Face Verification

Face Verification

Address Verification

Address Verification

Document Verification

Document Verification

Age Verification

Age Verification

VideoIdent

VideoIdent

Fast ID

Fast ID

Docless Verification

Docless Verification

Consent Verification

Consent Verification

NFC Verification

NFC Verification

Business Verification

Business Verification

Due Diligence

Due Diligence

Investor Verification

Investor Verification

E-Signature

E-Signature

QES

QES

AML Screening

AML Screening

Transaction Monitoring

Transaction Monitoring

Adverse Media

Adverse Media

Business AML Screening

Business AML Screening

PEP & RCA

PEP & RCA

Sanctions

Sanctions

Watchlist

Watchlist

Behavioural Biometrics

Behavioural Biometrics

Device Fingerprinting

Device Fingerprinting

Biometric Face Authentication

Biometric Face Authentication

MFA

MFA

Fraud Hub

Fraud Hub

Onboarding

Onboarding

Ongoing Monitoring

Ongoing Monitoring

KYC

KYC

KYB

KYB

KYI

KYI

Age Assurance

Age Assurance

Identity Verification

Identity Verification

Workforce IAM

Workforce IAM

Candidate Verification

Candidate Verification

Compliance

Compliance

Fraud prevention

Fraud prevention

Trust & safety

Trust & safety

Global expansion

Global expansion

Product Managers

Product Managers

Compliance Officers

Compliance Officers

Fraud Analysts

Fraud Analysts

Developers

Developers

Deepfake Detection

Deepfake Detection

Bonus Abuse / Promotion Abuse

Bonus Abuse / Promotion Abuse

Account Takeover

Account Takeover

Synthetic Identity Fraud

Synthetic Identity Fraud

Document Fraud

Document Fraud

Impersonation Fraud

Impersonation Fraud

Multi-Accounting

Multi-Accounting

Fraud Networks

Fraud Networks

Chargeback Fraud

Chargeback Fraud

Money Mule Activity

Money Mule Activity

Party Fraud

Party Fraud

Regulatory & Compliance Risks

Regulatory & Compliance Risks

Fintech

Fintech

Crypto

Crypto

iGaming

iGaming

Forex

Forex

Social Network

Social Network

Marketplace

Marketplace

Banking

Banking

Gig Economy

Gig Economy

Payments

Payments

Ride Hailing

Ride Hailing

Adult Content

Adult Content

Blind Spot Audit

Blind Spot Audit

Deepfake Detector

Deepfake Detector

Liveness Spoofs

