What Is Card Cloning?

Key takeaways

- Card cloning copies the data on a card (usually the magnetic stripe) onto a blank card. Your physical card never leaves your pocket.

- Skimming captures magstripe data, shimming targets the EMV chip. Both can feed a magstripe clone used in fallback mode.

- The FBI puts skimming losses at over USD 1 billion a year, and the US Secret Service removed 411 skimming devices in a single 2025 nationwide operation.

- Cloned cards can be traced. Every transaction carries metadata (terminal ID, location, time, read type) that fraud systems and law enforcement use.

- Prevention runs on two levels: card issuers and merchants (EMV, tokenisation, monitoring, terminal inspection) and cardholders (chip and contactless, PIN cover, transaction alerts).

- Most card fraud chains start earlier, at account opening, so identity verification at onboarding is the highest-leverage control.

What Is a Clone Card, and How Is It Used?

A clone card is a counterfeit copy of a payment card built to behave like the original. Credit cards, debit cards, and even gift cards can be duplicated by writing a legitimate card’s details onto a blank card’s magnetic stripe. When the clone is used, funds are drawn from the original cardholder’s account.

The danger sits in that last point. A criminal needs only seconds of access to your card data, or a device that reads it, with no direct contact. By the time something looks wrong on a statement, the clone may already have been used across several transactions.

Clones are used in three main ways. In card present settings such as ATMs and in-store terminals, where a captured PIN unlocks cash withdrawals. In resale, where stolen track data is sold in bulk on dark web markets to other fraudsters. And, when only the numbers are captured, the details feed card-not-present fraud online. Criminals typically prefer hard to trace outcomes: cash, resellable gift cards, or high value goods.

