AMLR Solutions

AMLR Solutions AMLR Consultation

AMLR Consultation Onboarding

Onboarding Ongoing Monitoring

Ongoing Monitoring FRAML

FRAML KYC

KYC KYB

KYB KYI

KYI Age Assurance

Age Assurance Workforce IAM

Workforce IAM Candidate Verification

Candidate Verification Account Takeover

Account Takeover Bonus/ Promotion Abuse

Bonus/ Promotion Abuse Chargeback Fraud

Chargeback Fraud Deepfake

Deepfake Document Fraud

Document Fraud Fraud Networks

Fraud Networks Impersonation Fraud

Impersonation Fraud Money Mule Activity

Money Mule Activity Multi-Accounting

Multi-Accounting Party Fraud

Party Fraud Regulatory & Compliance Risks

Regulatory & Compliance Risks Synthetic Identity Fraud

Synthetic Identity Fraud Adult Content

Adult Content Banking

Banking Crypto

Crypto Fintech

Fintech Forex

Forex Compliance

Compliance Fraud prevention

Fraud prevention Trust & safety

Trust & safety Global expansion

Global expansion Compliance Officers

Compliance Officers Developers

Developers Fraud Analysts

Fraud Analysts Product Managers

Product Managers Advanced Journey Builder (AJB)

