Runs On Your Cloud

Runs On Your Cloud No Data Sharing

No Data Sharing No Contract Required

No Contract Required Explore Now

Explore Now

Face Verification

Face Verification

Address Verification

Address Verification

Document Verification

Document Verification

Age Verification

Age Verification

VideoIdent

VideoIdent

Fast ID

Fast ID

eIDV

eIDV

NFC Verification

NFC Verification

Consent Verification

Consent Verification

Business Verification

Business Verification

Due Diligence

Due Diligence

Investor Verification

Investor Verification

E-Signature

E-Signature

Behavioural Biometrics

Behavioural Biometrics

Device Fingerprinting

Device Fingerprinting

MFA

MFA

AML Screening

AML Screening

Business AML Screening

Business AML Screening

User Risk Assessment

User Risk Assessment

Transaction Screening

Transaction Screening

Adverse Media Screening

Adverse Media Screening

Identity Verification

Identity Verification

KYC

KYC

KYB

KYB

KYI

KYI

Bonus Abuse

Bonus Abuse

Fraud Prevention

Fraud Prevention

Deepfakes

Deepfakes

Banking

Banking

Crypto

Crypto

Fintech

Fintech

Forex

Forex

Gaming

Gaming

Gig Economy

Gig Economy

Marketplace

Marketplace

Social Networks

Social Networks

Product Managers

Product Managers

Compliance Officers

Compliance Officers

Fraud Analyst

Fraud Analyst

Global Trust Platform

Global Trust Platform

Journey Builder

Journey Builder

Vendor Comparison

Vendor Comparison

Content library

Content library

Blogs

Blogs

News

News

Reports

Reports

Insights

Insights

Knowledgebase

Knowledgebase

ROI calculator

ROI calculator

Blind Spot Audit

Blind Spot Audit

Deepfake Detection

Deepfake Detection

Liveness Detection

Liveness Detection

Document Originality

Document Originality

Document Deepfake

Document Deepfake

Events & Webinar

Events & Webinar

Podcast Studio

Podcast Studio

Spotlight Studio

Spotlight Studio

API Documentation

API Documentation

Mobile SDKs

Mobile SDKs

Service Status

Service Status

Help Center

Help Center

Contact Us

Contact Us

Technical Support

Technical Support

Compliance

Compliance

Supported Document

Supported Document

About

About

Career

Career

Press Release

Press Release

Certifications

Certifications

Partnership

Partnership

Awards

Awards

240+

countries watchlist screened

<5 Sec

Average transaction verification Time

100%

Risk-based approach for businesses

A secure transaction is the backbone of trust, but the industry struggles with even the basics

A safe transaction is the backbone of trust, but the industry struggles with even the basics Moreover, the world is turning into a global economy and everyone wants a piece of the cake, but risky transactions break trust and hinder scalability for business. Here are the top challenges of transaction screening.

Rigid approach for compliance teams

- Most vendors rely on rigid name-matching that can’t handle cultural variations, transliterations, or messy payment fields. This floods compliance teams with irrelevant alerts, slowing legitimate transactions and driving up operational costs.

Poor payment message parsing

- Legacy tools struggle with ISO 20022, SWIFT MT/MX fields, and free-text notes. As a result, critical data is missed or misread, leading to blind spots where sanctioned entities or hidden counterparties can slip through.

Limited integration and Configurability

- Many solutions don’t let businesses fine-tune thresholds, rules, or corridor-specific risk logic, and they integrate poorly with existing payment flows or case management systems. This forces teams to work around the tool rather than with it.

When screening fails, trust breaks, but not on Shufti's watch

Gone are the days when transaction screening meant only basic checks against static lists. Shufti delivers advanced, real-time screening that analyzes transactions across global watchlists and risk signals ensuring the highest accuracy with minimal friction.

Smarter screening precision for cultural variations

Most screening vendors still don't recognize names written in multiple scripts or unconventional formats. Shufti doesn’t guess.

