Runs On Your Cloud

Runs On Your Cloud No Data Sharing

No Data Sharing No Contract Required

No Contract Required Explore Now

Explore Now

Face Verification

Face Verification

Address Verification

Address Verification

Document Verification

Document Verification

Age Verification

Age Verification

VideoIdent

VideoIdent

Fast ID

Fast ID

eIDV

eIDV

NFC Verification

NFC Verification

Consent Verification

Consent Verification

Business Verification

Business Verification

Due Diligence

Due Diligence

Investor Verification

Investor Verification

E-Signature

E-Signature

Behavioural Biometrics

Behavioural Biometrics

Device Fingerprinting

Device Fingerprinting

MFA

MFA

AML Screening

AML Screening

Business AML Screening

Business AML Screening

User Risk Assessment

User Risk Assessment

Transaction Screening

Transaction Screening

Adverse Media Screening

Adverse Media Screening

Identity Verification

Identity Verification

KYC

KYC

KYB

KYB

KYI

KYI

Bonus Abuse

Bonus Abuse

Fraud Prevention

Fraud Prevention

Deepfakes

Deepfakes

Banking

Banking

Crypto

Crypto

Fintech

Fintech

Forex

Forex

Gaming

Gaming

Gig Economy

Gig Economy

Marketplace

Marketplace

Social Networks

Social Networks

Product Managers

Product Managers

Compliance Officers

Compliance Officers

Fraud Analyst

Fraud Analyst

Global Trust Platform

Global Trust Platform

Journey Builder

Journey Builder

Vendor Comparison

Vendor Comparison

Content library

Content library

Blogs

Blogs

News

News

Reports

Reports

Insights

Insights

Knowledgebase

Knowledgebase

ROI calculator

ROI calculator

Blind Spot Audit

Blind Spot Audit

Deepfake Detection

Deepfake Detection

Liveness Detection

Liveness Detection

Document Originality

Document Originality

Document Deepfake

Document Deepfake

Events & Webinar

Events & Webinar

Podcast Studio

Podcast Studio

Spotlight Studio

Spotlight Studio

API Documentation

API Documentation

Mobile SDKs

Mobile SDKs

Service Status

Service Status

Help Center

Help Center

Contact Us

Contact Us

Technical Support

Technical Support

Compliance

Compliance

Supported Document

Supported Document

About

About

Career

Career

Press Release

Press Release

Certifications

Certifications

Partnership

Partnership

Awards

Awards

India

Identity Verification & KYC For India

Unified KYC, KYB, and AML controls aligned to India’s regulatory ecosystem. One platform to capture Aadhaar-led onboarding, verify entities, screen risk, and retain audit-ready evidence across RBI, FIU-IND, SEBI, IRDAI, and MCA expectations.

Operational performance for India KYC

Our Numbers Speak Volumes

96.76%

Pass

rates

< 5 secs

IDV Verification

100%

EIDV

Verification

Evidence-Ready Checks Across People & Businesses

Individual Documents We Verify

Shufti verifies 50+ Individual Documents of India.

View All Supported DocumentsAadhaar (Proof of Possession of Aadhaar)

Primary OVD (Officially Valid Document) route for identity and address in India; supports offline verification, QR validation, and consent-aligned handling.

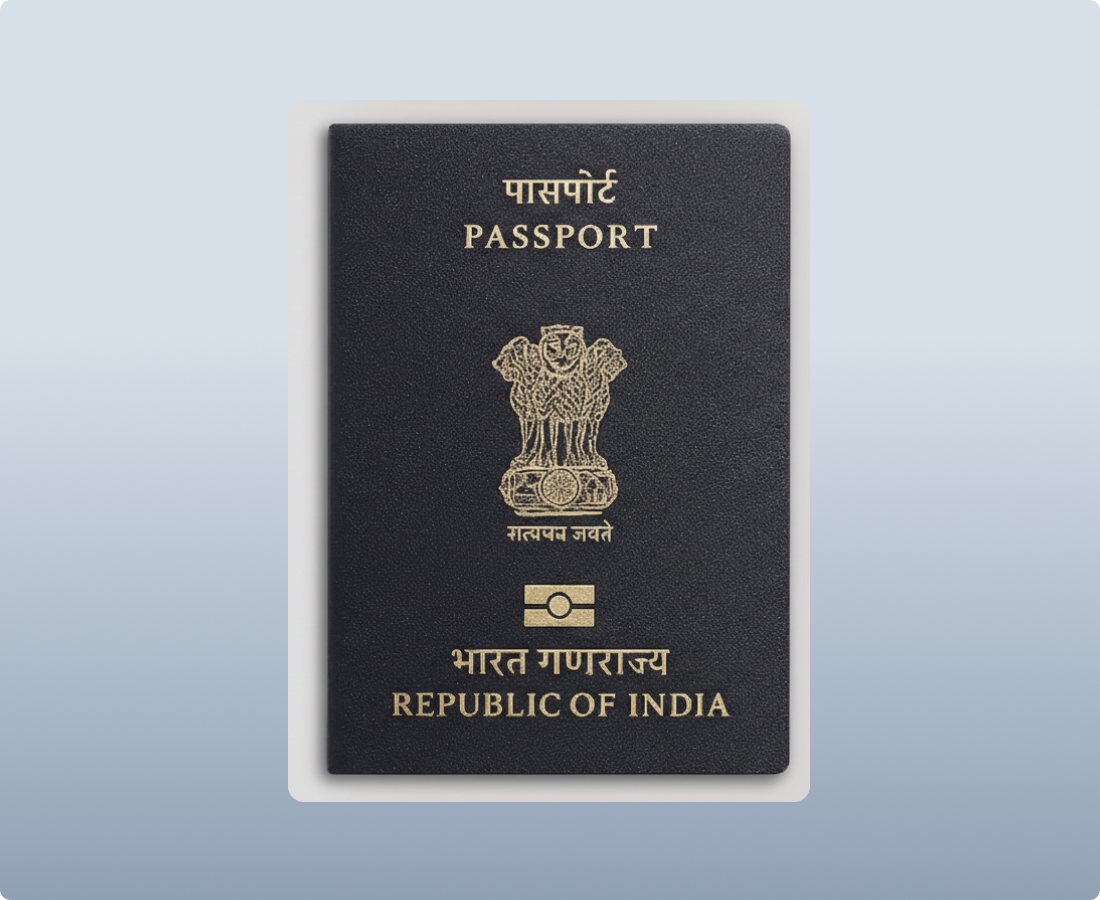

Indian Passport (including e-Passport)

High-assurance photo ID and OVD fallback; MRZ-compliant and used for domestic and cross-border onboarding.

Driving Licence (State-Issued DL)

Recognised OVD for identity and address; state layout variations require resilient capture logic.

