AMLR Solutions

AMLR Solutions AMLR Consultation

AMLR Consultation Onboarding

Onboarding Ongoing Monitoring

Ongoing Monitoring FRAML

FRAML KYC

KYC KYB

KYB KYI

KYI Age Assurance

Age Assurance Workforce IAM

Workforce IAM Candidate Verification

Candidate Verification Account Takeover

Account Takeover Bonus/ Promotion Abuse

Bonus/ Promotion Abuse Chargeback Fraud

Chargeback Fraud Deepfake

Deepfake Document Fraud

Document Fraud Fraud Networks

Fraud Networks Impersonation Fraud

Impersonation Fraud Money Mule Activity

Money Mule Activity Multi-Accounting

Multi-Accounting Party Fraud

Party Fraud Regulatory & Compliance Risks

Regulatory & Compliance Risks Synthetic Identity Fraud

Synthetic Identity Fraud Adult Content

Adult Content Banking

Banking Crypto

Crypto Fintech

Fintech Forex

Forex Compliance

Compliance Fraud prevention

Fraud prevention Trust & safety

Trust & safety Global expansion

Global expansion Compliance Officers

Compliance Officers Developers

Developers Fraud Analysts

Fraud Analysts Product Managers

Product Managers Advanced Journey Builder (AJB)

Advanced Journey Builder (AJB) Global Trust Platform

Global Trust Platform Customer Profiles

Customer Profiles Vendor Comparison

Vendor Comparison IDV Case Management

IDV Case Management AML Case Management

AML Case Management Regulatory Reporting

Regulatory Reporting Travel Rule Protocols

Travel Rule Protocols Agentic Rule Builder

Agentic Rule Builder AI Compliance Co-Pilot

AI Compliance Co-Pilot Fraud Analytics

Fraud Analytics Fraud Hub

Fraud Hub OCR

OCR Shufti AI

Shufti AI Bank Account Verification

Bank Account Verification Biometric Duplication

Biometric Duplication Database Checks

Database Checks Document Intelligence

Document Intelligence Government ID

Government ID Mobile Driver's License

Mobile Driver's License NFC

NFC Selfie Liveness

Selfie Liveness Brand Personalisation

Brand Personalisation Deployment Options

Deployment Options Identity Methods

Identity Methods IDV Modes

IDV Modes Multi-tenancy

Multi-tenancy On-Premise IDV

On-Premise IDV Secure Capture

Secure Capture

The world we live in no longer seems to be honest and fair. A large number of individuals are participating in fraudulent and unethical activities every day. Causing a loss of billions of dollars per annum, the fraud instances are still on the verge of increasing. According to the FTC, about 3 million complaints regarding identity theft and fraud were received in 2018, out of which 1.4 million were fraud-related. In 25 percent of those cases, money loss was reported. In the same year, it was reported that consumers lost about $1.48 billion in fraud complaints, an increase of $406 million from 2017.

In 2018, about 130,928 of the cybercrime cases were related to credit card frauds. These types of frauds are committed to obtain goods or services or to make payments to other accounts that are controlled by a criminal or fraudster. The Payment Card Industry Data Security Standard (PCI DSS) is the data security standard established to assist businesses to securely process card transactions and reduce card fraud. To cater to the problem of fraudulent credit card transactions, the concept of chargebacks was originated.

Chargebacks and their importance

Chargebacks are transaction reversals that are forcefully initiated by the cardholder’s bank in case of a fraudulent transaction. It is mostly considered a consumer protection mechanism. If you’re a business or merchant, chargebacks can be a frustrating threat to your livelihood. If you’re a consumer, chargebacks represent a shield between you and corrupt vendors. If someone’s payment card is stolen, it can be used to make transactions at any physical or online platform. When the cardholder is notified about the transaction, he/she claims that they were not responsible for it and they claim the transaction amount from their bank. This is known as a chargeback. The bank refunds the amount to the customer and in turn, imposes heavy regulatory penalties or fines to the business or merchant for not conducting proper due diligence of the customer.

Chargebacks were introduced in the early 1970s when the US has started introducing credit cards. There was consumer fear regarding the use of these new cards. There were also complaints regarding unethical merchants taking advantage of the consumers. This led to the creation of chargebacks in the Fair Credit Billing Act of 1974. According to a study, Chargebacks account for 70% of fraud and cost merchants nearly $11.2 billion in lost revenue in 2015. The E-commerce industry lost an estimated revenue of $6.7 billion as a result of chargebacks in 2016 out of which 71% ($4.8b) was due to friendly/chargeback fraud. While chargebacks provide a protective shield to customers against fake transactions, on the other hand, they cause losses to many businesses as well.

