AMLR Solutions

AMLR Solutions AMLR Consultation

AMLR Consultation Onboarding

Onboarding Ongoing Monitoring

Ongoing Monitoring FRAML

FRAML KYC

KYC KYB

KYB KYI

KYI Age Assurance

Age Assurance Workforce IAM

Workforce IAM Candidate Verification

Candidate Verification Account Takeover

Account Takeover Bonus/ Promotion Abuse

Bonus/ Promotion Abuse Chargeback Fraud

Chargeback Fraud Deepfake

Deepfake Document Fraud

Document Fraud Fraud Networks

Fraud Networks Impersonation Fraud

Impersonation Fraud Money Mule Activity

Money Mule Activity Multi-Accounting

Multi-Accounting Party Fraud

Party Fraud Regulatory & Compliance Risks

Regulatory & Compliance Risks Synthetic Identity Fraud

Synthetic Identity Fraud Adult Content

Adult Content Banking

Banking Crypto

Crypto Fintech

Fintech Forex

Forex Compliance

Compliance Fraud prevention

Fraud prevention Trust & safety

Trust & safety Global expansion

Global expansion Compliance Officers

Compliance Officers Developers

Developers Fraud Analysts

Fraud Analysts Product Managers

Product Managers Advanced Journey Builder (AJB)

