Face Verification

Face Verification

Address Verification

Address Verification

Document Verification

Document Verification

Age Verification

Age Verification

VideoIdent

VideoIdent

Fast ID

Fast ID

eIDV

eIDV

Consent Verification

Consent Verification

NFC Verification

NFC Verification

Business Verification

Business Verification

Due Diligence

Due Diligence

Investor Verification

Investor Verification

E-Signature

E-Signature

QES

QES

AML Screening

AML Screening

Transaction Monitoring

Transaction Monitoring

Adverse Media

Adverse Media

Business AML Screening

Business AML Screening

PEP & RCA

PEP & RCA

Sanctions

Sanctions

Watchlist

Watchlist

Behavioural Biometrics

Behavioural Biometrics

Device Fingerprinting

Device Fingerprinting

Biometric Face Authentication

Biometric Face Authentication

MFA

MFA

Fraud Hub

Fraud Hub

Onboarding

Onboarding

Ongoing Monitoring

Ongoing Monitoring

KYC

KYC

KYB

KYB

KYI

KYI

Age Assurance

Age Assurance

Identity Verification

Identity Verification

Workforce IAM

Workforce IAM

Candidate Verification

Candidate Verification

Compliance

Compliance

Fraud prevention

Fraud prevention

Trust & safety

Trust & safety

Global expansion

Global expansion

Product Managers

Product Managers

Compliance Officers

Compliance Officers

Fraud Analysts

Fraud Analysts

Developers

Developers

Deepfake

Deepfake

Bonus Abuse / Promotion Abuse

Bonus Abuse / Promotion Abuse

Account Takeover

Account Takeover

Synthetic Identity Fraud

Synthetic Identity Fraud

Document Fraud

Document Fraud

Impersonation Fraud

Impersonation Fraud

Multi-Accounting

Multi-Accounting

Fraud Networks

Fraud Networks

Chargeback Fraud

Chargeback Fraud

Money Mule Activity

Money Mule Activity

Party Fraud

Party Fraud

Regulatory & Compliance Risks

Regulatory & Compliance Risks

Fintech

Fintech

Crypto

Crypto

iGaming

iGaming

Forex

Forex

Social Network

Social Network

Marketplace

Marketplace

Banking

Banking

Gig Economy

Gig Economy

Blind Spot Audit

Blind Spot Audit

Deepfake Detector

Deepfake Detector

Liveness Spoofs

Liveness Spoofs

Document Originality

Document Originality

Document Deepfake

Document Deepfake

Global Trust Platform

Global Trust Platform

Journey Builder

Journey Builder

Case Management

Case Management

Shufti AI

Shufti AI

Fraud Analytics

Fraud Analytics

Vendor Comparison

Vendor Comparison

Brand Personalisation

Brand Personalisation

IDV Modes

IDV Modes

AI Compliance Co-Pilot

AI Compliance Co-Pilot

OCR

OCR

Secure Capture

Secure Capture

Deployment Options

Deployment Options

Identity Methods

Identity Methods

API Documentation

API Documentation

Mobile SDKs

Mobile SDKs

Service Status

Service Status

Help Center

Help Center

Contact Us

Contact Us

Technical Support

Technical Support

Supported Documents

Supported Documents

Supported Countries

Supported Countries

Content library

Content library

Blogs

Blogs

News

News

Reports

Reports

Insights

Insights

Knowledgebase

Knowledgebase

ROI calculator

ROI calculator

About

About

Career

Career

Press Release

Press Release

Certifications

Certifications

Partnership

Partnership

Awards

Awards

Events & Webinar

Events & Webinar

Interactive Demo

Interactive Demo

Podcast Studio

Podcast Studio

Spotlight Studio

Spotlight Studio

Know Your Customer

Verify Customers Faster Without Opening CDD Gaps

Shufti’s configurable KYC verification software integrates document verification, facial verification, eIDV, NFC checks, address verification, and AML screening into a streamlined KYC workflow. Verify genuine customers quickly, screen risk at onboarding, and escalate high-risk profiles to enhanced due diligence without stitching multiple vendors together.

One Platform for the Entire KYC Lifecycle

Synthetic Fraud Stopped Early

AI-generated documents and synthetic identities are raising onboarding risk. Shufti checks Synthetic Identity Fraud, originality, tampering, GenAI signals, replay attempts, & face liveness to detect deepfakes, injection, and synthetic document fraud before approval.

Tiered CDD Without Drop-Off

Risk-based CDD should not force every customer through the same checks. Shufti lets teams configure thresholds and routing, so low-risk users move faster while higher-risk profiles step up to NFC, eIDV, AML, or Customer Due Diligence software review.

Audit Trails With Context

Fragmented KYC stacks weaken evidence and slow compliance teams down. Shufti’s identity verification software connects identity checks, AML screening, alerts, reason codes, and case context into audit-ready records analysts can act on quickly.

Explore the Stack

Build a KYC Stack Without Stitching Vendors

Verify customers with the right identity checks

Confirm real users with document, biometric, NFC, address, and doc-less checks, then step up verification when risk or regulation requires it.

-

Document Verification

Verify government-issued IDs and supporting documents with in-house OCR, originality checks, tamper detection, and review-ready reason codes. Source-backed public metrics include <15s decision time, 150+ languages, 99% OCR accuracy, and 250+ regions.

