Runs On Your Cloud

Runs On Your Cloud No Data Sharing

No Data Sharing No Contract Required

No Contract Required Explore Now

Explore Now

Face Verification

Face Verification

Address Verification

Address Verification

Document Verification

Document Verification

Age Verification

Age Verification

VideoIdent

VideoIdent

Fast ID

Fast ID

eIDV

eIDV

NFC Verification

NFC Verification

Consent Verification

Consent Verification

Business Verification

Business Verification

Due Diligence

Due Diligence

Investor Verification

Investor Verification

E-Signature

E-Signature

Behavioural Biometrics

Behavioural Biometrics

Device Fingerprinting

Device Fingerprinting

MFA

MFA

AML Screening

AML Screening

Business AML Screening

Business AML Screening

User Risk Assessment

User Risk Assessment

Transaction Screening

Transaction Screening

Adverse Media Screening

Adverse Media Screening

Identity Verification

Identity Verification

KYC

KYC

KYB

KYB

KYI

KYI

Bonus Abuse

Bonus Abuse

Fraud Prevention

Fraud Prevention

Deepfakes

Deepfakes

Banking

Banking

Crypto

Crypto

Fintech

Fintech

Forex

Forex

Gaming

Gaming

Gig Economy

Gig Economy

Marketplace

Marketplace

Social Networks

Social Networks

Product Managers

Product Managers

Compliance Officers

Compliance Officers

Fraud Analyst

Fraud Analyst

Global Trust Platform

Global Trust Platform

Journey Builder

Journey Builder

Vendor Comparison

Vendor Comparison

Content library

Content library

Blogs

Blogs

News

News

Reports

Reports

Insights

Insights

Knowledgebase

Knowledgebase

ROI calculator

ROI calculator

Blind Spot Audit

Blind Spot Audit

Deepfake Detection

Deepfake Detection

Liveness Detection

Liveness Detection

Document Originality

Document Originality

Document Deepfake

Document Deepfake

Events & Webinar

Events & Webinar

Podcast Studio

Podcast Studio

Spotlight Studio

Spotlight Studio

API Documentation

API Documentation

Mobile SDKs

Mobile SDKs

Service Status

Service Status

Help Center

Help Center

Contact Us

Contact Us

Technical Support

Technical Support

Compliance

Compliance

Supported Document

Supported Document

About

About

Career

Career

Press Release

Press Release

Certifications

Certifications

Partnership

Partnership

Awards

Awards

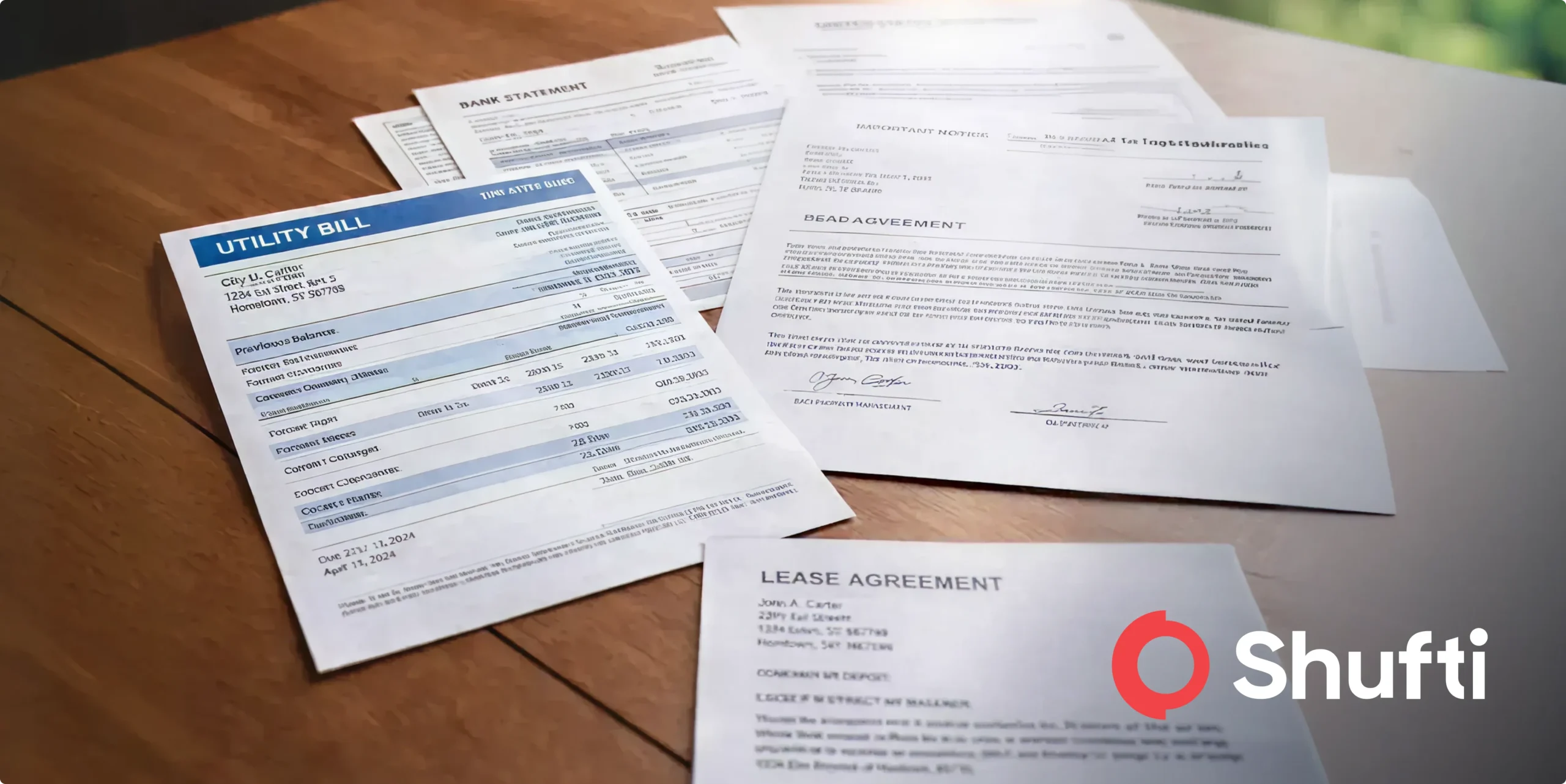

Common Proof of Address Documents for KYC and AML