Liveness Spoofs

Document Originality

Document Originality

Document Deepfake

Document Deepfake

Global Trust Platform

Global Trust Platform

Journey Builder

Journey Builder

Case Management

Case Management

Shufti AI

Shufti AI

Fraud Analytics

Fraud Analytics

Vendor Comparison

Vendor Comparison

Brand Personalisation

Brand Personalisation

AI Compliance Co-Pilot

AI Compliance Co-Pilot

OCR

OCR

Secure Capture

Secure Capture

Deployment Options

Deployment Options

Identity Methods

Identity Methods

API Documentation

API Documentation

Mobile SDKs

Mobile SDKs

Service Status

Service Status

Help Center

Help Center

Contact Us

Contact Us

Technical Support

Technical Support

Supported Documents

Supported Documents

Supported Countries

Supported Countries

Content library

Content library

Blogs

Blogs

News

News

Reports

Reports

Knowledgebase

Knowledgebase

ROI calculator

ROI calculator

About

About

Career

Career

Press Release

Press Release

Certifications

Certifications

Partnership

Partnership

Awards

Awards

Events & Webinar

Events & Webinar

Interactive Demo

Interactive Demo

Podcast Studio

Podcast Studio

Banking

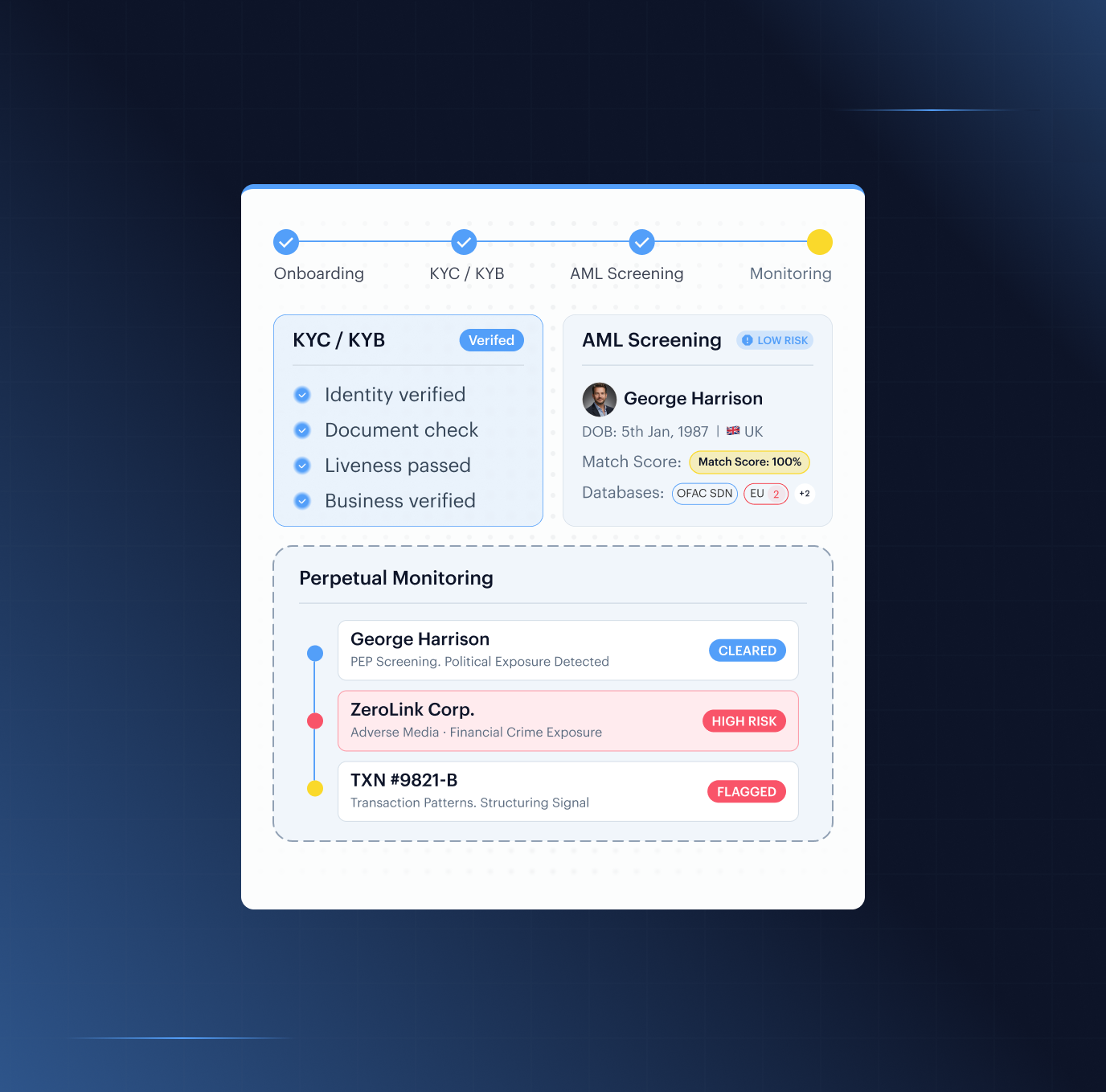

One platform to verify, screen & monitor every bank customer from onboarding to closure

KYC, KYB, AML screening and perpetual monitoring in one integration. No aggregators. No fragmented audit trail. Full data processor status under GDPR Article 28.

Proven Performance

Our Impact, By The Numbers

- <30sMedian Time-to-Decision

- 4,000+Watchlists Screened

- 240+Regions Actively Processed

Trusted by Leading Digital Enterprises Worldwide

Compliance Without Compromise

Why Banks Choose Shufti

-

Stay Examination-Ready

TD Bank's $3.09 billion BSA/AML settlement in October 2024 confirmed what examiners already expect: fragmented compliance stacks cannot produce a unified audit trail. OCC Bulletin 2023-17 and AMLD6 (transposition deadline 10 July 2027) require banks to evidence every CDD and EDD decision from a single, auditable source. Shufti's in-house AML compliance platform stores every verification, screening, and monitoring decision in a tamper-evident log, exportable in under five minutes.