-

Facial Biometrics

Match a live selfie to the ID photo and use iBeta-certified liveness, 3D depth/shape analysis, and deepfake/replay/injection defense to confirm real user presence. The public page lists 98.72% accuracy and <0.01% false match rate.

-

NFC Verification

Read chip-stored identity data from supported ePassports and NFC IDs for chip-level credential assurance, then compare the secure chip data against the user and document flow.

-

Address Verification

Validate proof of address as part of KYC for jurisdictions or risk tiers that require residential address evidence.

-

eIDV

Verify users through doc-less identity checks connected to eIDs, mobile wallets, and authoritative data sources; Shufti lists <3s response time, 85+ territories, and 270+ data sources.

Escalate high-risk customers and business relationships into deeper checks

Use this tab for higher-risk individual customers, corporate customers, UBO checks, investor onboarding, or EDD cases where standard KYC is not enough. Keep the wording focused on KYC escalation rather than repeating KYB page content.

-

Business Verification

For corporate customers, verify business registration, ownership/control structures, directors, and UBO evidence before opening the relationship.

-

Due Diligence

Route high-risk customers to EDD software workflows that can include additional documents, source-of-funds/source-of-wealth evidence, adverse media review, and analyst decisioning.

-

Investor Verification

For funds and investment platforms, combine investor KYC, business/entity checks, and AML screening in one onboarding path.

Screen at onboarding, monitor after approval

KYC should not stop after document capture. Run sanctions, watchlist, PEP/RCA, and adverse media checks alongside identity verification, then continue monitoring when regulations or internal policy require it.

-

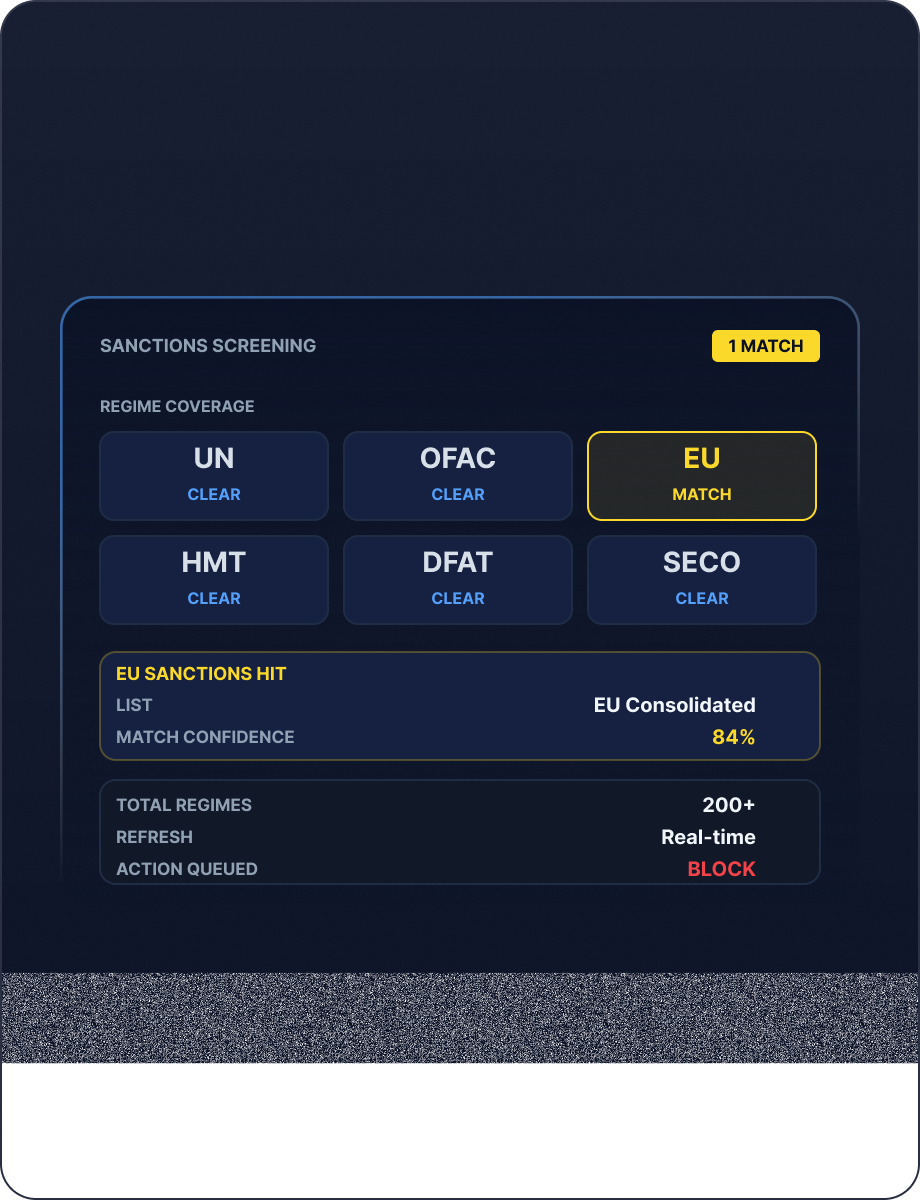

AML Screening

Screen individuals and entities with identity-aware matching, sanctions, watchlists, PEP/RCA intelligence, adverse media, case context, and audit-ready alert information. Shufti lists 3,500+ watchlists, 200+ sanctions regimes, and 50,000+ media sources.

-

Transaction Monitoring

Extend the KYC risk profile into post-onboarding monitoring for suspicious transaction behavior and evidence-led reporting.

