Blog

Adverse Media Screening Requirements and Why Do FIs Need It?

The financial services industry is under a lot of regulatory requirements recently, and for all t...

Explore More

Explore More

Blog

New KYC Regime for the UK, US, and Australia – What’s in it for Financial Institutions?

Financial institutions are known for getting their reputation maligned due to crimes like identit...

Explore More

Explore More

Blog

Identity verification in freelancing- no more smoke and mirrors

Freelancing platforms are rapidly growing. In 2017, around 57 million Americans were freelancing ...

Explore More

Explore More

Blog

Age Gating VS Age Verification | Enhancing Security for Minors

Age gating was once employed to stop minors from accessing age-restricted content. However, the a...

Explore More

Explore More

Blog

Risks of Vaccine Verification Apps & What IDV Industry can Offer

COVID-19 has brought enough changes to make the world smarter. Businesses and customers migrating...

Explore More

Explore More

Blog

Combating Money Laundering Threats in the Art and Antiquities Sector Through AML Screening Solutions

With transforming technologies and growing digitization, the global art industry has also embrace...

Explore More

Explore More

Blog

UK’s Digital Identity Framework – Cornerstone of Reliable ID

In today’s technology-driven era, digital identity is becoming inevitable. Physical interactions ...

Explore More

Explore More

Blog

How to Protect Yourself From Cyber Crime in the Holiday Season?

Most people around the world do the majority of their shopping during the holiday season. Accordi...

Explore More

Explore More

Blog

High-Risk Transactions – How Can Enhanced Due Diligence (EDD) Help?

In today’s continuously evolving world, businesses should not only focus on the revenue they gene...

Help?") Explore More

Explore More

Blog

Know Your Player – Preventing Identity Fraud in Sports Events

The ongoing trend of globalizing sports activities since the last few decades has resulted in a l...

Explore More

Explore More

Blog

Shahid Hanif’s Take on Shufti’s Five-Year Journey of Winning the Fight Against Fraud

The financial sector constantly faces new and emerging challenges in fighting sophisticated fraud...

Explore More

Explore More

Blog

AML/CFT Compliance – Why Australia is a Safe Haven for Money Laundering

Recent inquiries and cases against major Australian casinos have raised questions about the measu...

Explore More

Explore More

Blog

A Detailed Insight into the Best Practices for Digital Currency Providers

The world has seen an overwhelming rate of development in the cryptocurrency sector with Centrali...

Explore More

Explore More

Blog

Shufti’s Insights on Enhancing Customer Onboarding Experience

The digital world nowadays requires a lot of effort from businesses to ensure customer satisfacti...

Explore More

Explore More

Blog

What is KYC and Why is it Important for Crypto Exchanges?

Cryptocurrencies are causing significant disruptions in the financial world. Cryptograp...

Explore More

Explore More

Blog

KJM Age Restrictions Breaking New Grounds for Gaming Industry

Minor protection has become a challenge for everyone these days. Parents are worried about the ty...

Explore More

Explore More

Blog

Safeguarding Ride-Hailing Services with Identity Verification Solutions

With the global digitization, mobility services are known to the world before the pandemic has ir...

Explore More

Explore More

Blog

Address Verification: Types, Benefits, and Best Practices

Improving customer service and combating fraud frequently requires swiftly gathering and confirmi...

Explore More

Explore More

Blog

Securing Investment Industry with Shufti’s Investor Verification Solution

In this tech-driven world, perpetrators and organized crime groups are adopting sophisticated met...

Explore More

Explore More

Blog

Brazil to Launch CBDC: Its Impact on Financial Firms and How KYC/AML Can Help

Where does the cash come from? The country’s central bank authorises the printing of paper ...

Explore More

Explore More

Blog

Debunking the Top 5 Misconceptions about KYC Compliance

Know Your Customer (KYC) compliance suffers from the issue of unintentional secrecy. Businesses h...

Explore More

Explore More

Blog, Identity & KYC, Online Marketplace

Utilising Digital Identity Verification for Imparting Better Healthcare

The importance of patient identification and verification is crucial in the healthcare sector. Ac...