-

Stop Fraud Before It Onboards

Synthetic identity fraud is the largest single fraud loss vector in retail banking. AI-generated documents and deepfake biometrics now pass legacy verification checks. ISO/IEC 30107-3 PAD Level 3 certification, confirmed by iBETA in May 2026 with 0% APCER and 0% BPCER, validates that Shufti's passive liveness detection rejects the attack vectors that older systems miss.

-

Scale Without Adding Vendors

67% of banks have lost clients due to slow, inefficient onboarding. Every additional vendor adds integration debt, a separate DPA and another gap in the audit trail. A single REST API covering document verification, biometric liveness, AML screening, KYB with UBO resolution, and perpetual monitoring replaces three to five vendor relationships with one.

Secure Every Stage Of The Banking Customer Lifecycle

Sign Up

Bot Account Farming

A fraud ring uses scripts to bulk-register current accounts, exploiting welcome bonuses and free overdraft offers. Shufti's proprietary Device Fingerprinting identifies shared emulator stacks and proxy rotation at the point of registration. Behavioural Biometrics detects machine-speed form completions before any account is created.

Synthetic Identity Registration

An attacker blends real and fabricated PII to open an account that passes format checks but has no genuine financial history. Shufti's eIDV cross-references declared details against government and credit bureau records in real time, while Fraud Hub flags identity packages linked to previously rejected synthetic profiles.

Mule Recruitment Onboarding

Real individuals recruited via fake job adverts or romance scams open current accounts to layer criminal proceeds. Shufti's eIDV checks identity signals against known mule recruitment patterns, and AML Screening screens each applicant against mule ring watchlists at point of sign-up, flagging the account before it is opened.

Stolen Identity Application

A fraudster uses breached PII to open a bank account entirely without the victim's knowledge. Shufti's eIDV flags contact details that don't match the identity's known financial footprint, and Facial Biometrics independently requires a live selfie to confirm the applicant is the genuine document holder.

Duplicate Registration

One person registers multiple accounts under name variations to exceed FSCS limits or claim sign-up bonuses more than once. Shufti's 1:N Facial Deduplication continuously catches the same biometric appearing under different submitted identities, and Device Fingerprinting links applications from shared infrastructure before any account is approved.

Velocity and Anomaly Attacks

Fraud rings flood the bank's sign-up flow from shared infrastructure during peak hours to slip accounts past manual review queues. Shufti's Device Fingerprinting identifies coordinated hardware and network signals across near-simultaneous applications, and Fraud Hub intelligently correlates the velocity pattern against prior rejection events to flag the entire cluster.

Verify Identity (KYC)

Document Forgery

A fraudster submits a tampered or AI-generated government ID purchased from dark-web markets. Shufti's proprietary Document Verification applies forensic tamper detection across any government-issued document, checking MRZ consistency, font integrity and AI-generated artefacts. NFC Verification reads the cryptographic chip in e-passports and chip-enabled IDs, bypassing image manipulation entirely.

Deepfake and AI Face Attack

An attacker presents an AI-generated face video during the bank's selfie step to impersonate a real account holder. Shufti's Facial Biometrics (iBETA PAD Level 3, 0% APCER) uses 3D depth analysis and micro-movement detection to distinguish a live face from a synthetic video. Injection Detection independently identifies virtual camera drivers at OS level before biometric capture begins.

Camera Injection Attack

A fraudster injects a pre-recorded or synthetic image into the bank's KYC verification stream, bypassing the physical camera. Shufti's Injection Detection identifies virtual camera drivers at OS level before biometric capture begins, and Facial Biometrics adds a defensible liveness layer that rejects the injected feed even if the injection attempt is evaded.

Identity Pack Fraud

Dark-web KYC kits pair a forged bank ID with a synthetic selfie, designed to clear full onboarding in a single coordinated submission. Shufti's NFC Verification requires the cryptographic chip a purchased kit cannot replicate, stopping packaged fraud at source. Document Verification runs independent forensic checks on the physical document, and eIDV cross-references the declared identity against authoritative data sources.