- It applies layered fuzzy, phonetic, and transliteration models to reduce false positives without missing true risks.

- Ensures your compliance team spends time investigating what matters, not simply sifting through noise.

Native payment parsing to catch undetected risks

Payments don’t arrive cleanly packaged; they come in SWIFT MT, MX, or ISO 20022 formats with messy free-text fields.

- Shufti parses these structures natively, extracting the right data from the right tags.

- Ensures sanctioned entities and hidden beneficiaries don’t slip past unnoticed.

Configurable rules by context for easy understanding

Risk isn’t the same everywhere. High-value transactions in volatile corridors demand tighter thresholds than low-risk domestic payments.

- Shufti lets you calibrate screening logic by corridor, currency, and business model.

- You get ultimate control without forcing a one-size-fits-all framework.

Integration without friction for every industry

Screening is only effective if it fits inside your payment flows. Shufti offers a complete customizable solution for every business and every need.

- Shufti connects through APIs, webhooks, and batch ingestion so alerts move seamlessly into your case management or monitoring stack.

- You get no detours, no manual workarounds, just compliance where it belongs.

Audit clarity guaranteed so you don’t have to rely on guesswork

Regulators don’t accept “we think we checked.” They want a trail. Shufti offers this and more.

- It keeps an immutable record of every decision tied to the exact sanctions list version in use at the time.

- With near real-time updates and transparent logs, you’re not just compliant, you’re prepared for scrutiny.

Transaction screening that is the best of both worlds, stronger security and higher ROI

With Shufti, transaction screening doesn’t force a choice between fraud prevention and customer experience. Our AI-driven system delivers real-time accuracy while keeping friction low, so businesses can stay fully compliant, block bad actors, and still onboard customers seamlessly.

Decrease fraud by up to 65%

- Examine multiple inputs from a user’s account, their device, and location to assess transaction risk with Shufti Transaction Trust Screening. We accept up to 40 data points on a transaction and enrich that number to over 2500 in under 15 milliseconds to assess risk.

Increase revenue by up to 10%

- Minimizing false positives for fraud transactions is just as important as preventing fraudulent transactions. Our real-time scoring reduces false positives, enabling many organizations to process 10% more transactions.

Improve AML compliance

- Transaction Trust Screening uses AI technology to analyze historical and current transactions, flagging indications of money laundering or other financial crimes. This can include information such as transfers, deposits, and withdrawals.