Advanced Journey Builder (AJB) Global Trust Platform

Global Trust Platform Customer Profiles

Customer Profiles Vendor Comparison

Vendor Comparison IDV Case Management

IDV Case Management AML Case Management

AML Case Management Regulatory Reporting

Regulatory Reporting Travel Rule Protocols

Travel Rule Protocols Agentic Rule Builder

Agentic Rule Builder AI Compliance Co-Pilot

AI Compliance Co-Pilot Fraud Analytics

Fraud Analytics Fraud Hub

Fraud Hub OCR

OCR Shufti AI

Shufti AI Bank Account Verification

Bank Account Verification Biometric Duplication

Biometric Duplication Database Checks

Database Checks Document Intelligence

Document Intelligence Government ID

Government ID Mobile Driver's License

Mobile Driver's License NFC

NFC Selfie Liveness

Selfie Liveness Brand Personalisation

Brand Personalisation Deployment Options

Deployment Options Identity Methods

Identity Methods IDV Modes

IDV Modes Multi-tenancy

Multi-tenancy On-Premise IDV

On-Premise IDV Secure Capture

Secure Capture

Payments & Neobanks

Verify Users, Block Fraud and Stay Compliant From Sign-Up to Account Closure

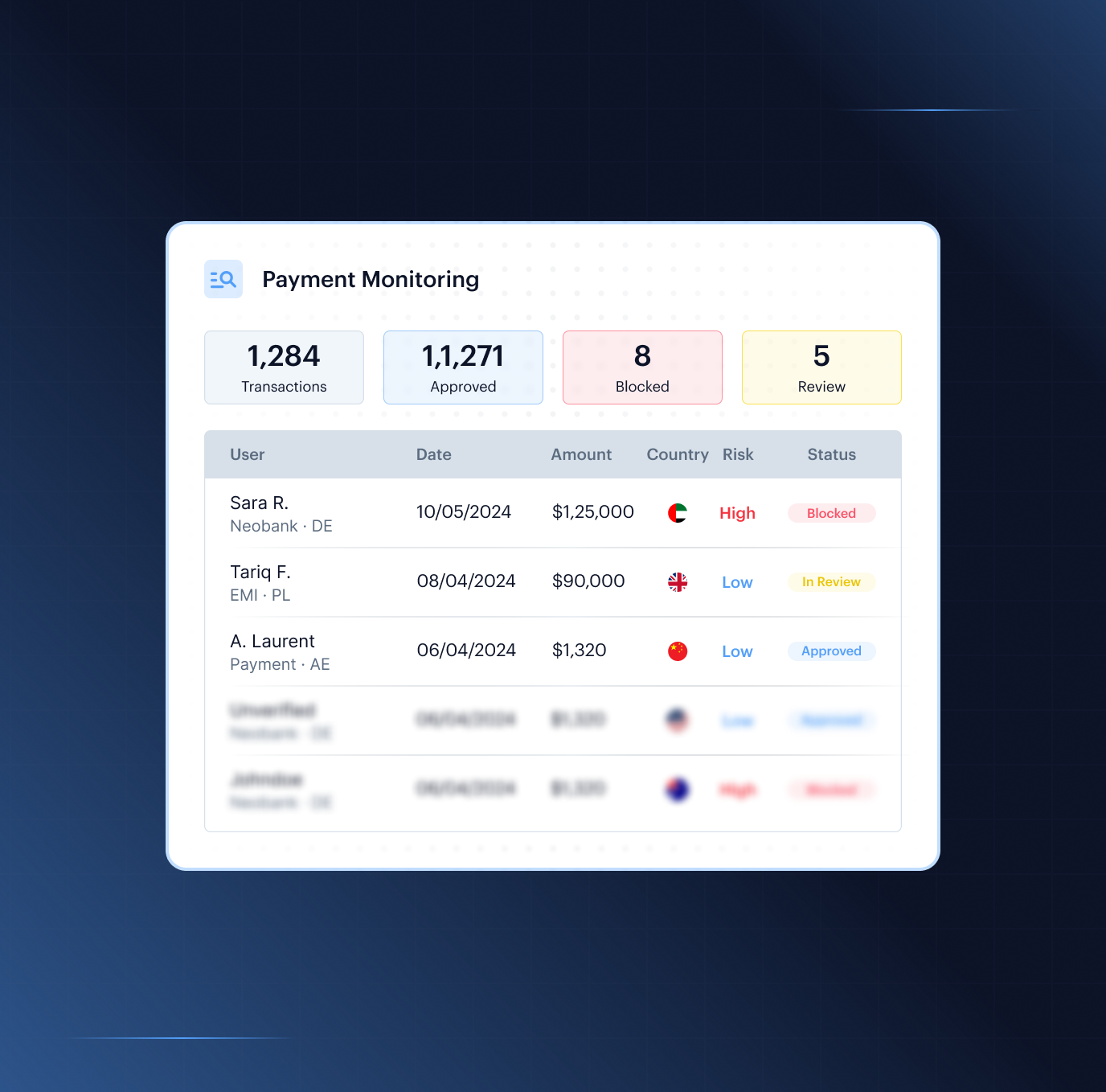

Shufti powers identity verification, AML screening, transaction monitoring and fraud prevention for neobanks, EMIs, payment processors and embedded-finance platforms across 240+ countries actively processed.

Proven Performance

Our impact, by the numbers

- <30sMedian Time-to-Decision

- 4,000+Watchlists Screened

- 240+Countries Actively Processed

Trusted by Leading Digital Enterprises Worldwide

Compliance Without Compromise

Why Payments Platforms Choose Shufti

-

Stay Ahead of Enforcement

The FCA fined Monzo £21 million in July 2025 for onboarding customers using addresses like Buckingham Palace and 10 Downing Street. Starling was fined £29 million for screening customers against only a fraction of the UK Sanctions List. Shufti's AML rule sets, sanctions coverage across 215+ regimes, and address verification update continuously so compliance keeps pace with regulatory change without engineering intervention.

-

Stop Fraud Before It Onboards

The Deloitte Center for Financial Services warns that generative AI fraud losses could grow to $40 billion by 2027 if adaptive defences remain undeployed. Shufti's iBETA Level 3-certified liveness detection, NFC chip verification and device intelligence intercept deepfakes, synthetic identities and injection attacks at first contact, before a fraudulent account is created.

-

Onboard Without Losing Users

A median decision time under 30 seconds across 240+ countries actively processed means legitimate users clear verification before they consider abandoning. Risk-tier configuration lets low-risk users move faster without compromising checks on high-risk segments.

Secure Every Stage of the Payments User Lifecycle

Sign Up

Bot Account Farming

Bot farms spin up thousands of neobank accounts in minutes, seeding referral bonus rings and mule networks. Shufti's Device Fingerprinting spots emulators and rotating proxy IPs at registration. Behavioural Biometrics kills the attempt early. No human typing rhythm and no dwell time have no human equivalent. The Fraud Hub consolidates signals to block the entire cluster.

Synthetic Identity at Sign-Up

A fraudster combines a stolen National Insurance number with fabricated details to create an account that passes format checks but belongs to no real person. Shufti's eIDV independently cross-references the declared identity against government, telco and credit bureau databases, exposing the absence of any real financial or address footprint. AML Screening adds a final check against watchlists before the account is ever created.

Bonus / Referral Abuse

A single operator registers dozens of neobank accounts under slight PII variations to harvest welcome bonuses and referral payouts. Shufti's proprietary 1:N Facial Deduplication surfaces the same face behind multiple identities across the full customer base. Device Fingerprinting links the shared hardware and IP ranges, ensuring one person can only hold one verified account.

Stolen Identity Registration

A fraudster uses PII from a data breach to open a neobank account the victim knows nothing about. Shufti's eIDV checks submitted details against the genuine identity's known data footprint, flagging mismatches that indicate the submitter is not the true owner. Face Verification then confirms the person in front of the camera matches the document holder, not someone presenting stolen information.

Emulator and VPN Spoofing

A fraudster routes neobank registrations through a VPN or emulated device to bypass region-based risk rules and UK residency checks. Shufti's Device Fingerprinting intelligently surfaces the emulated environment beneath spoofed signals. eIDV cross-checks the declared address against telco and utility data, catching the mismatch between a claimed UK address and a high-risk jurisdiction connection.

Consent and Disclosure Tampering

A customer disputes ever accepting the neobank's T&Cs or AML data-sharing obligations, creating regulatory exposure under FCA Consumer Duty. Shufti's Consent Verification captures a defensible cryptographic, time-stamped record of every acceptance at the moment it happens. When the dispute lands, the evidence is already exportable and tied to a verified identity.

