Face Verification

Face Verification

Address Verification

Address Verification

Document Verification

Document Verification

Age Verification

Age Verification

VideoIdent

VideoIdent

Fast ID

Fast ID

Docless Verification

Docless Verification

Consent Verification

Consent Verification

NFC Verification

NFC Verification

Business Verification

Business Verification

Due Diligence

Due Diligence

Investor Verification

Investor Verification

E-Signature

E-Signature

QES

QES

AML Screening

AML Screening

Transaction Monitoring

Transaction Monitoring

Adverse Media

Adverse Media

Business AML Screening

Business AML Screening

PEP & RCA

PEP & RCA

Sanctions

Sanctions

Watchlist

Watchlist

Behavioural Biometrics

Behavioural Biometrics

Device Fingerprinting

Device Fingerprinting

Biometric Face Authentication

Biometric Face Authentication

MFA

MFA

Fraud Hub

Fraud Hub

Onboarding

Onboarding

Ongoing Monitoring

Ongoing Monitoring

KYC

KYC

KYB

KYB

KYI

KYI

Age Assurance

Age Assurance

Identity Verification

Identity Verification

Workforce IAM

Workforce IAM

Candidate Verification

Candidate Verification

Compliance

Compliance

Fraud prevention

Fraud prevention

Trust & safety

Trust & safety

Global expansion

Global expansion

Product Managers

Product Managers

Compliance Officers

Compliance Officers

Fraud Analysts

Fraud Analysts

Developers

Developers

Deepfake Detection

Deepfake Detection

Bonus Abuse / Promotion Abuse

Bonus Abuse / Promotion Abuse

Account Takeover