Advanced Journey Builder (AJB) Global Trust Platform

Global Trust Platform Customer Profiles

Customer Profiles Vendor Comparison

Vendor Comparison IDV Case Management

IDV Case Management AML Case Management

AML Case Management Regulatory Reporting

Regulatory Reporting Travel Rule Protocols

Travel Rule Protocols Agentic Rule Builder

Agentic Rule Builder AI Compliance Co-Pilot

AI Compliance Co-Pilot Fraud Analytics

Fraud Analytics Fraud Hub

Fraud Hub OCR

OCR Shufti AI

Shufti AI Bank Account Verification

Bank Account Verification Biometric Duplication

Biometric Duplication Database Checks

Database Checks Document Intelligence

Document Intelligence Government ID

Government ID Mobile Driver's License

Mobile Driver's License NFC

NFC Selfie Liveness

Selfie Liveness Brand Personalisation

Brand Personalisation Deployment Options

Deployment Options Identity Methods

Identity Methods IDV Modes

IDV Modes Multi-tenancy

Multi-tenancy On-Premise IDV

On-Premise IDV Secure Capture

Secure Capture

Fintech

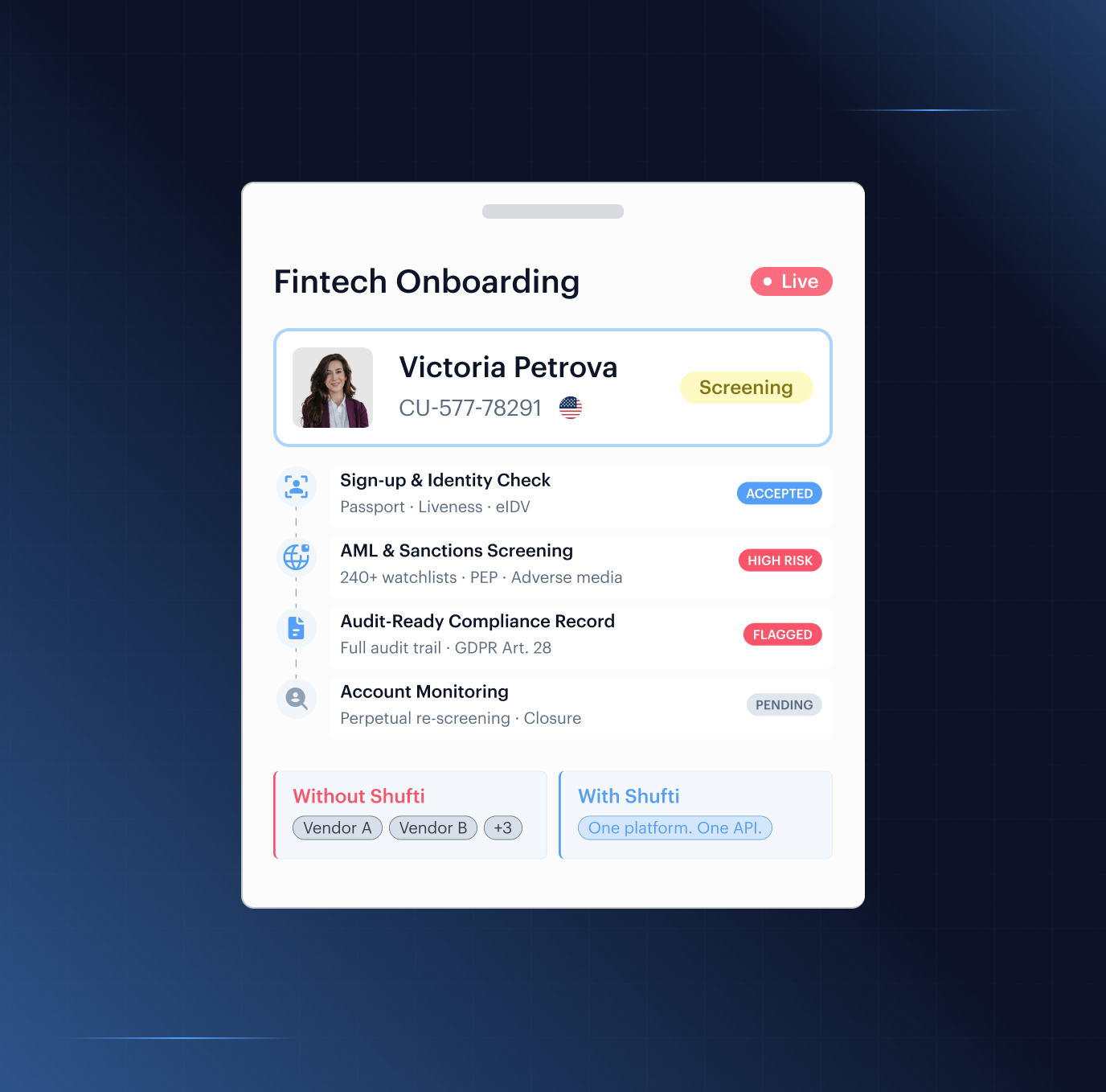

Secure the Entire Fintech Customer Lifecycle with Fintech Compliance

Verify users, screen for financial crime, and build audit-ready compliance records; from sign-up to account closure, without multiplying vendors.

Proven Performance

Our impact, by the numbers

- <30sMedian Time-to-Decision

- 4,000+Watchlists Screened

- 240+Countries Actively Processed

Trusted by Leading Digital Enterprises Worldwide

Compliance Without Compromise

Why Fintech Platforms Choose Shufti

-

Growth Without Compliance Gaps

Starling Bank was fined £28.9M by the FCA in 2024. Monzo received a £21.1M FCA fine in 2025. In both cases, compliance controls failed to scale with user growth; the FCA found high-risk accounts onboarded during periods of rapid expansion. Shufti's risk-based orchestration scales with your platform, not behind it.

-

Stop Fraud Before It Onboards

Deloitte projects generative AI fraud losses could reach $40 billion by 2027. Shufti's iBETA Level 3-certified liveness detection and device intelligence intercept synthetic identities, injection attacks, and bot-driven registrations at the device level; before a fraudulent account is ever created.

-

One Audit Trail, Every Regulator

FCA Consumer Duty, DORA, AMLD6, and PSD2 each require documentation your existing stack may not produce separately. Shufti generates a unified, regulation-mapped evidence chain for every user; exportable in under five minutes, in PDF and JSON.

Secure Every Stage Of The Fintech User Lifecycle

Sign Up

Bot Account Farming

A fraud ring deploys automated scripts to register thousands of accounts within hours, targeting sign-up bonuses and referral credits. Shufti's proprietary Device Fingerprinting identifies the emulators, proxy rotations, and shared infrastructure that scripts cannot hide. Behavioural Biometrics flags the inhuman form-completion speed and absence of natural touch patterns. The Fraud Hub cross-references device and behavioural signals across the platform to surface the ring before a single reward is paid out.

Synthetic Identity Registration

A fraudster assembles a fictitious identity from stolen PII fragments: a real national insurance number, a fabricated name, and a mismatched date of birth, then uses it to open an account. Shufti's eIDV cross-references every declared field independently against government, telco, and credit bureau records. Where the NI number is real but the name has no matching electronic footprint, the identity fails at source. Device Fingerprinting links the attempt to prior synthetic registrations from the same infrastructure.

Multi-Accounting / Duplicate Sign-Up

A user registers under three different email addresses and two slight name variations to multiply per-user incentives across the same platform. Shufti's 1:N Facial Deduplication continuously checks every new registration selfie against all enrolled faces. The same person cannot hold two verified accounts. Device Fingerprinting links accounts operating from the same hardware, even when VPNs or browser resets are used between sessions. The Fraud Hub surfaces the coordinated pattern before any duplicate account becomes active.

Stolen Identity Registration

An attacker uses a victim's PII, obtained from a data breach, to open an account the victim does not know about. Shufti's eIDV detects contact-detail mismatches: the name and number may be real, but the device, location, and declared contact data do not align with the identity's known data footprint. The Face Verification step requires a live selfie, confirming the person presenting is the identity owner. A stolen PII pack with no matching live face fails at this stage.

Emulator / Headless Browser Onboarding

An attacker runs the sign-up flow from a device emulator or headless browser to evade device-level controls, often across multiple fabricated identities in parallel. Shufti's Device Fingerprinting detects emulator signatures, missing hardware sensors, and abnormal screen properties that real devices always produce. Behavioural Biometrics identifies the absence of natural gesture and timing patterns that distinguish an emulated session from a genuine user. The registration is blocked before the identity check begins.

Referral / Sign-Up Bonus Exploit

A coordinated ring creates hundreds of accounts to self-refer or farm per-user sign-up rewards, using residential proxies to disguise the shared origin. Shufti's Device Fingerprinting links accounts by hardware fingerprint, IP, and proxy signatures that survive cookie wipes and browser resets. The Fraud Hub aggregates cross-account signals, including registration timing, referral chains, and shared devices, to surface the ring structure. Accounts within the ring are flagged simultaneously rather than as unconnected individuals.

Affiliate / Install Fraud

A fraudster generates fake sign-up events through scripted installs or click farms to drain acquisition budgets without producing genuine users. Shufti's Behavioural Biometrics distinguishes real user intent from scripted engagement by the absence of natural exploration patterns immediately after sign-up. Device Fingerprinting identifies the shared infrastructure behind click farm operations, including same hardware, same OS configuration, and same timing intervals. The Fraud Hub flags the volume and velocity of these events before campaign spend is wasted.