Onboarding in Breach of Risk Appetite

A neobank's controls fail to reject applicants who register with obviously implausible details, the precise failure the FCA cited in the Monzo Final Notice, where accounts were opened using Buckingham Palace and 10 Downing Street as addresses. Shufti's Address Verification validates every declared address against postal, utility and credit data in real time, rejecting inputs that have no matching footprint before the customer record is created. eIDV adds a further cross-check across government and authoritative sources. Perpetual KYC continues to monitor the account after onboarding, catching risk-profile changes that initial checks cannot anticipate.

Verify Identity (KYC)

Document Forgery

A fraudster uploads a tampered or fabricated government ID to open a neobank account, expecting automated checks to miss the edits. Shufti's Document Verification runs forensic analysis across any government-issued document, checking fonts, MRZ checksums and holographic elements. NFC Verification reads the cryptographically signed chip in modern passports and ID cards, bypassing the image layer that forgery targets entirely.

Deepfake and AI Face Attack

A fraudster presents an AI-generated deepfake clip during the neobank selfie step to impersonate the genuine document holder. Shufti's Face Verification, certified at iBETA Level 3 under ISO/IEC 30107-3, applies 3D depth mapping and micro-movement analysis to distinguish a live face from synthetic video. Injection Detection runs in parallel, blocking virtual camera feeds at OS level before any biometric data is captured.

Camera Injection Attack

A fraudster routes pre-recorded video into the neobank's verification SDK via virtual camera software, bypassing the device's physical camera. Shufti's Injection Detection verifies the camera stream at hardware level, rejecting any feed not originating from a genuine, attested device. Device Fingerprinting identifies the virtual camera driver, so synthetic feeds never reach the liveness engine.

Synthetic Identity Document

A fraudster overlays a real document template with fabricated details to create a composite ID for neobank account opening. Shufti's NFC Verification reads the cryptographically signed chip in the eMRTD, which no printed or digital fake can replicate. eIDV then confirms whether the identity has any genuine footprint in government and credit databases. A synthetic that passes the visual layer fails both checks.

Proof-of-Address Forgery

A fraudster submits an edited utility bill or bank statement to satisfy UK address verification for a neobank account, knowing basic editing tools can fool visual checks. Shufti's Address Verification validates the declared address against authoritative postal, utility and credit bureau data rather than the uploaded document itself. eIDV adds a cross-reference against government records for high-risk segments.

Business Ownership Concealment

A criminal uses nominee directors and layered holding structures to hide a sanctioned beneficial owner when opening a neobank business account. Shufti's KYB maps the full ownership chain to the ultimate beneficial owner across 140+ registry jurisdictions. Every identified person is then screened through AML Screening against 4,000+ watchlists and 215+ sanctions regimes.

Coerced or Money-Mule KYC

A real person passes neobank KYC genuinely, but is being coached by a money mule recruiter who will take over the account for laundering. Shufti's VideoIDnet conducts a live video interview that a trained reviewer assesses for coaching signals and signs of duress. Behavioural Biometrics establishes a baseline during onboarding and flags when subsequent usage drifts from the verified person's pattern.

Risk Screening

Sanctions Evasion via Spelling Variants

A sanctioned individual uses transliterated or misspelled name variants to open a neobank account and slip past exact-match screening. Shufti's AML Screening applies phonetic and Levenshtein distance matching across 215+ sanctions regimes and 4,000+ watchlists, catching variants a basic string-match engine would miss across Latin, Arabic, Cyrillic and CJK scripts in 150+ languages.

Stale Sanctions Screening

A neobank customer onboards clean but is re-designated to a sanctions list months later, the precise control failure the FCA cited in its £29 million fine against Starling Bank. Shufti's AML Screening continuously re-checks the full customer base against live watchlist updates, triggering an alert within hours of any re-designation rather than waiting for the next scheduled refresh. Perpetual KYC then updates the customer's risk score and routes the case to the Fraud Hub for immediate review.

PEP Concealment

A politically exposed person omits their state-owned enterprise role or close family connection to a senior official, hoping a declaration-only screening process will take their word for it. Shufti's AML Screening checks beyond self-declared PEP status, cross-referencing family members, relatives and close associates against PEP databases across four tiers. Adverse media coverage is indexed in 150+ languages, surfacing local reporting that English-only systems miss entirely. Due Diligence provides enhanced checks for entities that trigger initial PEP signals, building a complete risk picture before onboarding proceeds.

Adverse Media False Negative

A customer with serious criminal history appears clean on screening because the relevant coverage exists only in local-language media that the screening engine cannot read. Shufti's AML Screening indexes adverse media across 50,000+ sources in 150+ languages, including CJK, Arabic, Cyrillic and regional press that English-only systems bypass entirely. Automated severity classification prioritises the hits that matter, reducing analyst noise while ensuring no language-specific coverage is invisible to the review queue.