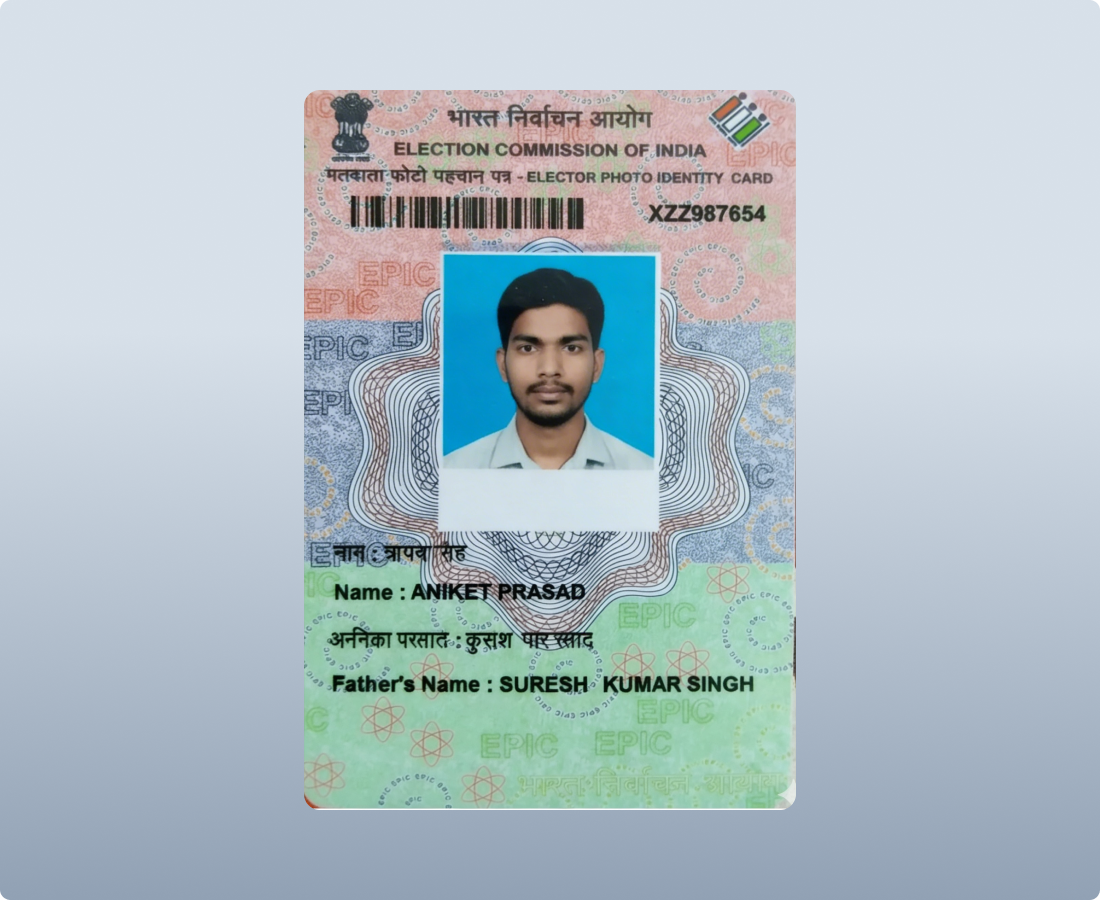

Voter’s Identity Card (EPIC)

Accepted OVD option; often used for address confirmation in financial onboarding.

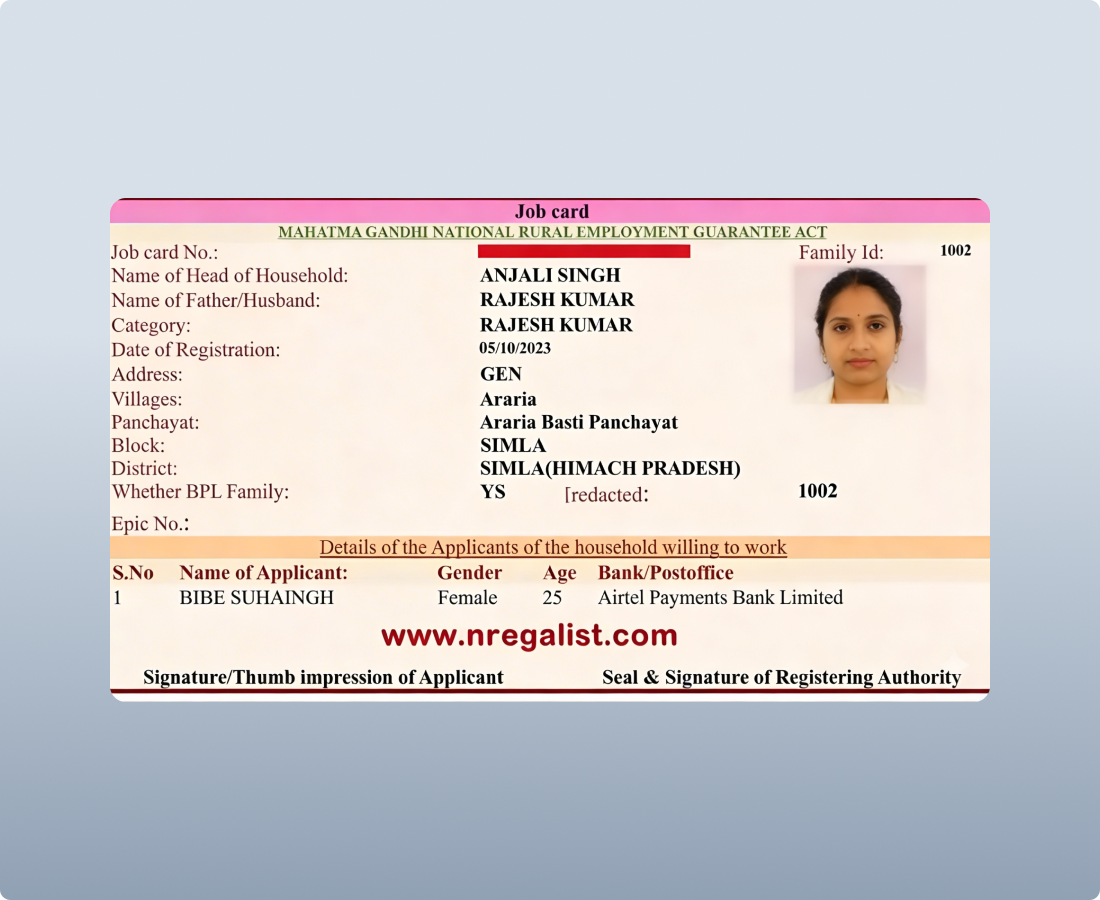

NREGA Job Card

OVD option under rule-based KYC in applicable scenarios; print and format variations require flexible OCR handling.

NPR / UIDAI Letter (as notified OVD)

Letter-based OVD route containing name, address, and Aadhaar number (where applicable).