Verify Identity (KYC)

Document Forgery

A fraudster submits a tampered or fabricated passport, purchased on a dark-web market, during the KYC step. Shufti's Document Verification runs forensic analysis across any government-issued document, checking template integrity, font consistency, MRZ validity, and AI-generated artefacts that standard OCR misses entirely. Where the physical document appears genuine but data has been altered, NFC Verification reads the cryptographic chip directly and rejects any mismatch between the chip and the presented document. A forged document cannot pass both layers.

Deepfake / AI Face Attack

An attacker generates a synthetic face video using AI tools and presents it at the selfie step, attempting to impersonate the real identity owner. Shufti's Face Verification, certified at iBETA Level 3, applies 3D depth mapping and micro-movement analysis to detect the absence of natural human physiological signals that live faces always produce. Injection Detection identifies when a pre-recorded or AI-generated video is being fed through a virtual camera rather than a live device sensor. The attack is rejected at the hardware layer before any face comparison runs.

Camera Injection Attack

An attacker installs virtual camera software that feeds a pre-recorded or synthetic image in place of the device's live camera feed during the verification step. Shufti's Injection Detection identifies virtual camera drivers and emulator signatures at OS level before biometric capture begins. Device Fingerprinting flags the absence of expected hardware sensor data, since a real camera produces signals that virtual cameras cannot replicate. The session terminates before the attacker reaches the facial comparison stage.

Identity Pack Fraud

A dark-web identity kit pairs a forged document with a matched synthetic selfie image, with packages costing $50 to $500, to present a consistent but fraudulent identity. Shufti's NFC Verification reads the cryptographic chip embedded in ePassports and chip-enabled IDs, data that a purchased kit cannot reproduce. Document Verification forensic checks confirm template integrity and field consistency independently of the chip read. A kit that passes the image check fails the chip read; both layers must be defeated simultaneously, which pre-packaged kits cannot do.

Synthetic Identity at KYC

A blended identity using a real national insurance number combined with a fabricated name and address is submitted at the KYC step to pass basic format validation. Shufti's eIDV cross-references each field independently: the NI number may exist, but the name attached to it finds no matching record in government or bureau data. Document Verification confirms that the submitted ID matches the declared identity on every field, not just the document number. A mismatch between the real identifier and the fabricated surrounding data surfaces at this stage, not at manual review.

Business Ownership Concealment

A criminal beneficial owner uses nominee directors and a layered corporate structure to hide behind a seemingly legitimate entity at KYB. Shufti's Business Verification maps the full ownership chain to the ultimate beneficial owner, regardless of how many intermediate entities are stacked between the surface and the real owner. AML Screening then runs against every UBO individually. A sanctioned individual cannot hide behind a clean-named nominee at the top of the structure. Due Diligence surfaces adverse media and PEP connections that the nominee arrangement is designed to conceal.

Risk Screening

Adverse Media Concealment

A customer with a criminal history in local-language publications passes initial screening because English-only AML tools return no results for them. Shufti's AML Screening covers 50,000+ adverse media sources in 80+ languages, with automated severity classification that separates financial crime coverage from irrelevant mentions of the same name. Due Diligence extends the search to the customer's associates and connected entities. A clean individual record does not offset a flagged record among close associates, and a clean English-language profile does not produce a clean overall result.

High-Risk Jurisdiction Misrepresentation

A user based in a sanctioned or high-risk country declares a different residence address and uses a VPN to make their device location appear to match. Shufti's Address Verification cross-references the declared address against independent data sources. A fabricated address finds no matching electronic footprint in bureau or government records. eIDV confirms whether the identity's known data footprint is consistent with the claimed jurisdiction. Device Fingerprinting flags VPN signatures and IP-to-location mismatches that the declared address cannot explain away.

PEP or Sanctioned Person Onboarding

A politically exposed or sanctioned individual attempts to onboard using an alias, a transliterated name variant, or a slightly altered date of birth to avoid watchlist matches. Shufti's AML Screening applies fuzzy matching across 80+ languages against 4,000+ watchlists and 215+ sanctions regimes, capturing name variants that exact-match tools miss entirely. All four PEP tiers are screened, including close associates and family members who may be acting on the PEP's behalf. A single character change in a name does not produce a clean screening result.

Beneficial Owner Sanctions Concealment

A sanctioned individual hides behind nominees, trusts, and a multi-layer corporate structure specifically built to obscure their beneficial ownership at the point of screening. Shufti's Business Verification resolves the full ownership chain to the ultimate beneficial owner, regardless of how many intermediate layers are involved. AML Screening then runs against each UBO independently. The sanctioned individual cannot shelter behind a clean-named nominee at the surface level. Due Diligence adds adverse media and PEP checks across the full resolved ownership chain.

Mule Recruitment Onboarding

A genuine person, recruited via a fake job offer or romance scam, opens an account that will later be used to receive and forward illicit funds without fully understanding their role. Shufti's Behavioural Biometrics flags application patterns consistent with coached or scripted form completion. The pacing, field navigation, and hesitation patterns of a coached applicant differ measurably from someone acting spontaneously. The Fraud Hub cross-references device and application signals against known mule-recruitment typologies. AML Screening catches associated accounts if the recruitment network has operated elsewhere on the platform..

Source of Funds Misrepresentation

A customer submits fabricated payslips or bank statements to support a false income declaration and access higher deposit or credit limits. Shufti's Document Verification runs forensic checks on supporting documents, with fonts, template integrity, and metadata inconsistencies serving as reliable indicators of fabrication. eIDV cross-references declared income and employment data against independent sources where available. A fabricated document with no matching electronic income footprint fails both defensible checks before the application reaches a credit or limit decision.

