eKYC stands for electronic Know Your Customer, is the digital process of verifying a customer’s identity remotely using automated technology instead of in person, paper based checks. A complete eKYC flow combines document authentication, biometric face matching, liveness detection, and sanctions screening, returning a verification decision in under a minute.

Key takeaways

|

This guide explains what eKYC is, how the process works step by step, how it compares to traditional KYC and Video KYC, the global regulations shaping it, the challenges businesses face when implementing it, and what to look for in an eKYC platform. It is written for compliance, product, and growth teams who need a reliable picture of the field, not a marketing brochure.

What is eKYC Meaning?

|

eKYC (electronic Know Your Customer) is a digital identity verification process that confirms a customer is who they claim to be using a combination of ID document checks, biometric face matching, liveness detection, and watchlist screening, all completed remotely through a mobile, web, or kiosk channel. |

eKYC modernises the traditional, branch-based KYC process by moving every step online. Customers submit a government-issued ID and a selfie through their device. Automated systems extract and validate the document data, match the selfie to the photo on the ID, confirm the person is physically present rather than a spoof, and screen the customer against sanctions, politically exposed persons, and adverse media lists. The outcome is a single decision (approve, refer for review, or reject) with a full audit trail attached.

Across regulated industries such as banking, fintech, crypto, lending, insurance, online gaming, and telecoms, eKYC has become the default onboarding method. It satisfies the same anti money laundering and counter terrorism financing obligations as traditional KYC verification, but completes them in seconds rather than days, and at a fraction of the cost.

eKYC vs Traditional KYC: Key Differences

The compliance outcome is identical. The execution is not. The table below summarises the practical differences between paper based KYC and modern, automated eKYC.

| Aspect | Traditional KYC | eKYC |

|

Channel |

In branch or mailed documents | Mobile, web, kiosk |

| Document handling | Physical copies, manual review |

Digital capture, automated forensics |

|

Identity match |

Visual comparison by staff | Biometric face match plus liveness |

| Time to decision | Hours to days, sometimes weeks |

Seconds to minutes |

|

Cost per check |

High (staffing, premises) | Low (per API or per check pricing) |

| Customer reach | Limited to branch network |

Global, 24 by 7 |

|

Audit trail |

Paper files | Tamper-evident digital logs |

| Drop-off rate | High due to friction |

Lower with risk based orchestration |

| Fraud detection | Reliant on reviewer experience |

AI driven forensics and deepfake defence |

The shift to eKYC is no longer optional in most consumer facing financial services. Customers expect to open an account from their phone in minutes, and regulators in the EU, Singapore, Qatar, India, and other jurisdictions have published explicit guidance on how remote, automated identity verification should be conducted.

How the eKYC Process Works (Step by Step)

Modern eKYC follows a layered architecture. Each step adds an independent control, and most steps run in parallel rather than sequentially. The customer experiences a single, short flow; the platform runs dozens of checks underneath.

1. Customer enrolment

The customer initiates onboarding through a brand’s app, website, or partner channel. Consent for data processing and biometric capture is collected upfront. A well designed eKYC SDK embeds directly into the host app so the customer never feels they have been routed to a third party.

2. Document capture and authentication

The customer is prompted to photograph a government issued ID. Behind the scenes, the platform runs:

- Optical character recognition (OCR) to extract name, date of birth, document number, and issue and expiry dates.

- MRZ parsing and checksum validation for passports and machine-readable ID cards.

- Barcode and PDF417 reads for driving licences.

- NFC chip authentication where the document supports it, reading the cryptographically signed data stored on the chip.

- Visual forensics to detect tampering, photo substitution, font anomalies, security feature inconsistencies, and signs of fully synthetic documents.

If the document fails quality or authenticity checks, the customer is asked to retake the image rather than the case being rejected outright. See Shufti’s document verification service for the full feature set.