How Card Cloning Works, Step by Step

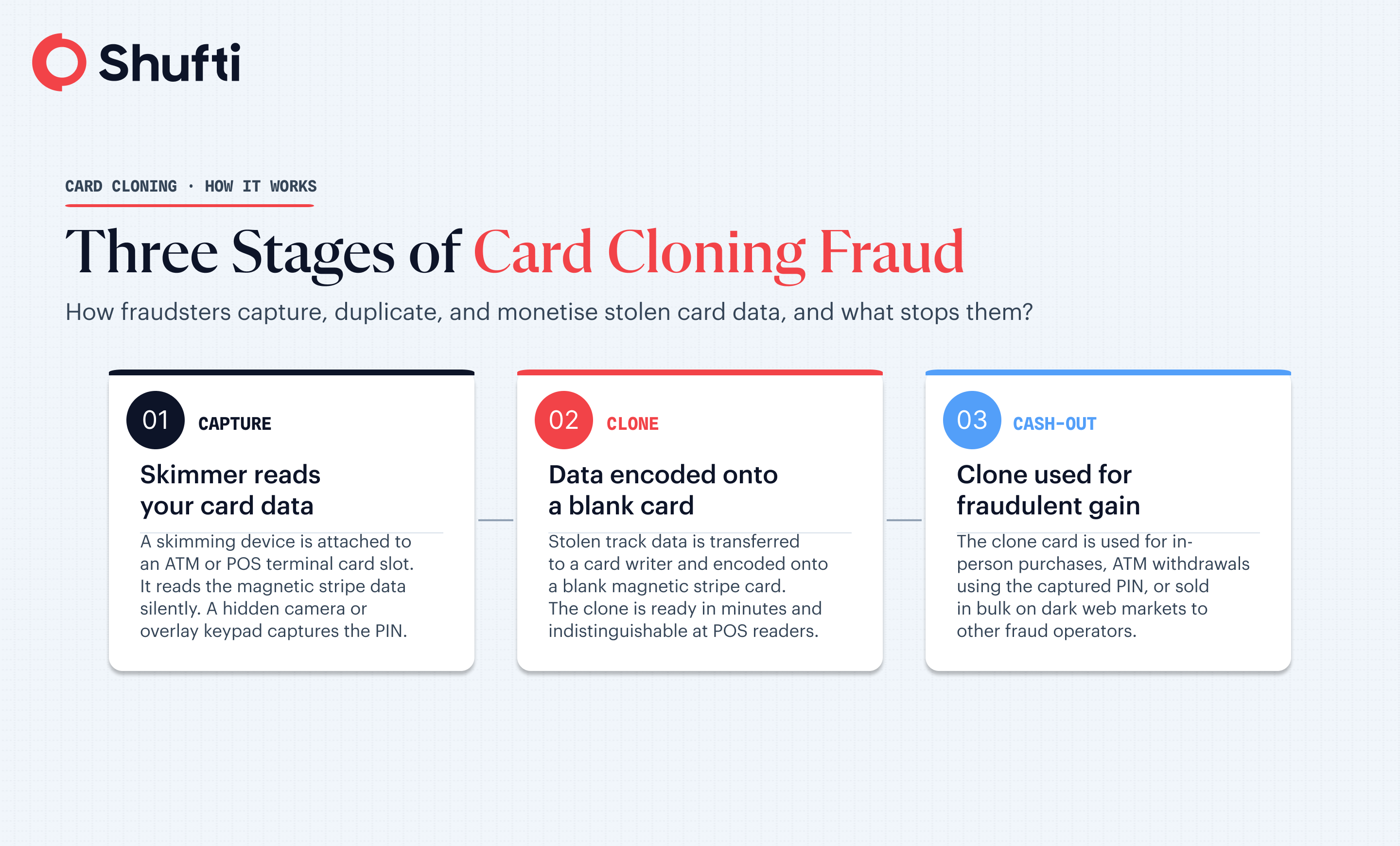

Card cloning follows a consistent three stage process: capture the card data, encode it onto a blank card, then convert that card into cash or goods.

1. Capture

The most common method is skimming: a small device fitted over or inside a legitimate card reader at an ATM, fuel pump, or payment terminal. As the card is inserted or swiped, the skimmer reads and stores the stripe data, while a hidden camera or fake keypad captures the PIN. Some operations use social engineering, where a dishonest employee swipes a card through a handheld skimmer.

2. Encode

The captured data is written to a blank magnetic stripe card using a widely available card writer. The resulting clone carries the same track data as the original, which makes it indistinguishable at terminals that read the magnetic stripe. This step takes minutes, and criminals working at scale can produce whole batches in one session.

3. Cash out

Clones are used for in-store purchases where magstripe is still accepted, for ATM withdrawals with the captured PIN, or resold in bulk. A single skimming device left on a busy ATM for 48 hours can yield hundreds of card records.

Common Card Cloning Methods

Criminals capture card data through several channels, physical and digital.

- ATM skimming: A skimming device is added to a real ATM, or a fake fascia is fitted, to capture card data during withdrawals. Devices can be hard to spot: look for loose or misaligned card slots and glue residue.

- POS terminal skimming: Overlays or internal implants on point-of-sale terminals capture card data at checkout. Coordinated campaigns have planted large numbers of skimmers across single regions.

- Fuel pump skimming: Devices are wired inside unattended fuel pumps, so nothing is visible from the outside. Pumps away from the attendant are a favourite target.

- EMV shimming: A thin shim inserted into the chip slot intercepts EMV data during a transaction. The chip itself cannot be cloned for chip on chip use, but captured data can seed a magstripe fallback clone.

- RFID / NFC theft: Scanners held near a contactless card attempt to read data. Contactless transactions use dynamic security, so routine cloning is far harder than it sounds, and most contactless fraud traces back to lost or stolen cards.

- Digital skimming (e-skimming): Malicious scripts injected into checkout pages harvest card details online. This now features in a large share of publicly disclosed data breaches.

- Insider capture and forums: Staff at merchants can copy details during transactions, and stolen data or cloning services are traded on criminal forums.