-

PEP & RCA

Identify politically exposed persons, relatives, and close associates during onboarding and monitor changes after approval.

-

Sanctions

Screen against global sanctions coverage, including UN, OFAC, EU, HMT, DFAT, SECO, and additional sanctions regimes.

-

Adverse Media

Surface relevant negative news across global and local sources and classify media exposure by risk theme.

Stop identity fraud before the account is activated

Layer device, behavior, replay, liveness, and re-authentication controls over the KYC flow to catch fraud that a document-only check can miss.

-

Fraud Hub

Bring fraud signals from document forensics, biometrics, device, behavior, and injection defense into the verification journey.

-

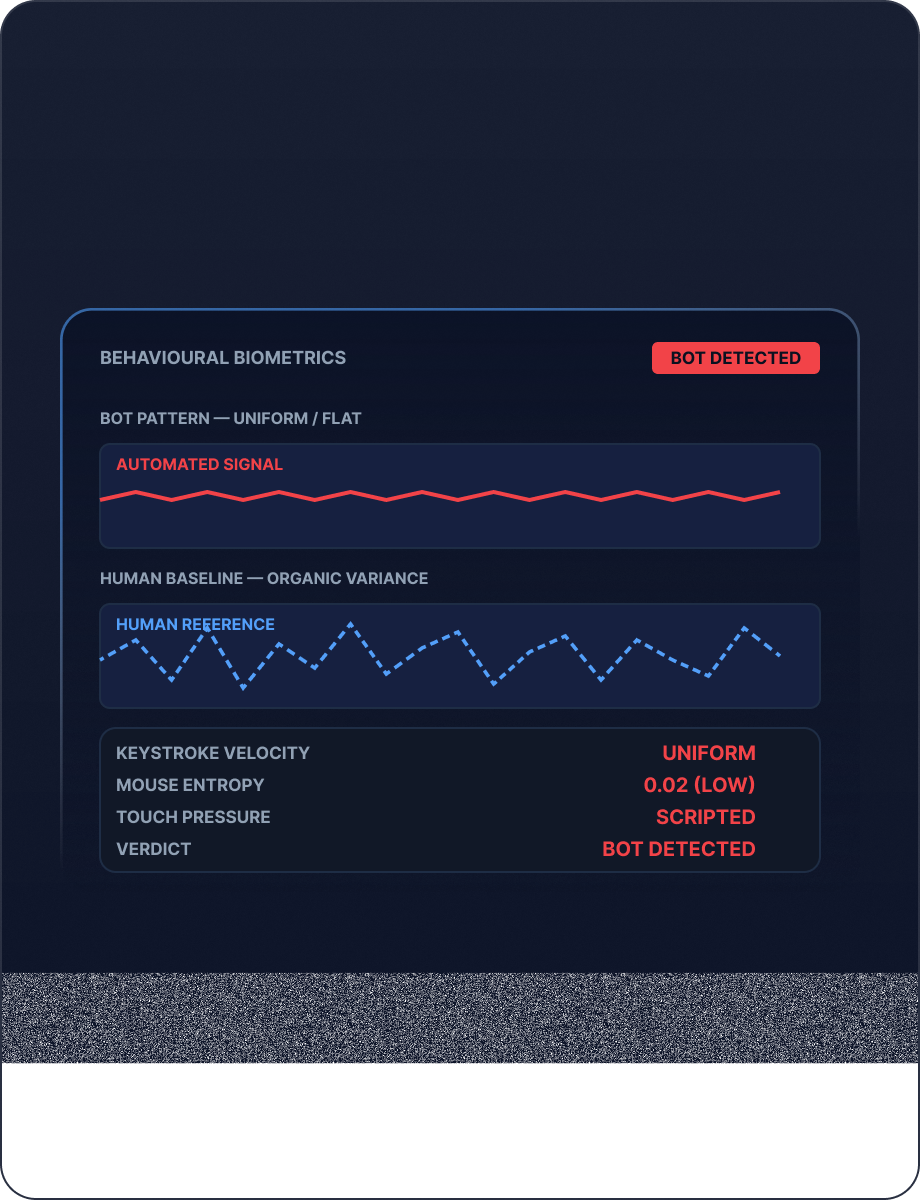

Behavioral Biometrics

Detects suspicious interaction patterns, bots, and automated submissions during the verification session.

