AMLR Solutions

AMLR Solutions AMLR Consultation

AMLR Consultation Onboarding

Onboarding Ongoing Monitoring

Ongoing Monitoring FRAML

FRAML KYC

KYC KYB

KYB KYI

KYI Age Assurance

Age Assurance Workforce IAM

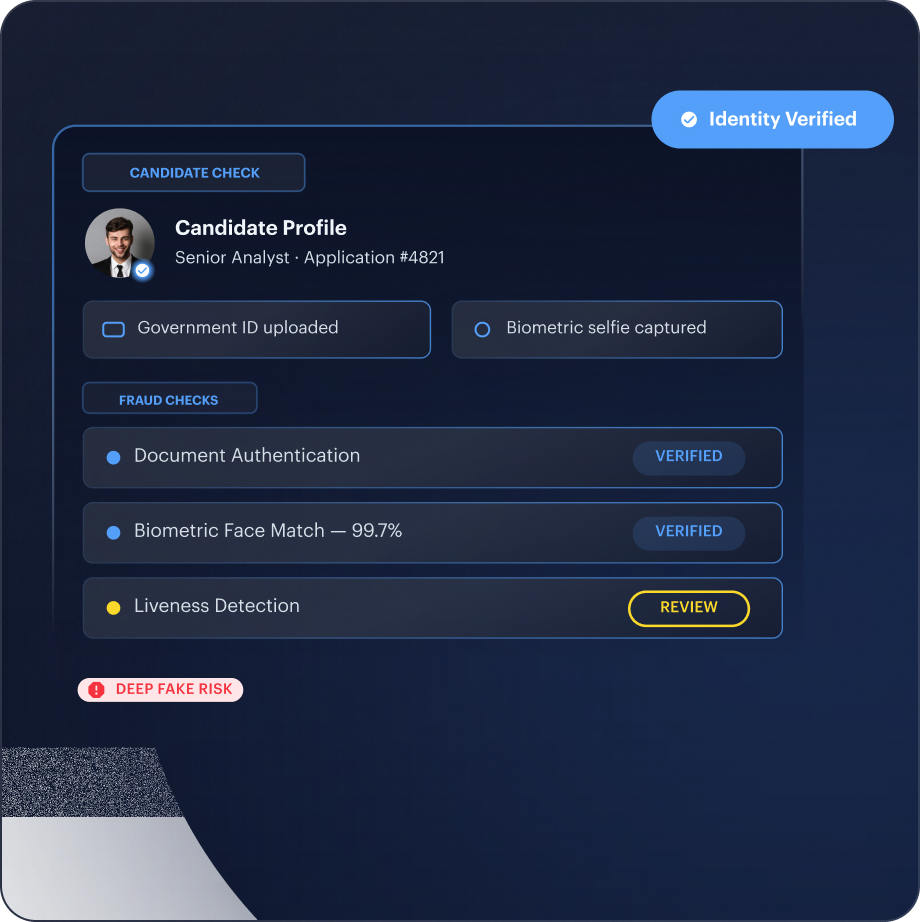

Workforce IAM Candidate Verification

Candidate Verification Account Takeover

Account Takeover Bonus/ Promotion Abuse

Bonus/ Promotion Abuse Chargeback Fraud

Chargeback Fraud Deepfake

Deepfake Document Fraud

Document Fraud Fraud Networks

Fraud Networks Impersonation Fraud

Impersonation Fraud Money Mule Activity

Money Mule Activity Multi-Accounting

Multi-Accounting Party Fraud

Party Fraud Regulatory & Compliance Risks

Regulatory & Compliance Risks Synthetic Identity Fraud

Synthetic Identity Fraud Adult Content

Adult Content Banking

Banking Crypto

Crypto Fintech

Fintech Forex

Forex Compliance

Compliance Fraud prevention

Fraud prevention Trust & safety

Trust & safety Global expansion

Global expansion Compliance Officers

Compliance Officers Developers

Developers Fraud Analysts

Fraud Analysts Product Managers

Product Managers Advanced Journey Builder (AJB)

