Face Verification

Face Verification

Address Verification

Address Verification

Document Verification

Document Verification

Age Verification

Age Verification

VideoIdent

VideoIdent

Fast ID

Fast ID

Docless Verification

Docless Verification

Consent Verification

Consent Verification

NFC Verification

NFC Verification

Business Verification

Business Verification

Due Diligence

Due Diligence

Investor Verification

Investor Verification

E-Signature

E-Signature

QES

QES

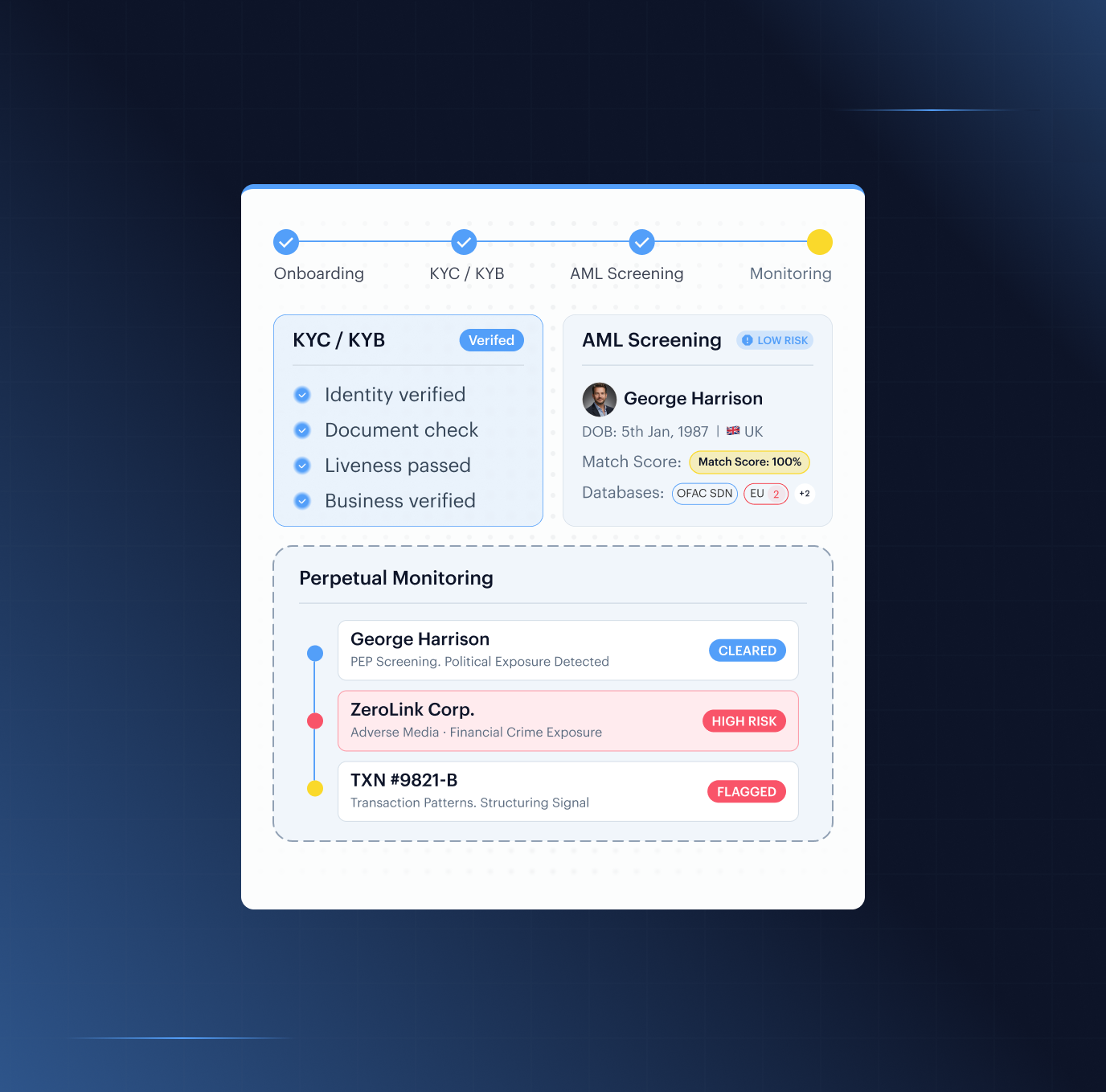

AML Screening

AML Screening

Transaction Monitoring

Transaction Monitoring

Adverse Media

Adverse Media

Business AML Screening

Business AML Screening

PEP & RCA

PEP & RCA

Sanctions

Sanctions

Watchlist

Watchlist

Behavioural Biometrics

Behavioural Biometrics

Device Fingerprinting

Device Fingerprinting

Biometric Face Authentication

Biometric Face Authentication

MFA

MFA

Fraud Hub

Fraud Hub

Onboarding

Onboarding

Ongoing Monitoring

Ongoing Monitoring

KYC

KYC

KYB

KYB

KYI

KYI

Age Assurance

Age Assurance

Identity Verification

Identity Verification

Workforce IAM

Workforce IAM

Candidate Verification

Candidate Verification

Compliance

Compliance

Fraud prevention

Fraud prevention

Trust & safety

Trust & safety

Global expansion

Global expansion

Product Managers

Product Managers

Compliance Officers

Compliance Officers

Fraud Analysts

Fraud Analysts

Developers

Developers

Deepfake Detection

Deepfake Detection

Bonus Abuse / Promotion Abuse

Bonus Abuse / Promotion Abuse

Account Takeover

Account Takeover

Synthetic Identity Fraud

Synthetic Identity Fraud

Document Fraud

Document Fraud

Impersonation Fraud

Impersonation Fraud

Multi-Accounting

Multi-Accounting

Fraud Networks

Fraud Networks

Chargeback Fraud

Chargeback Fraud

Money Mule Activity

Money Mule Activity

Party Fraud

Party Fraud

Regulatory & Compliance Risks