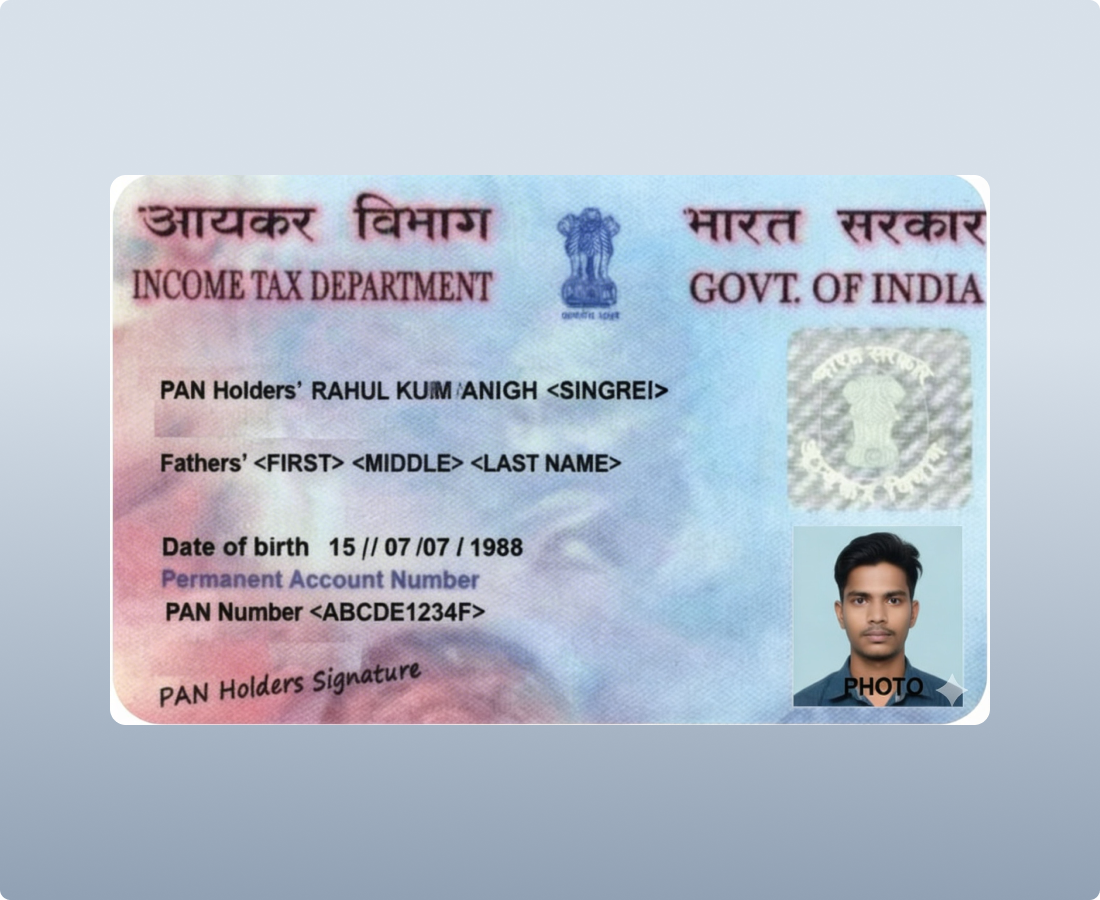

PAN (Permanent Account Number)

Mandatory tax identifier for individuals and entities (or Form 60 where PAN not available); central to CDD and reporting alignment.

Entity Identity

Certificate of Incorporation

Confirms company existence under MCA.

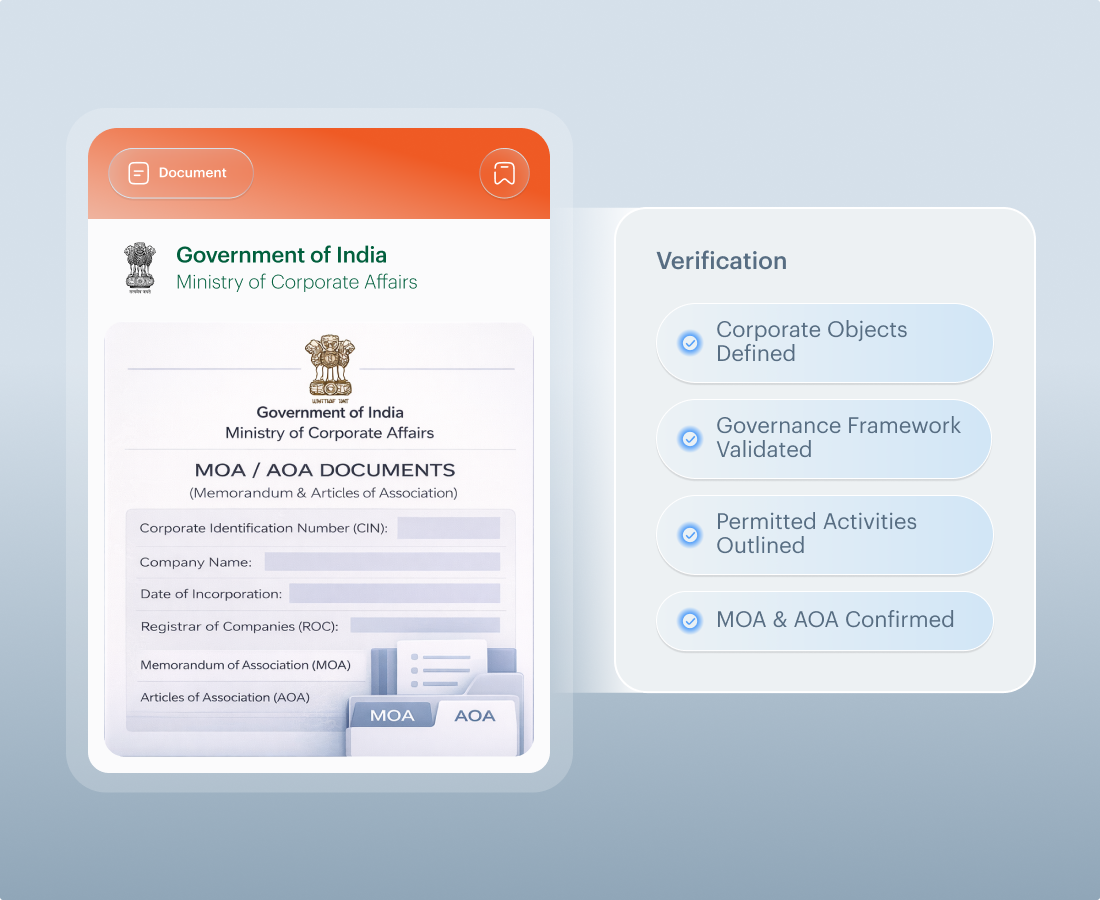

MoA / AoA

Establishes governance framework and permitted activities.

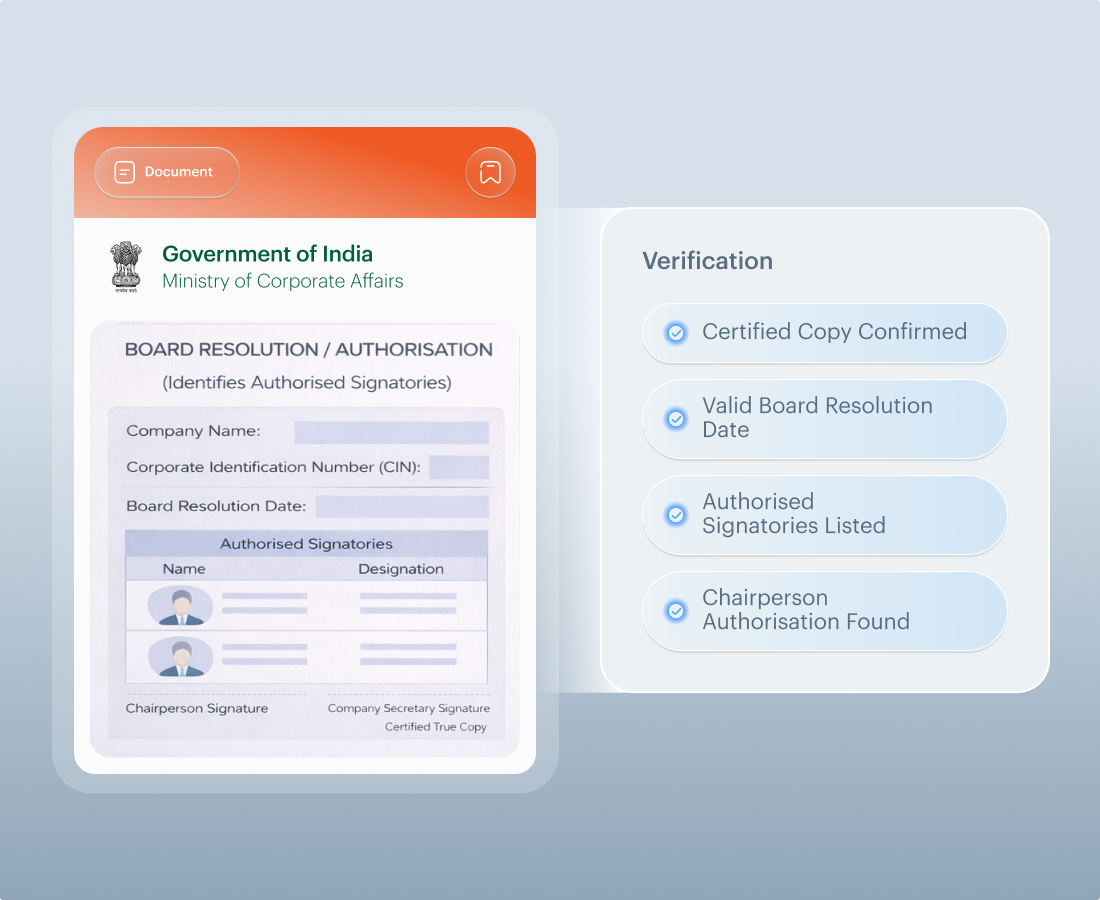

Board Resolution / Authorisation

Identifies authorised signatories.

