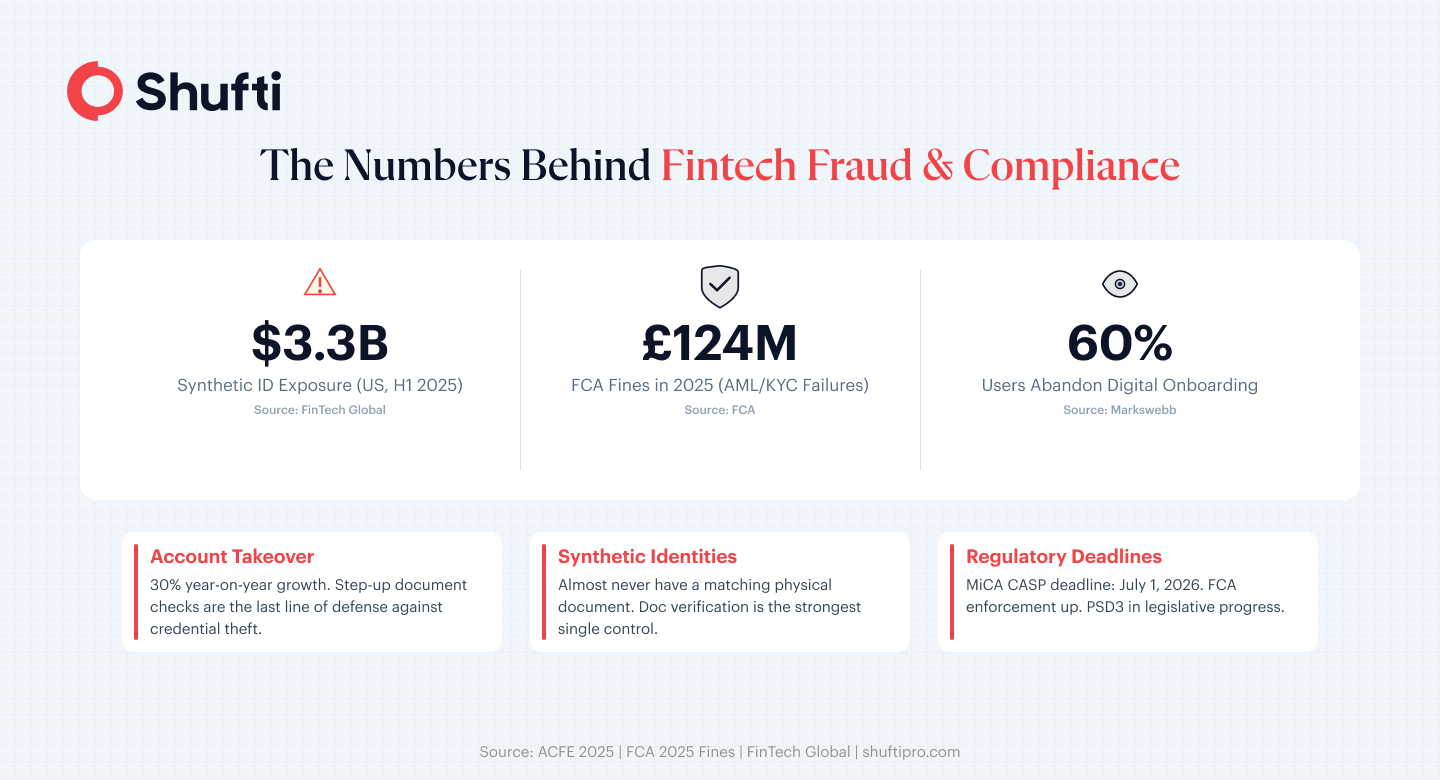

- FCA (UK). The Financial Conduct Authority’s 2025 fines register closed the year at £124,221,367.45 in penalties, with the bulk tied to AML and customer-due-diligence failures.

- Synthetic identity fraud exposed US lenders to 3.3 billion USD in losses in H1 2025 alone.

- FCA, PSD2, MiCA, and FATF all mandate identity document checks before customer onboarding.

- Markswebb’s digital-onboarding research found that up to 60% of users abandon the digital bank-account opening process before completion, and 40–50% of that abandonment happens at the KYC step, usually at document upload.

- Purpose-built document verification platforms now complete full forensic checks in under 60 seconds.