Regulatory & Compliance Risks

Fintech

Fintech

Crypto

Crypto

iGaming

iGaming

Forex

Forex

Social Network

Social Network

Marketplace

Marketplace

Banking

Banking

Gig Economy

Gig Economy

Payments

Payments

Ride Hailing

Ride Hailing

Adult Content

Adult Content

Blind Spot Audit

Blind Spot Audit

Deepfake Detector

Deepfake Detector

Liveness Spoofs

Liveness Spoofs

Document Originality

Document Originality

Document Deepfake

Document Deepfake

Global Trust Platform

Global Trust Platform

Journey Builder

Journey Builder

Case Management

Case Management

Shufti AI

Shufti AI

Fraud Analytics

Fraud Analytics

Vendor Comparison

Vendor Comparison

Brand Personalisation

Brand Personalisation

AI Compliance Co-Pilot

AI Compliance Co-Pilot

OCR

OCR

Secure Capture

Secure Capture

Deployment Options

Deployment Options

Identity Methods

Identity Methods

API Documentation

API Documentation

Mobile SDKs

Mobile SDKs

Service Status

Service Status

Help Center

Help Center

Contact Us

Contact Us

Technical Support

Technical Support

Supported Documents

Supported Documents

Supported Countries

Supported Countries

Content library

Content library

Blogs

Blogs

News

News

Reports

Reports

Insights

Insights

Knowledgebase

Knowledgebase

ROI calculator

ROI calculator

About

About

Career

Career

Press Release

Press Release

Certifications

Certifications

Partnership

Partnership

Awards

Awards

Events & Webinar

Events & Webinar

Interactive Demo

Interactive Demo

Podcast Studio

Podcast Studio

Spotlight Studio

Spotlight Studio

Crypto & Web3

Secure the Entire Crypto Lifecycle with End-to-End Crypto Compliance

Verify users, monitor transactions, and stop fraud; all in one place. Shufti powers identity verification, fraud prevention, AML compliance, and transaction monitoring; purpose-built for exchanges, wallets, and DeFi platforms worldwide.