Advanced Journey Builder (AJB) Global Trust Platform

Global Trust Platform Customer Profiles

Customer Profiles Vendor Comparison

Vendor Comparison IDV Case Management

IDV Case Management AML Case Management

AML Case Management Regulatory Reporting

Regulatory Reporting Travel Rule Protocols

Travel Rule Protocols Agentic Rule Builder

Agentic Rule Builder AI Compliance Co-Pilot

AI Compliance Co-Pilot Fraud Analytics

Fraud Analytics Fraud Hub

Fraud Hub OCR

OCR Shufti AI

Shufti AI Bank Account Verification

Bank Account Verification Biometric Duplication

Biometric Duplication Database Checks

Database Checks Document Intelligence

Document Intelligence Government ID

Government ID Mobile Driver's License

Mobile Driver's License NFC

NFC Selfie Liveness

Selfie Liveness Brand Personalisation

Brand Personalisation Deployment Options

Deployment Options Identity Methods

Identity Methods IDV Modes

IDV Modes Multi-tenancy

Multi-tenancy On-Premise IDV

On-Premise IDV Secure Capture

Secure Capture

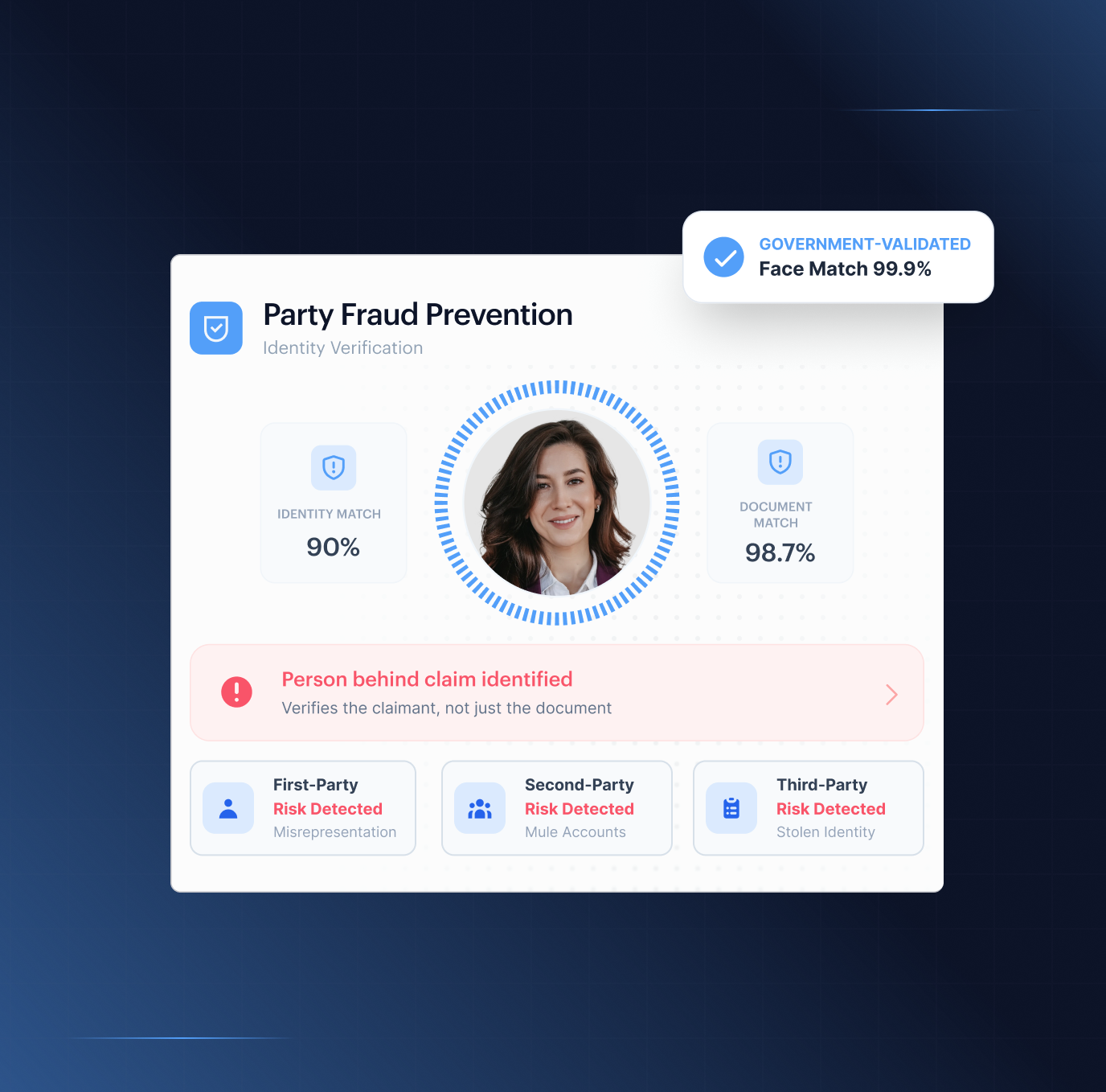

Party Fraud

Know the person. Stop the fraud

Party fraud attacks from three angles at once first-party misrepresentation, second-party mule accounts, and third-party stolen identities. From first party fraud detection onward, Shufti verifies the person behind the claim, not just the document in front of it. Government-validated. Live in days.

Live

in days

Integration

Cloud, on-prem, or hybrid

240+ Countries

covered

Seen Once Blocked Everywhere

Where Party Fraud Strikes

1. Onboarding

Third-party fraudsters arrive here. Stolen PII, AI-edited documents, synthetic identities, deepfake faces at biometric capture. The account opens before a single transaction fires

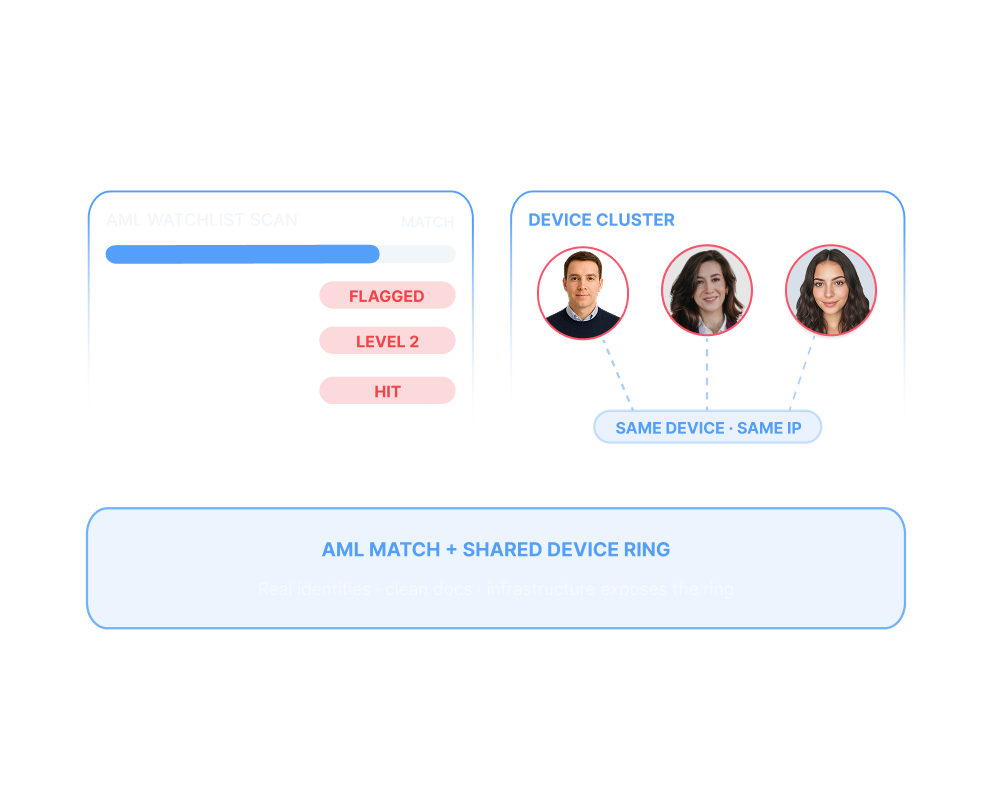

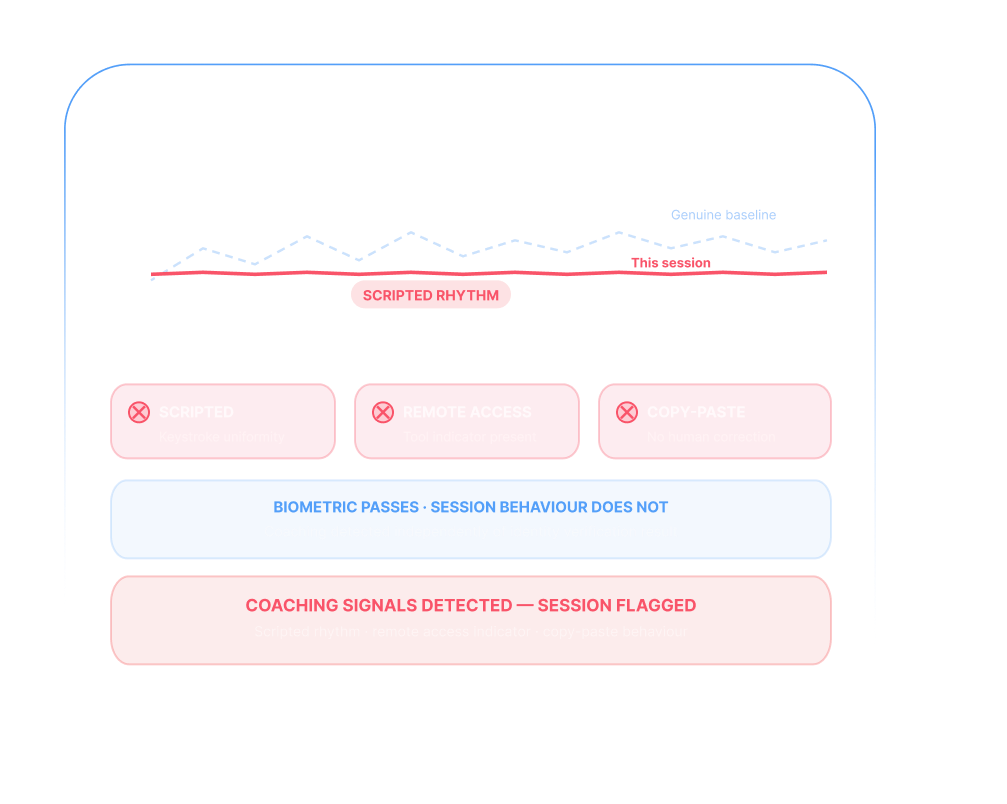

2. Authentication

Second-party fraud owns this layer. Genuine credentials handed to a mule operator. Coaching signals in the session. Shared device infrastructure connecting the ring across multiple accounts.