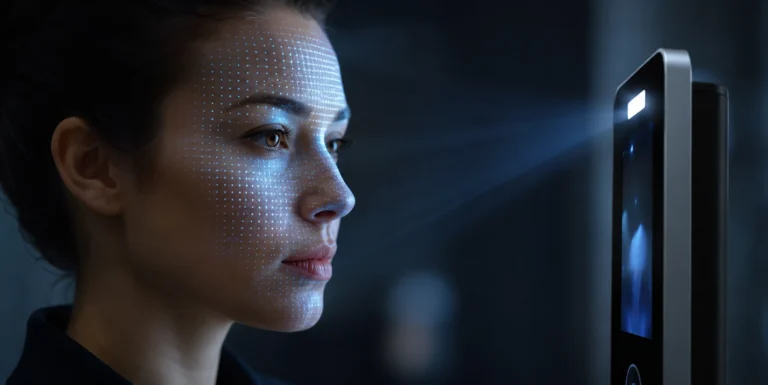

3. Biometric verification (face matching)

The customer captures a selfie. The eKYC engine compares it to the photo extracted from the ID using deep learning face recognition models, producing a similarity score against a configurable threshold. Strong platforms benchmark their matching algorithms against the NIST Face Recognition Vendor Test (FRVT) to provide an objective measure of accuracy across demographics. Read more about Shufti’s face verification capabilities.

4. Liveness detection

Face match alone is insufficient. Liveness detection, also known as Presentation Attack Detection (PAD), confirms that the selfie is from a real, present person rather than a photo, screen replay, 3D mask, or AI-generated deepfake. Two approaches are common:

- Passive liveness: analyses a single image or short video clip for spoofing artefacts without asking the customer to do anything. Lowest friction, best for high conversion flows.

- Active liveness: prompts the customer to perform a short action such as a blink, smile, or head turn. Higher assurance, used for higher risk flows or where regulators mandate it (Qatar Central Bank, for example, requires active liveness for unattended onboarding).

Independent certification against the iBeta PAD standard, particularly Level 2 and Level 3, is the production benchmark. Shufti’s biometrics are iBeta Level 3 certified. With deepfakes accelerating, robust deepfake detection is now a non-negotiable layer of the eKYC stack.

5. AML, sanctions, and PEP screening

Extracted identity data is screened against global sanctions lists (OFAC, UN, EU, HMT, and national lists), PEP databases, and adverse media sources. Matches are scored and routed to compliance review where required. This step is core to AML compliance and customer due diligence obligations under the FATF Recommendations.

6. Risk based orchestration and decisioning

A mature eKYC platform does not run the same flow for every customer. Risk based orchestration adjusts the steps based on jurisdiction, product, customer profile, and real time signals. A low risk applicant from a low risk geography may pass through passive liveness and database checks only. A higher risk applicant may face active liveness, additional document checks, source of funds questions, or a fallback to Video KYC.

The final output is a decision plus a full evidence package: captured documents, biometric scores, liveness results, screening hits, device signals, and a timestamped log of every check, ready for the next regulatory examination.

The Four Data Signals Used in eKYC

eKYC draws on a broader signal set than its paper predecessor. These signals fall into four categories. The power lies in cross checking them against one another, not in any single one.

Active signals

Information the customer provides directly: name, address, date of birth, national identification number, employment details, source of funds, and submitted documents such as ID, selfie, and proof of address.

Third party data

Data sourced from external authorities and providers without the customer’s direct input. This includes government registries and electoral rolls, credit bureau records, watchlists (sanctions, PEP, adverse media), phone risk reports, and email reputation reports.

Passive signals

Information emitted by the customer’s device while they complete the flow, captured silently in the background. Common examples include IP address, geolocation, device fingerprint, browser fingerprint, operating system, VPN or proxy use, and time zone consistency.

Behavioral signals

How the customer interacts with the application: typing cadence, hesitation patterns, copy-paste use, autofill detection, mouse movements, and use of developer tools. Behavioural signals help distinguish a real human applicant from a bot or a coached fraudster reading from a script.

An applicant who claims a UK address but presents an IP geolocated in a different region, with an unusually fast form completion and a freshly created email, looks materially different from a typical legitimate customer, even if every individual document passes its own check. Cross-signal correlation is where modern eKYC earns its keep.

eKYC vs Video KYC: When to Use Each

Both eKYC and Video KYC are digital, but they serve different operating contexts.

| Feature | eKYC | Video KYC |

| Human involvement | Fully automated | Live agent on video call |

| Typical duration | 30 to 90 seconds | 3 to 10 minutes |

| Cost per check | Low | Higher (agent time) |

| Scalability | Very high | Limited by agent capacity |

| Best for | Default onboarding, low and medium risk | High risk segments, regulator-mandated assisted flows, fallback when automation fails |

| Customer experience | Self-service, anytime | Scheduled or queue-based |

Most institutions deploy both, using eKYC as the front door and Video KYC as an escalation path. This combination preserves the conversion benefits of automation while keeping a human in the loop for cases that genuinely need one.