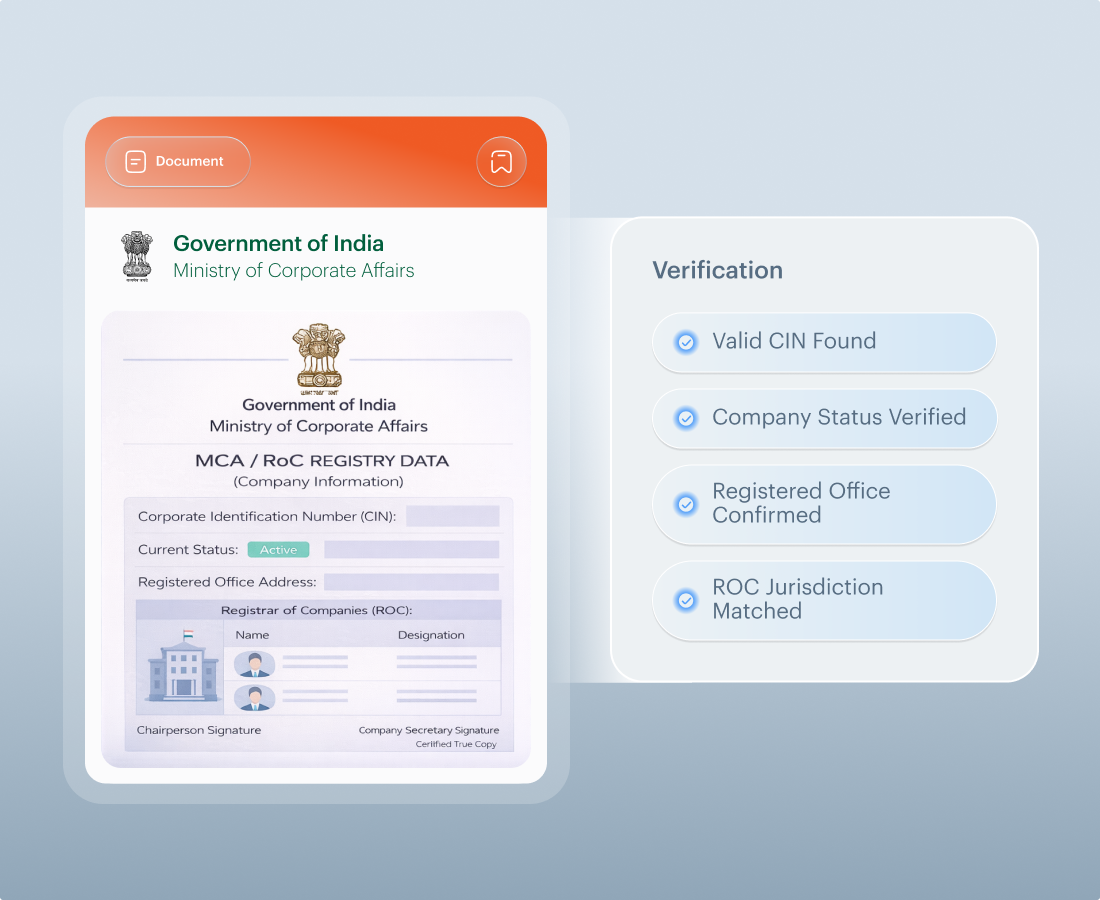

MCA / RoC Registry Data (CIN, status, registered office)

Confirms active status and official master data at onboarding.

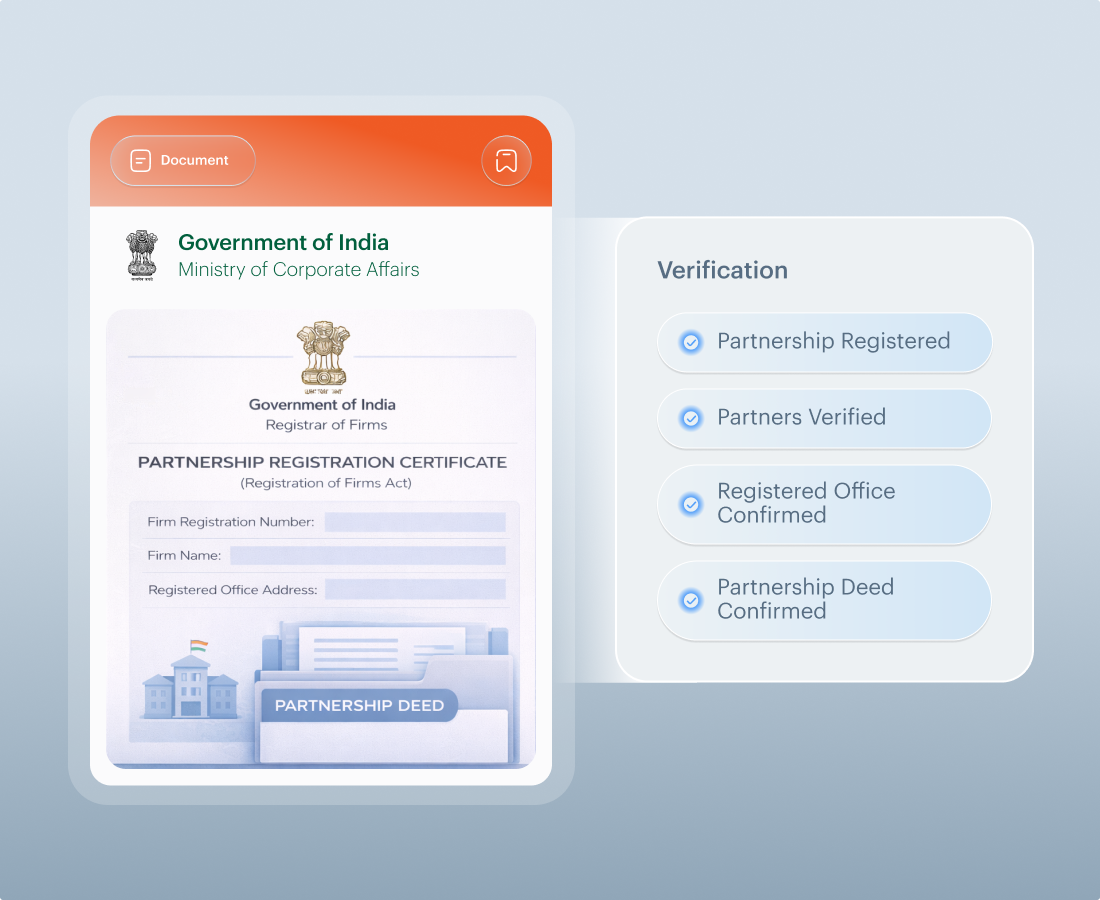

Partnership Registration Certificate

Required for partnership KYB.