Business Ownership Concealment

A sanctioned or criminal UBO hides behind nominee directors and layered holding structures when opening a business bank account. Shufti's Business Verification traces the full ownership chain across 140+ jurisdictions to identify the true beneficial owner, and AML Screening intelligently screens every UBO in real time against 4,000+ watchlists and 215+ sanctions regimes.

KYC Recycling

The same identity package, verified or used fraudulently at another bank, is reused to open additional accounts and avoid re-screening. Shufti's 1:N Facial Deduplication flags the biometric as already linked to a known identity even when different documents are submitted, and Fraud Hub surfaces consolidated prior rejection signals tied to the same underlying identity.

Risk Screening

PEP or Sanctioned Person Onboarding

A politically exposed or sanctioned individual uses aliases or transliterated name variants to slip past the bank's initial name check. Shufti's AML Screening applies fuzzy matching across 4,000+ watchlists and 215+ sanctions regimes, covering all four PEP tiers including close associates. Due Diligence adds a defensible deeper profile check to confirm or exclude the hit before the account proceeds.

Adverse Media Concealment

A customer's criminal or regulatory history exists only in regional or local-language publications that English-only screening tools miss. Shufti's AML Screening covers 50,000+ consolidated adverse media sources in 80+ languages, surfacing negative news regardless of publication language. Due Diligence reviews flagged articles in context and attaches the evidence to the customer's CDD risk profile.

Beneficial Owner Sanctions Concealment

A sanctioned UBO hides behind a chain of nominees, trusts or holding companies during CDD. Shufti's Due Diligence intelligently traces the ownership structure layer by layer, applying the FATF 25% threshold to identify the natural persons in control. AML Screening runs every identified UBO against global sanctions and PEP lists before the banking relationship is approved.

High-Risk Jurisdiction Misrepresentation

A customer based in a FATF grey-listed country declares a false address and uses a VPN to make their IP appear consistent with the claim. Shufti's Address Verification cross-references the declared address against independent authoritative data sources, and eIDV flags the mismatch between the declared jurisdiction and the customer's verifiable data footprint.

Source-of-Funds Fabrication

Fabricated payslips or bank statements are submitted to pass EDD checks on source of funds or source of wealth. Shufti's proprietary Document Verification detects template fraud, font anomalies and digital artefacts in submitted supporting documents, and eIDV cross-references declared income and employment against the applicant's known financial footprint.

Accreditation and Eligibility Fraud

A customer misrepresents their income, tax residency or financial status to access preferential rates, premium products or higher credit limits. Shufti's eIDV validates submitted eligibility documents against authoritative data sources and flags inconsistencies. Document Verification applies forensic analysis to supporting documentation, and AML Screening checks for adverse media or watchlist hits linked to fraudulent financial activity.

Account Opening

Application and Loan Fraud

A customer submits false information on a credit or mortgage application to obtain funds they would not qualify for. Shufti's eIDV validates declared identity fields against government and credit bureau records, flagging mismatches between the application and the verifiable data footprint. Document Verification applies forensic analysis to supporting payslips and bank statements, and QES captures a non-repudiable consent record tied to the verified identity.

Bust-out Fraud

A fraudster builds a convincing credit history over months, then simultaneously maxes out all credit lines and disappears before the bureau updates. Shufti's Fraud Hub tracks behavioural and network signals across the account lifecycle, identifying patterns consistent with bust-out preparation. Transaction Trust Monitoring flags unusual credit utilisation velocity and cross-references the account against others sharing device or identity signals.

Loan Stacking

The same applicant submits simultaneous applications to multiple lenders, taking advantage of the lag before bureau data reflects the first approval. Shufti's Device Fingerprinting links applications from the same underlying device or network across simultaneous submissions. Fraud Hub surfaces the cross-institution pattern and eIDV flags the identity as already active in a concurrent application, giving the lender the signal to pause before approval.

Second-Party Fraud

A real account holder acts as a knowing mule, opening bank accounts for fraudsters or sharing credentials in exchange for payment. Shufti's 1:N Facial Deduplication detects cases where the same face appears across multiple accounts with coordinated application timing, and Fraud Hub cross-references device and identity signals between colluding applicants.