-

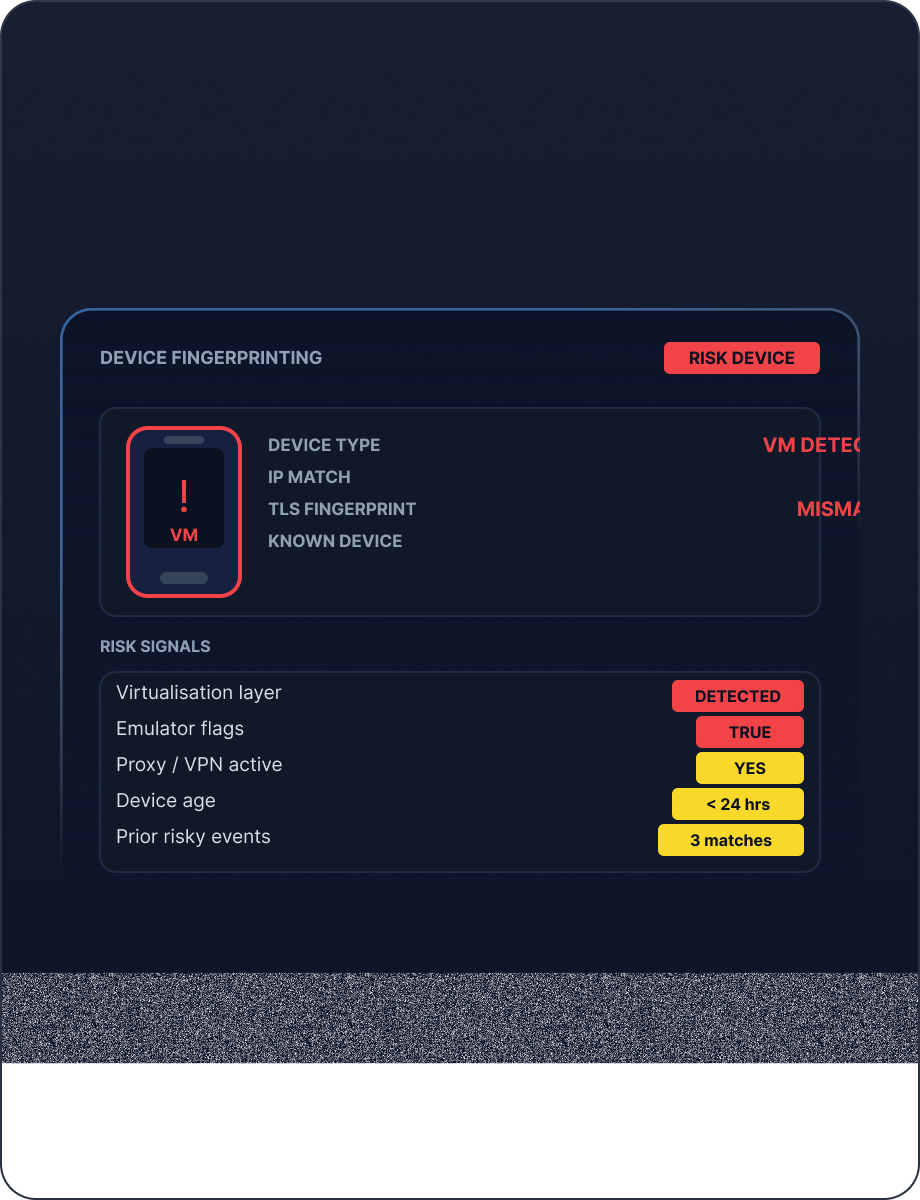

Device Fingerprinting

Assess whether the onboarding device looks genuine, spoofed, virtualized, or connected to prior risky behavior.

-

1:1 Authentication

For returning users, compare a live selfie against the enrolled profile to support re-KYC, account recovery, or step-up verification.