Explore More

Explore More

Blog, Financial Crime / AML, Identity & KYC, Reg Tech

Significance of AML Compliance in Money Services Business

The financial sector landscape is evolving with the advent of the FinTech industry. Many revoluti...

Explore More

Explore More

Blog

Secure the Fintech Future with RegTech

Financial Technology (Fintech) refers to the use of technological advancements in the financial i...

Explore More

Explore More

Blog

Liveness Detection and IDV: An Overview of Biometric Facial Recognition

Identity fraud and cybercrime have significantly surged in the past few years. Deepfake technolog...

Explore More

Explore More

Blog

Anti-Smurfing Solutions | Safeguard Your Business Against Money Laundering Risks

Businesses are under constant threat of financial damage. This is primarily because cybercriminal...

Explore More

Explore More

Blog

Identity Verification with Liveness Detection: The Key to Preventing Spoofing Attacks

Spoofing attacks are not limited to just emails and fake websites. Hackers and cybercriminals hav...

Explore More

Explore More

Blog

Video KYC Onboarding: Fintechs meeting KYC compliance with video identifications

The Financial industry is introducing a digital revolution globally. The term Fintech corresponds...

Explore More

Explore More

Blog

AML Compliance – How to Steer Clear of Cryptocurrency Crimes

Bitcoin, Ethereum, Dogecoin, and Tether along with thousands of other cryptocurrencies are rising...

Explore More

Explore More

Blog

How ID Verification can Help you Boost your Revenue in 2019?

For years now banks have been using laid back and inconvenient methods for ID verification of cus...

Explore More

Explore More

Blog

Safeguarding Financial Operations with Transaction Monitoring and AML Screening

To enhance the power of anti-money laundering regulation, transaction monitoring systems have evo...

Explore More

Explore More

Blog, Online Marketplace

Verify ID For a Secure Travel Experience

Since we are using the Internet for a great many things including shopping to online booking of f...

Explore More

Explore More

Blog

Video KYC in 2024 | A Step Towards Digital Evolution

The striking surge in theft and fraud through digitisation is a growing concern for many business...

Explore More

Explore More

Blog

AML Compliance for the Crypto Sector – How VASPs Can Adhere to the Regulations

With cryptocurrencies gaining traction and entering the mainstream, financial regulators are asse...

Explore More

Explore More

Blog

Securing Identities with Photo ID Verification

ID verification has seen unprecedented growth not only in the processes but also in the crime com...

Explore More

Explore More

Blog

Initial Exchange Offerings (IEOs) – A Detailed Insight

The advent of the Crypto industry brought decentralized and innovative fundraising ways. One of t...

– A Detailed Insight") Explore More

Explore More

Blog

Non-Fungible Tokens (NFTs), Financial Crimes and AML/KYC Regulations – How Shufti Can Help

Non-Fungible Tokens (NFTs) emergence is providing a whole new segment to buy or sell digital crea...

, Financial Crimes and AML/KYC Regulations – How Shufti Can Help") Explore More

Explore More

Blog

Worldwide Language Coverage from Shufti helps you go Global

Language serves the purpose of communication among people of a certain locality, nation or in cas...

Explore More

Explore More

Blog

Facial Recognition Technology Pioneered at Olympic and Paralympic Games Tokyo 2020

Facial recognition has grown by leaps and bounds with the arrival of the sophisticated pattern-ma...

Explore More

Explore More

Blog

E-Signature | Digitise and Verify Agreements in Compliance

The use of electronic signature, or e-signature, has transformed business dealings. The days of s...

Explore More

Explore More

Blog

How Businesses Can Leverage Optical Character Recognition Technology in 2023

Optical Character Recognition (OCR) has revolutionised how businesses gather, process, and analys...

Explore More

Explore More

Blog

Identity verification solutions to fight against faces of fraud

In this digital world, billions of smart devices are circulating, connecting and communicating wi...

Explore More

Explore More

Blog

UAE’s Crypto Landscape – Eliminating Financial Crime to Ensure Regulatory Compliance

The UAE is the Middle East’s rapidly growing cryptocurrency hub that is experiencing a heated-up ...