Fraudulent Business Account Application

A newly incorporated shell company applies for a business bank account with the sole purpose of accessing credit facilities or laundering funds through a legitimate-looking structure. Shufti's Business Verification flags entities with no genuine operating history, Due Diligence maps the ownership chain to identify UBOs with sanctions or PEP exposure, and AML Screening screens each identified person before the account is opened.

First-Party Fraud

A legitimate customer intentionally submits inaccurate income or employment data to obtain better credit terms or a higher overdraft limit. Shufti's eIDV cross-references declared income and residency against authoritative data, flagging fields that cannot be corroborated. Document Verification checks supporting documents for forensic signs of editing, and Fraud Hub matches the application against known first-party fraud behaviour signals.

Fund Account

Money Mule Deposit

A verified account holder receives criminal funds from third parties and rapidly moves the balance to external destinations. Shufti's Transaction Trust Monitoring intelligently detects the third-party funding pattern and flags the rapid inbound-to-outbound sequence in real time, while AML Screening checks each inbound transfer against sanctions and watchlist data.

Structuring and Smurfing

Criminal proceeds are broken into multiple sub-threshold cash deposits timed to avoid triggering CTR and AML alerts. Shufti's Transaction Trust Monitoring continuously analyses deposit patterns over time, detecting consistent sub-threshold amounts that form a structuring pattern. Fraud Hub surfaces coordinated activity across accounts sharing device or identity signals, identifying the mule ring before the total laundered value accumulates.

Stolen Card Funding

A stolen debit or credit card is used to fund a bank account before a rapid cash-out event. Shufti's proprietary Device Fingerprinting flags devices with known fraud associations at the point the funding instruction is submitted, and Transaction Trust Monitoring detects the deposit-to-withdrawal velocity that characterises stolen card cashing schemes.

Chargeback Fraud

A customer funds their account, extracts the value, then disputes the original funding charge with their card issuer to recover the payment. Shufti's Consent Verification captures a timestamped, non-repudiable record of the funding authorisation tied to the verified account holder, eliminating the repudiation basis when the dispute is raised.

Terrorist Financing

Funds deposited into a bank account are linked to a FATF-designated terrorist organisation, structured to appear below reporting thresholds. Shufti's AML Screening checks every inbound funding event against terrorism financing watchlists, PEP lists and adverse media in real time. Transaction Trust Monitoring flags the deposit velocity and source pattern, escalating the account for immediate SAR review.

Transact / Pay

Authorised Push Payment (APP) Fraud

A bank customer is socially engineered into authorising a payment to a fraudster's account. Shufti's Behavioural Biometrics detects hesitation and interaction patterns inconsistent with a routine self-initiated transfer. Consent Verification captures a timestamped authorisation record satisfying UK PSR reimbursement evidence requirements, and Transaction Trust Monitoring flags the destination against known APP fraud indicators.

Romance and Investment Scams

A bank customer is manipulated over weeks into authorising large transfers to fake investment platforms or romance fraudsters. Shufti's Behavioural Biometrics identifies interaction patterns consistent with an emotionally manipulated customer during payment authorisation. Transaction Trust Monitoring flags unusual destinations and escalating payment amounts, and Consent Verification records the authorisation event to support the bank's regulatory reporting obligations.

Impersonation Scams

A fraudster impersonates a bank, regulator or law enforcement officer to coerce the customer into urgently authorising a transfer. Shufti's Behavioural Biometrics detects authorisation events executed under unusual pressure, flagging deviation from the customer's established payment patterns. Transaction Trust Monitoring checks the destination against known impersonation scam indicators, and Consent Verification creates a timestamped record supporting any reimbursement claim.

Layering and Structuring

Illicit funds are moved through multiple transactions and accounts to obscure their origin before placement into the legitimate economy. Shufti's Transaction Trust Monitoring analyses the full transaction sequence rather than individual events, identifying layering patterns including cross-account flows and round-number amounts. AML Screening adds a watchlist check at each transaction event, ensuring a newly sanctioned counterparty does not receive funds already in motion.