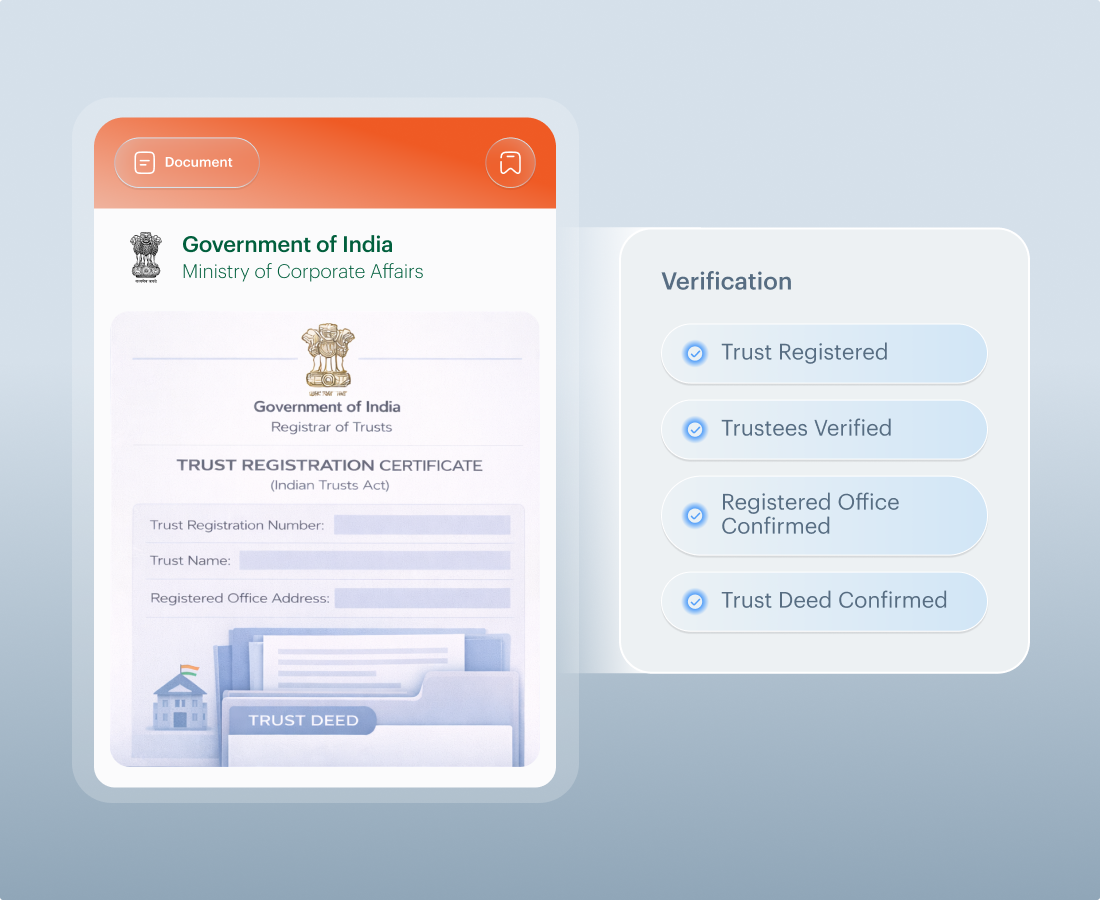

Trust Registration Certificate

Required for trust onboarding.

Business Tax Identity

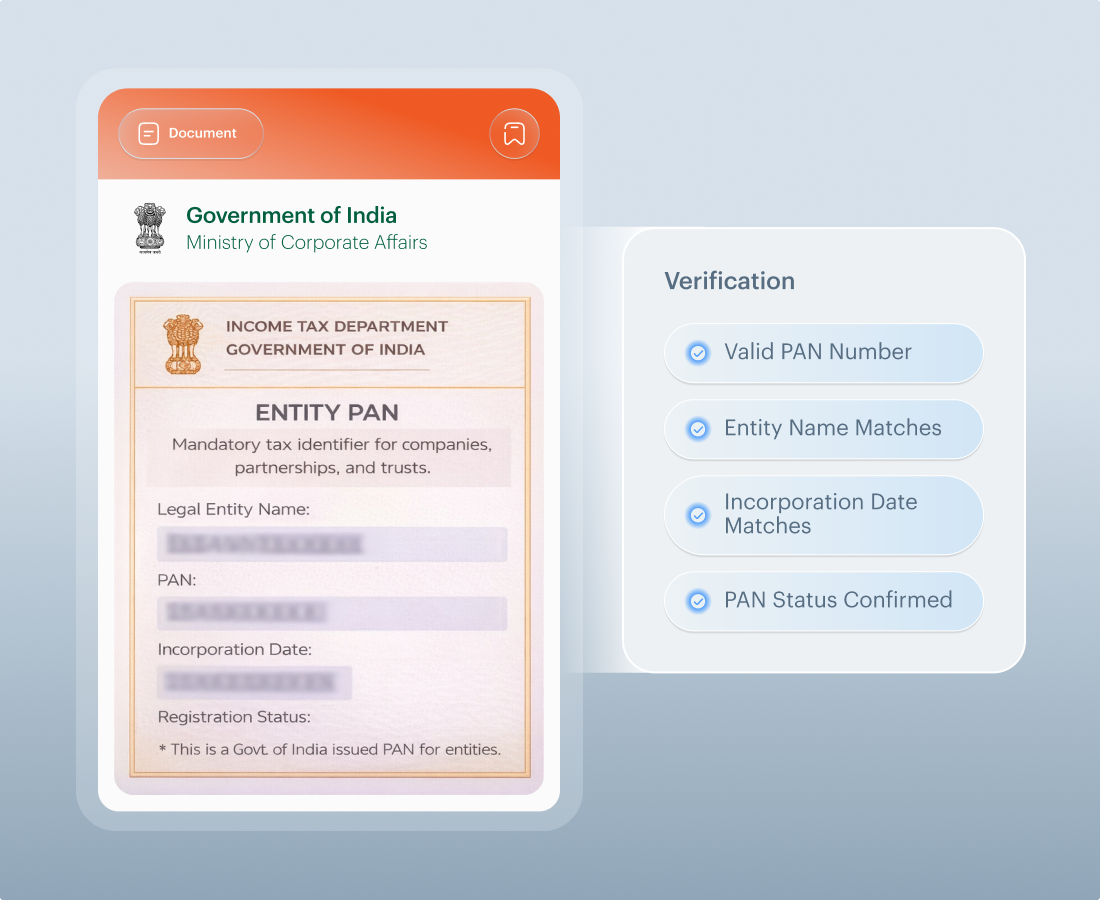

Entity PAN

Mandatory tax identifier for companies, partnerships, and trusts.