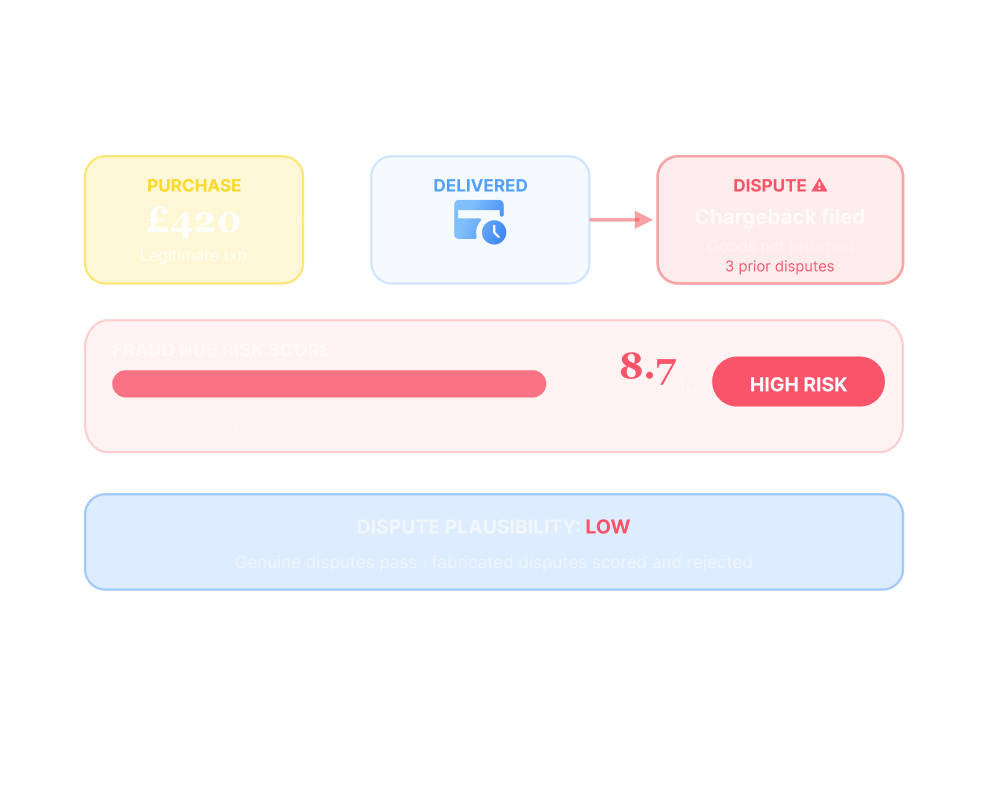

3. Transactions

First-party bust-out and friendly fraud execute here. Legitimate account, maximum credit drawn, deliberate default or chargeback filed on goods already received.

4. Ongoing

All three types return. Credit-washing schemes re-emerge. Dormant mule accounts activate. Stolen-identity accounts begin drawing on credit lines months after onboarding cleared them.

THREE TYPES, SIX PLAYS

How Shufti Stops It

Misrepresentation at Origination

First party fraud detection solutions are built for exactly this when an applicant presents a genuine identity alongside falsified income, employment, or asset documentation.

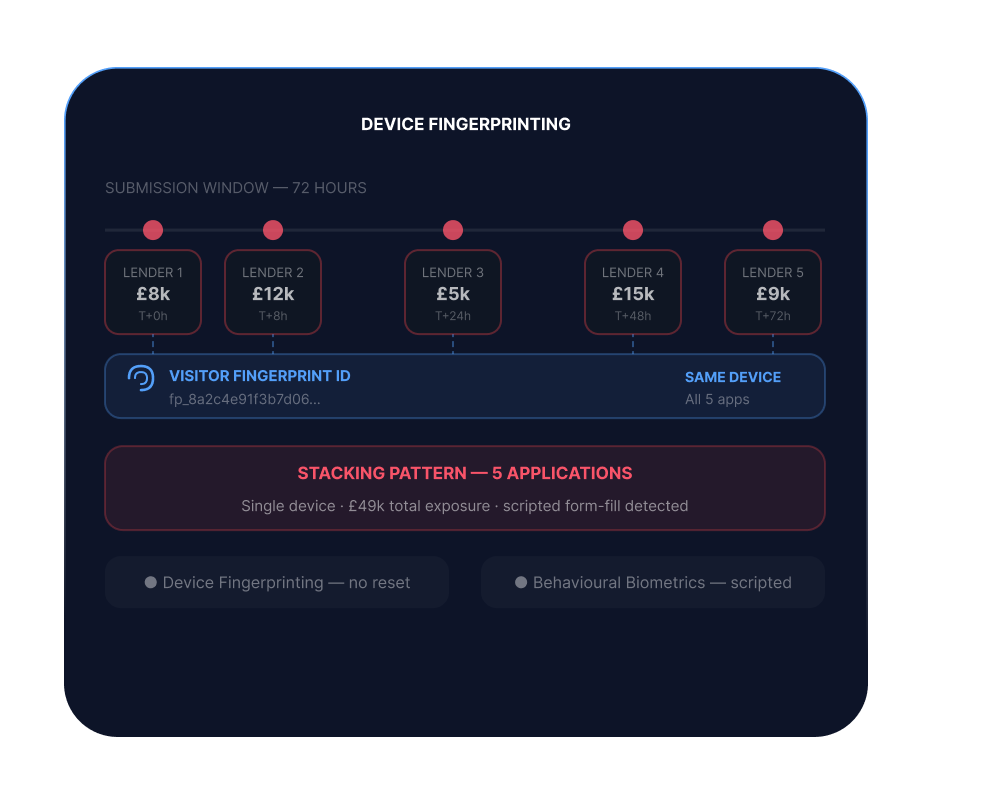

Bust-Out and Application Stacking

When multiple credit applications hit different lenders within a compressed window before any bureau update propagates.

Friendly Fraud

When legitimate transactions are disputed after goods are received.

Money Mule Accounts

When a genuine account holder opens an account on behalf of a criminal recruiter.

Coached Onboarding

When a mule is coached remotely through the verification session.

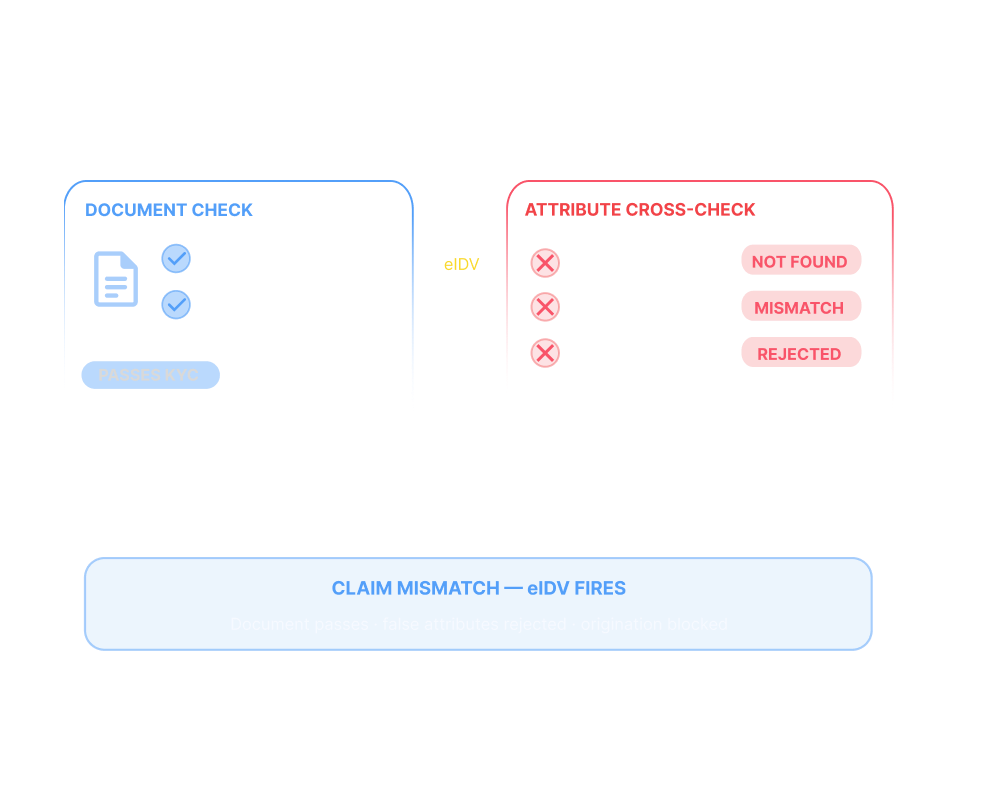

Synthetic Identity and Document Forgery

When stolen PII is combined with fabricated attributes or AI-edited document images.