Proven Performance

Our Impact, By The Numbers

- <30sMedian Time-to-Decision

- 4,000+Watchlists Screened

- 240+Countries Actively Processed

Trusted by Leading Digital Enterprises Worldwide

COMPLIANCE WITHOUT COMPROMISE

Why Crypto Platforms Choose Shufti

-

Stay Ahead of Regulation

MiCA enforcement is underway. FATF’s Travel Rule now applies to every VASP processing above-threshold transfers. Shufti’s AML rule sets and jurisdiction coverage update continuously; so your compliance posture keeps pace with regulatory change without engineering intervention.

-

Stop Fraud Before It Onboards

The Deloitte Center for Financial Services warns that generative AI fraud losses could grow to $40 billion by 2027 if adaptive defenses remain undeployed. Shufti’s iBETA Level 3-certified liveness detection and device intelligence intercept sophisticated fraud at first contact; before a fraudulent account is ever created.

-

Onboard Without Losing Users

A median decision time under 30 seconds across 240+ countries actively processed means legitimate users clear verification before they consider abandoning. Risk-tier configuration lets low-risk users move faster without compromising checks on high-risk segments.

Secure Every Stage of the Crypto User Lifecycle

Sign Up

Bot Account Farming

A bot operator floods a DEX airdrop campaign with thousands of wallets, each tied to a burner email and seeded with just enough gas to look active. Shufti's proprietary Device Fingerprinting exposes the shared emulator stack and proxy infrastructure, while Behavioural Biometrics flags machine-speed registrations with zero dwell time and no human signature.

Synthetic Identity

A fraudster pairs stolen PII with a generated wallet address and disposable email to pass basic format checks. Shufti's eIDV cross-references the identity against government, telco, and credit bureau databases simultaneously. A synthetic identity leaves no consistent footprint across all three, and the account never opens.

Multi-Accounting

A user registers multiple accounts under different IDs to stack airdrop allocations or stay under per-account trading limits. Shufti's 1:N Facial Deduplication continuously runs every new selfie against the fully verified user base, surfacing the same face regardless of which documents were presented.

Stolen Identity Registration

A fraudster buys breached crypto credentials, pairs them with their own contact details, and registers so all communications route to the attacker. Shufti's eIDV flags the contact mismatch. Face Verification then independently confirms the live face does not match the document holder.

Verify Identity (KYC)

Document Forgery

A user submits a dark-web passport template or a real document with a photo swap to pass KYC on a crypto exchange. Shufti's Document Verification runs forensic tamper detection, MRZ checks, and security-feature validation across any government-issued document. For e-passports, NFC Verification reads the chip directly, and a forged document has no working cryptographic signature.

Deepfake / AI Face Attack

An attacker routes AI-generated deepfake video through virtual camera software into an exchange's selfie step. Shufti's Face Verification (iBETA L3) applies 3D depth mapping and skin-texture analysis that no synthetic deepfake can replicate. Injection Detection independently intercepts virtual camera drivers at the OS layer before capture begins.

Camera Injection Attack

An attacker replaces the live camera feed with a pre-recorded video or AI-generated image using a virtual camera driver, sending what looks like valid input to the liveness check. Shufti's Injection Detection validates at the OS layer that every frame comes from the hardware camera, any stream that can't be traced to a physical sensor is blocked before liveness processing begins.

Identity Pack Fraud

Crypto-focused dark-web shops sell KYC kits — forged government ID, matching synthetic selfie, and a clean email history, for $50 to $500, purpose-built for exchange onboarding. Shufti's NFC Verification immediately kills this attack: a purchased kit cannot include a working cryptographic chip, which is physically embedded in the original government-issued document. eIDV then confirms the identity carries a defensible real-world data footprint that no fabricated kit can replicate.