Beneficial-Ownership Concealment

A corporate customer places a high-risk or sanctioned individual behind two or three layers of nominee-held holding companies, making the UBO invisible to a surface-level KYB check. Shufti's KYB resolves the full ownership chain across 140+ business registry jurisdictions, tracing each layer until it reaches the ultimate beneficial owner. Every natural person identified through that resolution is individually screened through AML Screening against 4,000+ watchlists and 215+ sanctions regimes. Where the chain raises further risk signals, Due Diligence applies enhanced checks before the account proceeds.

High-Risk Jurisdiction Misrepresentation

A user based in a sanctioned or high-risk country declares a different address and connects through a VPN to make their access appear local. Shufti's Address Verification cross-references the declared address against independent postal and credit data, flagging addresses with no supporting footprint in the claimed jurisdiction. Device Fingerprinting surfaces the VPN connection and IP-to-location mismatch that the declared address cannot explain. eIDV and AML Screening then apply jurisdiction-appropriate risk rules to the verified location rather than the declared one.

Fund Account

Stolen-Card Initial Top-Up

A fraudster funds a newly opened neobank account using compromised card details, racing to convert the balance before the cardholder notices. Shufti's Transaction Monitoring flags the combination of a new account, first funding and BIN-country mismatches in real time, triggering a hold before the funds settle. Device Fingerprinting cross-references the device against known fraud-associated hardware clusters, blocking the initial top-up.

Funder Does Not Match Account Holder

A money mule account receives its first top-up from a card or bank transfer registered to a different person. Shufti's eIDV validates the name on the funding instrument against the verified KYC record, flagging the mismatch immediately. Transaction Monitoring escalates when the incoming source and account owner do not resolve to the same identity, stopping the mule account before any outbound payment is possible.

BIN-Range Card Testing

A fraudster adds multiple stolen cards in rapid succession against a neobank account, running small test charges to identify live BIN ranges before cashing out. Shufti's Transaction Monitoring detects the velocity pattern, flagging multiple low-value funding attempts within a compressed time window as a testing signature rather than normal behaviour. Device Fingerprinting links the attempts across multiple accounts when a single device or IP cluster is driving the test sequence. The velocity throttle triggers before the fraudster has validated enough cards to make the attack profitable.

Card-Issuance Diversion

After passing neobank KYC, a fraudster changes their registered address so the physical debit card is delivered to a drop address they control. Shufti's Address Verification flags address changes within a short window of card issuance as high-risk, triggering re-verification. Biometric Face Authentication requires a live biometric step-up before any address change is committed, ensuring the genuine account holder is physically present. MFA adds a second independent factor, preventing the change from going through on credentials alone.

Virtual-Card Provisioning Fraud

A fraudster adds a newly issued virtual card to a digital wallet or marketplace they control, intending to spend against the balance immediately. Shufti's Device Fingerprinting identifies the unfamiliar device attempting the wallet provisioning and flags it as inconsistent with the account's registered hardware. Behavioural Biometrics detects the atypical usage cadence of a fraudster moving quickly through provisioning steps compared with the baseline of a real cardholder exploring the feature. Together they trigger re-authentication before the virtual card is active.

ACH and Direct-Debit Kiting

A fraudster exploits settlement delays by cycling funds between the new neobank account and one or more external accounts, inflating an apparent balance that does not yet reflect cleared funds. Shufti's Transaction Monitoring models cross-account velocity and float patterns, detecting the repeating in-out cadence that kiting produces before the cycle completes. Perpetual KYC monitors the account for early behavioural signals, including rapid opening activity and atypical transfer patterns, that indicate the account was opened for exploitation rather than genuine use.

Log In

Account Takeover via Phishing

A fraudster drives a customer to a spoofed login page, harvests their credentials in real time and uses them to access the genuine account before the customer realises. Shufti's Biometric Face Authentication requires a live biometric selfie matched to the enrolled KYC record, making stolen passwords alone insufficient to access the account. Fast ID binds the authentication to the device and the verified face, so credentials captured on a phishing page cannot be replayed on a different device. MFA with TOTP adds an on-device second factor that a phishing proxy cannot intercept.

SIM-Swap Account Takeover

A fraudster social-engineers the mobile carrier into reassigning the victim's phone number, intercepting SMS 2FA codes and triggering a password reset. Shufti's MFA uses TOTP codes generated on-device, removing any reliance on the phone number and making the swapped SIM entirely useless for authentication. Biometric Face Authentication then requires the enrolled biometric face rather than a code, so even a successful SIM swap cannot unlock the account. The Cifas Fraudscape 2026 recorded a 38% rise in unauthorised SIM swaps in 2025, making this protection particularly timely.

Credential Stuffing

An attacker sprays billions of leaked credentials against a neobank login endpoint, exploiting widespread password reuse. Shufti's Device Fingerprinting identifies non-human request cadence, rotating proxy infrastructure and emulated devices that stuffing tools use. Behavioural Biometrics detects scripted interaction at login, blocking the attack before any account is compromised.