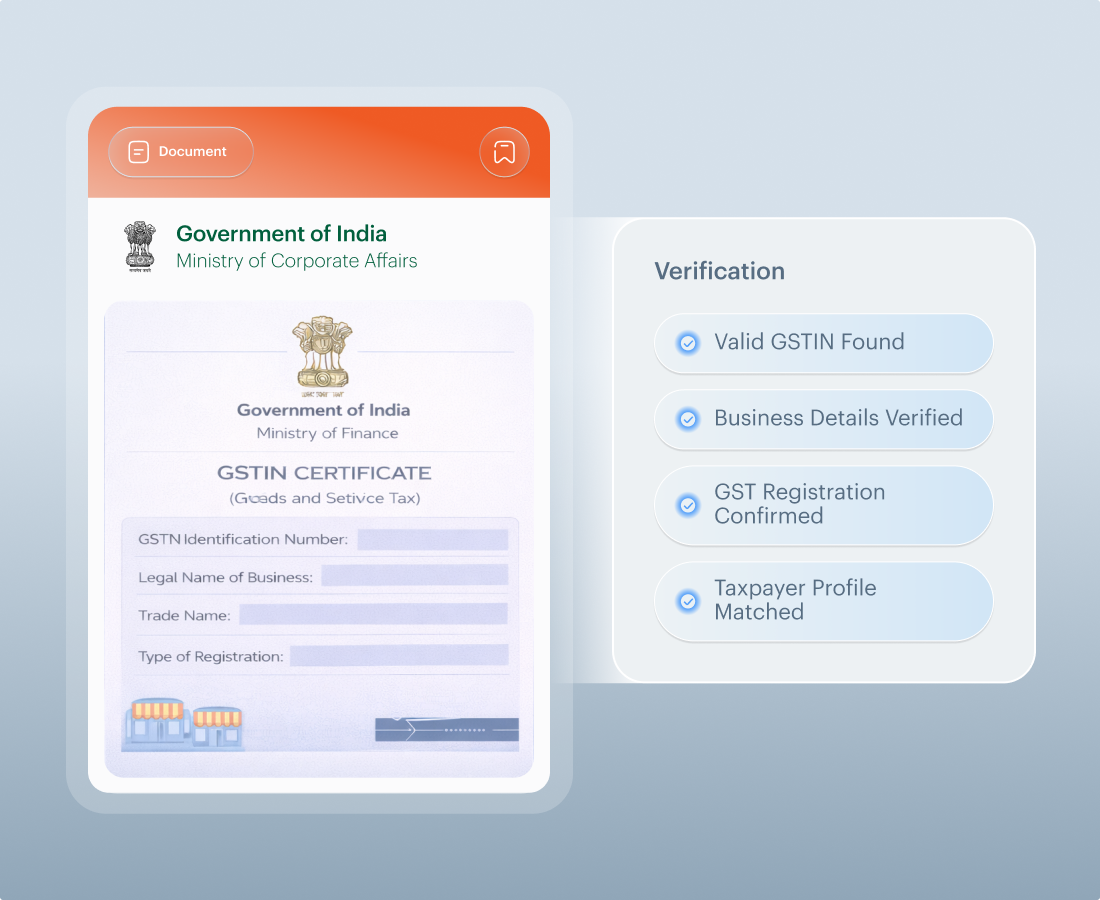

GSTIN (Goods and Services Tax Identification Number)

Validates indirect tax registration and trading profile.

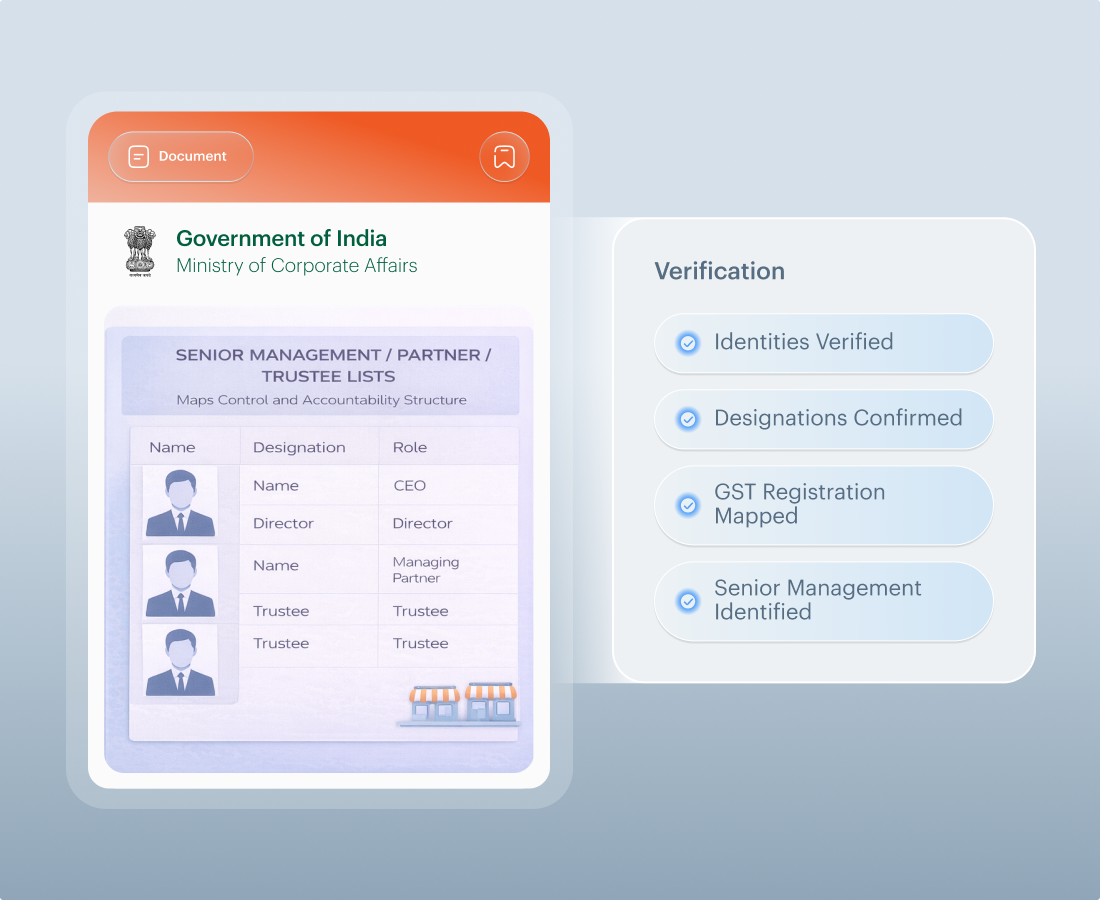

Ownership & Control (UBO)