Fund Account

Money Mule Deposit

A customer receives third-party funds from a criminal network, deposits them, and then forwards them onward, converting the account into a layering node in a money laundering chain. Shufti's Transaction Monitoring detects third-party funding patterns: source account characteristics, deposit velocity, and the rapid outbound transfer sequence that distinguishes mule activity from normal account use. Perpetual KYC updates the customer's risk score dynamically when the funding pattern diverges from their declared source of funds. The Fraud Hub surfaces the account as part of a wider mule ring if linked devices or identities appear across multiple accounts.

Stolen Card / CNP Fraud

An attacker uses stolen credit card details to fund a fintech account before rapidly converting the balance and initiating a withdrawal. Shufti's Device Fingerprinting flags devices associated with prior card fraud attempts across the platform, preventing the account from passing the funding step on a known-bad device. Transaction Monitoring detects the rapid deposit-to-withdrawal sequence, a pattern that distinguishes card-funded fraud from normal account activity. A hold is applied before the withdrawal executes, giving the compliance team time to investigate.

Chargeback Fraud

A user funds the account with their own card, moves the balance elsewhere, then files a chargeback claiming the original deposit was unauthorised. Shufti's Consent Verification creates a cryptographic record at the moment of funding, linking the verified account holder to that specific deposit transaction. When the chargeback is filed, the record demonstrates that the genuine card holder authorised the transaction and cannot credibly claim otherwise. The grounds for the dispute are documented before the chargeback request ever reaches the issuer.

Structuring / Smurfing

A customer makes repeated deposits just below AML reporting thresholds, such as £9,500, £9,700, and £9,200, across multiple sessions to avoid triggering any single alert. Shufti's Transaction Monitoring aggregates deposit history across configurable time windows, making the sub-threshold pattern visible at the account level in a way that single-transaction monitoring cannot. AML Screening flags the account against structuring typologies. The Fraud Hub escalates for review before the total laundered amount reaches the withdrawal stage.

APP Fraud Deposit

A genuine customer is deceived through an investment scam, impersonation call, or romance relationship into authorising a large inbound transfer they believe serves a legitimate purpose. Shufti's Transaction Monitoring flags anomalous inbound patterns: first-time high-value deposits that are inconsistent with the account's established risk tier and transaction history. Behavioural Biometrics detects interaction patterns consistent with external instruction, since a user being coached on a phone call behaves measurably differently from one acting independently. Consent Verification can confirm the user's stated intent before the transaction settles.

Inbound Sanctioned Source

A customer receives funds from an account or entity linked to sanctions, organised crime, or ransomware, whether or not the customer is aware of the source. Shufti's AML Screening checks every inbound transfer against live sanctions lists, adverse media databases, and known illicit source profiles before the funds settle. The check runs at the moment of transfer, not in a batch process, giving the platform the option to hold or reject before the money becomes available in the account. Every match result is cryptographically recorded as part of the tamper-evident audit trail.

Log In

Credential Stuffing

An attacker runs billions of leaked username and password combinations against the login endpoint, relying on the high rate of password reuse across consumer platforms. Shufti's Biometric Face Authentication requires a live biometric match to the enrolled KYC face. Stolen credentials alone cannot authenticate a session, because credentials without a matching live face produce nothing actionable. Device Fingerprinting flags login attempts originating from infrastructure associated with credential-stuffing campaigns. MFA adds a time-bound TOTP code layer that the attacker cannot generate without physical access to the account holder's authenticator app.

SIM Swap / 2FA Bypass

An attacker social-engineers the mobile carrier into redirecting the victim's phone number, then uses it to intercept SMS-based 2FA codes and take over the account. Shufti's MFA uses TOTP authenticator apps that generate time-bound codes independently of the phone network. A SIM swap does not intercept TOTP codes because they never travel over the phone network. Biometric Face Authentication requires a live selfie match to the KYC record for any high-risk post-login action, adding a biometric layer that phone-number compromise cannot defeat. The account remains protected even if the attacker has full control of the victim's number.

Session Hijacking

A stolen session token, extracted via malware or a phishing kit, allows an attacker to operate an authenticated account without going through a new login. Shufti's Behavioural Biometrics monitors interaction patterns continuously throughout the authenticated session, not just at login. Navigation cadence, field interaction patterns, and device handling change measurably when a different person takes over. Device Fingerprinting flags when the session continues from a new device or network without re-authentication. Any detected deviation triggers an immediate step-up verification requirement before the session continues.

Phishing / Adversary-in-the-Middle

A fake site proxies the real platform in real time, capturing credentials, OTPs, and session tokens as the genuine user enters them on what appears to be the legitimate login page. Shufti's Biometric Face Authentication is bound to the genuine SDK flow. A spoofed site cannot replicate the cryptographic handshake that the Shufti SDK performs at authentication. Fast ID authenticates the returning user against their enrolled biometric rather than a reusable password, so there are no static credentials for a proxy site to capture. The phishing site receives nothing it can use.

MFA Fatigue / Bombing

An attacker floods the victim with repeated MFA push notification requests until exhaustion or confusion causes the victim to accept one, granting the attacker account access. Shufti's MFA uses TOTP codes that the attacker cannot generate. Push notification bombing is not possible in a TOTP flow because no push notification is sent. Behavioural Biometrics detects unusual approval events: a prompt accepted without preceding user-initiated interaction is flagged immediately. The account is held pending step-up verification before any session continues.

RAT / Scam-in-Progress

A criminal remotely controls the victim's device, or instructs the victim over a phone call in real time, directing them to authorise transactions they believe are legitimate while the account is active and authenticated. Shufti's Behavioural Biometrics detects the cadence shift between a user acting independently and one responding to external instruction. Timing, sequence, and hesitation patterns differ measurably from the account's established baseline. Consent Verification confirms the user's genuine intent before any high-value action completes. Sessions flagged as potentially coerced are held for review before the transaction clears.