Session Hijacking

A fraudster steals a valid neobank session token via an infostealer and operates the account as the authenticated customer. Shufti's Behavioural Biometrics detects the moment the person behind the device changes, triggering a step-up authentication challenge. Device Fingerprinting flags the shift to an unrecognised hardware or network profile mid-session, terminating access before funds move.

Remote-Access Trojan Takeover

Malware installed on a customer's device gives a fraudster real-time remote control of the neobank session, initiating payments while the genuine user is unaware. Shufti's Behavioural Biometrics detects the divergence between the user's natural interaction patterns and the scripted precision of a remote operator. Device Fingerprinting identifies accessibility-service abuse and screen-sharing signals at OS level. Transaction Monitoring flags the payment patterns remote-control fraud produces.

MFA Push Fatigue

A fraudster bombards a neobank customer with MFA push notifications until exhaustion prompts an accidental approval. Shufti's MFA uses TOTP codes generated on-device, eliminating the approve/deny prompt that fatigue attacks exploit. Fast ID adds a passkey-based alternative tied to the enrolled biometric, so neither method can be resolved by someone who does not hold the registered device.

Receive Funds

Money Mule Receipt (Witting)

A neobank account holder knowingly receives transfers from strangers and quickly forwards them, making the account the first domestic hop in a laundering chain. Transaction Monitoring flags the mule velocity signature: rapid inbound-outbound cycling, growing transfer amounts and unusual counterparty networks. Perpetual KYC triggers a risk-tier review when spending patterns diverge from the onboarding profile. The Fraud Hub packages the evidence for SAR submission before funds exit the platform.

Money Mule Receipt (Unwitting)

A genuine neobank customer is manipulated through a romance scam or fake job offer into receiving and forwarding funds on behalf of a fraudster, often unaware they are committing money laundering. Behavioural Biometrics detects coached interaction patterns, including scripted chat replies, unusual hours and unfamiliar devices, that signal external direction. Transaction Monitoring flags the inbound-to-outbound forwarding pattern, triggering an EDD review to protect a potentially vulnerable customer rather than simply blocking the account.

APP Fraud Proceeds Inbound

Under the PSR mandatory reimbursement rules, a neobank is liable from the moment APP fraud proceeds land in a mule account it hosts. Shufti's Transaction Monitoring scores every inbound payment in real time, flagging Confirmation of Payee mismatches and counterparty risk signals that indicate the account is receiving APP fraud proceeds. AML Screening continuously monitors the account for the layering activity that follows mule receipt. Rapid identification and offboarding of mule accounts directly reduces the receiving PSP's reimbursement exposure.

Sanctioned-Counterparty Inbound

Funds routed through a sanctioned bank, intermediary or jurisdiction put the receiving neobank in breach regardless of whether the account holder is themselves complicit. AML Screening checks the originator, intermediary BIC and routing jurisdiction against 215+ sanctions regimes before settlement, not after. A match triggers an immediate hold, giving the compliance team the option to reject or escalate the payment before the transaction completes.

Salary and Payroll Mule Spoofing

A laundering ring pushes illicit funds through neobank accounts disguised as salary or payroll credits, giving inbound transfers the appearance of legitimate employment income. Transaction Monitoring checks consistency of declared employer, inbound IBAN and payment frequency against genuine payroll patterns, surfacing irregular dates, mixed sources and atypical amounts. Perpetual KYC cross-references the pattern against the verified income and employment profile, escalating mismatches for EDD review.

Cross-Border Layering

Illicit funds move through a chain of neobank accounts across jurisdictions via SEPA Instant or SWIFT, with each hop designed to obscure the origin before the next transfer. Transaction Monitoring runs multi-hop graph analytics, tracing the link between inbound and outbound payments across accounts rather than evaluating each transfer in isolation. Due Diligence applies enhanced checks to cross-border activity above risk thresholds, building the evidence chain the compliance team needs to file a credible SAR.

Send Money

Authorised Push Payment Fraud

A fraudster socially engineers a neobank customer into authorising a large payment to an account they believe belongs to their bank, solicitor or builder. Under PSR mandatory reimbursement rules, the sending neobank faces 50% liability from the moment funds leave. Behavioural Biometrics detects screen-sharing activity, atypical typing patterns and payment amounts inconsistent with account history that signal a coached transaction. Transaction Monitoring scores the destination account, and Biometric Face Authentication adds a biometric step for high-value sends, creating friction precisely where APP attacks are most effective.

New-Payee First-Send Fraud

A fraudster who has taken over a neobank account adds a new beneficiary and immediately sends a large transfer before any monitoring baseline exists. Transaction Monitoring flags the combination of a freshly added payee and a first payment above threshold as a high-risk event. MFA applies a step-up challenge, Confirmation of Payee checks the beneficiary name against bank records, and the cooling-off period gives the genuine account holder time to confirm or cancel the transfer.