Account Takeover

Synthetic Identity Fraud

Synthetic Identity Fraud

Document Fraud

Document Fraud

Impersonation Fraud

Impersonation Fraud

Multi-Accounting

Multi-Accounting

Fraud Networks

Fraud Networks

Chargeback Fraud

Chargeback Fraud

Money Mule Activity

Money Mule Activity

Party Fraud

Party Fraud

Regulatory & Compliance Risks

Regulatory & Compliance Risks

Fintech

Fintech

Crypto

Crypto

iGaming

iGaming

Forex

Forex

Social Network

Social Network

Marketplace

Marketplace

Banking

Banking

Gig Economy

Gig Economy

Payments

Payments

Ride Hailing

Ride Hailing

Adult Content

Adult Content

Blind Spot Audit

Blind Spot Audit

Deepfake Detector

Deepfake Detector

Liveness Spoofs

Liveness Spoofs

Document Originality

Document Originality

Document Deepfake

Document Deepfake

Global Trust Platform

Global Trust Platform

Journey Builder

Journey Builder

Case Management

Case Management

Shufti AI

Shufti AI

Fraud Analytics

Fraud Analytics

Vendor Comparison

Vendor Comparison

Brand Personalisation

Brand Personalisation

AI Compliance Co-Pilot

AI Compliance Co-Pilot

OCR

OCR

Secure Capture

Secure Capture

Deployment Options

Deployment Options

Identity Methods

Identity Methods

API Documentation

API Documentation

Mobile SDKs

Mobile SDKs

Service Status

Service Status

Help Center

Help Center

Contact Us

Contact Us

Technical Support

Technical Support

Supported Documents

Supported Documents

Supported Countries

Supported Countries

Content library

Content library

Blogs