Make Payments

Authorised Push Payment Fraud

A customer is deceived by an impersonation scam, fake investment opportunity, or fraudulent emergency into authorising a large transfer to an account controlled by a criminal. Shufti's Transaction Monitoring flags anomalous outbound patterns: first-time payees, transfer amounts that diverge from the account's established baseline, and high-value single transactions inconsistent with the customer's risk tier. Behavioural Biometrics detects the interaction signatures of a user under external instruction. The timing and review patterns of a coached transfer differ measurably from an independent one. Consent Verification creates a cryptographically linked intent record at the moment of authorisation, providing an evidence basis for regulatory reporting.

Invoice Redirection / Vendor Fraud

A genuine invoice is intercepted and reissued with the fraudster's bank account details, directing a legitimate B2B payment to the wrong destination without the payer realising. Shufti's Consent Verification confirms the payee account against the verified identity of the intended recipient before the transfer is authorised. Transaction Monitoring flags payee additions or changes that occur immediately before a high-value transfer, a pattern consistent with invoice redirection. A mismatch between the expected and actual payee triggers a hold before funds move.

Romance / Investment Scam Exit Rail

A fintech account or bank transfer is used as the exit rail for a long-form social engineering scam. The customer believes they are investing in a legitimate opportunity after weeks or months of relationship building. Shufti's Transaction Monitoring flags the anomalous outbound pattern: rapid escalation in transfer size, first-time high-value payees, and transfer timing that is inconsistent with the account's history. The Fraud Hub surfaces the behavioural signals, including increased transfer frequency, new payee addition, and large single transactions, that together indicate the account has entered a scam-facilitated transfer pattern. A step-up review requirement is applied before the transfer completes.

Money Laundering: Layering

Illicit funds move through rapid multi-hop transfers, account to account and platform to platform, to obscure their origin before extraction at the other end. Shufti's Transaction Monitoring maps the full transaction chain and flags circular flows and rapid multi-hop sequences that distinguish layering from normal payment behaviour. AML Screening checks every outbound destination against sanctions and adverse media databases in real time, not in overnight batches. The Fraud Hub aggregates signals across the platform to surface coordinated layering networks, not just the individual accounts within them.

Sending to Sanctioned Entity

A customer attempts to transfer funds to an OFAC-listed or globally sanctioned account, whether intentionally or because the payee's details have been manipulated through invoice fraud or phishing. Shufti's AML Screening checks every outbound destination against live sanctions databases before the transfer executes, covering OFAC SDN, EU Consolidated List, UK HM Treasury Financial Sanctions, UN Security Council lists, and 215+ additional regimes. The transfer is blocked before any funds move, and the screening result is recorded in the tamper-evident audit trail. The compliance team receives an immediate alert with the matching sanction record.

Structured Outbound Transfer

High-value outbound payments are deliberately split into sub-threshold transactions, each just below the reporting threshold, spread across multiple sessions to avoid triggering any single monitoring rule. Shufti's Transaction Monitoring aggregates outbound transaction history across configurable time windows, making the sub-threshold splitting pattern visible at the account level where individual transaction monitoring cannot detect it. The Fraud Hub flags the account when the aggregate outbound pattern matches structuring typologies. A manual review hold is applied before the next transaction in the sequence clears.

Apply for Credit

Application / Loan Fraud

A fraudster submits false income, employment status, or address data to qualify for a credit or BNPL product they would not legitimately be approved for. Shufti's eIDV cross-references every declared field against authoritative government and bureau records. A fabricated address or inflated income figure finds no matching electronic footprint and fails immediately. Document Verification runs forensic checks on supporting documents, detecting font inconsistencies, metadata anomalies, and template mismatches that are reliable indicators of fabrication. The application fails at the point of submission, not at the manual review stage.

Loan Stacking

The same applicant submits credit applications to multiple lenders simultaneously, before any bureau reporting catches up, to accumulate far more credit than any single lender would approve. Shufti's eIDV and Device Fingerprinting link the applications by identity and device signals across the platform in real time, surfacing the multi-application pattern before any single application completes the approval process. The Fraud Hub flags rapid multi-application velocity, specifically the same identity or device appearing in multiple credit flows within a short window. A hold is applied across all active applications while the pattern is reviewed.

Bust-Out Fraud

A customer builds a seemingly legitimate profile over weeks or months, then draws down all available credit across every product simultaneously and disappears before repayment is due. Shufti's Transaction Monitoring monitors account behaviour continuously. A sudden drawdown to limit across multiple products, followed by a rapid withdrawal or transfer, triggers an immediate alert before the cycle completes. Perpetual KYC tracks the drift between the customer's declared profile and their actual behaviour, surfacing inconsistencies that a point-in-time assessment would miss. The Fraud Hub links the account to prior bust-out patterns if the same device or identity signals have appeared in previous incidents.

Synthetic Identity for Credit

A blended identity built from a real NI number and fabricated personal details applies for credit products with the intention of defaulting after extraction. Shufti's eIDV detects the mismatch between the real identifier and the fabricated surrounding data. The name finds no electronic footprint, and the address resolves to nothing in authoritative records. Document Verification confirms that submitted ID documents match the declared identity on every field, not just the document number. A synthetic identity fails both checks before reaching a credit decision engine.