Money Mule Pay-Out

A neobank mule account that received illicit funds rapidly sweeps the balance to further mule accounts or crypto off-ramps, aiming to complete the outbound leg before the inbound flag is reviewed. Transaction Monitoring models velocity, in-out ratio and graph clustering in real time, surfacing the mule pay-out pattern within the same session as the inbound receipt. Perpetual KYC has already updated the account's risk score based on the inbound pattern, so the outbound alert fires faster. The Fraud Hub consolidates both events into a single case for SAR preparation.

Beneficiary on Sanctions List

A neobank customer attempts to send funds to a payee that resolves to a sanctioned individual, entity or jurisdiction, either knowingly or because a fraudster has manipulated destination details. AML Screening checks the destination IBAN/BIC against 4,000+ watchlists and 215+ sanctions regimes before the payment settles, blocking the send with an immediate hold. AML Screening keeps continuous coverage of saved payees, so a beneficiary clean at first payment still triggers an alert if subsequently designated.

Investment Scam Send

A fraudster builds a relationship with a neobank customer over weeks before persuading them to transfer funds to a fake investment platform. Investment scam APP losses rose approximately 75% year-on-year in the UK according to UK Finance. Transaction Monitoring applies risk scores to destination accounts associated with known investment scam typologies, flagging the payment before it leaves. Consent Verification captures a cryptographic in-app acknowledgment at the point of send, creating a timestamped record that defeats did-not-authorise repudiation.

First-Party Did-Not-Authorise Repudiation

A genuine neobank customer makes a real payment then disputes it as unauthorised to claim a PSR reimbursement while keeping the funds. Behavioural Biometrics establishes the interaction pattern at the point of the disputed payment, confirming whether it matches the genuine account holder's baseline. Biometric Face Authentication provides a timestamped biometric confirmation of the authorisation, and Consent Verification supplies a signed in-app acknowledgment that defeats the did-not-authorise claim.

Card Spend

Card-Not-Present Fraud

A fraudster uses stolen card details to make purchases at online merchants where neither the physical card nor a PIN is required, exploiting the gap between card issuance and transaction-time verification. UK Finance recorded nearly 2.6 million CNP fraud cases in 2024, with losses up 11% to just under £400 million. Shufti's Transaction Monitoring applies real-time risk-scoring to every CNP transaction, using device and behavioural signals to distinguish the genuine cardholder from a fraudster reusing stolen credentials. Only high-risk transactions trigger a 3DS step-up challenge, keeping friction low for legitimate spend while blocking fraud at the point of transaction.

Chargeback and Friendly Fraud

A genuine cardholder makes a purchase, receives the goods or service, then disputes the transaction as unauthorised in order to recover the funds without returning what they paid for. Shufti's Behavioural Biometrics records the interaction patterns at the moment of the original authorisation, creating a behavioural baseline that confirms the genuine account holder was in control of the device. Consent Verification captures any in-app fraud warnings the customer acknowledged before completing a high-value transaction. The Fraud Hub assembles both evidence types into a chargeback representment package before the dispute deadline.

Card Testing and Enumeration

A fraudster systematically tests large volumes of stolen card numbers by running small transactions across different merchants, identifying which numbers are live before using them for high-value fraud. Shufti's Transaction Monitoring detects the velocity signature of card testing, flagging multiple low-value authorisation attempts within a compressed window as an enumeration pattern. Device Fingerprinting links attempts across multiple accounts when a single device or IP cluster is driving the sequence, exposing the coordinated nature of the attack rather than treating each small transaction in isolation.

Digital-Wallet Provisioning Fraud

A fraudster uses stolen card details to add a card to a digital wallet on a device they control, gaining the ability to make contactless payments without the physical card. Shufti's Device Fingerprinting identifies the unfamiliar device attempting the provisioning and flags it as inconsistent with the cardholder's registered hardware profile. MFA with TOTP replaces the SMS OTP that SIM-swap attacks routinely intercept, ensuring the activation code cannot be redirected. Biometric Face Authentication adds a biometric step for high-risk provisioning events, tying the activation to the verified face of the account holder.

Refund and Return Fraud

A fraudster manipulates the returns process to redirect refund credits to a different card or account, effectively extracting cash from the platform while retaining the original purchase. Shufti's Transaction Monitoring monitors refund-destination consistency, flagging cases where the refund target does not match the original payment instrument. Biometric Face Authentication requires a biometric confirmation before any refund above a defined threshold is processed, ensuring the genuine account holder authorises the destination change rather than a fraudster acting on partial account access.

Lost and Stolen Card Spend

A fraudster finds or steals a physical card and immediately uses it for a series of low-value contactless transactions below the floor limit before the cardholder has reported the loss. Shufti's Transaction Monitoring models the cardholder's typical spending patterns and detects geolocation drift and spending anomalies that do not match their behaviour history. Behavioural Biometrics flags the divergence in real time, triggering an in-app prompt asking the genuine cardholder to confirm or freeze the card before the loss reaches a material amount.