Types of Chargebacks:

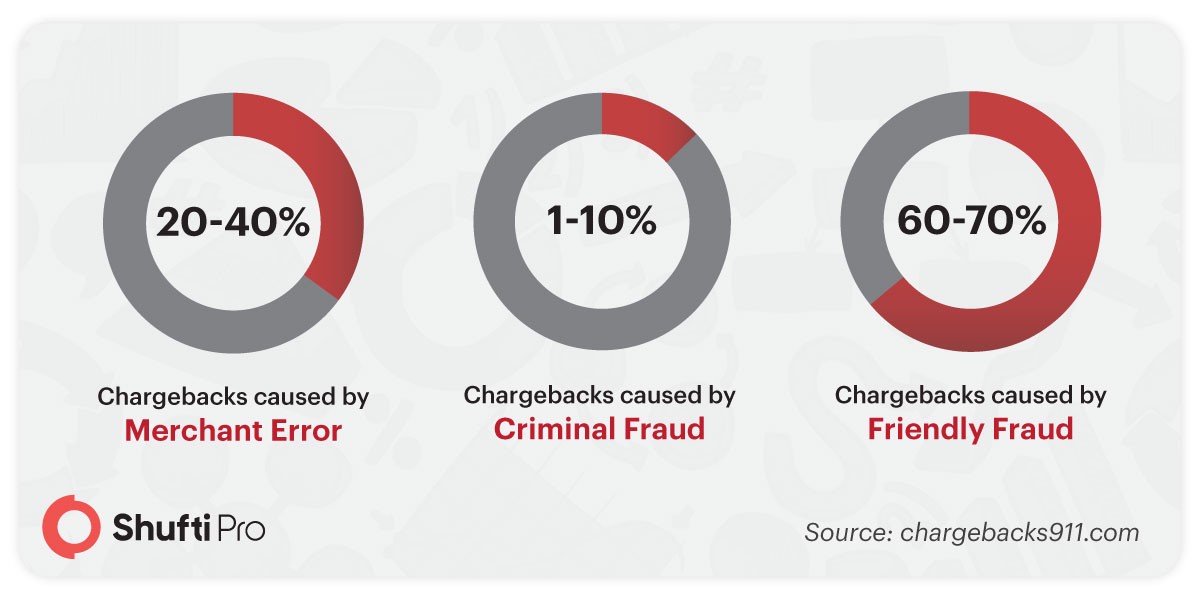

1: Merchant Error

Innocent mistakes and errors at the merchant’s behalf can have a major impact on the business’s bottom line. Errors are mostly linked with merchant setup, transaction data, and order processing. About 20-40% of all chargebacks are caused by merchant error.

2: Criminal Fraud

Criminal fraud is one of the primary reasons chargebacks were created. In this type the cardholder claims that the transaction was not authorized. This chargeback is triggered due to various forms of criminal activities:

- A criminal finds a lost card

- Counterfeit cards are generated with stolen account information

- Hacked account information is used to conduct the card-not-present transaction

About 1-10% of all chargebacks are caused by criminal fraud. 3: Friendly Fraud

3: Friendly Fraud

This chargeback involves unsatisfied customers who contact the business directly with any complaints they may have. However, some consumers use the bank as a middleman and file a chargeback instead of asking for a refund. And because the business is not aware of any issues with the transaction, friendly fraud is performed by apparently satisfied customers. Friendly fraud chargebacks account for 60-70% of all chargebacks.

How can businesses save themselves from false chargeback claims?

As we can conclude from the statistics above, false chargebacks can have devastating effects on the prosperity of a business. It is crucial for businesses to take strict measures for the prevention of chargeback instances. This is possible by conducting proper identity verification or due diligence of customers before transactions are conducted. Financial regulatory authorities such as FATF have introduced strict KYC and AML regulations that are mandatory to follow for financial institutions and banks. However, businesses are increasingly adhering to these compliances for their own security.

Identity verification has been practiced for many decades but the manual method is very time-consuming and there are chances of human error. Recently due to the innovations in the IT sector, artificial intelligence-based digital identity verification systems have been introduced. These systems remotely verify the identities of customers from any corner of the world within a few seconds. There are different types of digital ID verification techniques that are used by businesses:

- Face Verification

- Document Verification

- Address Verification

- 2-Factor Authentication

- Consent Verification

Once the identity of the customers is verified before every transaction, businesses will have recorded proof for it which can be presented to the bank in case of a false chargeback claim. If businesses ensure the provision of prompt and attentive customer service, quality products and services, and paying attention to transaction details, customers will not have a sound reason to file a chargeback. Instances of friendly fraud will decrease significantly.

Wrapping Up…

Fighting chargebacks is the last major responsibility businesses should face at this time. Banks have allowed fewer chargebacks to be filed against businesses that regularly argue regarding these claims. Not only does chargeback resentment make sure that the business gains more profits, but it is also helpful in educating consumers about what isn’t and what is a chargeback and how it should be used accurately. Customers should also understand that chargebacks should be filed in extreme scenarios only; they are the last resort rather than the first action to take to seek a refund. Chargebacks should not be used senselessly, as the consequences for the businesses are quite harsh. Hopefully, with proper education about chargebacks, both customers and businesses can notice a decline in the number of fraudulent chargeback claims.