Suitability Misrepresentation

A customer overstates income, financial experience, or risk tolerance on an application to access credit products or investment tiers they do not qualify for. Shufti's Document Verification runs forensic checks on supporting financial documents. Fabricated payslips and bank statements fail on font, metadata, and template integrity grounds reliably. eIDV cross-references declared data against bureau records where available, surfacing discrepancies between what is declared and what the identity's known footprint supports. A declared income figure with no matching independent record triggers a review before the application proceeds.

Velocity / Anomaly Attack

A coordinated group submits rapid sequences of similar credit applications, often under slightly varying identities, to overwhelm manual review queues and create pressure for approvals. Shufti's Device Fingerprinting links applications by shared hardware and infrastructure across the platform in real time. Behavioural Biometrics detects the scripted application pattern, with identical field navigation and identical timing intervals distinguishing an automated attack from genuine individual applicants. The Fraud Hub surfaces the coordinated nature of the attack in a single case view rather than as a series of unconnected individual flags.

Account Maintenance

Password Reset Account Takeover

An attacker compromises the victim's email address or mobile number, via SIM swap, phishing, or credential stuffing, and uses the password reset flow to lock the genuine user out and take control. Shufti's Biometric Face Authentication requires a live selfie matched to the KYC record before any password reset completes. An email or phone compromise alone cannot unlock this step. MFA using TOTP ensures the reset flow does not depend on a phone number that can be diverted to the attacker. Device Fingerprinting flags when the reset request comes from an unrecognised device or network, triggering an additional hold.

Fraudulent Payment Destination Added

An attacker who has gained partial access to an account immediately adds their own bank account as a withdrawal destination before the genuine user notices the breach. Shufti's Biometric Face Authentication requires a live biometric match before any new payout destination is saved. The attacker cannot complete this step without the genuine account holder's enrolled face. Device Fingerprinting flags when a new destination addition originates from an unrecognised device or network. The step-up requirement ensures that a partial credential compromise cannot result in fund diversion, regardless of what else the attacker knows.

Identity Detail Change to Evade Screening

A customer who has received an AML flag attempts to alter their registered name or date of birth, intending to appear as a new, unscreened identity to the monitoring system. Shufti's AML Screening re-screens the account automatically whenever core identity fields are changed. The new values are checked against watchlists and adverse media in the same run as any new customer. Document Verification confirms that any new identity documents match the original enrolled biometric, not just the updated field. An altered name that clears a name check still fails the face match against the original KYC record.

Continuous Session Takeover

A stolen session token, extracted after the original authentication, allows an attacker to modify account settings and extract data across an extended session without triggering a new login event. Shufti's Behavioural Biometrics monitors interaction patterns across the full authenticated session, not just at login. Navigation cadence, field interaction patterns, and device handling change measurably when a different person takes over. Device Fingerprinting flags when session activity continues from different hardware or a new network. Any detected deviation triggers an immediate re-authentication requirement before the session continues.

Support Social Engineering

An attacker calls the support channel with the victim's PII, including name, address, mother's maiden name, and date of birth, and uses it to convince an agent to change account details or raise limits. Shufti's Biometric Face Authentication requires a live biometric match before any account-level change is applied. No amount of PII knowledge can substitute for the genuine account holder's enrolled face. Fast ID allows the genuine account holder to re-authenticate themselves quickly if they initiate the request directly. A successful social engineering conversation produces no account change without the biometric confirmation step.

Phishing for Settings Change

A fake customer service communication, via SMS, email, or in-app message, directs the user to a spoofed page designed to capture credentials and then make account changes in the background. Shufti's Biometric Face Authentication is bound to the genuine SDK flow. A spoofed site cannot replicate the cryptographic handshake required to trigger a validated settings change. Behavioural Biometrics flags any settings-change session that does not match the account holder's normal interaction pattern for that type of action. The credentials captured by the phishing page are useless without the biometric layer that the SDK enforces.

Upgrade

Fake Documents for Higher Tier

A customer submits a forged passport or fabricated utility bill to unlock higher transaction limits without meeting the genuine verification requirements for that tier. Shufti's Document Verification runs the same forensic checks at tier upgrade as at initial onboarding. Template integrity, font consistency, MRZ validation, and AI-generated artefact detection all apply regardless of when the document is submitted. NFC Verification reads the cryptographic chip in the submitted ID. A purchased fake has no working chip and fails the chip read immediately. The document face must also match the biometric enrolled at original sign-up; a document change cannot substitute a new identity.

Address Fraud for Tier Upgrade

A fabricated utility bill is submitted as proof of address to move into a lower-risk jurisdiction tier with higher limits or reduced ongoing verification requirements. Shufti's Address Verification cross-references the declared address against independent data sources. A fabricated bill has no matching electronic footprint in bureau or government records, regardless of how convincing it looks as an image. Document Verification checks the utility bill's template against known issuer templates, flagging inconsistencies in fonts, logos, and layout that indicate fabrication. A document that passes the visual check still fails the independent data cross-reference.

Support Social Engineering for Limit Increase

An attacker impersonates the account holder in a support interaction, using PII gathered from a data breach or social engineering, to request a limit increase without going through formal re-verification. Shufti's Biometric Face Authentication requires a live selfie matched to the KYC record before any limit change is applied. The support channel cannot override this requirement. Fast ID allows the genuine account holder to complete this step themselves in under 30 seconds if they initiate the request. No quantity of PII knowledge bypasses the biometric requirement.

Deepfake at Re-Verification

An attacker generates a synthetic face video to present at the biometric step required for a limit upgrade, attempting to pass as the genuine account holder. Shufti's Face Verification at iBETA Level 3, the highest independent PAD certification available with 0% APCER and 0% BPCER, applies 3D depth mapping, micro-movement analysis, and injection detection simultaneously. The system rejects synthetic video, 3D masks, and camera-injected media at the hardware layer before any face comparison runs. A deepfake cannot pass all three detection layers in a single session.