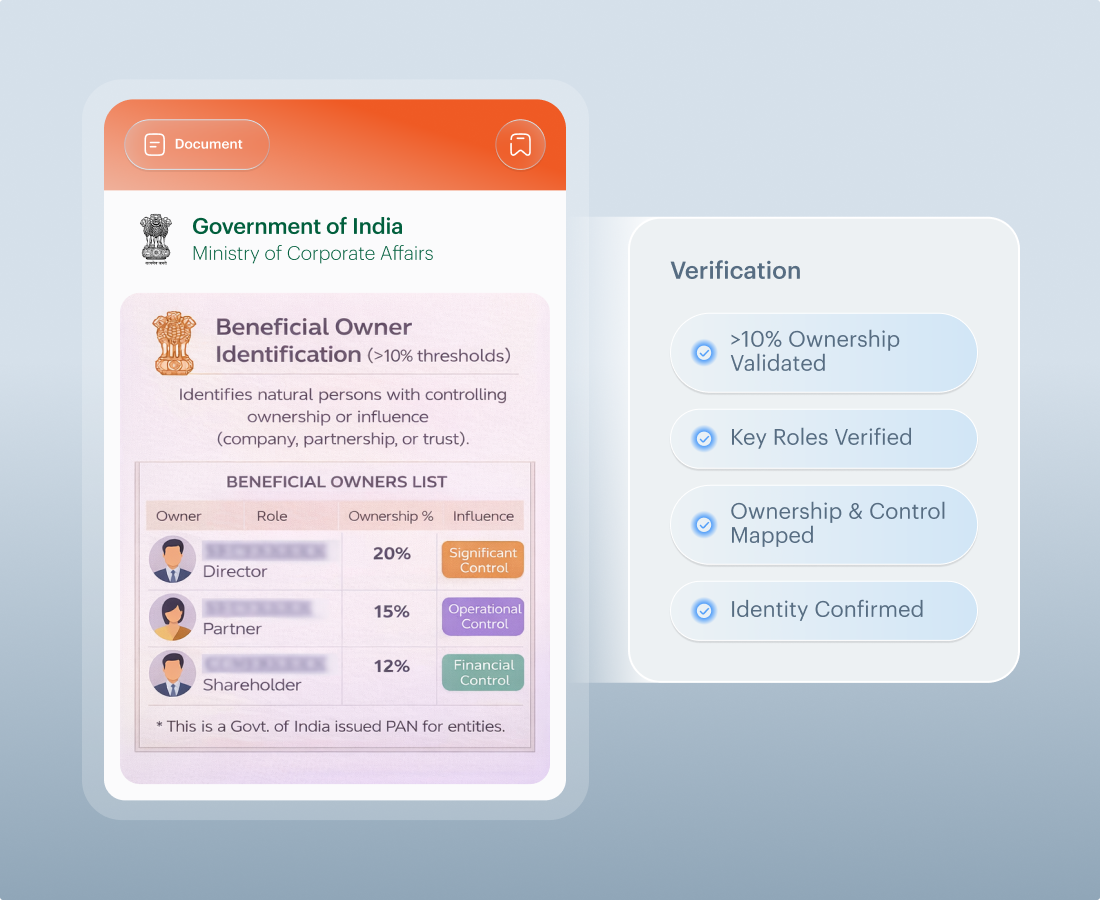

Beneficial Owner Identification (>10% thresholds)

Identifies natural persons with controlling ownership or influence (company, partnership, or trust).

Senior Management / Partner / Trustee Lists

Maps control and accountability structure.

Languages We Cover

Document text handling

Supports bilingual Aadhaar issuance (English + Hindi) and non-Latin-script and Latin-script passports. Captures both script layers and preserves structured data.

Name matching controls

Applies transliteration-aware matching for Hindi (Devanagari) and regional scripts, and MRZ-aware normalisation for passports (e.g., punctuation and diacritic removal).

Evidence consistency

Reconciles Aadhaar, PAN, and OVD records into a unified identity profile to reduce cross-document mismatch during CDD and reporting.

GOVERNANCE & CONTROLS

Audit-Ready Decisions, Lower Operational Drag

Fewer Avoidable Re-Submissions

Capture logic accounts for Aadhaar bilingual fields, PAN format rules, and state-level document variations, reducing rework.

Cleaner Audit Trails

Structured logs support RBI, FIU-IND, and SEBI inspection expectations by documenting decision reasons and retaining evidence.

Better Name Matching Outcomes

Transliteration-aware matching reconciles Devanagari and Latin-script variants and separates MRZ form from display form.

One workflow, one

back office

KYC, CKYC alignment, KYB, and AML screening are managed within a unified case view for India operations.

Aadhaar-First Flow Design

Journeys built around Aadhaar-led onboarding with PAN validation and OVD fallback when required.

India’s IDV/KYC Challenges

Digital KYC Evidence Burden

Digital KYC requires live photo capture, OVD proof and geo-tagged metadata, increasing failure points and operational review load.

Aadhaar Language Variance

English plus regional-script Aadhaar fields create transliteration drift across PAN, passport, and OVDs, driving manual reconciliation.

PAN / Form 60 Friction

PAN mismatches against name or DOB disrupt onboarding and trigger remediation loops before activation.

UBO Mapping at Low Thresholds

Beneficial ownership above 10% increases controller mapping effort and audit exposure for layered structures.

Shufti’s IDV Solution for the India

KYC Solutions

Face Verification

Matches live selfie capture against Aadhaar, passport, or driving licence imagery. This matters in India, where remote onboarding, SIM-based OTP flows, and fraud risks require strong identity binding.

.

Age Verification

Combines selfie-based age estimation with document verification when regulatory certainty is required. This matters in India for regulated sectors where age confirmation must be defensible under AML and sector rules.

.

Address Verification

Verifies any address-bearing document, including electricity bills (e.g., BSES, Tata Power, MSEB), water bills, and bank statements from SBI, HDFC Bank, ICICI Bank, or Axis Bank. This matters in India, where address proof is core to OVD-based CDD and digital KYC requirements.

.

Document Verification

Supports Aadhaar (offline proof), PAN, passport, driving licence, EPIC, and other OVDs. Handles bilingual scripts, QR validation, and MRZ extraction. This matters in India, where Aadhaar-led onboarding and multi-document reconciliation are standard.

.KYB Solutions

Business Verification

Validates CIN status, entity PAN, GSTIN, directors, and beneficial owners using MCA registry data and rule-based thresholds. This matters in India, where >10% BO identification and registry-backed evidence are mandatory in KYB.

.

Enhanced Due Diligence (EDD)

Triggers on layered ownership, high-risk sectors, incomplete filings, or tax inconsistencies. Generates structured evidence packs. This matters in India, where regulators expect documented risk-based controls and FIU-ready audit trails.

.AML Screening

Business AML Screening

Screens entities, directors, and beneficial owners against Indian and global sanctions, PEP and watchlists. This matters in India, where reporting entities must support FIU-IND obligations and sector regulator inspections.

.

Transaction Screening

Supports ongoing monitoring for unusual transaction velocity, high-value cash patterns, and cross-border flows. This matters in India, where STR/CTR reporting obligations apply under the AML framework.

.Built To Fit India’s Compliance Landscape

Reserve Bank of India (RBI)

Regulates banks and NBFCs' KYC/AML controls via the KYC Master Direction. Shufti supports OVD-based CIP, beneficial ownership capture, ongoing monitoring logic, and structured record retention aligned to RBI requirements.

Financial Intelligence Unit – India (FIU-IND)

National AML reporting authority operating FINnet 2.0 reporting infrastructure. Shufti structures onboarding data and suspicion rationale to support STR/CTR reporting and audit reconstruction.

Securities and Exchange Board of India (SEBI)

Regulates securities intermediaries and AML/CFT obligations in capital markets. Shufti enables intermediary-grade KYC, risk profiling, and monitoring workflows aligned to PMLA-linked obligations.

Insurance Regulatory and Development Authority of India (IRDAI)

Oversees AML/CFT controls for insurers. Shufti supports customer identification, recordkeeping, and video-based identification processes relevant to insurance onboarding.

Unique Identification Authority of India (UIDAI)

Governs Aadhaar issuance, authentication, and data protection under the Aadhaar Act. Shufti supports Aadhaar QR validation, consent-aligned capture, and secure handling of Aadhaar-originated data.

Ministry of Corporate Affairs (MCA) / Registrar of Companies (RoC)

Maintains corporate registry and official entity identifiers. Shufti verifies CIN status, registered office, and filing-backed entity data to support audit-ready KYB.

Central KYC Registry (CKYCR)

Operates India’s centralised KYC record repository under the AML framework. Shufti structures customer data to align with CKYC data fields and supports reuse logic where permitted.

Digital Personal Data Protection Act, 2023 (DPDP) & Data Protection Board of India

Establish statutory governance for the processing of personal data. Shufti enables defined retention controls, lawful processing workflows, and access logging aligned to India’s data protection regime.

Deployment Choice

India-based cloud regions (e.g., Mumbai, Hyderabad) or on-premise deployment support RBI data localisation expectations and stronger control over AML/KYC data.

Regulatory Alignment

Aligned to PMLA CDD, beneficial ownership and STR obligations, alongside DPDP Act principles of lawful processing and accountability.