Skimming vs shimming

| Attribute | Card skimming | Card shimming |

| Target | Magnetic stripe | EMV chip contacts |

| Device | External overlay on the card slot | Thin shim inserted inside the slot |

| Card type exploited | Magnetic stripe cards | Chip and PIN cards |

| Detection difficulty | Moderate, sometimes visible | Very hard, hidden inside the slot |

| Fraud outcome | Fully functional magstripe clone | Partial chip data used for magstripe fallback |

Read: Synthetic identity fraud →

Card Cloning vs Related Card Fraud

Card cloning is often confused with adjacent fraud types. The distinctions matter for detection, because each leaves a different signature.

| Fraud type | What it is | Card present? |

| Card cloning | Duplicating a card’s data onto a counterfeit card | Yes, usually |

| Card skimming | The capture step that feeds cloning | Yes (at the reader) |

| Card-not-present fraud | Stolen details used online or by phone | No |

| Account takeover | Criminal seizes control of an existing account | No |

| Card testing | Small transactions to validate stolen numbers before large ones | Often no |

Card Cloning Statistics and Trends in 2026

A few figures frame the scale and direction of the threat. Confirm each against the primary source before publishing.

- The FBI estimates card skimming costs US financial institutions and consumers more than USD 1 billion a year.

- In a 2025 nationwide crackdown, the US Secret Service removed 411 illegal skimming devices and prevented an estimated USD 428.1 million in losses across roughly 9,000 businesses inspected.

- EMV chip technology now accounts for the large majority of card present transactions, which cut counterfeit card present fraud but pushed criminals toward fallback and online channels.

- Industry reporting attributes a large share of ATM related fraud to skimming, and links digital skimming to a significant portion of publicly disclosed data breaches.

- Payment card details remain widely traded on dark web markets, with millions of stolen records circulating and fuelling cloning operations.

Is Card Cloning Illegal?

| Region | How card cloning is penalised |

| United Kingdom | Fraud Act 2006: imprisonment up to 10 years, fines, or both. |

| United States | 18 U.S.C. 1029 (access device fraud): fines up to USD 250,000 and imprisonment up to 10, 15, or 20 years depending on the subsection and prior convictions. |

| European Union | Varies by member state, but treated as a serious offence, with imprisonment and substantial fines. |

| Singapore | Computer Misuse Act (Ch 50A): up to 10 years or fines up to SGD 50,000; Penal Code s420 covers cheating; Payment Services Act 2019 adds duties on institutions. |

| Australia | Criminal Code Act 1995 (Cth) s480.4: up to 7 years for dealing in identification information; s477.2: up to 2 years for unauthorised data modification; state laws apply too. |

| Canada | Criminal Code s342 (up to 7 years), s380 fraud (up to 14 years for large scale), s402.2 identity theft (up to 5 years). |

| Brazil | Penal Code: theft under Article 155 (1 to 4 years plus fines) and fraud under Article 171 (1 to 5 years plus fines). |

This is general information, not legal advice. Confirm obligations for your sector and jurisdiction with qualified counsel.

Can Cloned Cards Be Traced?

Card networks maintain velocity and geolocation models that can surface a cloned card within hours of first use, and banks share fraud intelligence so a flagged card can be blocked globally. Tracing is harder when money mules, prepaid cards, VPNs, and cross-border rings are involved, which is why speed of detection matters as much as the trail itself.

How Banks Detect Cloned Cards

Detection blends real-time monitoring with behavioural and device signals.

- Real-time transaction monitoring: AI models score transactions as they happen, flagging patterns that fit a cloned card rather than the genuine holder, at a volume no manual team could match.

- Behavioural profiling: Most customers behave predictably. A baseline of normal spend, location, and timing lets anomalies stand out for review.

- Device intelligence: One device attempting transactions across many cards is a hallmark of card testing and cloning, and device fingerprinting catches it.

- Link and network analysis: Accounts sharing an IP, device ID, or unique browser configuration are surfaced as a likely fraud network.

- Velocity and geolocation checks: Impossible travel, and mismatches between issuing country, claimed residence, and current IP, flag a card in use in two places at once.

- Physical inspection and EMV enforcement: Regular terminal checks for tampering, plus disabling magstripe fallback where possible, remove the most accessible cloning vector.