PEP or Sanctioned Person Onboarding

A sanctioned individual or PEP attempts to open a crypto trading account using a transliterated alias or close associate's identity to avoid direct name-match lists. Shufti's AML Screening covers 4,000+ watchlists and 215+ sanctions regimes with fuzzy matching and phonetic analysis across 80+ languages, all four PEP tiers are covered, with every match returning a consolidated confidence score and source citation.

Business Ownership Concealment

A crypto OTC desk or institutional trading firm registers using nominee directors and multi-layer offshore holding structures to hide a sanctioned beneficial owner behind a layer of legitimacy. Shufti's KYB maps the full ownership chain to the ultimate beneficial owner, intelligently AML-screens them individually, and triggers enhanced Due Diligence where the structure warrants it, before the account is activated.

Risk Screening

Adverse Media Concealment

A crypto trader with criminal history applies relying on English-only searches to miss local-language coverage. Shufti's AML Screening covers 50,000+ adverse media sources in 80+ languages, distinguishing allegations from convictions and surfacing regional coverage that narrow searches miss.

High-Risk Jurisdiction Misrepresentation

A user from a sanctioned or high-risk crypto jurisdiction declares a compliant country and routes via VPN to match. Shufti's Address Verification cross-references the declared address against independent data sources, while Device Fingerprinting flags VPN usage and IP-to-location mismatches.

Corporate Structure Evasion

A crypto corporate entity restructures mid-onboarding, inserting a clean nominee shareholder to hide a high-risk UBO from screening. Shufti's KYB cross-checks ownership claims against multiple independent registries, changes in registered ownership timed to a compliance query are flagged as evidence of evasion.

Log In

Credential Stuffing

An attacker runs a database of millions of leaked email-password pairs against an exchange's login endpoint, using residential proxies to sidestep rate limiting. Shufti’s Biometric Face Authentication requires a live selfie matched against the enrolled KYC biometric for any high-risk action. A valid password alone is not enough; stolen credentials are useless without the account holder’s live face.

SIM Swap / 2FA Bypass

An attacker calls a mobile carrier posing as the account holder and gets the victim's number transferred to an attacker-controlled SIM, rerouting all SMS 2FA codes within the hour. Shufti's TOTP-based MFA uses an authenticator app, not a phone number, so it cannot be hijacked via SIM swap. For withdrawals and sensitive actions, Biometric Face Authentication adds a biometric factor that no SIM swap can replicate.

Session Hijacking

An attacker steals a valid session cookie via infostealer malware and replays it to access an exchange account without triggering a new login. Shufti's Behavioural Biometrics tracks keystroke cadence, mouse movement, and navigation patterns, any abrupt shift flags a different operator and forces immediate re-authentication.

Phishing / Adversary-in-the-Middle

An attacker clones an exchange to proxy the real site and capture credentials and 2FA tokens in real time. Shufti's Biometric Face Authentication is bound to the genuine platform's verified SDK flow and can't be proxied by a lookalike domain, the live selfie must pass through the authenticated endpoint, making the phishing relay useless.

Deposit Money

Money Mule Deposit

A crypto money mule receives fiat from multiple third parties, deposits it on an exchange, converts to crypto, and sweeps to an external wallet, layering funds one hop at a time. Shufti's Transaction Monitoring flags the third-party funding pattern and rapid convert-and-transfer sequence, while Perpetual KYC escalates the risk score as mule behaviour accumulates.

Stolen Card / CNP Fraud

An attacker uses stolen card details to fund a crypto exchange account, converts to BTC or stablecoins, and withdraws before the cardholder spots the charge. Shufti's Transaction Monitoring flags the deposit-convert-withdraw velocity as anomalous against account history and peer benchmarks, catching the sequence before funds leave the platform.