- Document Verification runs forensic authenticity checks on every submission: template match, security-feature detection, MRZ checksum, font drift, and tamper detection.

- eIDV cross-references attributes against authoritative sources to expose synthetic constructions that document forensics alone cannot surface.

Industry Playbook

Party fraud hits every sector differently

Trusted Sellers, Repeat Fraud Blocked

Verify the seller is real at onboarding, then prevent re-joins with duplicate detection and optional 1:N matching across the marketplace.

The Broader Platform

Shufti covers the full attack surface

What We Do

The core workflows Shufti delivers , verifying customers at onboarding and monitoring them throughout the full relationship. Every touchpoint, one platform.

-

AI-powered document forensics, biometric verification, and real-time AML screening in one adaptive flow, verifying genuine customers while blocking synthetic identities at the door.

-

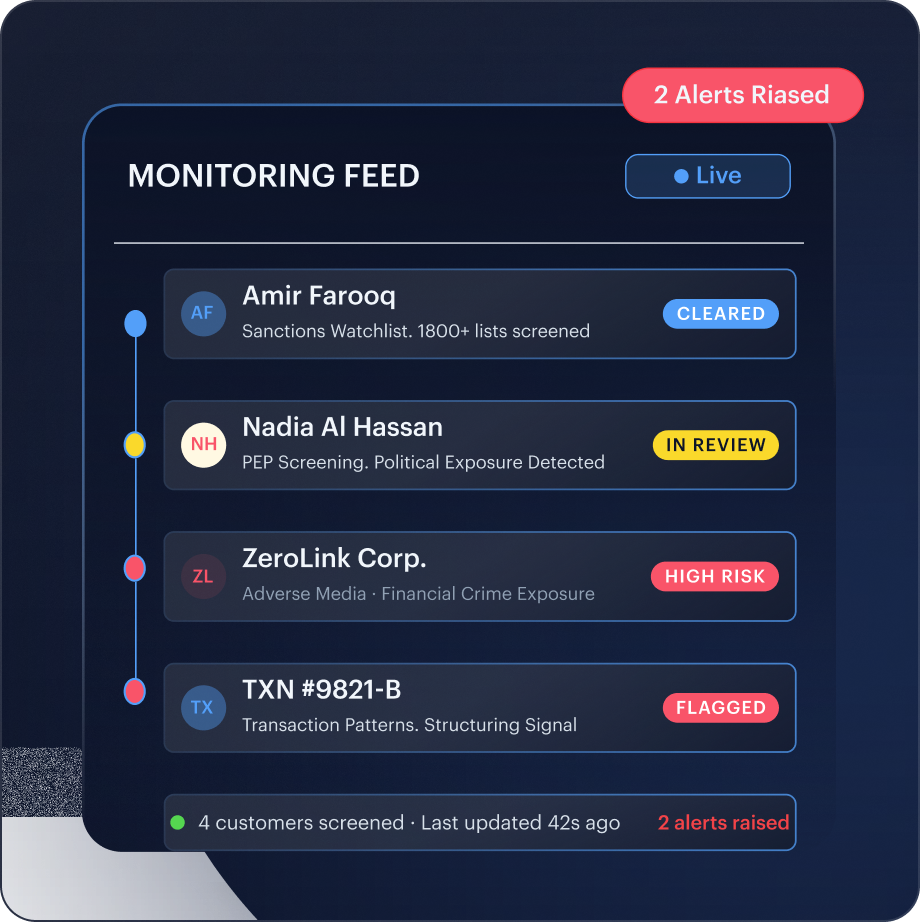

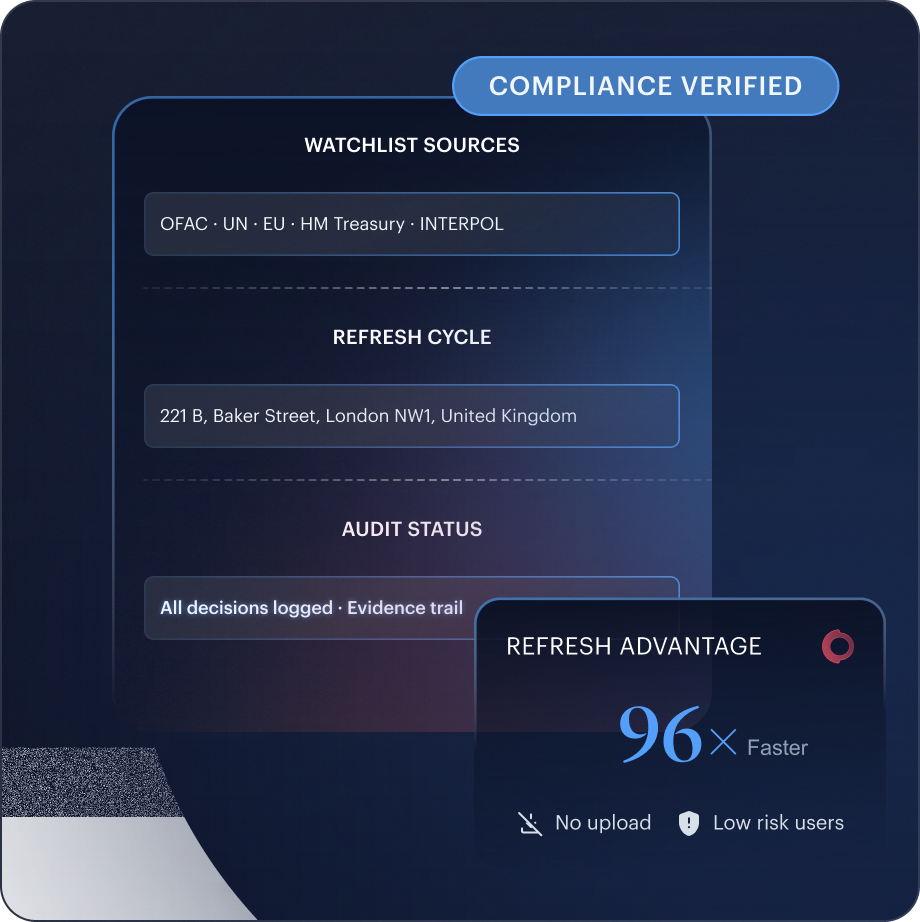

Continuous screening against 1,700+ sanctions, PEP, and adverse media sources. Customer records rechecked within minutes of a list update, not at the next periodic review.

What We Solve

The compliance and identity challenges regulated businesses face, KYC, KYB, fraud, age, workforce, and investor verification, resolved without stitching vendors together.

-

Document forensics, iBeta-certified biometric liveness, NFC chip verification, and AML screening through one API. Authenticate customers across 240+ regions from a single integration.