-

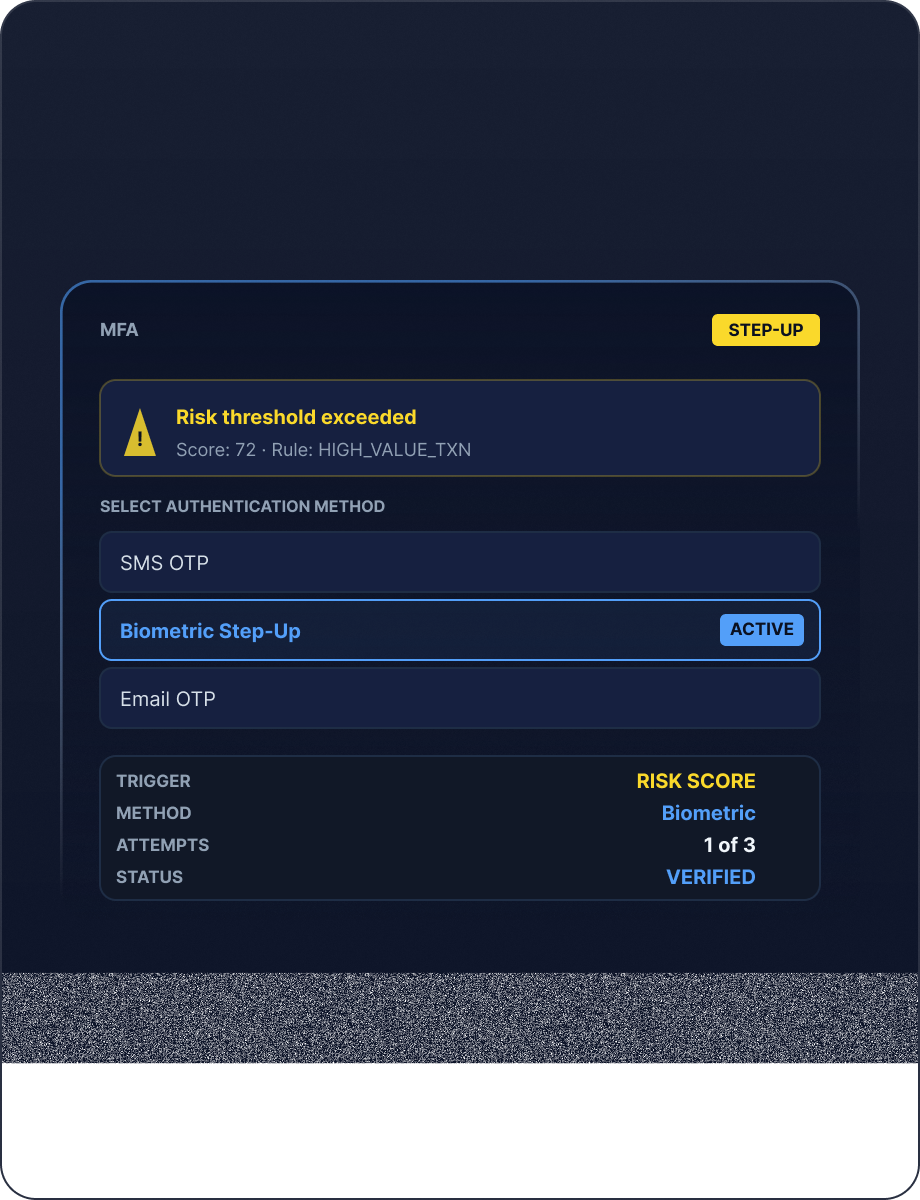

MFA

Trigger OTP or biometric step-up when a risk score, jurisdiction, or transaction context requires stronger assurance.

Everything You Need to Know About Your Customer

Build a compliant KYC stack from a single integration. Combine document verification, biometric checks, AML screening, and ongoing monitoring with role-aware tooling for compliance, product, engineering, and fraud teams.

Compliance Officer

Audit-ready evidence on every verification, structured for regulatory inspection across every jurisdiction you operate in.

Product Manager

Configurable verification flows that balance speed against risk tolerance, without rebuilding the integration each time.

Developer

REST API, mobile SDKs, and sandbox access. First verification call within hours of integration start.

Fraud Analyst

Pre-scored evidence and fraud signals on every flagged case, so your team reviews decisions, not raw submissions.

Detect Every Fraud Type Targeting Your Platform

Deepfake

AI-generated faces and synthetically forged documents bypass legacy liveness checks at scale. Shufti’s passive liveness & document forensics detects synthetic media before it reaches your onboarding flow.

Identity Fraud

Credential theft, blended synthetic identities, and manipulated documents exploit gaps in manual review. Shufti’s layered verification surfaces fraud signals before accounts are created.

Account & Platform Abuse

Duplicate registrations, bot-driven sign-ups, and referral exploits erode platform economics. Shufti links device, identity, and behavioural signals to flag abuse rings at scale.

Transaction & Payment Fraud

False chargeback claims, money mule networks, and sanctions evasion expose your business to financial and regulatory risk. Shufti ties identity verification directly to transaction context.

How it works

How Shufti Processes KYC Checks Without Extra Vendor Handoffs

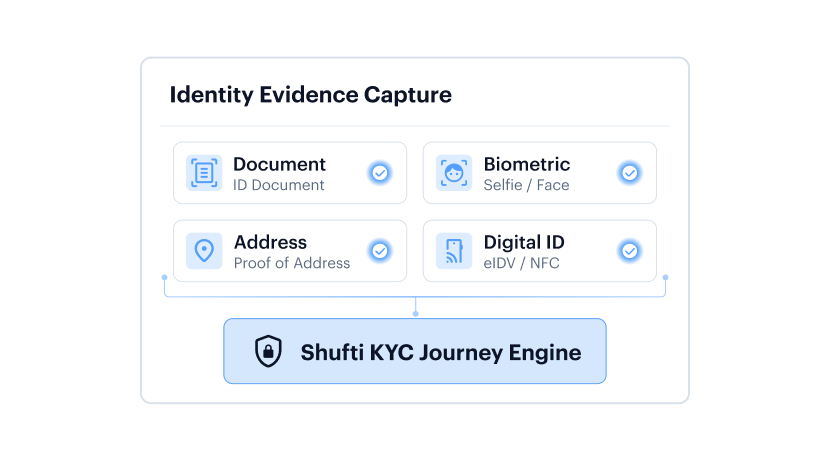

01

STEP 01

Identity Evidence Capture

The user captures or uploads an ID document, selfie, address proof, eID credentials, or other required evidence through the configured Shufti journey.

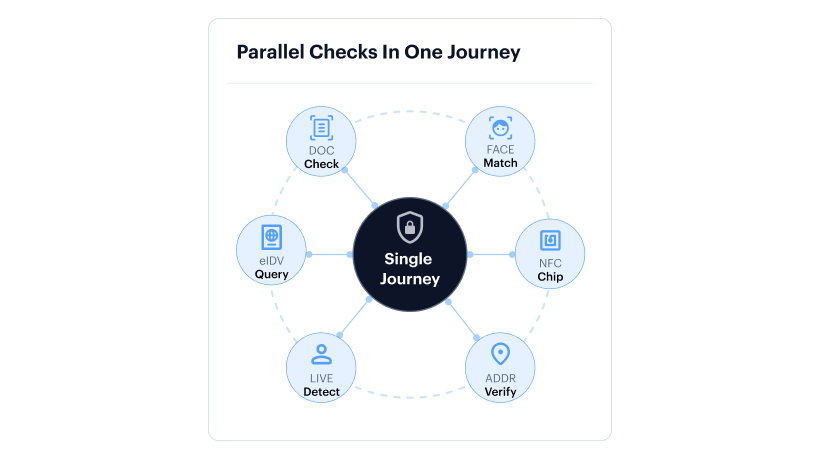

02

STEP 02

Parallel Checks In One Journey

Shufti checks document quality, authenticity, field extraction, face match, liveness, and optional NFC/eIDV signals based on the risk tier and jurisdiction.