Suitability Misrepresentation for Credit Tier

A customer inflates their declared income or financial position in order to move into a higher credit tier or access a lower-rate product they do not qualify for. Shufti's Document Verification forensic checks surface fabricated payslips and bank statements through font, metadata, and template integrity analysis that the human eye would miss. eIDV cross-references declared income and employment data against independent records where available. A declared financial position with no supporting electronic footprint triggers a review before the tier change is approved.

Jurisdiction Fraud for Lower-Risk Tier

A user misrepresents their location, using a VPN or fabricated address documents, to shift into a jurisdiction tier with lower verification requirements or higher transaction limits. Shufti's Address Verification cross-references the declared address against bureau and government data independently of the submitted document. Device Fingerprinting flags VPN usage and IP-to-location mismatches that contradict the declared jurisdiction. eIDV confirms whether the identity's known data footprint is consistent with the claimed location across all three data sources simultaneously.

Periodic Review

Sanctions Re-Listing Not Caught

A customer who passed all onboarding checks is subsequently added to a global sanctions list, but the platform's annual review cycle means weeks or months pass before the change is detected. Shufti's Ongoing AML Screening re-screens continuously against live sanctions databases. A new designation triggers an alert within the same session it appears, not at the next scheduled annual review. Perpetual KYC updates the customer's risk profile automatically when the AML status changes, and the compliance team receives an immediate alert. No further transactions are processed before the alert is reviewed.

Risk Profile Drift

A customer's transaction behaviour gradually shifts toward high-risk patterns over months, including increasing transfer volumes, new high-risk payees, and undeclared jurisdiction changes, without the risk assessment reflecting any of it. Shufti's Perpetual KYC monitors behavioural signals continuously and updates the customer's risk score dynamically rather than at a fixed annual review date. Transaction Monitoring tracks the drift in payment behaviour over time, surfacing the pattern before it reaches a threshold that should have triggered enhanced due diligence months earlier. An automatic EDD requirement is applied when the risk score crosses the configured threshold.

Periodic Review Evasion

A customer who knows the schedule of periodic reviews temporarily suppresses suspicious activity in the weeks before review, then resumes after the review is marked clean. Shufti's Perpetual KYC is event-driven rather than calendar-driven. It evaluates the full account history continuously, not just the recent window before a scheduled review. A customer who suppresses activity for four weeks does not reset their risk score; the suppression period itself becomes a signal in the full behavioural record. The complete transaction and risk history is available at review time, not just the most recent period.

Identity Swap at Re-Verification

A customer presents different identity documents at the re-KYC step, claiming the original ID was lost or expired, intending to effectively replace their identity on record with someone else's. Shufti's Biometric Face Authentication requires the current selfie to match the biometric enrolled at original onboarding, regardless of what new documents are submitted alongside it. Face Verification at iBETA Level 3 ensures the biometric match cannot be defeated by a deepfake substitution at the re-verification stage. A new document set that fails the face match against the original enrolled biometric triggers immediate escalation, not re-enrollment.

Aged Synthetic Identity Unmasked

A synthetic identity cultivated over months through small deposits and a growing transaction history passes initial and subsequent periodic checks before attempting a large-value extraction at the point the attacker judges it safe. Shufti's eIDV continues cross-referencing the identity against authoritative data sources at each review point. Perpetual KYC tracks the drift between the customer's transaction behaviour and their declared profile. An identity that was credible at onboarding becomes inconsistent as the fabricated data footprint fails to develop the way a real person's financial life would. The extraction attempt triggers an immediate hold.

Re-emerging Adverse Media

A customer with a clean record at onboarding is later linked to financial crime in news published after their account was opened, including enforcement actions, fraud allegations, or investigations that did not exist at the time of onboarding. Shufti's Ongoing AML Screening monitors 50,000+ adverse media sources in 80+ languages continuously, not just at the point of onboarding or scheduled review. A new adverse media match triggers a real-time alert rather than waiting for the next review cycle. The alert is linked to the customer's existing risk record and presented to the compliance team with a severity classification and source reference.

Close Account

Pre-SAR Closure

A customer under compliance investigation requests account closure and data erasure simultaneously, attempting to destroy the transaction and identity evidence trail before a SAR is filed. Shufti's Transaction Monitoring and Ongoing AML Screening run a final history review before any closure is processed. A pending flag prevents the account from moving into a closed state. Regulatory retention obligations under AMLD6 and the Proceeds of Crime Act override erasure requests; a closure request does not delete records that must be legally retained. AML Screening confirms whether an open investigation flag applies before the closure is approved.

Balance Extraction Before Closure

A customer withdraws the full account balance immediately after receiving a compliance communication, then submits a closure request to pre-empt any asset freeze that might follow. Shufti's Transaction Monitoring flags full-balance withdrawal events that follow compliance-triggered communications. This sequence is a recognised typology for pre-closure extraction. Biometric Face Authentication confirms that the withdrawal was authorised by the genuine account holder and not by an attacker who triggered the compliance alert. An automatic hold is applied to the closure request while the withdrawal is reviewed.

Re-Application Under New Identity

An offboarded customer applies for a new account using different documents, such as a sibling's ID, a forged passport, or a newly acquired identity, assuming the platform cannot link the new application to the closed account. Shufti's 1:N Facial Deduplication screens every new applicant's selfie against all previous accounts, including deactivated and closed ones. The same face cannot create a new account regardless of what documents are presented with it. AML Screening cross-references the new application against the closed account's risk record. The link is surfaced before the new application reaches the identity verification step.