Structuring / Smurfing

A user fragments a large crypto purchase into multiple deposits, each kept just below the reporting threshold and spread across several days, to avoid triggering an AML review. Shufti's Transaction Monitoring analyses behavioural patterns over time, not individual transactions. Consistent sub-threshold amounts, unusual deposit frequency, and coordinated patterns across linked accounts are flagged as structuring even when each individual deposit looks routine.

Inbound Sanctioned Wallet Deposit

A threat actor sends crypto from a wallet linked to ransomware payments, darknet markets, or OFAC-sanctioned entities to a clean, verified exchange account to begin layering. Shufti's AML Screening checks every inbound on-chain deposit against OFAC, global sanctions lists, and known illicit wallet databases in real time. Deposits from flagged addresses are blocked before the balance is credited to the account.

Chargeback Fraud

A user deposits via their own card, converts to BTC, sweeps to a self-custodied wallet, then files a chargeback claiming unauthorised use. Shufti's Transaction Monitoring identifies the buy-withdraw-dispute sequence and triggers automatic withdrawal holds until the card settlement window closes.

Buy / Trade

Wash Trading

A market-maker runs matched buy-sell orders between their own verified accounts to inflate reported volume on a low-liquidity token, boosting its ranking or unlocking volume-based fee rebates. Shufti's Transaction Monitoring detects circular trading flows netting near-zero P&L between accounts sharing device infrastructure. 1:N Facial Deduplication closes the loop by linking the accounts biometrically to a single operator.

Pump and Dump Coordination

A coordinated Telegram group uses multiple exchange accounts to accumulate a low-cap token, then collectively pumps its price through public promotion before dumping at the peak. Shufti's Fraud Hub surfaces the coordination signals: shared device infrastructure, concurrent registration timing, and correlated login behaviour across accounts that appear unrelated but trade in statistical synchrony.

Airdrop / Bonus Farming

A Sybil attacker spins up hundreds of exchange accounts, each performing the bare minimum qualifying trade volume or referral activity, to claim multiple shares of a token reward or referral pool. Shufti's 1:N Facial Deduplication ensures one verified face means one account, regardless of how many identities are presented. Device Fingerprinting links accounts sharing underlying device infrastructure across the entire attack cluster.

P2P Trade Scam

A buyer on a P2P crypto marketplace marks a payment as sent without transferring funds, or uses a reversible payment rail and cancels after the seller releases the crypto. Shufti's Transaction Monitoring flags accounts with abnormally high dispute rates and rapid trade-completion patterns that signal systematic exploitation of the escrow release window.

Withdraw / Send

Account Takeover Withdrawal

An attacker who took over an exchange account via stolen credentials immediately adds a new withdrawal address and attempts to drain all holdings before the legitimate owner reacts. Shufti's Biometric Face Authentication requires a live selfie matched to the enrolled KYC biometric before any withdrawal above a configured threshold. Knowing the password is not enough; the account holder's live face is the only key that opens the withdrawal.

Sending to Sanctioned Wallet

A user attempts to withdraw crypto to an OFAC-listed or globally sanctioned wallet address, either intentionally evading sanctions or unknowingly sending to a counterparty re-designated after the address was saved. Shufti’s AML Screening checks every destination wallet against live sanctions databases before the transfer executes. Transfers to sanctioned addresses are blocked, not flagged after the fact.

Rapid Cash-Out Scheme

An attacker deposits fraudulently obtained funds, converts to crypto, and withdraws in a tightly sequenced operation to clear the balance before any alert fires. Shufti's Transaction Monitoring flags anomalous deposit-to-withdrawal velocity, an immediate full-balance withdrawal following a first-ever deposit triggers an automatic hold pending review.

Withdrawal Address Manipulation

Clipboard-hijacking malware swaps a copied withdrawal address with the attacker's, often matching first and last characters to pass a quick visual check. Shufti's Biometric Face Authentication requires live biometric confirmation before any withdrawal address is added or changed; clipboard malware can substitute the address, but it cannot generate a matching live face.