Withdraw / Transfer

Account Takeover Withdrawal

An attacker who has compromised a bank account attempts to drain the balance to an external account. Shufti's Biometric Face Authentication requires a live selfie matched to the enrolled KYC record for any withdrawal above the configured threshold, so a stolen password or OTP alone cannot authorise the transfer. Device Fingerprinting flags withdrawal attempts from unrecognised devices.

Transfer to Sanctioned Account

A customer initiates a transfer to a beneficiary account linked to a sanctioned entity or OFAC-listed individual. Shufti's AML Screening checks every destination account against live sanctions databases, 4,000+ global watchlists and 215+ sanctions regimes before the transfer executes. Transaction Trust Monitoring flags destination accounts matching patterns associated with illicit fund movements even when no direct sanctions hit is returned.

Rapid Cash-Out Scheme

Funds are deposited and withdrawn within minutes, completing the full cycle before monitoring alerts can fire. Shufti's Transaction Trust Monitoring detects the deposit-to-withdrawal velocity in real time and applies an automatic hold on full-balance withdrawals following recent funding. Biometric Face Authentication requires biometric re-verification before the hold can be lifted.

Invoice Redirection

Payment instructions are intercepted and replaced with the fraudster's account details, causing the customer to transfer funds to the wrong beneficiary. Shufti's Biometric Face Authentication requires biometric re-verification when a new beneficiary is added, ensuring the instruction change was made by the genuine account holder. Transaction Trust Monitoring flags the first payment to a newly added beneficiary for review.

Fraudulent Beneficiary Addition

An attacker with partial account access adds their own bank account as a payout destination, ready to drain funds later. Shufti's Biometric Face Authentication requires a live selfie matched to the enrolled KYC record before any new payout destination is confirmed, making partial access insufficient to complete the addition. Device Fingerprinting triggers a step-up challenge if the change originates from an unrecognised device.

Account Management

Password Reset Account Takeover

An attacker intercepts a password reset via SIM swap or email compromise to gain full account control. Shufti's Biometric Face Authentication requires a live selfie matched to the enrolled KYC record as part of the recovery flow, so control of the phone number alone cannot complete the reset. MFA with TOTP eliminates the SMS interception vector, and Device Fingerprinting escalates recovery attempts from unrecognised devices.

Support Social Engineering

An attacker uses stolen PII to impersonate a genuine customer in a bank support interaction, requesting account changes or credit limit increases. Shufti's Biometric Face Authentication requires biometric re-verification for any sensitive account modification, so PII knowledge alone cannot authorise the request. Behavioural Biometrics flags anomalies that distinguish a scripted attacker from the genuine account holder.

Identity Detail Change to Evade Screening

A customer who has received an AML flag attempts to alter their registered name or address to reset or bypass the screening result. Shufti's AML Screening re-runs automatically on any change to core identity fields, screening updated details against 4,000+ watchlists immediately. Document Verification confirms any new supporting documents are genuine, and eIDV cross-references new details to determine whether the change is legitimate or evasive.

Limit Upgrade Document Fraud

A customer submits forged documents to move to a higher transaction tier or lower-risk jurisdiction classification. Shufti's Document Verification applies full forensic checks at the upgrade stage, including tamper detection, template analysis and MRZ validation. NFC Verification checks any chip-enabled document to bypass image manipulation, and the submitted face must match the biometric enrolled at account opening.

Session Hijacking

A stolen session token is used to change bank account settings or add beneficiaries without triggering a new login event. Shufti's Behavioural Biometrics monitors interaction patterns throughout the session, detecting when the person operating the account changes mid-session. Device Fingerprinting corroborates whether the session originates from the account's established device environment, and a behavioural deviation triggers automatic re-authentication.

MFA Fatigue Attack

An attacker floods the legitimate bank customer with repeated MFA push notifications until one is accepted in frustration or by mistake. Shufti's MFA implementation limits prompt frequency and escalates repeated rejections as a fraud signal. Biometric Face Authentication replaces SMS-based MFA for high-risk account actions, so accepting a pushed notification is insufficient to authorise a sensitive change.

Account Maintenance

Sanctions Re-listing Not Caught

A customer clean at onboarding is subsequently added to a sanctions or PEP list, and the bank's annual review cycle doesn't catch it for months. Shufti's Ongoing AML Screening monitors all active customer records against watchlist updates on a 15-minute refresh cycle, firing an immediate alert when a customer is re-designated. Perpetual KYC routes the flagged account into an EDD workflow automatically, without waiting for a compliance analyst.