Documents Accepted for eKYC Verification

The document set varies by jurisdiction and product, but a mature eKYC platform supports a wide range of identity documents across countries.

| Document type | Notes |

| Passport | Globally accepted. Supports MRZ parsing and NFC chip reads. |

| National ID card | Primary document in most jurisdictions outside the US and UK. |

| Driving licence | Widely accepted in the US, UK, Canada, Australia, and across Europe. |

| Residence permit | For non citizens and long term residents. |

| Voter ID | Accepted in several emerging markets. |

| Government-issued digital ID | Aadhaar (India), Estonia eID, EUDI Wallet (EU, rolling out), state issued mobile driving licences (US). |

| Proof of address | Utility bill, bank statement, or government letter, where address verification is conducted separately. |

Shufti’s eKYC platform supports verification across 240+ countries and territories, with document templates for thousands of identity document variants and form factor changes.

Why eKYC Verification Matters

|

eKYC matters because it enables regulated businesses to satisfy anti-money laundering obligations, prevent identity fraud, and onboard customers remotely at scale, all while delivering the fast, frictionless experience customers now expect. |

Four forces are driving adoption:

- Customer expectations have permanently shifted: Branch visits and multi day waiting periods do not survive against digital first competitors. In the UK, only a minority of younger adults prefer to apply for financial products in person.

- Regulators have endorsed remote verification: The EBA’s guidelines on remote customer onboarding require liveness detection in unattended flows. The Monetary Authority of Singapore has issued guidance for non-face-to-face verification including biometrics. Qatar Central Bank introduced formal eKYC procedures in 2023. India’s Aadhaar based eKYC has been operational for over a decade. FATF guidance on digital identity explicitly recognises that reliable digital identity systems can support customer due diligence.

- Fraud has industrialised: Deepfake selfies, AI generated synthetic IDs, injection attacks, and account takeover automation have raised the cost of weak controls. eKYC platforms with strong liveness and document forensics are now the principal defence at the front door.

- Unit economics demands it: Manual review at scale is uneconomical. An automated eKYC decision costs a fraction of a manual review and operates around the clock without overtime or training overhead.

Benefits of eKYC for Businesses and Customers

For businesses

- Faster onboarding: Verification completes in seconds, lifting application completion rates and conversion.

- Lower cost per verified customer: Less manual review, less back office headcount, lower customer acquisition cost.

- Scalable global reach: A single platform onboards customers across jurisdictions without opening branches.

- Stronger fraud control: Layered document, biometric, liveness, and device checks intercept attacks that manual review would miss.

- Cleaner audit trails: Every check, score, decision, and reviewer action is logged in a tamper evident format for examiners.

- Easier compliance updates: When rules change, configuration changes propagate instantly across the customer base with no retraining of branch staff.

For customers

- Convenience: Onboarding from a sofa, a commute, or another country, on a phone, with no paperwork.

- Speed. Approvals in minutes, not days.

- Consistency: The same experience at 2 pm or 2 am, with no dependence on branch hours.

- Privacy: Fewer humans handle sensitive data because automated systems do most of the work.

Industries Using eKYC

eKYC has spread well beyond traditional banking. Common applications include:

- Banking and fintech: Account opening, lending, credit card issuance, periodic re-verification.

- Crypto and digital assets: Exchange onboarding, wallet KYC, travel rule data exchange.

- Insurance: Policy onboarding, claims verification, beneficiary checks.

- Lending and BNPL: Application screening, identity binding to credit decisions.

- Online gambling and gaming. Age verification, jurisdiction checks, source of funds for high rollers.

- Telecoms: SIM activation in countries where SIM registration is mandatory.

- Healthcare. Patient onboarding, telemedicine identity binding, controlled substance prescriptions.

- Government services: Tax filings, benefits, voter and civil registration in jurisdictions with digital identity programmes.

- Sharing economy and gig platforms: Driver, host, and worker verification.

- Real estate and high-value retail: Identity checks for high-value transactions subject to AML obligations.

For businesses, verifying corporate entities and beneficial owners (not just individuals) is equally important. See Shufti’s KYB verification for the business side counterpart.

eKYC Regulatory Landscape (Global Overview)

eKYC requirements vary materially by jurisdiction. A multi-market programme has to handle each set of rules without fragmenting into siloed flows.

- European Union: The EBA’s guidelines on remote customer onboarding require liveness detection in unattended flows. The eIDAS 2.0 regulation entered into force in 2024, and Member States are expected to issue EU Digital Identity Wallets, opening a new channel for high-assurance verification.