Blogs

News

News

Reports

Reports

Insights

Insights

Knowledgebase

Knowledgebase

ROI calculator

ROI calculator

About

About

Career

Career

Press Release

Press Release

Certifications

Certifications

Partnership

Partnership

Awards

Awards

Events & Webinar

Events & Webinar

Interactive Demo

Interactive Demo

Podcast Studio

Podcast Studio

Spotlight Studio

Spotlight Studio

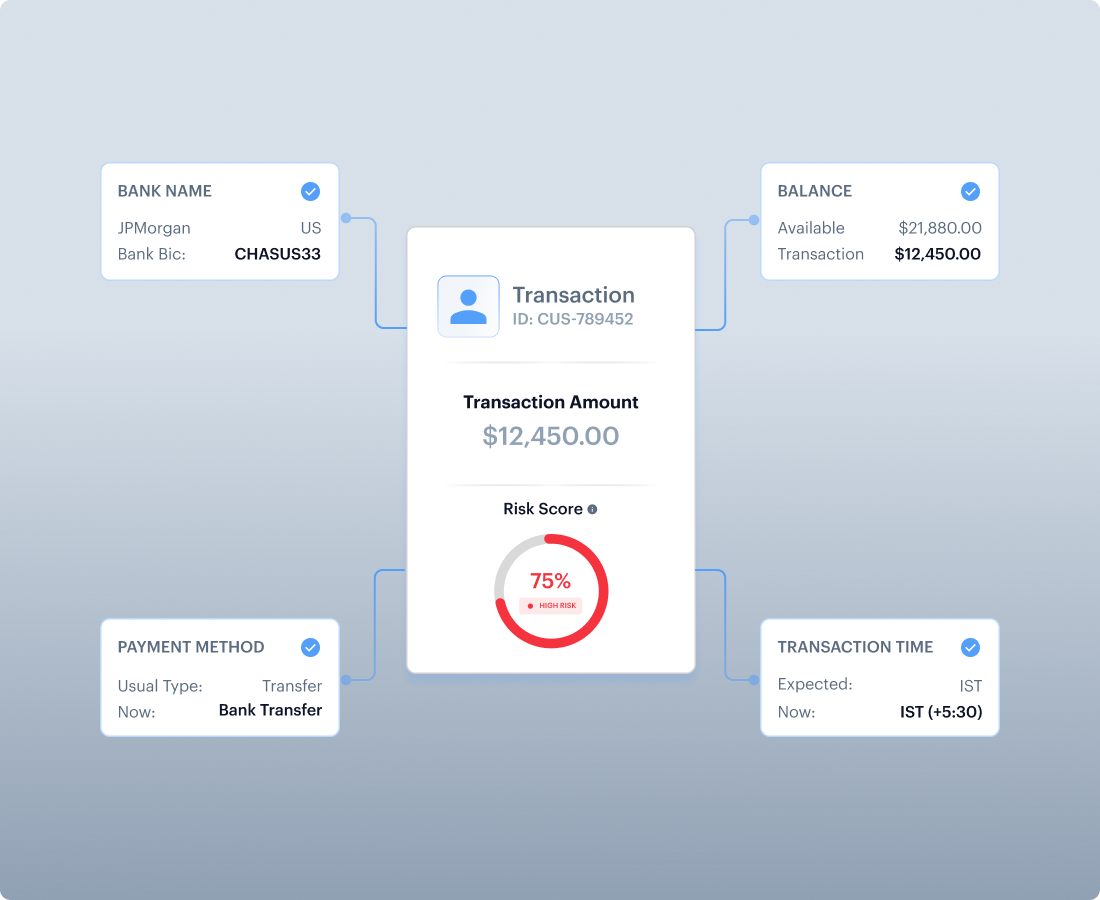

Transaction Trust Monitoring

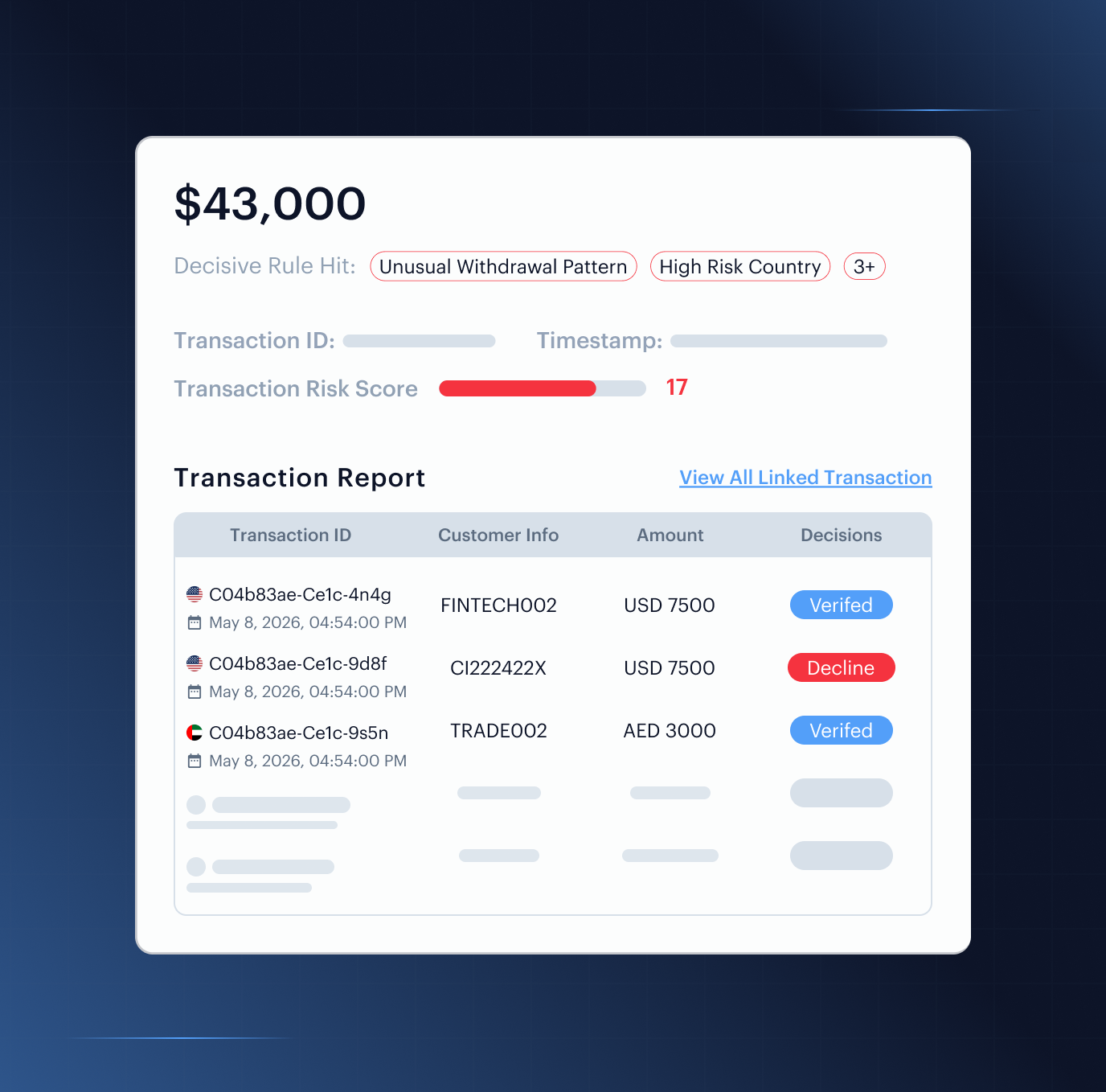

Transaction Monitoring Built For Faster Alert Triage

Shufti scores every transaction against deterministic AML and fraud rules, anchored to the verified identity behind the account. Every alert shows what triggered, why it matters, and what evidence supports the decision, so compliance teams can move from detection to defensible action without rebuilding context from separate systems.

Book a Demo

Evidence at Every Decision, Auditability at Every Step

One Platform for KYC, AML, and Transaction Monitoring

One Platform, One Trail, Zero Gaps

Verified identity, KYC outcome, screening status, customer risk, device context and transaction behaviour resolve into one decision trail that compliance can review, export and defend.

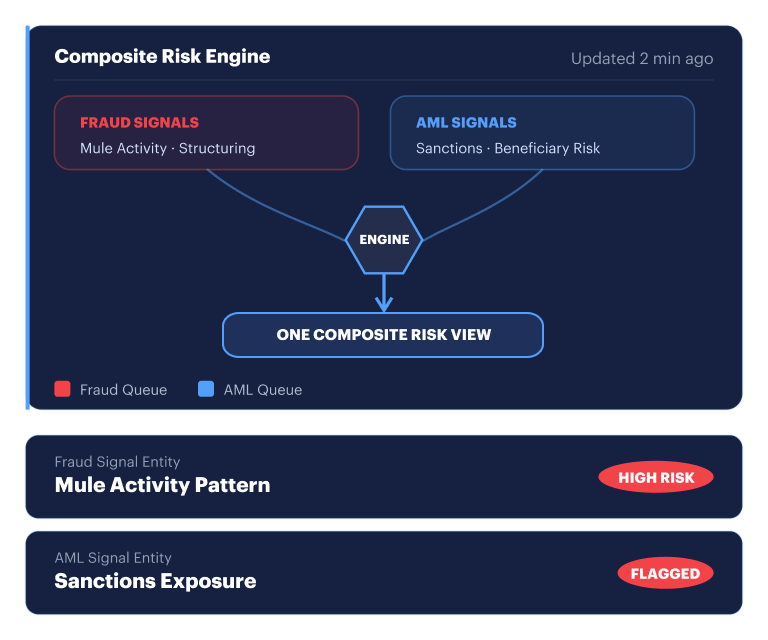

Fraud and Financial Crime, One Engine

Fraud and AML signals are evaluated together, so mule activity, structuring, beneficiary risk, device signals and sanctions exposure can resolve into one composite risk view instead of two disconnected queues.