In October 2024, the UK’s Financial Conduct Authority fined Starling Bank £28.96 million for financial crime, failing gaps in its financial sanctions screening and customer identification controls. The fine landed because a digitally native neobank’s verification controls could not keep pace with its growth rate. That gap between onboarding speed and verification quality is the defining compliance risk for fintechs in 2026.

Document verification for fintech is not a back-office formality. It is the control layer between your onboarding funnel and your operating licence. Get it right and you’re onboard faster with fewer fraud losses. Get it wrong and the regulator sets the terms.

What does the fraud landscape look like for fintechs in 2026?

Fintechs are the primary target for identity fraud. Digital-only onboarding, API-first architecture, and fast account activation create an environment fraudsters actively exploit.

Account Takeover and Money Mule Schemes

Account takeover (ATO) attacks increased over 36% in 2024 compared to 2023 filed with FinCEN. The mechanism is consistent: fraudsters obtain credentials through phishing or data breaches, layer in a stolen or manipulated document to pass identity checks, and take over the account before the legitimate customer notices. Money mule accounts follow the same pattern opened with misrepresented documents, used to cycle proceeds before monitoring flags them.

Synthetic Identity Fraud at Onboarding

Synthetic identity fraud is harder to detect. A fraudster assembles a plausible identity from real and fabricated data, a genuine government ID number with an invented name and address and presents it at onboarding. BIIA’s 2026 analysis puts US lender exposure at $3.3 billion in H1 2025. The entry point is almost always the document check: a forged ID that passes a basic photo-match but fails a forensic structural review. Fintechs relying on surface-level checks absorb these losses months later, when the fraudulent account has already served its purpose.

Which Regulations Require Document Verification for Fintech Companies?

Every major regulatory framework covering fintech operations mandates document verification as part of customer due diligence(CDD). The baseline is the same across jurisdictions: verify a government-issued identity document before onboarding.

|

Regulation |

What it mandates |

Who it covers |

Key 2026 milestone |

|

FCA / UK MLRs |

ID verification before onboarding; ongoing monitoring |

UK payment institutions, e-money firms, neobanks |

Ongoing; Starling fine reinforced expectations |

|

PSD2 (EU) |

Strong Customer Authentication + CDD for payment initiation |

EU payment service providers |

PSD3 harmonisation in progress |

|

MiCA |

Full KYC including government photo ID for all CASP users |

EU crypto-asset service providers |

CASP authorisation deadline: 1 July 2026 |

|

FATF Rec 10 & 16 |

Document-based CDD; originator and beneficiary data on transfers |

All regulated financial institutions globally |

Rec 16 updated at June 2025 Plenary |

MiCA’s July 2026 deadline is the most immediate pressure point. VASPs without CASP authorisation by that date must cease crypto-asset services in EU member states with no grace period, no provisional licence per InnReg’s 2026 MiCA Guide.

How does Document Verification affect your Onboarding funnel?

Document verification affects your funnel in two directions at once. Done well, it reduces fraud losses and regulatory exposure without adding friction. Done poorly, it generates abandonment at the highest-intent moment in your user journey.

Achieving Sub-60-second Onboarding with Full Document Checks

The benchmark has shifted. A modern document verification service completes a full forensic check MRZ parsing, security feature detection, NFC chip read where present, and face match in under 60 seconds. The bottleneck in most fintech stacks is not the check itself; it is the handoff between systems. Fintechs that run document capture, forensic verification, and AML screening through separate vendors introduce latency at every API boundary. A single-pipeline document verification solution eliminates those handoffs and delivers the full check within the sub-60-second window without compromising forensic depth.

Fitting Document Verification into your KYC/AML Stack

Document verification does not replace your KYC stack, it anchors it. The verified document establishes the identity claim that every downstream control builds on: the AML screening, the sanctions check, the ongoing transaction monitoring. When document verification and AML run through the same decisioning layer, the identity record stays consistent across the customer lifecycle. When they run through separate vendors, the audit pack has gaps and regulatory enforcement actions against fintechs consistently cite disconnected systems, not absent checks, as the proximate cause.

Document Verification Use Cases by Fintech Vertical

The document requirement is consistent across fintech. Risk profile and document types vary by vertical.

|

Vertical |

Primary document requirement |

Key fraud risk |

|

Neobanks |

National ID, passport, residence permit |

Synthetic identity at account opening |

|

Crypto / VASPs |

Government photo ID; proof of address above thresholds |

MiCA CDD gaps; Travel Rule originator data |

|

BNPL |

ID and address verification at point of credit |

Bust-out fraud; age misrepresentation |

|

Payments |

ID for higher-value or recurring transfers |

Money mule; account-to-account fraud |

|

Lending |

Full KYC including source-of-funds documentation |

Synthetic credit file; identity layering |

What Does Non-Compliance Actually Cost a Fintech?