- United Kingdom: The FCA permits and expects digital verification, with the Joint Money Laundering Steering Group (JMLSG) providing guidance. The UK Digital Identity and Attributes Trust Framework is shaping certified digital identity providers.

- United States: Customer Identification Programs under the Bank Secrecy Act allow documentary and non-documentary verification. FinCEN guidance permits digital identity solutions, and an increasing number of states accept digital driving licences.

- Singapore: MAS guidance permits non-face-to-face onboarding with biometrics, and SingPass MyInfo provides a national digital identity rail.

- Qatar: Qatar Central Bank issued formal eKYC procedures in 2023, mandating active liveness in unattended mobile and web onboarding.

- India: Aadhaar-based eKYC, supplemented by Central KYC Records (CKYC), has been operational for years. DigiLocker provides verifiable digital documents.

- FATF: International standards explicitly recognise reliable, independent digital identity systems for customer due diligence, provided risk is appropriately managed.

A reliable eKYC platform abstracts this complexity, allowing compliance teams to configure jurisdiction-specific rules rather than building parallel flows.

Common Challenges in eKYC Implementation

The benefits are well established. The implementation pitfalls are less talked about.

- Deepfakes and AI generated fraud: Generative AI has lowered the cost of producing convincing fake selfies, video replays, and even fully synthetic ID documents. Older liveness systems trained on pre 2022 attack data struggle against current threats. Continuous model retraining and certified PAD coverage are now table stakes.

- Regulatory variance: A rule set that works in Singapore may not satisfy regulators in Frankfurt. Multi-market businesses need configurable flows rather than a single fixed pipeline.

- The friction versus security trade-off: Every additional step costs completion. Adding active liveness, additional document captures, or source of funds questions to the wrong customer segment can create conversion. Risk based orchestration is the answer, but it has to be designed deliberately.

- Tooling fragmentation: When document checks, biometrics, liveness, screening, case management, and reporting live in different tools, compliance teams lose visibility and engineers lose time on integration. A single orchestrated platform is materially easier to operate.

- Phishing and social engineering of the verification flow itself: Fraudsters use real eKYC verification language as a pretext in phishing messages, tricking customers into completing verification on a fake site. Customer education and clear in-app branding mitigate this.

- Manual review still matters: Automation should handle the vast majority of cases. The remainder (edge cases, ambiguous documents, conflicting signals) needs a well-designed review workflow with clear escalation paths.

How to Choose the Right eKYC Solution

The market is crowded. The differences are not always visible on a marketing page. Evaluate against the following criteria:

- Document coverage: Number of countries and document variants supported. Coverage matters when you expand internationally.

- Biometric accuracy: Independent benchmarks such as NIST FRVT for face matching, and iBeta PAD certification for liveness (ideally Level 2, and where possible Level 3).

- Liveness depth: Passive and active options, with documented resistance to current deepfake and injection attacks.

- Decision speed: End-to-end latency for the full flow under realistic load.

- Orchestration: Ability to configure step-up, fallback, and risk-based logic without code changes.

- Integration: Web, iOS, and Android SDKs, plus a clean API for headless flows.

- Compliance and security certifications: ISO 27001, SOC 2, GDPR alignment, and regional AML certifications.

- Auditability: Completeness of evidence logs, reviewer interface usability, and export formats for regulators.

- Data residency: Ability to store data in specific jurisdictions where required.

- Total cost of ownership: Per check pricing plus integration cost, support, and ongoing tuning.

- Roadmap and responsiveness: A vendor’s ability to ship updates as regulations and threats evolve is a material long-term factor.

Best Practices for eKYC Implementation

- Start with a clear risk policy: The eKYC flow should be the operational expression of that policy, not a substitute for it.

- Segment customers by risk: Apply the lightest flow that meets your risk appetite, and step up only where signals warrant.

- Test with real-world fraud samples: Deepfake test sets, recycled ID images, and injection attacks should be part of your acceptance testing.

- Instrument every step: Measure completion, drop-off, false positives, and false negatives at each stage.

- Train your reviewers: Automation handles volume, but humans make the final call on edge cases. Reviewer judgement is a competence to maintain.

- Plan for re-verification: eKYC is not a one-off. Triggered re-verification on high risk activity or expired documents keeps records current.

- Communicate clearly with customers: Tell them why you are verifying, what data you collect, and how it is protected. Trust is conversion.

The Future of eKYC

Three trends are shaping the next phase.