-

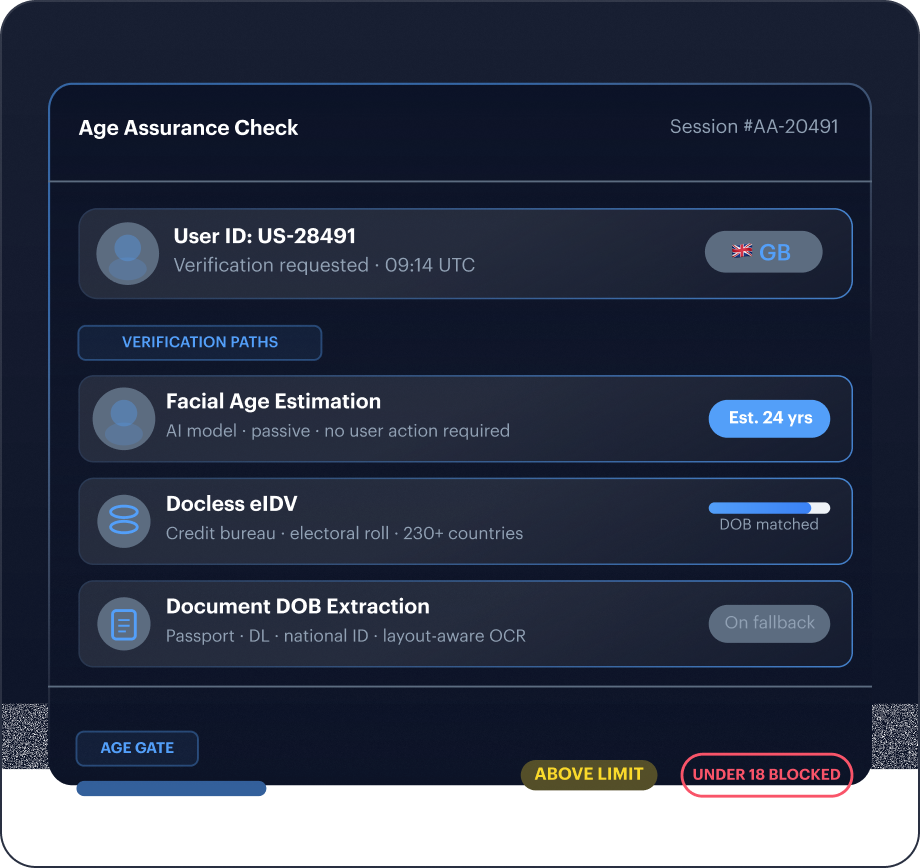

Three verification paths, facial estimation, docless eIDV, and document DOB extraction, in one flow. Stop underage access without driving away legitimate users.

-

One configurable flow for document verification, face verification, eIDV, NFC, address verification, and AML screening. One integration, one audit trail, no vendor stitching.

-

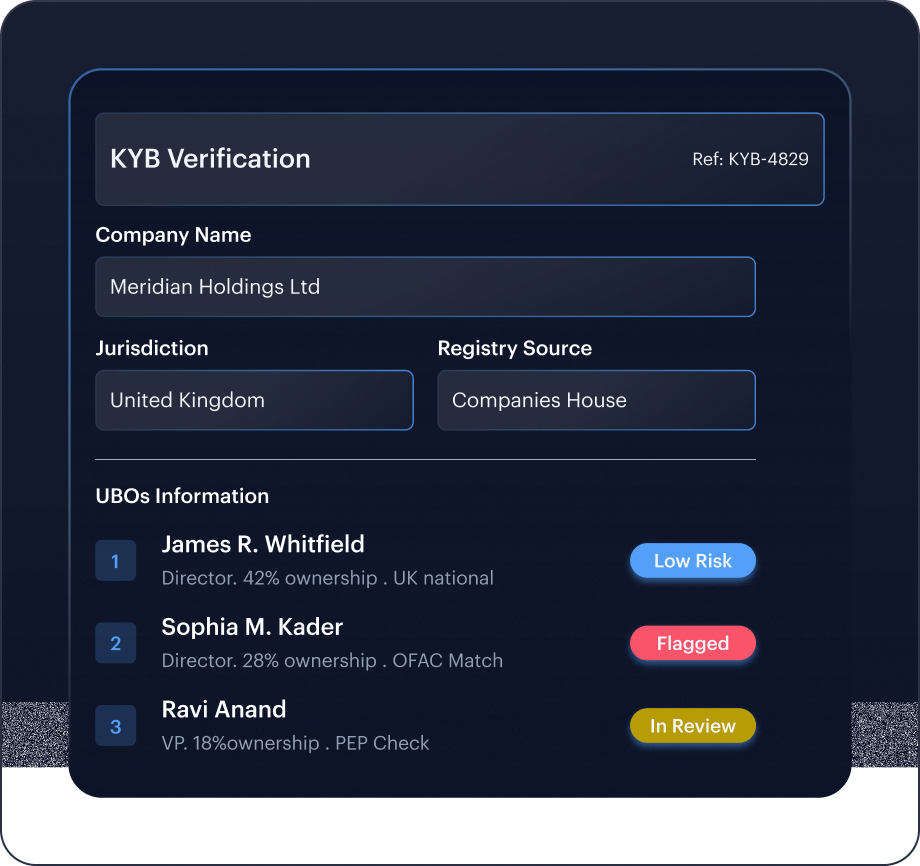

Live registry checks across 240+ official sources, complete UBO due diligence, and AML screening in one flow.