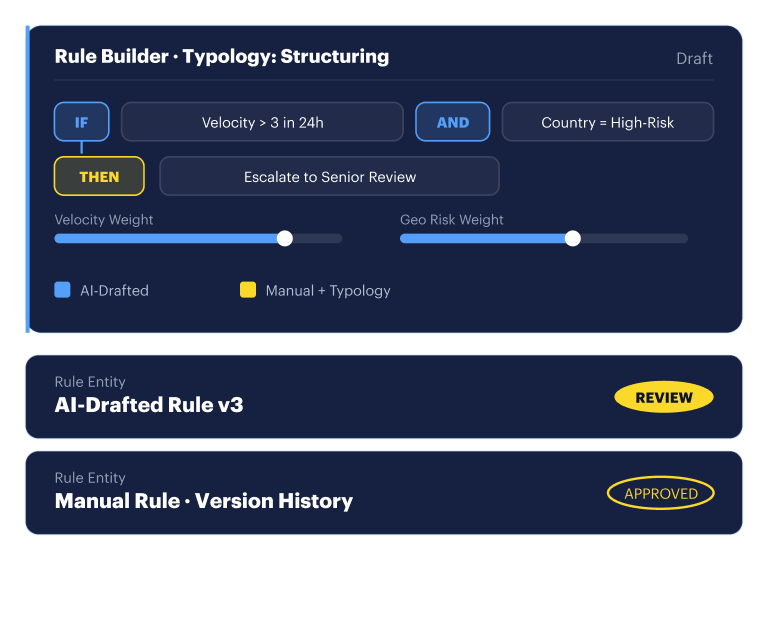

AI Rule Builder, Manual Rules, and a Typology Library

Start from typology rules, create logic manually, or use the AI wizard to draft reviewable rules. Thresholds, filters, weights, velocity windows, approvals and version history stay readable and audit-ready.

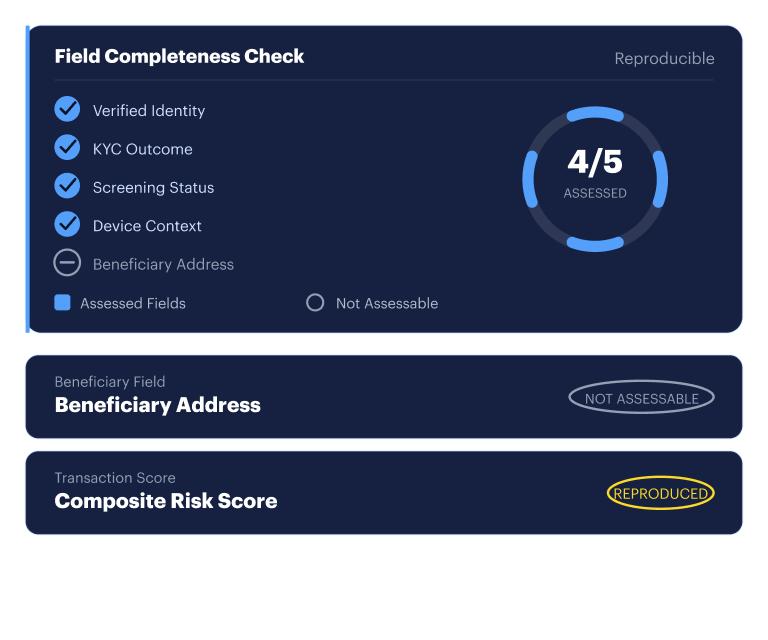

Evidence Completeness, Not Silent Passes

Scores stay reproducible, and missing data stays visible. If a required field cannot be assessed, Shufti marks it Not Assessable instead of treating the transaction as low risk.