Retention controls

PMLA rules require retention of identity and transaction records for at least five years after the end of the business relationship.

Encryption posture

Encryption, strict access controls and secure logging support DPDP Act safeguards and RBI cybersecurity expectations.

Data and Privacy Controls in India

India AML Sources That Strengthen Decision

")

Council of States (Rajya Sabha)

")

Ministry of Defence (India)

Parliament of India

")

Ministry of Home Affairs (India)

")

Ministry of Finance (India)

")

Ministry of Law and Justice (India)

")

Ministry of External Affairs (India)

")

Ministry of Information and Broadcasting (India)

")

Ministry of Parliamentary Affairs (India)

")

Ministry of Personnel, Public Grievances and Pensions (India)

")

Ministry of Power (India)

Council of States (Rajya Sabha)

Ministry of Defence (India)

Parliament of India

Ministry of Home Affairs (India)

Ministry of Finance (India)

Ministry of Law and Justice (India)

Ministry of External Affairs (India)

Ministry of Information and Broadcasting (India)

Ministry of Parliamentary Affairs (India)

Ministry of Personnel, Public Grievances and Pensions (India)

Ministry of Power (India)

Council of States (Rajya Sabha)

Ministry of Defence (India)

Parliament of India

Ministry of Home Affairs (India)

Ministry of Finance (India)

Ministry of Law and Justice (India)

Ministry of External Affairs (India)

Ministry of Information and Broadcasting (India)

Ministry of Parliamentary Affairs (India)

Ministry of Personnel, Public Grievances and Pensions (India)

Ministry of Power (India)

Frequently Asked Questions

What is the primary ID used for KYC in India?

Aadhaar (proof of possession of Aadhaar) is widely used under RBI KYC rules. Passport, driving licence, EPIC, and other OVDs act as alternatives where required.

Is PAN mandatory for onboarding?

PAN is required for individuals and entities under CDD rules, or Form 60, where PAN is not available. Name-PAN consistency must be verified.

How does CKYC fit into onboarding?

CKYC enables centralised KYC record storage. Shufti structures customer data to align with CKYC fields where reuse is permitted.

What reporting infrastructure applies in India?

Reporting entities file STRs and CTRs to FIU-IND through FINnet 2.0. Onboarding records must support reconstruction and audit.

How are bilingual Aadhaar names handled?

Shufti captures both English and regional-script fields and applies transliteration-aware matching to reduce false mismatches.

What documents are typically required for KYB in India?

Certificate of Incorporation, CIN status check, entity PAN, GSTIN, authorised signatory proof, and beneficial owner details (>10% thresholds).

How is personal data governed in India?

Processing must align with the Digital Personal Data Protection Act, 2023. Shufti supports defined retention and access controls.

What happens if a customer fails digital KYC capture?

Structured retries are supported, with geo-tagged and timestamped evidence preserved for compliance review.

Build a India-ready KYC, KYB & AML programme with Shufti

INDEPENDENTLY AUDITED. GLOBALLY CERTIFIED.

Certified to Global Standards

PROVEN WORKFLOWS

Use Cases for Regulated Growth in India

Accelerate Growth, Eliminate Friction

Onboard users in seconds, not days. Deploy tiered address verification flows that maximise completion rates for genuine users while filtering out synthetic fraud.

Onboard Global Traders in Real-Time

Verify investors across 250+ countries & territories. Ensure compliance with international financial regulations while preventing identity theft and high-risk chargebacks.

Secure Trust at Every Transaction

Automate KYC and AML workflows to reduce manual onboarding costs. Strengthen residency checks while delivering the frictionless digital experience modern customers expect.

Power a Fair & Secure Player Experience

Reduce bonus abuse and multi-accounting rings at the door. Enforce location rules and trigger step-up checks without disrupting the player journey.

Build a Trusted, Verified Workforce

Screen freelancers and drivers at scale. Verify residency and reduce onboarding friction while maintaining trust between users.

Scale Your Exchange with Confidence

Balance anonymity with compliance. Instantly verify user jurisdiction to meet Travel Rule obligations and help stop abuse without slowing down legitimate trading volume.

Reduce fraud without blocking growth

Shufti supports marketplace integrity by verifying seller and buyer identities, enabling age-gated journeys where needed, and preserving evidence to support investigations, disputes and risk-led enforcement actions.

Accelerate Growth, Eliminate Friction

Onboard users in seconds, not days. Deploy tiered address verification flows that maximise completion rates for genuine users while filtering out synthetic fraud.

Onboard Global Traders in Real-Time

Verify investors across 250+ countries & territories. Ensure compliance with international financial regulations while preventing identity theft and high-risk chargebacks.

Secure Trust at Every Transaction

Automate KYC and AML workflows to reduce manual onboarding costs. Strengthen residency checks while delivering the frictionless digital experience modern customers expect.

Power a Fair & Secure Player Experience

Reduce bonus abuse and multi-accounting rings at the door. Enforce location rules and trigger step-up checks without disrupting the player journey.

Build a Trusted, Verified Workforce

Screen freelancers and drivers at scale. Verify residency and reduce onboarding friction while maintaining trust between users.

Scale Your Exchange with Confidence

Balance anonymity with compliance. Instantly verify user jurisdiction to meet Travel Rule obligations and help stop abuse without slowing down legitimate trading volume.

Reduce fraud without blocking growth

Shufti supports marketplace integrity by verifying seller and buyer identities, enabling age-gated journeys where needed, and preserving evidence to support investigations, disputes and risk-led enforcement actions.

Accelerate Growth, Eliminate Friction

Onboard users in seconds, not days. Deploy tiered address verification flows that maximise completion rates for genuine users while filtering out synthetic fraud.

Onboard Global Traders in Real-Time

Verify investors across 250+ countries & territories. Ensure compliance with international financial regulations while preventing identity theft and high-risk chargebacks.

Secure Trust at Every Transaction

Automate KYC and AML workflows to reduce manual onboarding costs. Strengthen residency checks while delivering the frictionless digital experience modern customers expect.

Power a Fair & Secure Player Experience

Reduce bonus abuse and multi-accounting rings at the door. Enforce location rules and trigger step-up checks without disrupting the player journey.

Build a Trusted, Verified Workforce

Screen freelancers and drivers at scale. Verify residency and reduce onboarding friction while maintaining trust between users.

Scale Your Exchange with Confidence

Balance anonymity with compliance. Instantly verify user jurisdiction to meet Travel Rule obligations and help stop abuse without slowing down legitimate trading volume.

Reduce fraud without blocking growth

Shufti supports marketplace integrity by verifying seller and buyer identities, enabling age-gated journeys where needed, and preserving evidence to support investigations, disputes and risk-led enforcement actions.

Let’s Tailor your journey

Just a few quick questions to guide your Shufti experience.

Shufti

Market Positioning and Commercial Assessment

Industry stands at 1.7rating

Best ID Verification Innovator

TOP 10 KYC Solution Provider

Best Client Onboarding Solution

Samer Al Tamimi@CEO of Safwa Bank

We take our client's privacy very seriously and always look for new innovative solutions to ensure a safe banking experience. Working with Shufti feels like a breath of fresh air, as their 100% in-house tech keeps our customer's data free from vulnerabilities and fully safe and protected.

PROVEN PLAYBOOKS

Explore Practical KYC & AML Resources

16 August, 2025

5 minutes read

How Much of What You’ve Verified Is Actually Real?

Shufti’s Deepfake Blindspot Audit now runs fully inside your AWS environment, auditing historic KYC for manipulation signals without moving sensitive data off-prem.

whitepapers

Thanks For Your Submission.