-

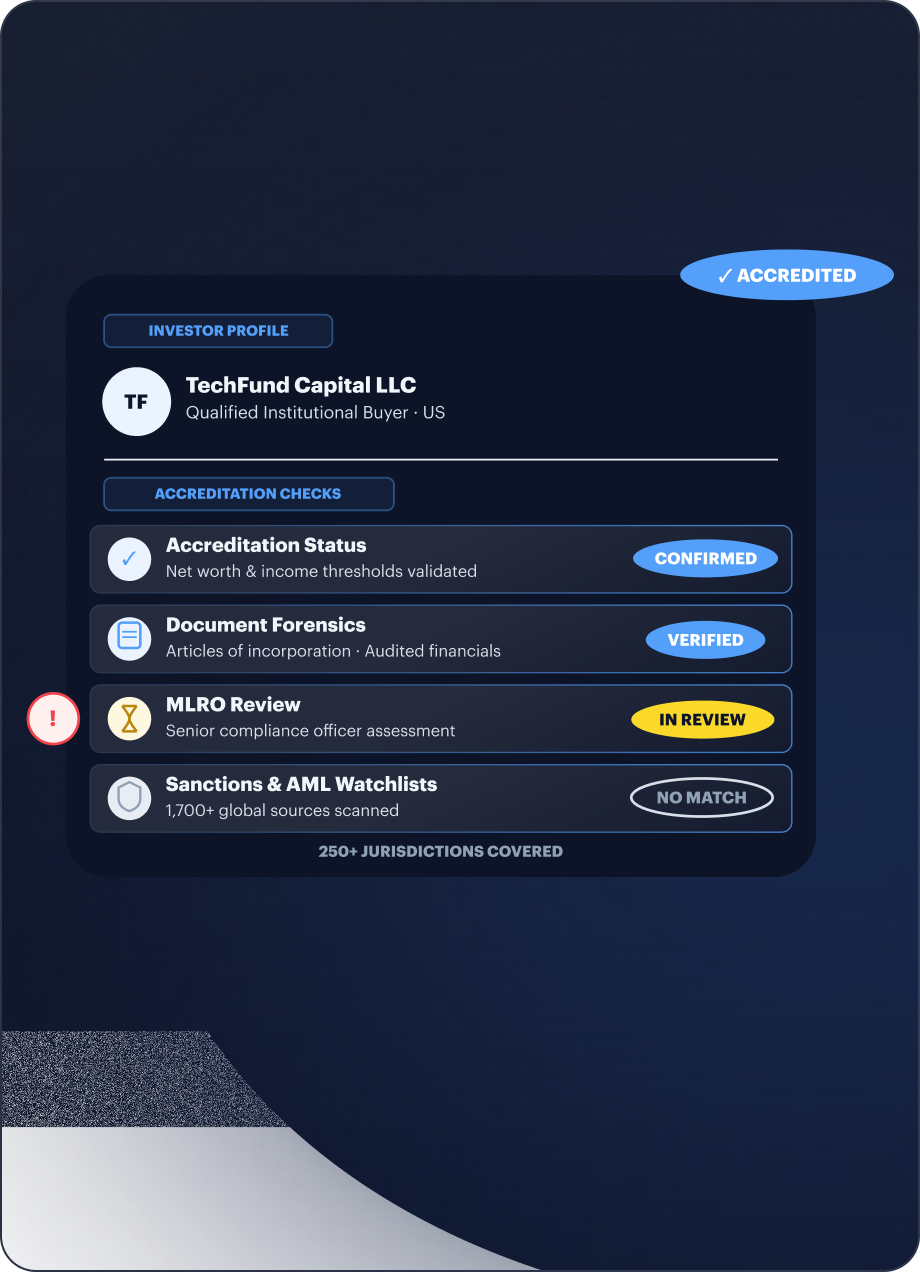

Accreditation validation, document forensics, and MLRO-backed review in one investor verification flow. Meet accredited-investor mandates across 240+ jurisdictions without additional vendors.

-

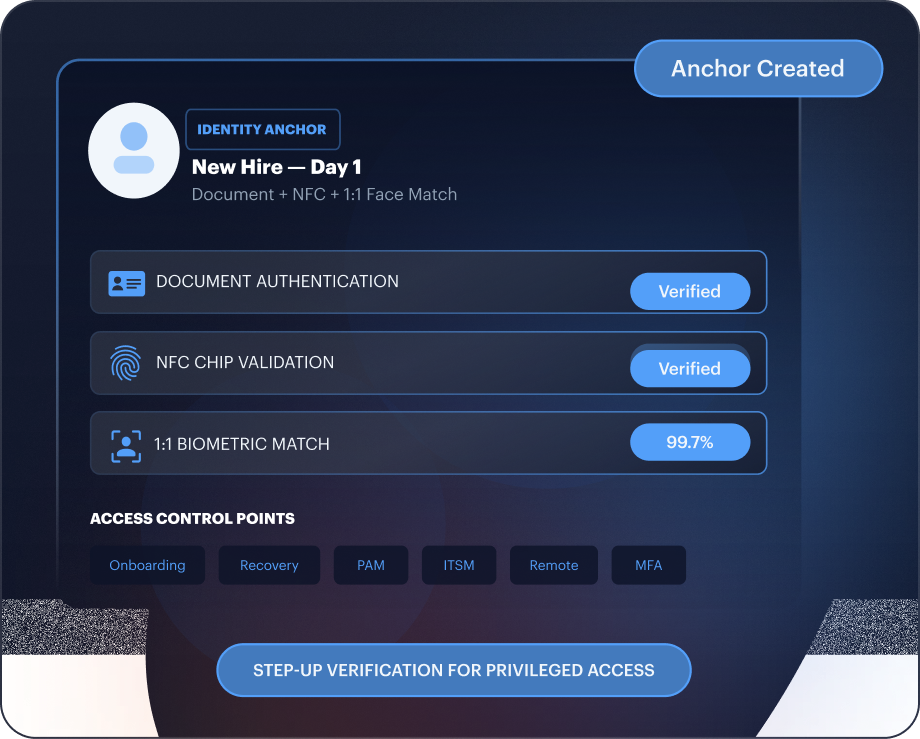

Verified identity at every access control point, onboarding, account recovery, privileged access, and MFA re-enrolment, without replacing your existing IAM stack.

-

Document forensics, biometric matching, and enhanced due diligence inside your hiring pipeline. Catch fraudulent applicants and AI-generated candidates at application stage, not after offer.

Business Outcome

The results Shufti delivers at scale, staying compliant, stopping fraud, building user trust, and expanding globally from a single integration.

-

Automated KYC, KYB, and AML across 240+ regions. Audit-ready evidence trails for every decision. Sanctions refreshed every 15 minutes — 96x faster than industry standard.

-

40+ ensemble AI models across the full customer lifecycle. Independent testing: 8 of 8 document forgeries detected where legacy stacks caught zero.

-

Verify users, sellers, workers, and businesses before risk reaches your platform. One trust layer across marketplaces, gaming, gig economy, fintech, and age-restricted services.

-

240+ countries, 10,000+ document types, 150+ languages. One API with jurisdiction-configurable workflows and regional cloud infrastructure across EU, UK, US, APAC, and MENA.

BUILT FOR YOUR TEAM

One platform. Every stakeholder

Compliance Officer

Regulator-defensible audit trail at every account-change event.

Product Manager

0.75s passive biometric. Legitimate pass rates up, fraud acceptance down. Live in a sprint.

Developer

RESTful API. Lightweight SDKs. One integration point. 100% uptime.

Fraud Analyst

Signal-level Risk Score with full breakdown. >70% fraud reduction without growing the review queue.