Upgrade Limits

Fake Documents for Higher Tier

A verified user submits a forged passport or purchased proof of income to unlock a higher withdrawal tier on an exchange. Shufti's Document Verification applies the same forensic checks at upgrade as at onboarding, and Face Verification confirms the face presented matches the originally enrolled biometric.

Address Fraud for Tier Upgrade

A user submits a fabricated utility bill to shift their registered address to a lower-risk jurisdiction and unlock higher withdrawal limits. Shufti's Address Verification cross-references the declared address against utility registries, postal records, and credit bureau data, a fabricated document can't produce a matching footprint across all three.

Support Social Engineering

An attacker calls an exchange's support team impersonating the account holder, armed with scraped PII, to approve a tier upgrade. Shufti's Biometric Face Authentication requires the legitimate account holder to confirm any limit change with a live selfie matched to their enrolled biometric, no amount of PII knowledge substitutes for the face on file.

Account Maintenance

Password Reset Account Takeover

An attacker compromises the victim's email inbox or SIM-swaps their phone to intercept the password reset link, locking the real owner out of their exchange account. Shufti's Biometric Face Authentication requires a live selfie matched to the enrolled KYC biometric before account recovery completes, email or phone compromise alone is not enough.

Fraudulent Bank Account Addition

An attacker with partial account access adds their own bank account as a fiat off-ramp to redirect future withdrawals from an exchange. Shufti's Biometric Face Authentication gates the addition of any new payout destination, the password alone isn't enough without the account holder's live face.

Identity Detail Change to Evade Screening

A crypto user who received an AML flag submits a profile correction with a slightly altered name or adjusted date of birth, hoping to reset their risk status. Shufti triggers Document Verification and AML re-screening automatically whenever a core identity field is modified, profile edits don't reset the compliance record.

Continuous Session Takeover

An attacker exfiltrates a live session cookie to silently control an active exchange account, adding withdrawal addresses without triggering a re-login. Shufti's Behavioural Biometrics continuously monitors typing patterns, mouse movement, and navigation sequences, a sudden shift identifies a different operator and triggers immediate re-authentication mid-session.

Periodic Review

Sanctions Re-Listing Not Caught

A user passes onboarding cleanly but gets added to OFAC or UN sanctions lists months later, often linked to a crypto enforcement action. Shufti's Ongoing AML Screening re-checks every active customer against live databases on a configurable schedule, triggering immediate alerts before further trades are processed.

Risk Profile Drift

A retail crypto user who onboarded as low-risk gradually migrates to institutional-scale volumes and high-risk counterparty wallets, but their risk classification stays unchanged. Shufti's Perpetual KYC monitors on-chain and platform signals continuously, when a score crosses a configured threshold, enhanced due diligence fires automatically, not at the next scheduled review.

Periodic Review Evasion

A high-risk crypto trader goes quiet before a scheduled review, reducing trading volumes and wallet interactions until it clears, then resumes. Shufti's Perpetual KYC is event-driven, not calendar-driven, artificially quiet behaviour around a review date does not erase the historical risk pattern.

Identity Swap at Re-Verification

A flagged account holder submits fresh documents at re-verification claiming their ID expired, attempting to swap their flagged identity for a cleaner variant. Shufti's Biometric Face Authentication matches the current selfie against the biometric enrolled at original onboarding, the same face must be present regardless of new documents, making identity substitution biometrically impossible.

Close Account

Pre-SAR Closure

A crypto user under active compliance review submits a GDPR erasure request to wipe the evidence trail before a SAR is filed. Shufti enforces regulatory data-retention requirements over erasure requests, and AML Screening surfaces all SAR obligations before the closure is processed.

Balance Extraction Before Closure

A user who receives a compliance notice immediately sweeps all crypto holdings to external wallets and requests account closure before any freeze applies. Shufti's Transaction Monitoring flags full-balance withdrawal events that follow compliance-related triggers, enabling an automatic hold before funds leave the platform.