- Reusable digital identity: Wallet-based identity systems such as the EUDI Wallet, India’s DigiLocker, and bank-issued identity wallets allow customers to present pre-verified, cryptographically signed credentials. Verification becomes a credential check rather than a fresh document capture.

- Continuous identity assurance: Onboarding KYC is becoming the first step of an ongoing assurance process. Behavioral biometrics, device intelligence, and transaction monitoring continuously refresh the confidence score attached to a customer.

- AI on both sides of the line: Generative AI is accelerating fraud creation and fraud detection in parallel. The next generation of eKYC platforms will be defined by how well they fight AI with AI, including injection attack defence, synthetic identity detection, and deepfake resistance.

For regulated businesses, the practical takeaway is straightforward: pick a platform built to evolve, not one designed for the threat landscape of three years ago.

How Shufti Powers eKYC Verification

Shufti delivers eKYC verification across 240+ countries and territories, with support for 150+ languages and thousands of document templates. The platform combines AI-driven document authentication, NIST-benchmarked face verification, iBeta Level 3 certified liveness detection, and integrated AML screening into a single orchestrated flow. Verification decisions complete in seconds, with a complete audit trail and full configurability for jurisdiction-specific rules.

If you are building or upgrading your eKYC programme and want to see how Shufti compares against your current stack, our team is ready to walk through the platform with you. Talk to Shufti for a tailored demo.

Conclusion

eKYC has moved from “promising technology” to standard operating practice. For regulated businesses, the question is no longer whether to adopt it but how to implement it well: with strong liveness, broad document coverage, configurable risk-based orchestration, clear audit trails, and a vendor capable of keeping pace with both regulators and fraudsters.

Built deliberately, eKYC delivers the rare combination compliance and growth teams both want: fewer fraud losses, faster onboarding, lower cost per customer, and an experience that customers actually finish.

Book a personalised demo with Shufti and see how a single platform can replace four point solutions.

Frequently Asked Questions

What Does eKYC Stand For? (Full Form of eKYC)

The full form of eKYC is electronic Know Your Customer. It is the digital process of verifying a customer's identity remotely using technologies such as document verification, biometric face matching, optical character recognition (OCR), and liveness detection. eKYC enables organizations to comply with KYC and anti money laundering (AML) regulations without requiring customers to visit a physical location.

How does eKYC work?

An eKYC process typically begins when a customer uploads a government issued identity document, such as a passport or driver's licence. The system verifies the document's authenticity, extracts relevant information using OCR, performs biometric face matching and liveness detection, and checks the identity against applicable compliance databases. If all verification steps are successful, the customer can usually be onboarded within minutes.

Is eKYC legally valid?

Yes. eKYC is legally recognised in many jurisdictions, including the European Union, the United Kingdom, the United States, Singapore, India, and several Middle Eastern countries. However, regulatory requirements differ by region, so businesses should ensure their eKYC solution complies with local KYC, AML, data protection, and recordkeeping regulations.

What is the difference between KYC and eKYC?

KYC (Know Your Customer) is the regulatory requirement to verify a customer's identity before establishing a business relationship. eKYC is the digital method of fulfilling that requirement using automated identity verification technologies. While traditional KYC often relies on in person verification and paper documents, eKYC streamlines the process through secure online verification, improving speed, accuracy, and customer experience.

How long does the eKYC verification process take?

A fully automated eKYC verification typically takes between 30 and 90 seconds, depending on document quality, internet connectivity, and the complexity of the verification checks. Cases requiring manual review may take longer if additional validation is needed.

Which documents are required for eKYC verification?

Most eKYC solutions accept government issued identity documents such as passports, national identity cards, driver's licences, and residence permits. Depending on local regulations and business requirements, customers may also need to provide proof of address or other supporting documents.

Is eKYC safe, and can it detect deepfakes?

Yes. Modern eKYC platforms use multiple layers of security, including encrypted data transmission, biometric authentication, document forensics, and certified liveness detection to help prevent identity fraud. Advanced solutions can detect many deepfake and presentation attacks, but the strongest protection comes from combining AI powered fraud detection with document verification, device intelligence, and continuous risk monitoring.

Which industries use eKYC?

eKYC is widely used across industries that must verify customer identities and meet regulatory requirements. Common sectors include banking, fintech, cryptocurrency exchanges, lending, insurance, online gaming, telecommunications, healthcare, government services, travel, and digital marketplaces. By automating identity verification, these organizations can accelerate onboarding while reducing fraud and maintaining compliance.