Upgrade Limits

First-Party Credit Bust-Out

A fraudster opens an account, establishes a pattern of normal usage over several months to build credibility, then applies for a limit increase, maxes the overdraft or credit facility and disappears. Shufti's Perpetual KYC continuously monitors the account's behaviour against the evolving cohort of similar customers, flagging the characteristic pattern of normal activity followed by rapid drawdown before the limit increase is granted. Transaction Monitoring detects the rapid drawdown behaviour that follows a bust-out decision, enabling a hold to be placed before the funds fully exit.

Fake Documents for Higher Tier

A fraudster submits a forged passport or fabricated proof-of-income document to unlock a higher transaction tier, knowing that the platform applies lighter checks at the upgrade stage than at onboarding. Shufti's Document Verification applies the same forensic checks at upgrade as at onboarding, including MRZ validation, font analysis and holographic element verification. NFC Verification reads the eMRTD chip in the submitted document, confirming the cryptographic integrity of the identity data. Face Verification then verifies that the face on the upgrade documents matches the biometric enrolled at onboarding, catching substitutions immediately.

Synthetic Identity Ageing

A fraudster nurtures a synthetic identity through months of low-risk activity, building a transaction history that makes the fabricated person appear creditworthy before applying for a limit increase that will be immediately exploited. Shufti's eIDV re-runs at the upgrade trigger, checking whether the identity now has a deeper and more consistent authoritative footprint than at onboarding. 1:N Facial Deduplication screens the upgrade selfie against the full customer base, identifying cases where the same operator is cycling multiple synthetic identities through the upgrade process simultaneously.

Business-Account Upgrade Fraud

A personal account holder attempts to upgrade to a business account by submitting shell-company registration papers, seeking the higher limits that business accounts carry without the corresponding commercial legitimacy. Shufti's KYB resolves the corporate structure against business registries across 140+ jurisdictions, verifying that the entity is active, has genuine directors and has not been flagged in adverse media. Due Diligence applies enhanced screening to the UBOs identified during the resolution, ensuring the individuals behind the upgrade request are themselves clean.

Support Social Engineering

A fraudster calls or messages customer support, impersonating the genuine account holder with enough personal details to persuade an agent to raise the account's transaction limits manually. Shufti's Biometric Face Authentication requires a live biometric selfie matched to the enrolled KYC record before any limit change is committed, regardless of how the request arrives or how much PII the caller provides. Fast ID binds the authorisation to the verified face on the enrolled device, so no amount of social engineering through a support channel can substitute for the genuine account holder's biometric.

Coerced Limit Increase

A scammer pressures or manipulates a vulnerable customer into requesting a higher limit themselves, usually as a precursor to persuading them to make a large APP payment they would not otherwise be able to send. Shufti's Behavioural Biometrics detects the coaching signals and atypical interaction cadence that indicate the customer is acting under instruction rather than independently. Consent Verification captures a cryptographic record of the limit-increase request and any associated in-app warnings under FCA Consumer Duty, creating an evidence trail for regulators and reimbursement decisions alike. Biometric Face Authentication adds a biometric step that ensures the genuine account holder is physically present at the moment of approval.

Account Closure

Sanctions Re-Listing Not Caught

A customer who was clean at onboarding is subsequently added to an OFAC, UK or EU sanctions list, but the platform only screened at the point of account opening and has no mechanism to detect the change. This was the central failure in the FCA's £29 million fine against Starling Bank. Shufti's AML Screening continuously re-checks the full customer base against live watchlist updates, triggering an alert within hours of any re-designation. Perpetual KYC updates the customer's risk score immediately and routes the case to the Fraud Hub for urgent review and account freeze.

Risk Profile Drift

A customer's behaviour gradually shifts toward high-risk activity over months, with no single transaction triggering a threshold, but the cumulative pattern representing a materially different risk profile to the one assessed at onboarding. Shufti's Perpetual KYC monitors behaviour continuously and updates the customer's risk score dynamically rather than waiting for a scheduled review. Transaction Monitoring contributes transaction-level signals to the risk model, and when the combined score crosses a defined threshold, the system automatically routes the account for Enhanced Due Diligence rather than waiting for a human to notice.

Periodic Review Evasion

A customer suppresses suspicious transaction activity in the weeks before a known scheduled review and resumes it immediately after, exploiting the predictability of calendar-based compliance cycles. Shufti's Perpetual KYC is event-driven rather than calendar-driven, evaluating the full account history and all available signals continuously. Because there is no fixed review date to game, behaviour suppression cannot improve the risk score. The model flags the pattern of inactivity followed by resumption as suspicious in its own right.

Identity Swap at Re-Verification

A fraudster who has taken over an account attempts to submit different identity documents at the periodic re-KYC stage, claiming the original ID was lost or expired, in order to replace the enrolled biometric with one they control. Shufti's Face Verification requires the live selfie submitted at re-verification to match the biometric enrolled at onboarding, regardless of what new documents are presented. Biometric Face Authentication applies the same match requirement for any account action tied to the re-verification event. A substitution is detected the moment the new face fails to match the original enrolment.