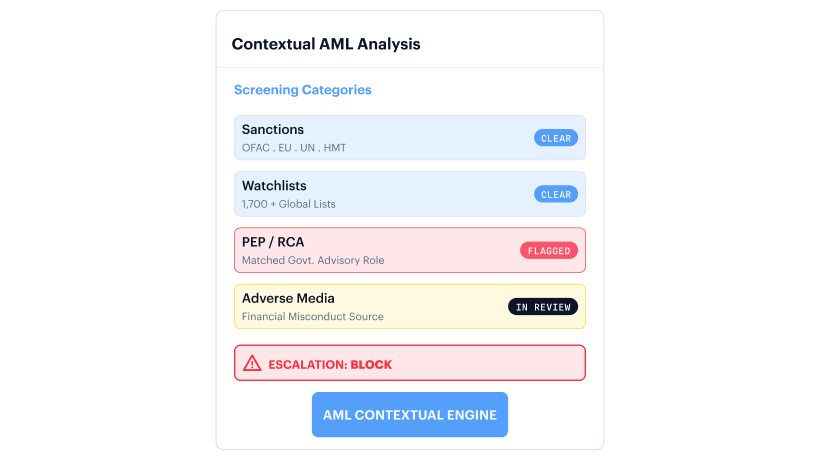

03

STEP 03

AML Screening Attaches Risk Context

Sanctions, watchlist, PEP/RCA, and adverse media checks create an identity-aware AML profile instead of a disconnected alert.

04

STEP 04

Evidence is Ready for Review

Analysts see reason codes, match signals, document integrity checks, AML context, and case records, reducing the need to rebuild the decision trail manually.

Single API, Seamless Integration

Build fully customisable verification flows with seamless backend integration.

- Gain full control by customising verification flows end-to-end.

- Integrate seamlessly with your backend for quick implementation.

- Design flexible verification journeys tailored to your users.

Launch a native verification experience in your mobile app within minutes.

- Launch native verification within minutes on iOS or Android.

- Use ready-made UI with camera, capture, and real-time feedback.

- Customise flows to fit seamlessly into your mobile app.

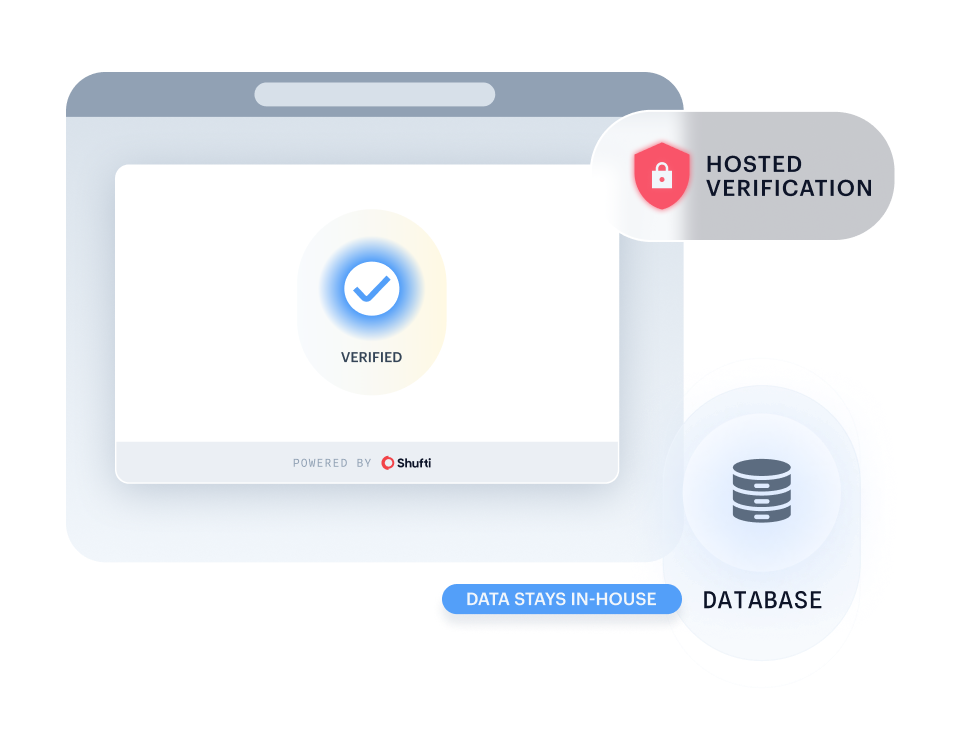

Run Shufti within your own identical-capability infrastructure for maximum data control and privacy.

- Keep all sensitive information in-house to meet strict governance and data residency requirements.

- Keep sensitive information fully private and secure in-house.

- Deploy in highly regulated sectors without compromising compliance.