How it works

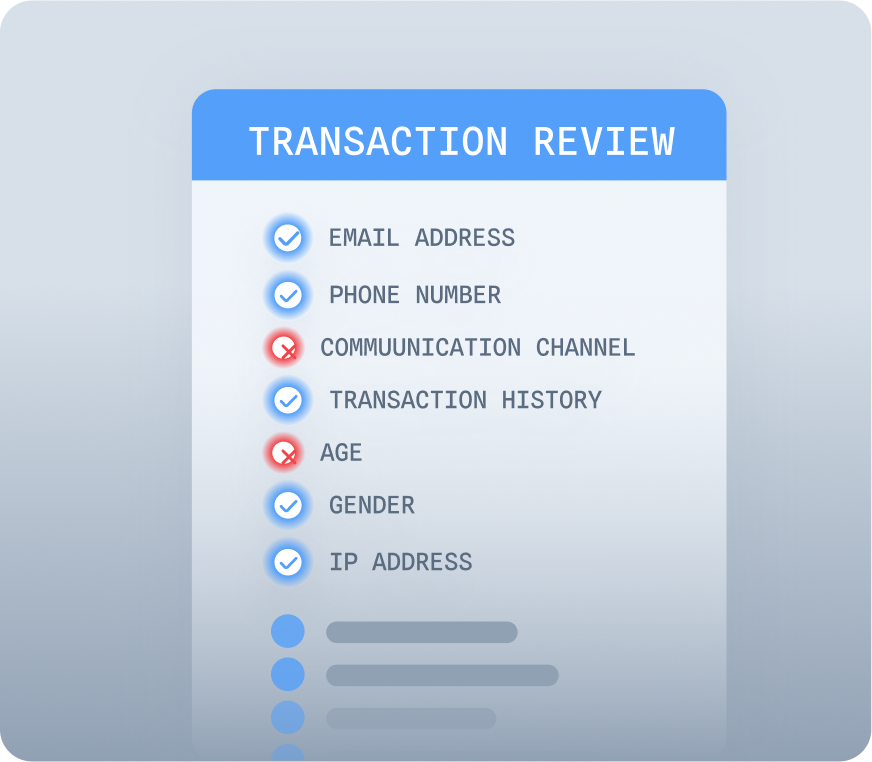

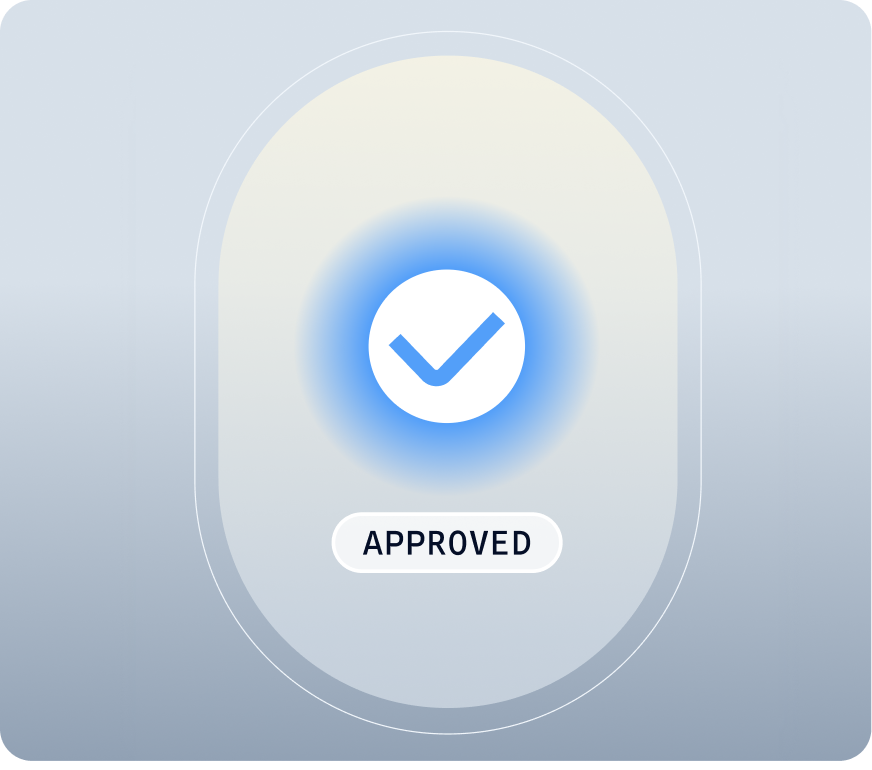

Collect data

Before a transaction is executed, we collect all the data points of this transaction.Evaluate

Powerful AI algorithms review the transaction in relation to the rules and risk parameters set by your business.Decide

Our system analyzes results and determines the next step, whether that’s declination, approval, or further manual review to ensure security.Transact

Once approved, the transaction is executed and you can rest assured that no fraudulent activity happens under our watch.

Protect payments by screening end-to-end users across more than 240 watchlists and millions of data points.

Explore Shufti's AML screeningProtect payments with Shufti's global trust platform

Screening so efficient that only good transactions pass and fraud doesn't last

There are different data formats, incomplete fields, and evolving regulations that means transactions need to be screened continuously. At Shufti's innovation room, every transaction screened is fraud prevented at the forefront.

Denies hijacked accounts and stolen access

Account Takeover happens when fraudsters exploit stolen credentials to impersonate real users. Shufti detects unusual patterns at login and payment stages, blocking intrusions before they turn into losses.