Exit Fraud at Account Closure

A fraudster empties the account balance through a rapid sequence of transfers immediately after receiving a compliance communication, then submits a closure request in an attempt to prevent further investigation. Shufti's Transaction Monitoring applies enhanced monitoring rules in the period following compliance events, flagging full-balance withdrawal activity as a high-risk signal. The Fraud Hub holds the closure request pending SAR review, ensuring that the account and its transaction history are preserved for regulatory purposes rather than closed and purged on the fraudster's timeline.

Re-Application Under New Identity

An offboarded fraudster returns to the platform under a different name, a close associate's identity or a freshly created synthetic, expecting that the negative file only tracks the previous account identifier rather than the person behind it. Shufti's 1:N Facial Deduplication screens every new applicant's biometric against all previous accounts, including deactivated and closed ones, matching on the face rather than the identity presented. AML Screening applies immediately to the new application, surfacing any watchlist matches associated with the underlying identity. The Fraud Hub links the new case to the prior offboarding record for the review team.

Built For Every Role That Owns The Onboarding Decision

Combine products across identity, compliance and fraud defence to build a verification stack that meets your regulatory requirements, without rebuilding the integration each time the rulebook changes

Compliance Officer

Stop manually reconciling vendor data and let Shufti automate the audit trail, providing a unified, jurisdiction-specific evidence package for every user, updated in real time.

Head of Product

Eliminate market-specific friction with a configurable engine that scales to 240+ countries actively processed, using localised pass-rate data to optimise UX before you even go live.

Head of Engineering

Stop managing vendor sprawl and start building. Deploy one REST API for the entire user lifecycle, backed by enterprise-grade SLAs and comprehensive SDK coverage.

Fraud Analyst

Slash manual review times with a unified Fraud Hub that surfaces the reason behind every flag before your team even opens the case.

Don’t just take our word for it, hear from our customers

The Confidence Our Clients Share

The future of digital identity is defined by trust, interoperability, and regulatory alignment, so our partnership with Shufti reinforces DevCode Identity’s commitment to supporting our global customers with the most secure, best-in-class, compliant identity verification solutions available today.

Combining our Conversion Driven Compliance Orchestration Platform with Shufti’s global KYC and IDV capabilities allows our customers not only to navigate complex regulatory demands but also to maintain a seamless customer onboarding experience with the highest achievable conversion rates.

We’re proud to continue our partnership with Shufti as we expand into new jurisdictions.

Shufti’s verification technology not only strengthens our compliance framework but also ensures our players enjoy a smooth, secure onboarding experience.

We aim to offer our clients and their traders the very best tools with which to do their jobs, we’re excited to be able to work with Shufti.

They’re a leading company, and we’re looking forward to offering their solutions to our clients through our CRM.

The relationship with Shufti was born out of frustration with an existing provider, so we started our discussion with Shufti.

The response time was excellent, from the start of speaking to sales to getting up and running with the demo.

Everything you need to know in one place

Frequently Asked Questions

UK-licensed firms operate under the FCA's MLRs, Consumer Duty and PSR APP reimbursement rules. EU-licensed firms must prepare for AMLR (applies 10 July 2027), AMLD6 transposition, PSD3/PSR application (expected Q2/Q3 2028) and DORA, which has applied since 17 January 2025. US-licensed firms are subject to BSA/AML and FinCEN CDD obligations. Shufti's compliance team maintains rule sets across 240+ countries actively processed so coverage updates without engineering intervention.

Transaction Trust Monitoring scores both sending and receiving payments in real time. Behavioural Biometrics detects duress signals and coaching patterns. Consent Verification captures cryptographic evidence of in-app fraud warnings. Together, these provide the evidence base that determines reimbursement liability under the PSR's 50:50 sending/receiving-PSP split.

ISO/IEC 30107-3 PAD Level 3 is the highest independent certification tier for presentation attack detection. iBETA tested Shufti's liveness system against physical artefacts (printed photos, 3D masks), video replay attacks and deepfake injection vectors. Level 3 certification confirms the system passed with 0% APCER and 0% BPCER on both iOS and Android.

Where local regulation permits document-free onboarding, Shufti supports database-validated KYC flows via eIDV. NFC verification is also available for users with e-passport-capable devices, providing chip-level identity assurance without a separate document scan.

A sandbox environment is available immediately for integration testing. The single REST API covers document verification, biometric liveness, AML screening and transaction monitoring, eliminating the multi-vendor integration cycle that typically extends deployment timelines.

Evaluate Shufti Against Your Current Payments Stack

FCA enforcement, PSR APP reimbursement, DORA and the incoming AMLR require a verification architecture that connects onboarding identity to ongoing transaction monitoring. Point-solution stacks cannot share identity records, produce consistent audit trails or update compliance rules from a single source. Evaluate whether your current stack meets that standard.