Verifying proof of address seems the simplest part of the Know Your Customer (KYC) process. However, it becomes more unpredictable when there are hundreds or even thousands of customers that need to be onboarded, and that too globally.

At present, the main challenge with the KYC process is not just that customers fail to submit their documents. The bigger issue is that proof-of-address documents differ widely from one region to another. Most verification systems are not built to handle this variety.

For example, the utility bill required for address verification in Germany will not be the same as one in India. Similarly, a bank statement in the UK follows a different structure from one in Nigeria. Some countries issue digital address certificates, while others still rely on scanned paper letters. Verifying an address has become more than just a document because addresses follow different formats, languages, and abbreviations, creating an operational challenge.

Most KYC systems were built for structured identity, which mainly includes documents like passports, national IDs, and driver’s licenses. However, proof of address documents were treated as secondary inputs. As a result, they were not designed for:

- Regional formatting differences

- Non-latin scripts

- Non-standard layouts

- Mixed digital and paper sources

When compliance teams need to manage onboarding in multiple countries, verifying documents that don’t follow a standard format becomes a big challenge.

Proof of address documents can differ by country, authority, and format. Since fraudsters can easily alter these documents, can compliance teams really use one verification method across all regions? Or do they need a different validation strategy for proof of address compared to identity documents?

This is where many address verification solutions that lack adaptability and understanding of regional nuances fail compliance teams. And that’s why proof of address remains one of the weakest links in KYC and AML controls today.

Commonly Accepted Proof of Address Documents

Despite the lack of global standardization, compliance teams tend to rely on a familiar set of proof of address documents. These documents appear “common” on paper, but in practice, their acceptance depends heavily on local regulation, issuing authorities, and data reliability.