GDPR Erasure to Destroy Evidence

A customer invokes their right to erasure under GDPR Article 17 at the point of account closure, targeting transaction records and identity data that would support a fraud or AML investigation. Shufti's system enforces the Article 17(3)(b) exemption. Records subject to AML, anti-fraud, or regulatory retention obligations are not erasable on customer request during the legally mandated retention period. The request is logged and responded to with the applicable legal basis, creating an audit record of the erasure attempt itself. Retained records remain available for law enforcement or supervisory access throughout the retention period.

Chargeback Cascade at Closure

A customer disputes every card-funded transaction at account closure, claiming all were unauthorised, after having already moved or spent the funds through conversion or transfer. Shufti's Consent Verification creates a cryptographic record at the moment of every card-funded transaction, linking the verified account holder to each specific authorised payment. When the chargeback cascade is filed, the platform has a timestamped, verifiable consent record for each disputed transaction. The grounds for each individual dispute are documented before any chargeback reaches the issuer.

Coordinated Account Closure Ring

Multiple linked accounts close simultaneously, after a fraud scheme completes, to reduce the investigable footprint and make it harder to reconstruct the network or recover proceeds. Shufti's Fraud Hub monitors for coordinated account activity across the platform, flagging simultaneous closure requests from accounts that share device signals, identity connections, or transaction flows. 1:N Facial Deduplication links accounts that used the same face across different registered identities. AML Screening runs a final check across all accounts in the ring before any records are marked closed.

Built For Every Role That Owns The Compliance Decision

Combine products across identity, compliance, and fraud defence to build a verification stack that meets your regulatory requirements, without rebuilding the integration each time the rulebook changes.

Compliance Officer

One audit trail per user, one evidence export per exam. Risk-tier logic, DORA-compliant vendor documentation, and AMLD6-ready CDD records are all accessible without switching portals.

Head of Product

Configure verification depth by risk tier and geography. Localised pass-rate data and a no-code workflow builder let you optimise conversion before you launch in a new market.

Head of Engineering

One REST API for the full user lifecycle. SDKs for web and mobile. Sandbox access in minutes. SOC 2 Type II and DORA register-of-information documentation available on request.

Fraud Analyst

A unified Fraud Hub surfaces every signal across device, behavioural, identity, and transaction data in one case view. See why a flag fired before the case is opened.

Don’t just take our word for it, hear from our customers

The Confidence Our Clients Share

The future of digital identity is defined by trust, interoperability, and regulatory alignment, so our partnership with Shufti reinforces DevCode Identity’s commitment to supporting our global customers with the most secure, best-in-class, compliant identity verification solutions available today.

Combining our Conversion Driven Compliance Orchestration Platform with Shufti’s global KYC and IDV capabilities allows our customers not only to navigate complex regulatory demands but also to maintain a seamless customer onboarding experience with the highest achievable conversion rates.

We’re proud to continue our partnership with Shufti as we expand into new jurisdictions.

Shufti’s verification technology not only strengthens our compliance framework but also ensures our players enjoy a smooth, secure onboarding experience.

We aim to offer our clients and their traders the very best tools with which to do their jobs, we’re excited to be able to work with Shufti.

They’re a leading company, and we’re looking forward to offering their solutions to our clients through our CRM.

The relationship with Shufti was born out of frustration with an existing provider, so we started our discussion with Shufti.

The response time was excellent, from the start of speaking to sales to getting up and running with the demo.

Everything you need to know in one place

Frequently Asked Questions

UK-authorised fintechs operate under FCA Consumer Duty (in force July 2023), PSD2 Strong Customer Authentication, and the AMLD6/AMLR framework (general transposition deadline 10 July 2027). DORA, in force since 17 January 2025, adds resilience and incident-reporting obligations for every ICT vendor in the stack. Shufti maintains compliance rule sets across 240+ countries actively processed.

The risk-tiered onboarding flow supports configurable vulnerability-indicator flags during the verification step, producing a per-customer Consumer Duty record aligned with the FCA/ICO Joint Statement. The record is exportable for supervisory review without additional vendor data calls.

ISO/IEC 30107-3 PAD Level 3 is the highest independent certification tier for biometric liveness. iBETA tested Shufti's system against presentation attacks, video replay, deepfake injection, and 3D masks at the most demanding tier in the standard. Shufti is the first European vendor to achieve Level 3 with 0% APCER and 0% BPCER on both iOS and Android.

DORA requires regulated entities to document every critical ICT provider, with contractual clauses covering resilience, incident notification, audit rights, and exit strategy. Shufti provides a register-of-information pack including SOC 2 Type II, ISO 27001, BCP/DR documentation, incident-notification SLA, and a sub-processor list, available on request.

Sandbox access is immediate. The single REST API covers document verification, biometric liveness, eIDV, AML screening, and transaction monitoring in one integration. Average production deployment runs 2 to 8 weeks depending on scope.

Yes. Shufti processes verification data on behalf of the client and holds no ownership claim over it. The Article 28-compliant DPA, sub-processor list, EU and UK data residency options, and deletion certificate capability are provided at contract stage.

Evaluate Shufti Against Your Current Fintech Compliance Stack

FCA Consumer Duty, DORA, and AMLD6 require a verification architecture that connects onboarding identity to ongoing transaction monitoring and produces a single audit trail. Point-solution stacks cannot do that from a shared record. Evaluate whether your current stack