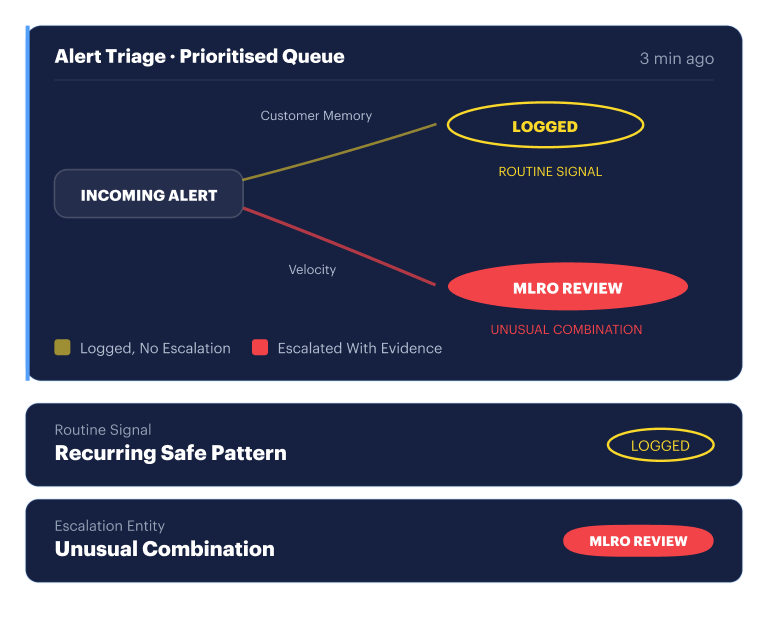

Context-Rich Alert Triage Before MLRO Review

Shufti uses identity context, customer memory, beneficiary history, velocity, previous decisions and recurring safe patterns to prioritise alerts before escalation. Routine signals can be logged without distracting the MLRO, while unusual combinations reach senior review with the evidence already attached.