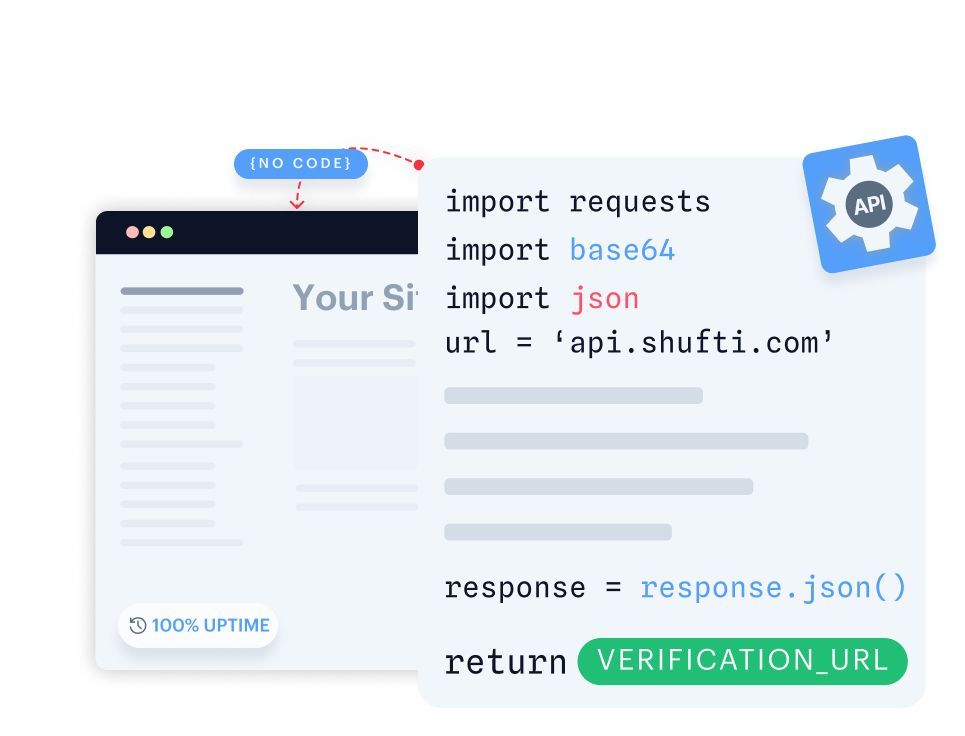

Quickly launch identity verification through a secure, customisable web link, no code required. Learn more.

- Start verifying users instantly with a no-code setup.

- Deliver a consistent identity experience via a link or embedded iframe.

- Deploy quickly via a secure link or embedded iframe.