Risk Profile Drift

A customer's transaction behaviour gradually shifts toward money laundering patterns without the static risk rating assigned at onboarding ever being updated. Shufti's Perpetual KYC monitors behavioural and transactional signals continuously and updates the customer's risk score dynamically. When the score crosses a configured threshold, Transaction Trust Monitoring escalates the account to enhanced review automatically.

Periodic Review Evasion

A customer suppresses suspicious activity in the weeks before a known annual review date, then resumes the behaviour once it passes. Shufti's Perpetual KYC is event-driven rather than calendar-driven, evaluating the full account history rather than a snapshot at review time. A suppression-then-resumption pattern generates a score change that triggers review regardless of when it falls in the calendar.

PEP Status Change Not Reflected

A bank customer's PEP status changes after onboarding, but the CDD record continues applying standard due diligence rather than the enhanced level required. Shufti's Ongoing AML Screening detects PEP designation changes within the 15-minute refresh cycle and immediately reclassifies the customer. Perpetual KYC triggers an EDD workflow automatically, prompting updated source-of-funds documentation.

Emerging Adverse Media

Negative news linking an existing bank customer to fraud, corruption or organised crime surfaces in a regional publication after their account was opened. Shufti's Ongoing AML Screening monitors 50,000+ adverse media sources continuously, surfacing new articles within the watchlist refresh cycle. AML Screening attaches the media evidence to the customer's risk profile, giving the compliance team a sourced, severity-classified alert rather than a raw news hit.

Identity Swap at Re-Verification

A customer submits different identity documents at scheduled re-KYC, claiming the original ID was lost, in an attempt to assume a different identity or clear a prior flag. Shufti's Facial Biometrics requires the current selfie to match the biometric enrolled at original account opening, regardless of which new documents are presented. Document Verification applies forensic analysis to newly submitted documents.

Account Closure

Pre-SAR Closure

A customer who suspects an AML investigation requests account closure and invokes GDPR erasure to destroy the transaction history before a SAR can be filed. Shufti's regulatory retention configuration enforces BSA five-year and FATF Recommendation 11 minimum retention periods that cannot be overridden by a customer erasure request. Transaction Trust Monitoring and AML Screening run a final history review as closure is processed, and any SAR obligation is assessed before the closure is processed.

Balance Extraction Before Closure

A customer executes a full-balance withdrawal immediately after receiving a compliance communication, then submits a closure request to close the account before a hold can be placed. Shufti's Transaction Trust Monitoring flags full-balance withdrawal events that follow compliance-related account activity and applies an automatic hold pending review. Biometric Face Authentication is required to proceed, ensuring the withdrawal is authenticated against the enrolled identity before any funds are released.

Re-application Under New Identity

An offboarded bank customer reapplies using different identity documents to bypass the closure record. Shufti's 1:N Facial Deduplication screens every new applicant's selfie against all previous accounts, including deactivated and rejected ones, flagging the biometric match before the new application proceeds. AML Screening checks the new identity against watchlists.

Bust-out at Closure

A customer maxes out all available credit lines immediately before submitting a closure request, completing the drawdown before the bank can place a hold. Shufti's Transaction Trust Monitoring detects rapid credit utilisation preceding a closure request, which differs significantly from normal wind-down behaviour. Fraud Hub cross-references the account against others with coordinated bust-out timing.

Regulatory Data Destruction Request

A customer requests deletion of transaction records required to be retained under BSA, FATF or local AML legislation, citing GDPR rights. Shufti's retention policy enforces statutory minimums that cannot be overridden by a customer request, while deleting data genuinely outside the retention period. The system generates a deletion certificate for each item removed and a separate retention notice for records that must be kept.

Built For Every Role That Owns The Onboarding Decision

Combine products across identity, compliance, and fraud defence to build a verification stack that meets your regulatory requirements; without rebuilding the integration each time the rulebook changes.

CCO

Stop manually reconciling vendor data for each examination. Shufti generates a unified, jurisdiction-specific evidence package for every customer, updated continuously by the in-house compliance engine. Every CDD, EDD, AML screening and monitoring decision is stored in a single tamper-evident log, exportable in under five minutes.