The most widely used proof of address documents include:

- Utility bills (electricity, gas, or water): It includes utility bills like electricity, gas, water, internet, or landline phone. The bill must show the same address as your residence, and some bills (such as mobile phone bills) may not be accepted in certain countries.

- Bank statements: These can be digital or paper bank statements that show your name and address. They must come from a regulated bank, and in some countries, statements from neobanks may not be accepted.

- Government-issued ID showing address: Official government letters, such as tax notices or registration letters, are usually accepted as proof of address.

- Tax letters or assessments: These are official tax documents that show your name and residential address and are commonly accepted as proof of address.

- Rental or lease agreements: These documents confirm your current residence and must clearly display your name and address.

- Mortgage statements: Statements showing your property address as proof of residence.

- Insurance policy documents: Insurance documents that include your name and address can be used as proof of address.

- Employer-issued address confirmation letters: A letter from your employer confirming your residential address may be accepted in some cases.

- Municipal or voter registration letters: These official registration letters show your name and address and are usually accepted as proof of address.

- Social security or pension statements: Official statements including your name and address.

Each of these documents carries different levels of trust depending on the region. What qualifies as “official” in one country may be considered unverifiable in another. Businesses that operate across multiple jurisdictions or seek to scale across borders need an address verification solution trained to handle both Latin and non-Latin scripts, varied layouts, and regional nuances with global coverage.

What Makes the PoA Document Acceptable?

Not all proof of address documents are equally trustworthy. For compliance teams, it’s not just about the type of document; it’s about whether they can verify the information and confidently link it back to the customer.

Reliable issuing authority

To establish a valid proof of address, you need a document from a trusted source. The best proof comes from government agencies, banks, or public utilities because their information can be checked easily. Documents from private individuals, like landlords or employers, are seen as less reliable because it’s harder to verify them.

Time of Issue

Recency of the document is an important factor. Commonly, regulators require proof of address documents to be no older than 90 days. Older documents are more likely to show that a customer’s address has changed, which can make it harder to accurately assess customer risk.

Data clarity

The document must clearly show the customer’s full name and home address, with no missing or incorrect details. Even small mistakes, like a missing apartment number or a misspelt name, can lead to extra checks.

Tamper resistance

Signs of changes, poor image quality, or different fonts often show that a document has been altered. As more people submit documents digitally, it is crucial to check both the document’s content and its accuracy.

Why Verifying Proof of Address is Challenging?

During address verification, even the most basic type of document can pose a challenge. Some of the challenges can be:

Varying Document Templates

Proof of address documents differ drastically across countries and regions. Utility bills, bank statements, and government letters come in different formats, languages, and scripts. Most systems depend on country-specific templates, which are hard to maintain and quickly become outdated when document layouts change. This makes global address verification inconsistent and prone to failure.

Lack of Layout-Aware Extraction

Address documents often contain multiple addresses on the same page — the customer’s address, the issuing authority’s address, branch addresses, and footer contact details. Traditional OCR tools extract all text without understanding context, leading to confusion between the customer’s address and irrelevant issuer information. This results in false rejections and unnecessary manual reviews.

Address Decomposition Is a Major Data Challenge

Addresses are usually written in free-form text rather than structured fields. Different users describe the same address in different ways, mixing landmarks, abbreviations, and local formatting styles. Without breaking addresses into components such as street, unit, city, region, and postal code, downstream systems struggle with matching, storage, and compliance checks.

Fuzzy Matching vs. Strict Matching Dilemma

Small human errors, such as spelling mistakes, abbreviations (Street vs. St.), or formatting differences, can cause legitimate users to fail verification when systems rely on strict matching rules. However, allowing too much flexibility can increase fraud risk. Striking the right balance between accuracy and tolerance remains one of the hardest technical challenges in Proof of Address verification.

How Shufti Resolves PoA Challenges and Speeds Up Verifications?

Address checks often break down when documents vary by country, language, and layout, which pushes more cases into manual review and slows onboarding. Shufti supports proof of address, docless checks, address validation, and geolocation risk signals in one suite to help regulated businesses verify residency with stronger consistency at scale.

Request a demo to see how address verification workflows can be configured for different risk tiers.

: A Growing Threat to Identity Verification Systems")