Where Card Fraud Really Starts

Card fraud rarely begins at the terminal. It usually starts earlier, when a fraudster opens a mule account, loads cloned card data into a new digital wallet, or registers a payment instrument under a fabricated identity. By the time a cloned card is declined at an ATM, the account level fraud has already happened upstream. This is why identity verification and behavioural analytics at onboarding are the highest leverage controls a business has: they close the gap between card issuance and compromise before a clone becomes an active instrument.

Explore fraud prevention →

How to Prevent Card Cloning

Prevention works at two levels: what issuers and merchants must do, and what cardholders can do.

For issuers and merchants

- Enforce EMV and disable magstripe fallback on terminals where possible, removing the most accessible cloning vector.

- Secure terminals physically, keep them tamper evident, and inspect them on a schedule.

- Run velocity checks, geolocation anomaly detection, and behavioural models that catch chip capable cards suddenly running fallback.

- Tokenise card data in processing, so a stolen token has no reuse value.

- Verify identity at onboarding to stop fabricated and mule accounts that turn stolen card data into active fraud.

For cardholders

- Inspect ATMs and terminals for loose parts, overlays, or hidden cameras before inserting a card.

- Cover your hand when entering a PIN, which defeats PIN capture even if a skimmer is present.

- Prefer chip and contactless over magstripe, and use virtual or single-use cards online where offered.

- Turn on real-time transaction alerts and review statements weekly.

- Avoid public Wi-Fi for financial transactions, and never enter card details on sites you do not trust.

The Future of Card Cloning and Fraud Prevention

As card security hardens, cloning gets harder, but attackers adapt. Several shifts will define the next few years:

- Biometric payment authentication (fingerprint, face, voice) replacing static PINs and passwords.

- Tokenization and dynamic CVV cards that render stolen data useless for reuse.

- AI and machine learning detection that scores transactions in real time and blocks anomalies before losses mount.

- AI assisted attacks too: automated card testing at scale and more convincing phishing, which raises the bar for defences.

- Geolocation based approval and richer device intelligence to bind transactions to a genuine cardholder.

How Shufti Helps Stop Card Fraud at the Source

Shufti focuses on the stage where most card fraud chains are built: account opening and onboarding. Document verification authenticates a government issued ID and detects tampering, biometric verification with liveness confirms a real person behind the account, and device and velocity signals flag the anomalous registrations that precede cloned card use.

Because the same platform covers identity verification, KYC, business verification, and AML screening, teams can close the gap between issuance and compromise without adding friction for genuine customers. Shufti verifies identities across 240+ countries and territories.

Request a demo →

Frequently Asked Questions

What is card cloning?

Card cloning is copying a card's payment data, usually from the magnetic stripe, onto a duplicate card that criminals use for fraudulent purchases or withdrawals. Fraudsters often also capture the PIN or CVV so the clone works in more situations.

Can a cloned card be used at an ATM?

Yes, if the criminal also captured the PIN. A magstripe clone plus the PIN allows cash withdrawals. This is why covering the keypad when entering a PIN is one of the most effective simple defences.

Can cloned cards be traced?

Yes. Financial institutions trace cloned cards through transaction monitoring, using metadata such as terminal ID, location, time, and read type. AI and machine learning flag suspicious patterns quickly, which speeds up tracing.

Can EMV chip cards be cloned?

The chip itself cannot be cloned for chip on chip use, because it generates a unique code per transaction. However, if a chip card also has a magnetic stripe, or is exposed to shimming, the captured data can be used to make a magstripe clone for fallback terminals.

What is the difference between card cloning and card skimming?

Skimming is the capture method, a device that reads card data at a reader. Cloning is the next step, writing that data onto a blank card. Skimming feeds cloning.

How can I tell if my card has been cloned?

Watch for unfamiliar transactions, charges in places you have not visited, small test transactions before larger ones, and impossible travel alerts. Many people only find out when their bank contacts them, so real-time alerts are the best early warning.

Which industries are most targeted by cloned card fraud?

Any sector with high transaction volumes and card use: retail, fuel, and ATMs. Businesses with weak fraud detection are at higher risk.

How do banks detect credit card cloning fraud?

Machine learning models analyse transaction patterns and flag anomalies in real time, supported by behavioural profiling, device intelligence, and velocity and geolocation checks.