Head of Digital Banking

67% of banks lose customers at identity verification. Risk-tier orchestration applies lighter checks to low-risk applicants and reserves document capture and biometric liveness for higher-risk profiles. Median time-to-decision stays below 30 seconds without cutting compliance on the segments that need it most.

Head of Engineering

One REST API covers the full customer lifecycle: document verification, biometric liveness, AML screening, KYB with UBO resolution, and perpetual monitoring. Sandbox setup takes under five minutes. SR 11-7 model-review evidence packages are available for AI/ML model validation. 99.95% uptime across all regions in the trailing 12 months.

Fraud Analyst

A unified Fraud Hub surfaces the reason behind every flag before the case is opened. Cross-customer network signals, device links, and biometric deduplication results appear in one view. Manual review time falls because context is already assembled when the alert fires.

Don’t just take our word for it, hear from our customers

The Confidence Our Clients Share

The future of digital identity is defined by trust, interoperability, and regulatory alignment, so our partnership with Shufti reinforces DevCode Identity’s commitment to supporting our global customers with the most secure, best-in-class, compliant identity verification solutions available today.

Combining our Conversion Driven Compliance Orchestration Platform with Shufti’s global KYC and IDV capabilities allows our customers not only to navigate complex regulatory demands but also to maintain a seamless customer onboarding experience with the highest achievable conversion rates.

We’re proud to continue our partnership with Shufti as we expand into new jurisdictions.

Shufti’s verification technology not only strengthens our compliance framework but also ensures our players enjoy a smooth, secure onboarding experience.

We aim to offer our clients and their traders the very best tools with which to do their jobs, we’re excited to be able to work with Shufti.

They’re a leading company, and we’re looking forward to offering their solutions to our clients through our CRM.

The relationship with Shufti was born out of frustration with an existing provider, so we started our discussion with Shufti.

The response time was excellent, from the start of speaking to sales to getting up and running with the demo.

Everything you need to know in one place

Frequently Asked Questions

Banks in the US are subject to the BSA, the PATRIOT Act CIP requirements and the FinCEN CDD Final Rule (31 CFR § 1010.230). EU-supervised banks must comply with AMLR 2024/1624, which applies from 10 July 2027, and AMLD6, which member states must transpose by the same date. OCC Bulletin 2023-17 governs third-party risk for US national banks. FATF Recommendations 10, 11 and 17 apply globally.

Risk-based orchestration routes low-risk customers through passive eIDV and reserves document capture and biometric liveness for higher-risk profiles. Every route produces a CIP-compliant evidence package with extracted fields, document hashes and confidence scores. Median time-to-decision is under 30 seconds at P50.

ISO/IEC 30107-3 PAD Level 3 is the highest independent certification tier for presentation attack detection. iBETA tested Shufti's passive liveness system against physical artefacts, video replay attacks and deepfake injection vectors in May 2026. The system passed with 0% APCER and 0% BPCER on both iOS and Android, making Shufti the third company globally and the first European company to achieve this conformance.

Shufti operates as a data processor under GDPR Article 28 and UK DPA 2018. The bank retains full controller status. A single DPA covers all Shufti products. Data residency options include EU, UK and US hosting. Deletion certificates are generated for every erasure request, exportable for examination and audit purposes.

Yes. Deployment options include cloud (SaaS), hybrid, on-premise and private cloud. For banks with data sovereignty requirements or internal policies against cloud processing of biometric data, the full verification and screening stack runs within the bank's own infrastructure. All deployment models produce the same tamper-evident audit trail and evidence exports.

Sandbox setup takes under five minutes. Production integration typically takes two to eight weeks depending on the number of verification flows configured and whether on-premise deployment is required. A single REST API covers the full customer lifecycle, which eliminates the multi-vendor integration cycles that extend most deployment timelines.

Examination-ready banking compliance from day one

BSA, AMLR, FATF and OCC 2023-17 require a verification architecture that connects onboarding identity to ongoing transaction monitoring. Fragmented vendor stacks cannot produce a unified audit trail, cannot share identity records across compliance functions, and cannot update rules from a single source. Evaluate whether your current stack meets that standard.