Re-Application Under New Identity

A banned crypto user re-applies using a different passport or family member's identity, expecting to be treated as a new applicant. Shufti's 1:N Facial Deduplication screens every new selfie against all existing and deactivated accounts, a match to a previously rejected face triggers immediate escalation regardless of the documents presented.

Built For Every Role That Owns The Onboarding Decision

Combine products across identity, compliance, and fraud defence to build a verification stack that meets your regulatory requirements; without rebuilding the integration each time the rulebook changes.

Compliance Officer

Stop manually reconciling vendor data and let Shufti automate your audit trail, providing a unified, jurisdiction-specific evidence package for every user, updated in real time by the in-house compliance team.

Head of Product

Eliminate market-specific friction with a configurable engine that scales to 240+ countries actively processed, using localised pass-rate data to optimise your UX before you even go live.

Head of Engineering

Stop managing vendor sprawl and start building; deploy one REST API for the entire user lifecycle, backed by enterprise-grade SLAs and comprehensive SDK coverage.

Fraud Analyst

Slash manual review times by 80% with a unified Fraud Hub that surfaces the 'why' behind every flag before your team even opens the case.

Don’t just take our word for it, hear from our customers

The Confidence Our Clients Share

The future of digital identity is defined by trust, interoperability, and regulatory alignment, so our partnership with Shufti reinforces DevCode Identity’s commitment to supporting our global customers with the most secure, best-in-class, compliant identity verification solutions available today.

Combining our Conversion Driven Compliance Orchestration Platform with Shufti’s global KYC and IDV capabilities allows our customers not only to navigate complex regulatory demands but also to maintain a seamless customer onboarding experience with the highest achievable conversion rates.

We’re proud to continue our partnership with Shufti as we expand into new jurisdictions.

Shufti’s verification technology not only strengthens our compliance framework but also ensures our players enjoy a smooth, secure onboarding experience.

We ain to offer our clients and their traders the very best tools with which to do their jobs, we’re excited to be able to work with Shufti.

They’re a leading company, and we’re looking forward to offering their solutions to our clients through our CRM.

The relationship with Shufti was born out of frustration with an existing provider, so we started our discussion with Shufti.

The response time was excellent, from the start of speaking to sales to getting up and running with the demo.

Everything you need to know in one place

Frequently Asked Questions

Exchanges operating in the EU are subject to MiCA and the 6th Anti-Money Laundering Directive. FATF’s updated Recommendation 16 extends Travel Rule obligations to VASPs globally, requiring originator and beneficiary data on transfers above threshold. Shufti’s compliance team maintains rule sets across 240+ regions actively processed to keep coverage current as requirements evolve.

Transaction Trust Monitoring identifies VASP-to-VASP payment flows and triggers automated data collection for Travel Rule reporting. Originator and beneficiary data is captured, matched, and transmitted through a single protocol; reducing the manual counterparty due diligence effort that separate Travel Rule vendors typically introduce.

ISO/IEC 30107-3 PAD Level 3 is the highest independent certification tier for presentation attack detection. iBETA tested Shufti’s liveness system against physical artefacts (printed photos, 3D masks), video replay attacks, and deepfake injection vectors. Level 3 certification confirms the system passed at the most demanding attack tier in the standard.

Where local regulation permits document-free onboarding, Shufti supports database-validated KYC flows. NFC verification is also available for users with e-passport-capable devices, providing chip-level identity assurance without a separate document scan.

A sandbox environment is available immediately for integration testing. The single REST API covers document verification, biometric liveness, AML screening, and transaction monitoring; eliminating the multi-vendor integration cycle that typically extends deployment timelines.

Evaluate Shufti Against Your Current Crypto Stack

MiCA, the Travel Rule, and FATF Recommendation 16 require a verification architecture that connects onboarding identity to ongoing transaction monitoring. Point-solution stacks cannot share identity records, produce consistent audit trails, or update compliance rules from a single source. Evaluate whether your current stack meets that standard.