Explore More

Explore More

Blog, Identity & KYC

Merchant Identity Proofing: Building Strong B2B Relations

Identity Proofing: The success of e-commerce has been very remarkable. It is expected that global...

Explore More

Explore More

Blog

Curbing Real Estate Crimes and Hunting Down Russian Investors with Shufti’s AML Screening Solution

The real estate industry has become attractive to money launderers in the same way it is to any l...

Explore More

Explore More

Blog

AML Compliance – How to Steer Clear of Cryptocurrency Crimes

Bitcoin, Ethereum, Dogecoin, and Tether along with thousands of other cryptocurrencies are rising...

Explore More

Blog

Strategic Evaluation and Elimination of Money Laundering in Real-Estate Sectors

The exchange of illicit money through real estate has been the most commonly encountered method o...

Explore More

Explore More

Blog

Navigating the New Era of Customer Identity: Strategies for Compliance Professionals

Introduction

The identity verification and authentication landscape is undergoing a rapid transfo...

Explore More

Explore More

Blog

New KYC Regime for the UK, US, and Australia – What’s in it for Financial Institutions?

Financial institutions are known for getting their reputation maligned due to crimes like identit...

Explore More

Blog

Top OCR Use Cases in 2025: Compliance, Automation & Customer Experience

Optical Character Recognition (OCR) has shifted from a back‑office convenience to a board‑level c...

Explore More

Explore More

Blog

Secure Your Digital Presence | Combat Transaction Fraud and Cyberthreats with IDV

Financial crimes, especially payment and transaction fraud, have seen a massive surge in recent y...

Explore More

Explore More

Blog

Restricting Criminals from Exploiting Investment Industry with Shufti AML Screening Solution

Investing the accumulated capital of investors in financial securities is the primary task of inv...

Explore More

Explore More

Blog

AML Compliance for Luxury Goods Market – How Shufti can Help

Money laundering using high-value goods such as jewelry, yachts, motor vehicles, watches, fine ar...

Explore More

Explore More

Blog

Keeping AI Bias Out of the IDV Game with Shufti

Consider this: 85% of financial institutions today use some form of AI in their products. The tec...

Explore More

Explore More

Blog

Understanding AML Sanction Lists: Key Global Regimes and their Importance

Sanction lists are expanding regularly and sanctions imposed by different authorities do not alwa...

Explore More

Explore More

Blog

Gold Industry and Prevailing Financial Crimes – How Shufti’s AML Screening Can Help

Using gold for financial crimes has a long history and in many countries, jewellery is not only c...

Explore More

Explore More

Blog

KYC/AML Compliance for Startups in the Financial Sector – How Shufti Can Help

As technology continues to transform the financial industry, the need for identity verification h...

Explore More

Explore More

Blog

Jobs in the frame for money laundering

How banks can detect money mules?

Remote jobs are trending but not every job is legitimate. Some ...

Explore More

Explore More

Blog

Japan’s AML/CFT Assessment – August 2021 Report

Financial crime is soaring sky high with digitisation becoming a part of our daily lives. Cyber a...

Explore More

Explore More

Blog

What Counts as Proof of Income? A Guide for Businesses That Need to Verify Financial Status

Verifying a person’s income isn’t just about numbers, it’s about trust. Whether you’re approving ...

Explore More

Explore More

Blog

Common Types of BNPL Fraud and the Role of KYC/AML Regulations

The Buy Now Pay Later (BNPL) services are growing rapidly. 42% of credit customers are interested...

Explore More

Explore More

Blog

Fraud Detection, Compliance, and ID Verification Solution to Secure the Telecom Industry

The telecommunication industry has played a crucial role in global digitization, innovation, and ...

Explore More

Explore More

Blog

Gaming Industry Crimes and KYC/AML Solutions – What Shufti Can Offer

From the world’s glitziest gaming development to betting shops on the high streets, the global ga...

Explore More

Explore More

Blog

KYC Compliance for DeFi Platforms – Finding the Balance for a Secure Future

The rise of decentralized services in the form of digital asset trading platforms and DeFi consta...