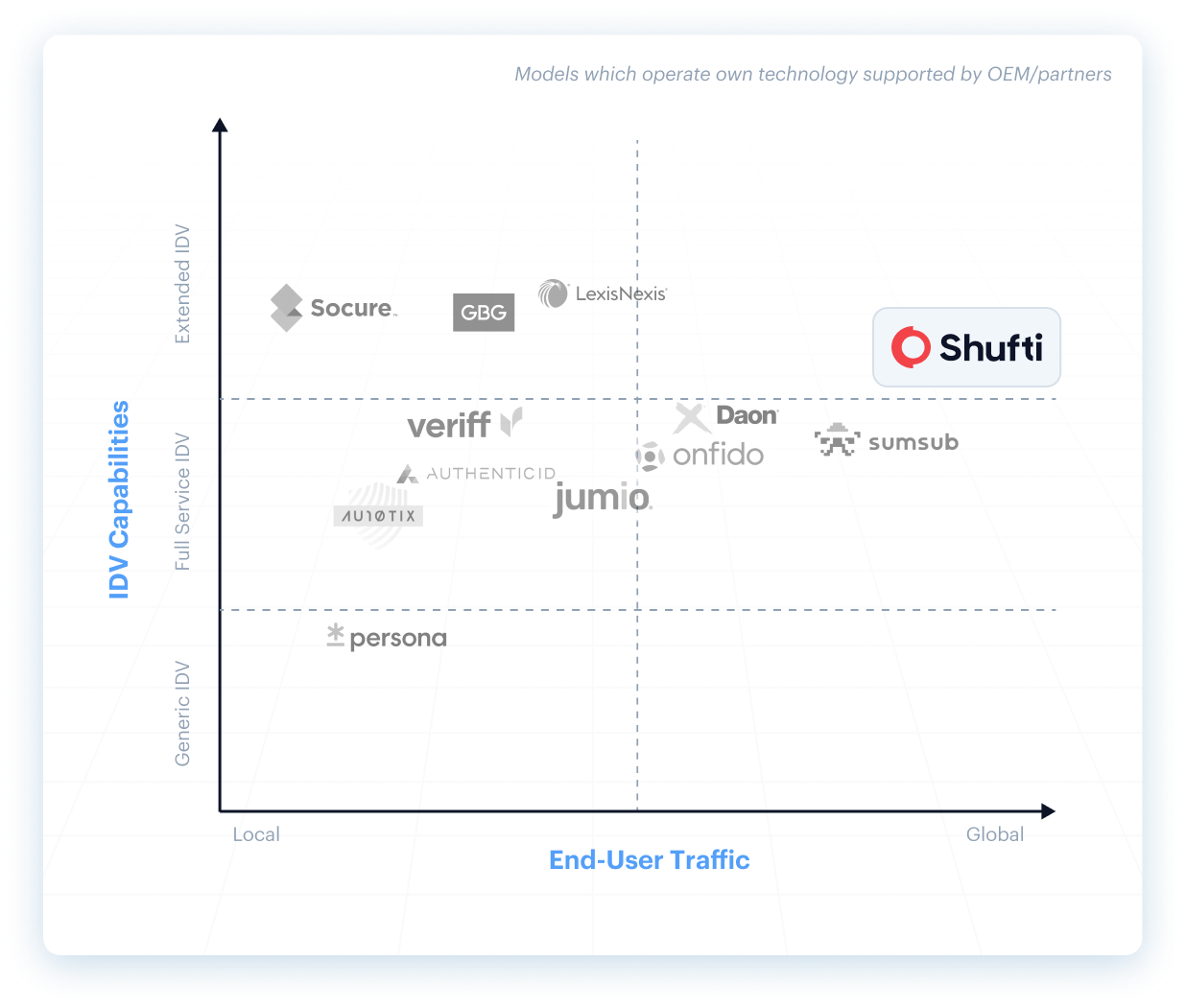

Shufti Is A Top Solution Serving Global Clients

Shufti delivers the widest global coverage with its own technology, ensuring flexibility, innovation, and stronger Extended IDV capabilities than regional or orchestrated competitors.

Download Full Report

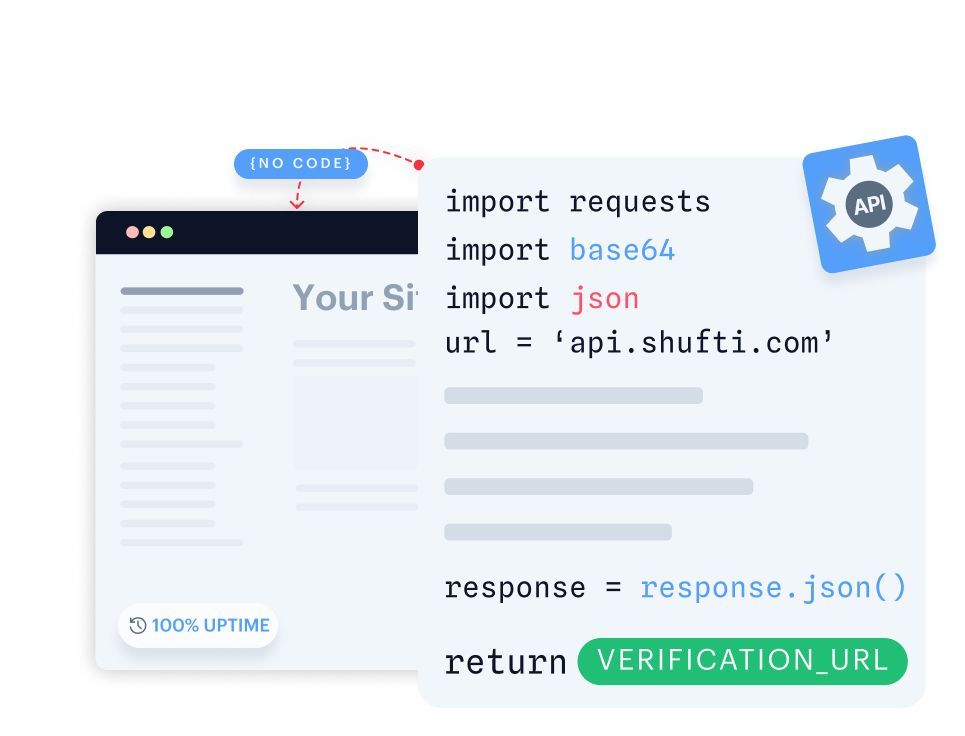

Single API, Seamless Integration

Build fully customisable verification flows with seamless backend integration.

- Gain full control by customising verification flows end-to-end.

- Integrate seamlessly with your backend for quick implementation.

- Design flexible verification journeys tailored to your users.

Launch a native verification experience in your mobile app within minutes.

- Launch native verification within minutes on iOS or Android.

- Use ready-made UI with camera, capture, and real-time feedback.

- Customise flows to fit seamlessly into your mobile app.

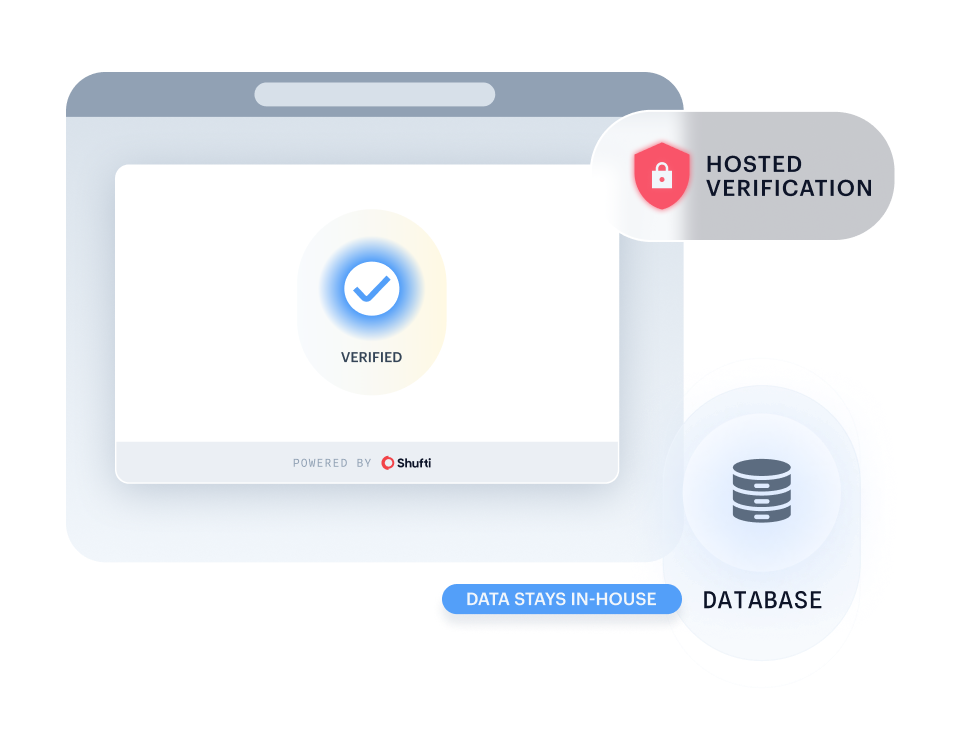

Run Shufti within your own identical-capability infrastructure for maximum data control and privacy.

- Keep all sensitive information in-house to meet strict governance and data residency requirements.

- Keep sensitive information fully private and secure in-house.

- Deploy in highly regulated sectors without compromising compliance.