- Tracks behavioral anomalies and device fingerprints in real time.

- Links every login attempt back to a verified identity signal.

Instantly catch chargebacks that drain revenue

Fraudsters complete a transaction only to dispute it later, claiming it wasn’t authorized. Shufti reduces this risk by validating the payer’s identity at the point of purchase, making false disputes harder to sustain.

- Confirms the authenticity of each transaction with multi-layer checks.

- Provides strong evidence trails to fight illegitimate chargeback claims.

Flags fake identities that seem authentic and built from scratch

Synthetic identity fraud blends fragments of real and fabricated data to create convincing new profiles. Shufti’s verification stack exposes these fabrications before they ever reach approval.

- Matches documents, biometrics, and behaviour against trusted data sources.

- Flags inconsistencies across multiple signals to uncover hidden fakes.

Frequently Asked Questions

What is transaction screening?

Transaction screening is the process of checking financial transactions against global sanctions, PEPs, and watchlists to detect suspicious activity and ensure compliance.

Why is transaction screening important?

It helps businesses prevent money laundering, terrorist financing, and regulatory fines while protecting customer trust and safeguarding the financial system.

How does Shufti’s transaction screening work and reduce false positives?

Shufti uses AI-driven checks, real-time monitoring, and global watchlists to instantly flag high-risk transactions while allowing legitimate ones to pass. To reduce false positives, Shufti applies fuzzy matching, phonetic intelligence, and contextual risk scoring to minimize false alerts, so compliance teams can focus on genuine risks.

Which industries need transaction screening?

Banks, fintech, payment providers, crypto platforms, insurance, and e-commerce businesses all benefit from transaction screening to stay compliant and reduce fraud.

What’s the difference between transaction screening and transaction monitoring?

Screening happens instantly at the point of a transaction, while monitoring is continuous analysis of patterns over time. Together, they provide full protection against financial crime. However, transaction monitoring can sometimes be an exhaustive process.

Can transaction screening adapt to different regulatory requirements?

Yes. Shufti tailors screening rules by jurisdiction, ensuring businesses meet global standards like FATF, OFAC, EU AMLD, and local regulations without overblocking.

How often should businesses perform transaction screening?

Businesses should screen transactions in real time or continuously, especially in high-risk sectors. Low-risk businesses may perform periodic or batch screening based on their risk level and regulations.

Is transaction screening mandatory for all businesses?

It’s mandatory for regulated entities like banks, fintechs, and crypto firms under AML/CTF laws. Non-regulated businesses aren’t required but often adopt it for fraud prevention and compliance.

What happens if a transaction is flagged during screening?

Flagged transactions are paused for review. If found suspicious, they’re reported to authorities and possibly blocked; if cleared, they proceed as normal.

Does transaction screening work for crypto transactions and digital assets?

Yes, it uses blockchain analytics to monitor wallet addresses, detect high-risk activity, and ensure compliance with global AML and FATF Travel Rule standards.

Related Solutions

E-Commerce

Fast confirmation of identity and age for individuals engaged in e-commerce or using marketplaces such as vacation homes, ride sharing or pet sitting.

") Explore

Explore

Foreign Exchange (Forex)

Safeguard clients and onboard more customers while meeting legal and requirements for KYC and AML regulations.

") Explore

Explore

Fintech

Expand globally with KYC solutions that meet your business needs and adhere to varied regional and country requirements.

Explore

Explore

learn more

Learn what is transaction monitoring?

Transaction screening and transaction monitoring are both key components of AML compliance, but they serve different purposes. Screening is a real-time check that evaluates transactions while monitoring looks at transaction patterns over time to identify suspicious behavior, such as structuring, unusual volumes, or money laundering risks. Learn more about transaction monitoring here.

Take the next steps to better security.

Contact us

Get in touch with our experts. We'll help you find the perfect solution for your compliance and security needs.

Contact us