Explore More

Explore More

Blog

5 Key Questions about Facial Recognition Answered by Experts

Technology has definitely made life convenient but comes with a gazillion concerns from anyone wh...

Explore More

Explore More

Blog

Online Document Verification – The Role of Shufti’s Optical Character Recognition (OCR) in Eliminating Fraud

Document verification is the most important stage when it comes to doing online business, getting...

in Eliminating Fraud") Explore More

Explore More

Blog, Financial Crime / AML, Fraud Prevention, Identity & KYC

Facial Recognition: Worries About the Use of Synthetic Media

In 2019, 4.4 billion internet users were connected to the internet worldwide, a rise of 9% from l...

Explore More

Explore More

Blog

Mobile Payments – Way of the Future or a Fad of the Digital Age?

Are we moving towards a world where retailers may one day say “We don’t take cash”? As mobile pay...

Explore More

Explore More

Blog

Know Your Patient – Balancing Security, Customer Experience and Compliance in the Healthcare Sector

As the healthcare industry continues to offer life-critical services while making efforts to impr...

Explore More

Explore More

Blog

Evolution of Digital Payments and Prevailing Crimes – How Shufti’s AML Screening Can Help

With emerging technologies, the digital payments trend is rising, and users are executing frictio...

Explore More

Explore More

Blog

Video KYC – Answer to Digital Revolution in the Gulf Region & UAE

The digital revolution in the Gulf region and UAE has been a hot topic these days. The economic d...

Explore More

Explore More

Blog

Evolving Regulations Shaping Digital Crypto Ecosystem – How Shufti Can Help

Since the start of civilization, humans have used money in several different ways, and throughout...

Explore More

Explore More

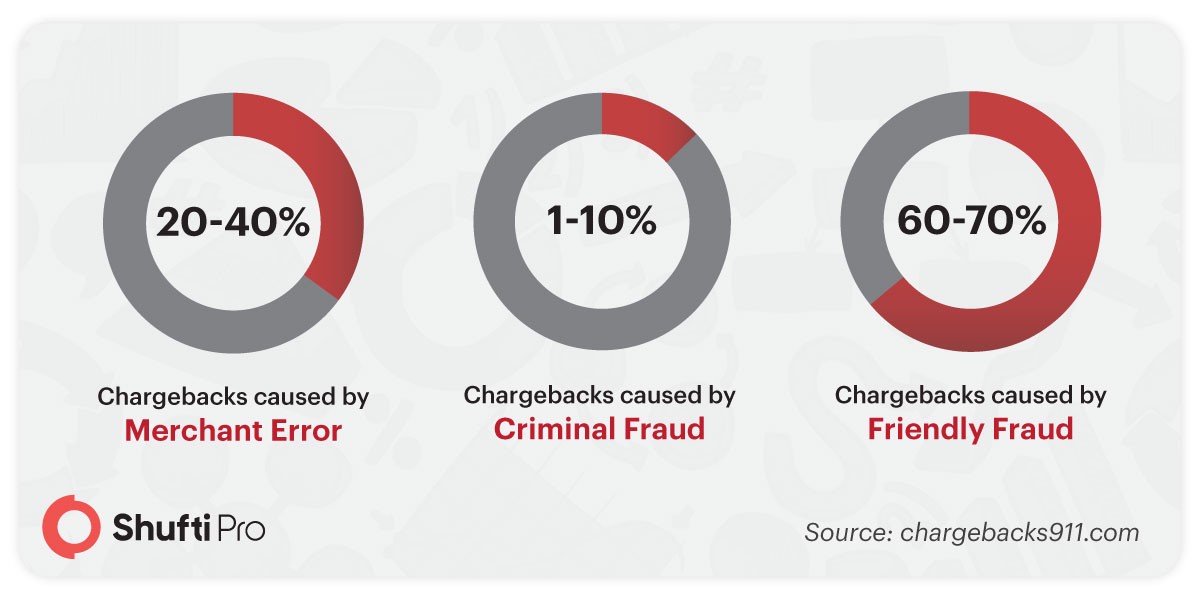

3: Friendly Fraud

3: Friendly Fraud