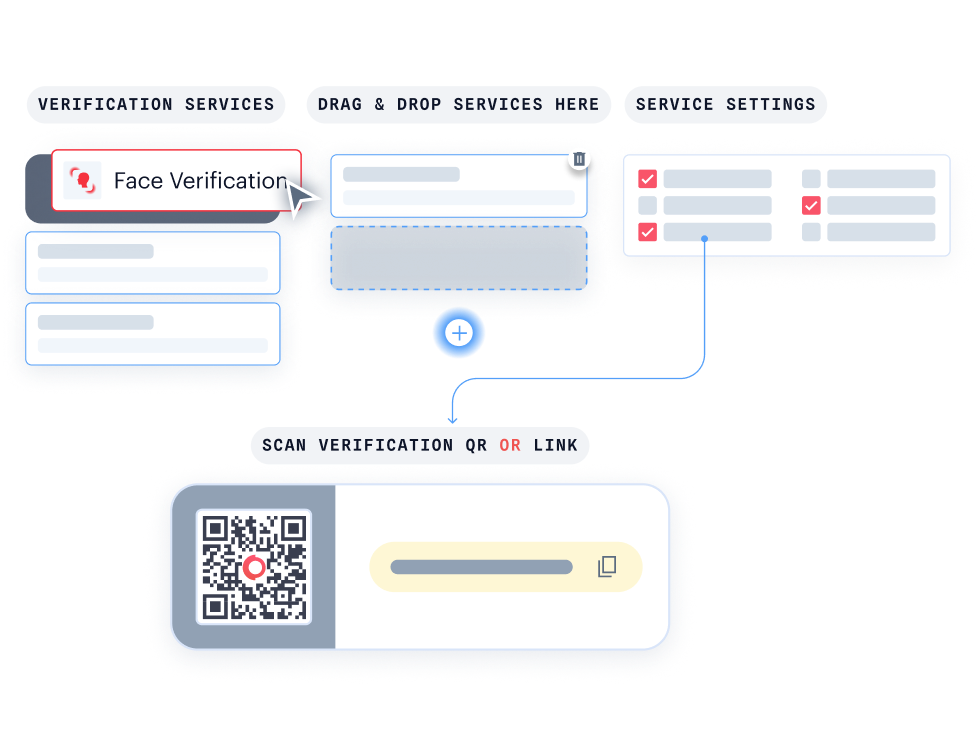

Quickly launch identity verification through a secure, customisable web link, no code required. Learn more.

- Start verifying users instantly with a no-code setup.

- Deliver a consistent identity experience via a link or embedded iframe.

- Deploy quickly via a secure link or embedded iframe.

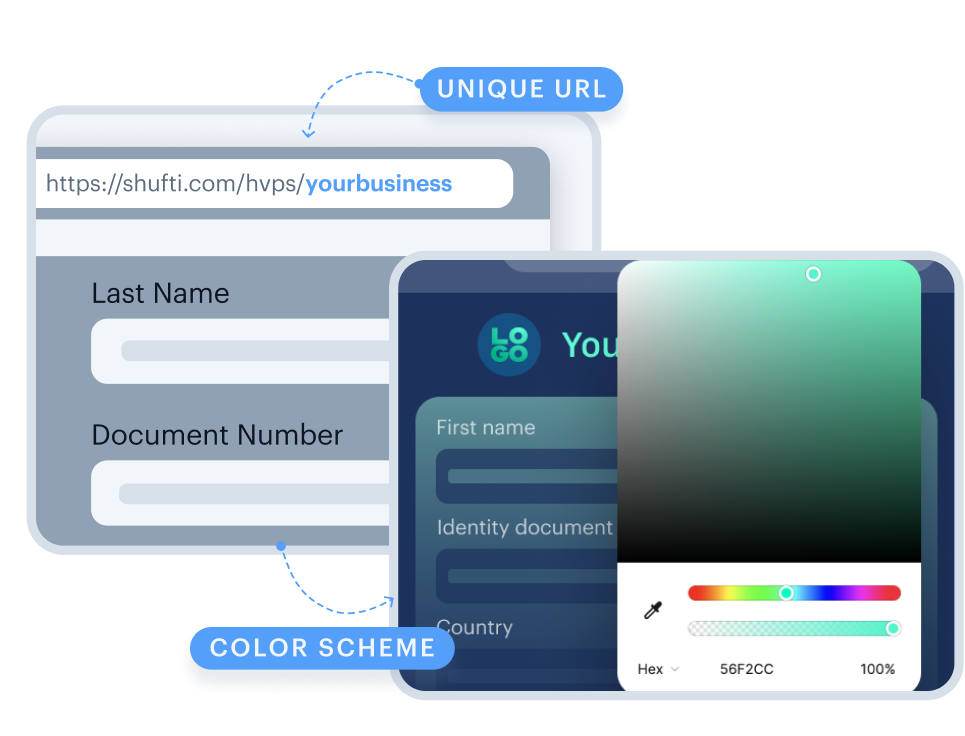

With KYC Journey Builder, create personalised verification journeys without writing a single line of code.

- Customise your journey effortlessly with drag-and-drop functionality.

- Instantly see how your verification flow looks for your users.

- Easily connect with Hosted Verification for a consistent, branded experience.

Independently Audited. Globally Certified

Certifications

Your Go-To for KYC/AML & Fraud

Resources

February 26, 2026

4 minutes read

Shufti eIDV: Building Trust Through Secured Identity

Seamless, secure, and global identity verification in seconds through a single unified layer.

Product Brief

Frequently Asked Questions

What is party fraud?

Party fraud is identity misuse categorised by who owns the identity being abused. First-party: your customer uses their real identity to deceive you. Second-party: they lend it to a criminal. Third-party: a criminal steals it without their knowledge. Most fraud stacks are built to catch one type. Party fraud operates across all three simultaneously.

Why does KYC pass first-party fraud if the identity is genuine?

KYC confirms the document is real and the face matches it. It does not verify whether the income, employment, or assets declared alongside that identity are accurate. First-party fraudsters rely on that gap. Shufti’s eIDV cross-references claimed attributes against authoritative government registries, credit bureaus, and reputable databases across 85+ countries, catching the misrepresentation that document forensics cannot reach.

How do you detect a money mule account when the person and documents are both real?

The identity is clean. The infrastructure and session behaviour are not. Device Fingerprinting links shared device signatures, IP ranges, and geolocation clusters across multiple accounts submitted by different named individuals. Behavioural Biometrics catches coaching signals, scripted typing, and remote-access patterns that genuine users do not exhibit. Nearly 2 million money mule accounts were reported in a single year; the shared infrastructure connecting them is the signal that works when documents and biometrics cannot.

Can an AI-edited document fool document verification?

Not Shufti’s. Most vendors run forensic checks on flagged documents only. Shufti runs template match, security-feature detection, tamper and edit detection, font drift analysis, and MRZ checksum on every single submission. AI-edited documents leave artefacts; forensics finds them regardless of how clean the OCR output appears. Paired with biometric liveness and pre-match deepfake defences, synthetic identities and AI-edited documents do not progress past onboarding.

Does party fraud protection apply after the account is already open?

Yes. AML Screening runs continuous monitoring after onboarding; any new sanctions hit or adverse-media article triggers a delta alert without re-submission. Fraud Hub stays active at every high-risk event: login, payment, account change. Behavioural Biometrics flags the shift in session behaviour that signals a first-party bust-out beginning or a dormant second-party mule account activating.

How fast can Shufti deploy?

Live in days. Pre-built APIs, SDKs, and a no-code Journey Builder integrate with your existing fraud stack with no rip-and-replace. Clients configuring the full party fraud stack typically have protection active inside a single sprint. Expert Agent Review Modes are configured via dashboard with no additional code deployment.

Where is biometric and identity data stored?

You own your data. Shufti supports cloud, on-prem, and hybrid deployments. Biometric templates stay in your jurisdiction or your own infrastructure. Default retention is configurable. GDPR, CCPA, and SOC 2 Type II compliant by default.

Get your free Party Fraud

Blind-Spot Audit

The Blind Spot Audit rescans verified sessions with four detection engines deployed in your cloud, no PII exposure, no integration, one click.