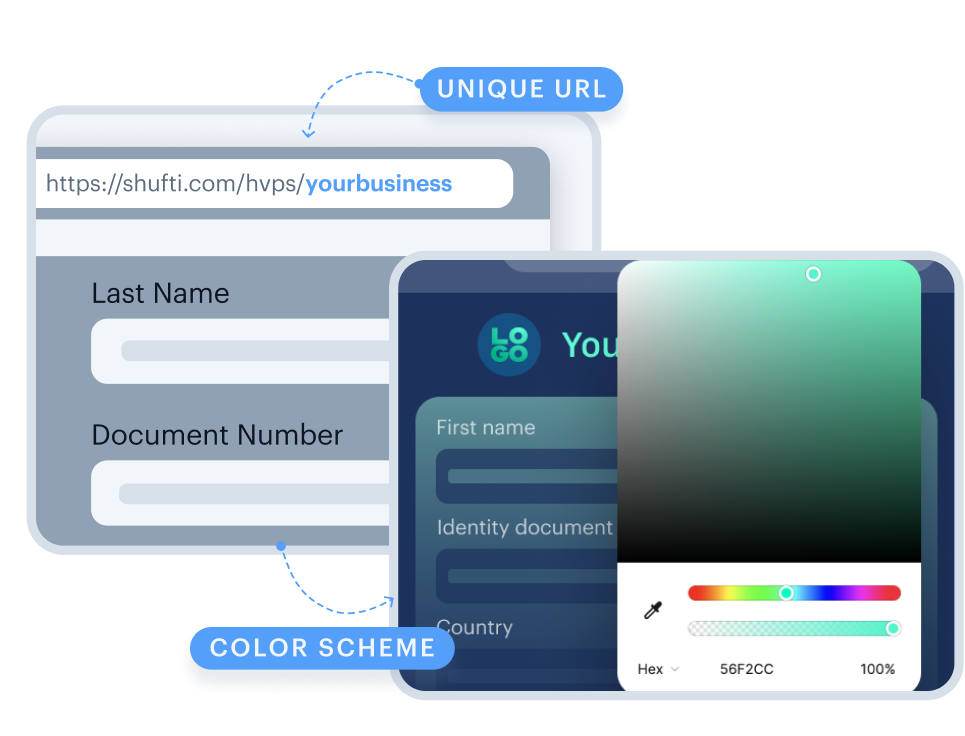

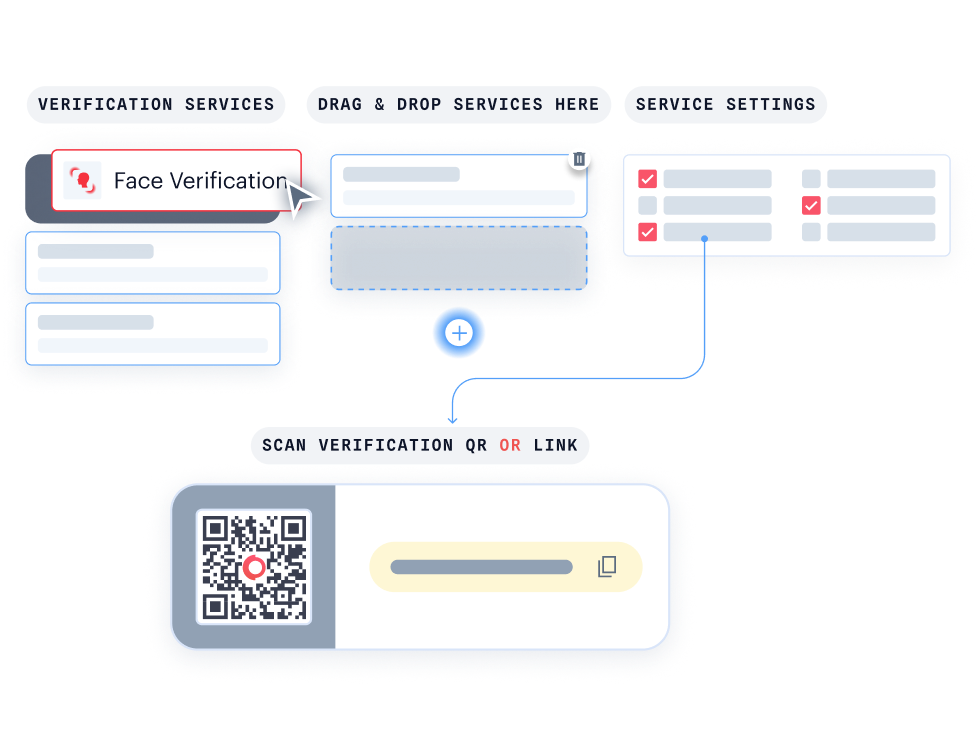

With KYC Journey Builder, create personalised verification journeys without writing a single line of code.

- Customise your journey effortlessly with drag-and-drop functionality.

- Instantly see how your verification flow looks for your users.

- Easily connect with Hosted Verification for a consistent, branded experience.

Validated by Leading Analysts and Certification Bodies

Where It Fits

KYC Built for Regulated Customer Onboarding

Trusted Sellers, Repeat Fraud Blocked

Verify the seller is real at onboarding, then prevent re-joins with duplicate detection and optional 1:N matching across the marketplace.

Don’t just take our word for it, hear from our customers

The Confidence Our Clients Share

The future of digital identity is defined by trust, interoperability, and regulatory alignment, so our partnership with Shufti’s global KYC and IDV software reinforces DevCode Identity’s commitment to supporting our global customers with the most secure, best-in-class, complaints identity verification solutions available today.

Combining our Conversion Driven Compliance Orchestration Platform with Shufti's global KYC and IDV capabilities allows our customers not only to navigate complex regulatory demands but also to maintain a seamless customer onboarding experience with the highest achievable conversion rates.

Shufti gives us verification journeys we can trust across every market we serve. The ability to route players through passive database checks, eID authentication, and full biometric liveness — all behind one API — has reshaped how we think about onboarding compliance.

Their team acts like an extension of ours. When regulators added new requirements across two European markets, Shufti’s journey builder let us adapt in days, not months.

FXBO customers demand speed without compromising AML rigour. Shufti’s eIDV fits exactly there — high-assurance verification for large deposits, invisible background checks for everything else, and one compliance trail across the board.

Integration took a single sprint. The SDK handled the full journey, so our product team stayed focused on trading features instead of building KYC screens.

As a regulated European payments platform, we need identity verification that meets eIDAS 2.0 and AMLD6 without multi-vendor stitching. Shufti delivers both — native eID authentication for high-assurance markets and docless database checks where eIDs don’t reach.

One contract, one audit log. That changes the compliance conversation entirely.

Frequently Asked Questions

What KYC checks does Shufti perform?

A standard Shufti KYC flow can include document verification, face verification with liveness, eIDV, NFC chip verification, address verification, AML screening, and ongoing monitoring. Teams can configure which checks run by geography, product, and customer risk tier.

Does AML screening run inside the KYC flow?

Yes. Shufti positions KYC/AML as a combined workflow, and the AML Screening product supports sanctions, watchlists, PEP/RCA intelligence, adverse media, case context, and audit-ready alerting.

Which regulations does the Shufti’s KYC compliance solutions help support?

The flow is designed to support CDD, risk profiling, AML screening, and ongoing monitoring workflows relevant to frameworks such as FinCEN CDD in the US, EU AMLD6/AML package requirements, and MAS Notice 626 for Singapore banks. Final regulatory mapping should be reviewed by legal/compliance for each client jurisdiction.

How does Shufti detect AI-generated documents and deepfakes?

Document verification checks originality, tampering, replay/recapture, GenAI/synthetic patterns, and quality signals. Face verification adds iBeta-certified liveness, 3D depth/shape analysis, and deepfake, replay, and injection defense.

How fast is KYC verification?

Use product-specific wording: Shufti Document Verification lists <15s decision time; Shufti Face Verification is built to confirm a real user in seconds; Shufti eIDV lists <3s response time. Avoid broad page-level timing claims unless confirmed by product.

What happens when a verification is high risk or fails?

Cases can be rejected, routed to manual review, or escalated to EDD depending on the configured risk policy. Shufti returns review-ready reasons and supporting signals so analysts can understand why the case was flagged.

How does Shufti reduce manual review?

The platform surfaces structured reasons, identity-aware AML context, and supporting signals. Shufti AML Screening publicly references fewer manual reviews and fewer false positives as impact metrics, but these should be used only where the page is comfortable relying on the product-page claim.

How do developers integrate the KYC flow?

Developers can integrate via API, SDKs, Journey Builder, and Back Office workflows. The exact timeline should be stated only after product confirmation for this page.

Assess Your KYC Stack Against Current Fraud and CDD Requirements

Digital document forgery, synthetic identity fraud, and AML enforcement risk are still material. Review whether your KYC architecture verifies identity, screens AML risk, escalates high-risk customers, and preserves review-ready evidence without manual vendor stitching.