholds and why they vary by jurisdiction

A UBO, or ultimate beneficial owner, is the natural person who ultimately owns or controls a company, identified by reference to a minimum shareholding threshold. The FATF’s amended Recommendation 24 sets 25% as the standard and requires that beneficial ownership information be accurate, current, and independently verifiable, not simply self-declared at onboarding.

Europe has moved to tighten this standard further. AMLD6 shifts the threshold from “more than 25%” to “25% or more,” a narrow technical change that expands the reporting universe. AMLA, the EU’s Anti-Money Laundering Authority, became operational in July 2025, with the full AMLR and AMLD6 framework applying from July 2027. Eleven member states faced infringement proceedings in 2025 for delays in beneficial ownership register access, a signal that regulators now treat register compliance as an active obligation.

Other jurisdictions apply tighter thresholds. Nigeria and Colombia require disclosure from 5%. Kenya sets the threshold at 10%. If your organisation onboards corporate clients across multiple markets, your ownership structure verification needs to account for the applicable threshold in each registration jurisdiction, not just the FATF default.

Red flags in a corporate ownership structure

Ownership patterns that change frequently without documented commercial rationale warrant closer attention. A company that has updated its registered shareholders multiple times in a short period may reflect genuine restructuring, or may indicate an attempt to shift ownership ahead of a regulatory scrutiny event. The pattern alone justifies enhanced due diligence and a request for supporting documentation.

Jurisdictional mismatches are another indicator. A trading company incorporated in a high-transparency market that routes ownership through an intermediate holding entity in a secrecy jurisdiction creates no operational benefit and appears repeatedly in FATF financial crime typologies.

Nominee directors and shareholders are not inherently suspicious. They are legally permitted in many markets. What they require is verification beyond the nominee’s identity alone: your team needs to identify who appointed the nominee and confirm that the appointment was disclosed at onboarding.

The FATF has described shell companies as the mechanism that enables money to move internationally without detection. When a company has no employees, no revenues, and no physical premises, alongside a multi-layer ownership chain, that combination warrants additional verification steps before the business relationship proceeds.

How to verify a company’s ownership structure

Verification starts with the official company registry in the jurisdiction of incorporation. Registry data confirms legal existence, registered shareholders, and in many markets the director list. For any company where the registered shareholder is itself a legal entity, the process continues upward through each ownership layer until a natural person is identified.

That chain-of-ownership tracing requires documentation at each step: articles of incorporation, shareholder registers, trust declarations, and director appointment records. Where nominee arrangements exist, the underlying agreement should be collected. Where a layer sits in a jurisdiction whose registry is not publicly accessible, the company can be asked to provide a notarised extract or a corporate service provider letter confirming the structure.

AML screening of each identified UBO is a required step, not an optional one. A natural person at the top of an ownership chain must be screened against sanctions lists, PEP databases, and adverse media before the business relationship proceeds. KYB processes that combine ownership tracing with AML screening reduce the manual co-ordination burden that slows most business onboarding programmes.

Ownership structures also change after onboarding. Frameworks including AMLD6 and the UK’s Economic Crime and Corporate Transparency Act now require that beneficial ownership information remain accurate over time, not only at the point of first check. Corporate KYC programmes built with continuous monitoring avoid the re-verification backlogs that accumulate when post-onboarding changes go undetected.

When your business onboarding relies on registry data alone, nominees, circular structures, and multi-layer holding entities can leave the person who actually controls a company completely invisible to your compliance team.

Shufti’s know your business verification traces ownership chains across 250+ jurisdictions, identifies UBOs in under 30 seconds, and flags post-onboarding ownership changes through continuous monitoring so your risk picture stays current.

Request a demo to see how ownership structure verification works on a real corporate structure from your target markets.

Frequently Asked Questions

What is a business ownership structure?

A business ownership structure identifies who owns and controls a company, covering the legal entities and natural persons that hold shares, voting rights, or other instruments of control. Compliance teams use ownership structure data to trace from a registered company to the individuals who ultimately benefit from or direct it.

How do you verify a company's ownership structure?

Verification starts with the official company registry, then works through each layer of ownership until a natural person is identified. At each step, supporting documentation should be collected: shareholder registers, trust declarations, nominee agreements, and director appointment records. Identified UBOs must then be screened against sanctions lists and PEP databases before onboarding proceeds.

What is a UBO in corporate ownership structure?

A UBO is the natural person who ultimately owns or controls a company, typically identified when their direct or indirect shareholding reaches the applicable disclosure threshold. The FATF standard is 25%, though some jurisdictions require disclosure from as low as 5%.

What ownership thresholds trigger UBO disclosure?

The FATF standard is 25% of shares or voting rights. The EU's AMLD6 applies the same level but as "25% or more," which slightly expands the reporting scope. Thresholds vary by jurisdiction: Nigeria and Colombia set the bar at 5%, Kenya at 10%. Compliance teams operating across multiple markets need to apply the relevant local threshold rather than defaulting to the FATF standard alone.