OKX paid $504 million in 2025 after pleading guilty to operating an unlicensed money transmission business with inadequate AML controls. Remediation programmes mandated by regulators independent monitors, mandatory process overhauls routinely run three to five years and cost tens of millions beyond the initial fine. Licence suspension ends operations in the affected jurisdiction entirely, and the reputational damage carries into every subsequent licence application and banking partnership.

How to Choose a Document Verification Platform for Fintech Companies

Not every document verification solution is built for the fintech context. Five criteria separate a fit platform from one that creates problems at scale.

Document Coverage

Your users are global; a platform trained on a narrow document set fails on non-standard IDs and drives abandonment. The operational baseline is 10,000+ document types across 230+ countries.

Forensic Depth

Photo-match is not document verification. MRZ parsing, security feature detection, and NFC chip reads are the layers that catch what surface-level tools miss.

Speed without Compromise

Fast but inaccurate creates compliance gaps; accurate but slow kills conversion. The benchmark is a full forensic check in under 60 seconds.

Regulatory Coverage

Your platform must evidence compliance against FCA, PSD2, MiCA, and FATF. Request the vendor’s compliance documentation before integration, not after.

Stack Integration

The right document verification platform integrates in days, connects natively to your AML layer, and produces a single audit pack per session, not separate records across multiple vendor dashboards.

How Shufti Handles Document Verification for Fintech Companies

The failure mode regulators keep pricing into fines is the same one: document verification through one vendor, AML through another, no single owner of the complete identity record.

Shufti’s document verification runs in the same pipeline as AML screening and face verification: one API, one decisioning layer, one audit pack. The forensic layer checks MRZ data, security features, and NFC chip integrity across 10,000+ document types in 230+ countries, with proprietary OCR trained natively on 150+ languages. For fintechs operating under MiCA, FCA, or PSD2 obligations, that single-pipeline architecture is the structural difference between a defensible audit trail and an exposed gap.

|

See how Shufti’s document verification fits your stack, request a demo and run it on your actual document mix. |

Frequently Asked Questions

Q1: Is Document Verification Mandatory for Fintechs?

Yes. In the UK, EU, and under FATF guidance globally, document verification is a required element of customer due diligence before onboarding. Failure exposes the firm to regulatory fines, licence suspension, and lasting reputational damage.

Q2: What Regulations Require Document Verification for Fintech?

The FCA's Money Laundering Regulations, PSD2, MiCA, and FATF Recommendations 10 and 16 all mandate document-based identity checks. MiCA's CASP authorisation deadline of 1 July 2026 makes this urgent for any fintech providing crypto-asset services in the EU.

Q3: How do Fintechs Balance Fast Onboarding with Document Verification?

By consolidating document capture, forensic verification, and AML screening in a single pipeline. Multi-vendor stacks add latency at every API boundary. A unified document verification platform completes a full forensic check in under 60 seconds without sacrificing regulatory depth.

Q4: What Documents do Fintechs Need to Verify for KYC?

The core requirement across FCA, PSD2, and MiCA is a government-issued photo ID — passport, national ID, or driver's licence. Higher-risk onboarding adds proof of address, biometric face match, and in some jurisdictions source-of-funds documentation.

Q5: How Does Document Verification Help Prevent Fintech Fraud?

Forensic checks catch manipulated or forged IDs that pass basic photo matching. MRZ parsing, security feature detection, and NFC chip reads confirm a document is genuine before an account is created closing the entry point for synthetic identity fraud, account takeover, and money mule schemes.

Q6: Can a Fintech Company use Document Verification without a full KYC Platform?

Yes. API-based document verification services integrate with existing stacks without a full platform replacement. Running verification in isolation from AML and biometric checks creates audit gaps, however. Native AML integration delivers the complete audit trail without a rebuild.

Q7: What is the Best Document Verification Solution for a Neobank?

One that combines forensic accuracy on global document types, sub-60-second completion, and native AML integration through a single API. Coverage is the critical differentiator: a platform trained on 10,000+ document types across 230+ countries avoids the rejection rates that drive abandonment.