CORE FEATURES OF TRANSACTION MONITORING SOFTWARE

Powering AML Transaction Monitoring at Enterprise Scale

Real-Time Transaction Monitoring

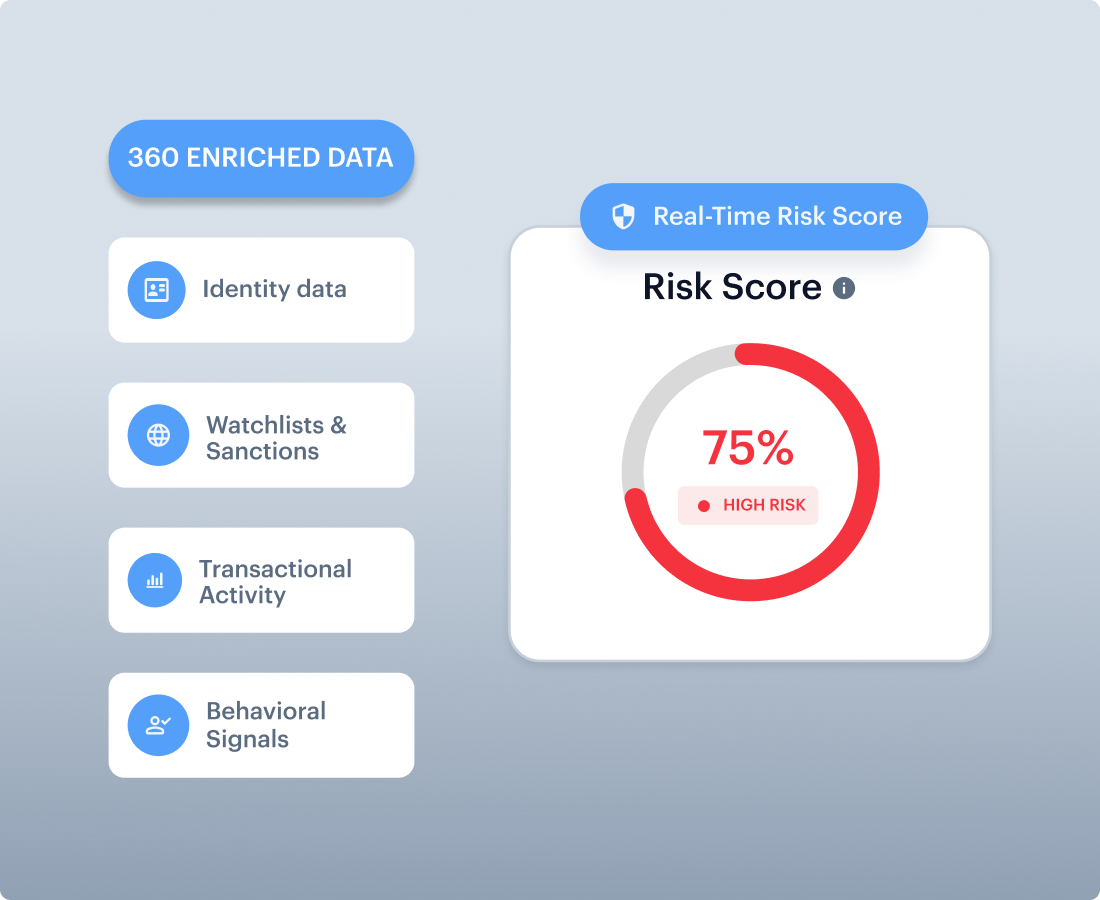

Compliance Risk Score

Quantifies regulatory, fraud and behavioural risk across the enriched transaction record.

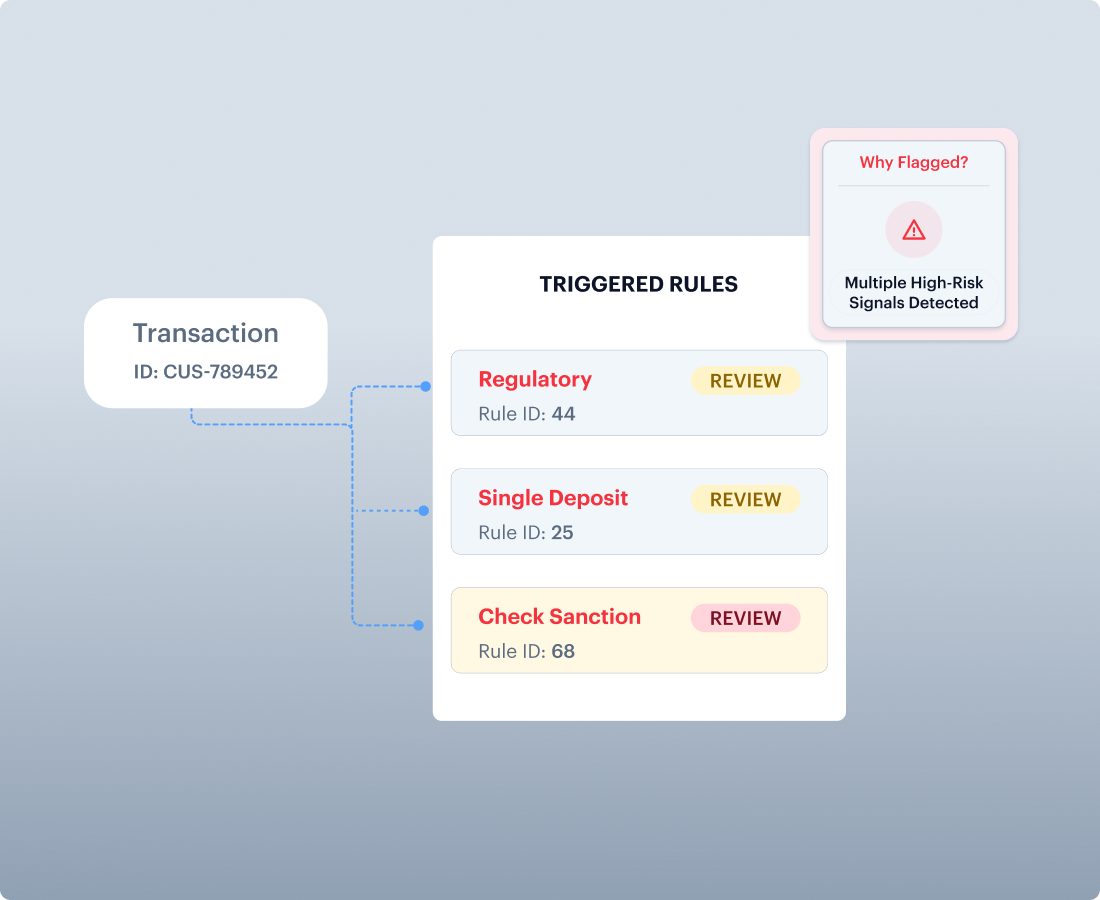

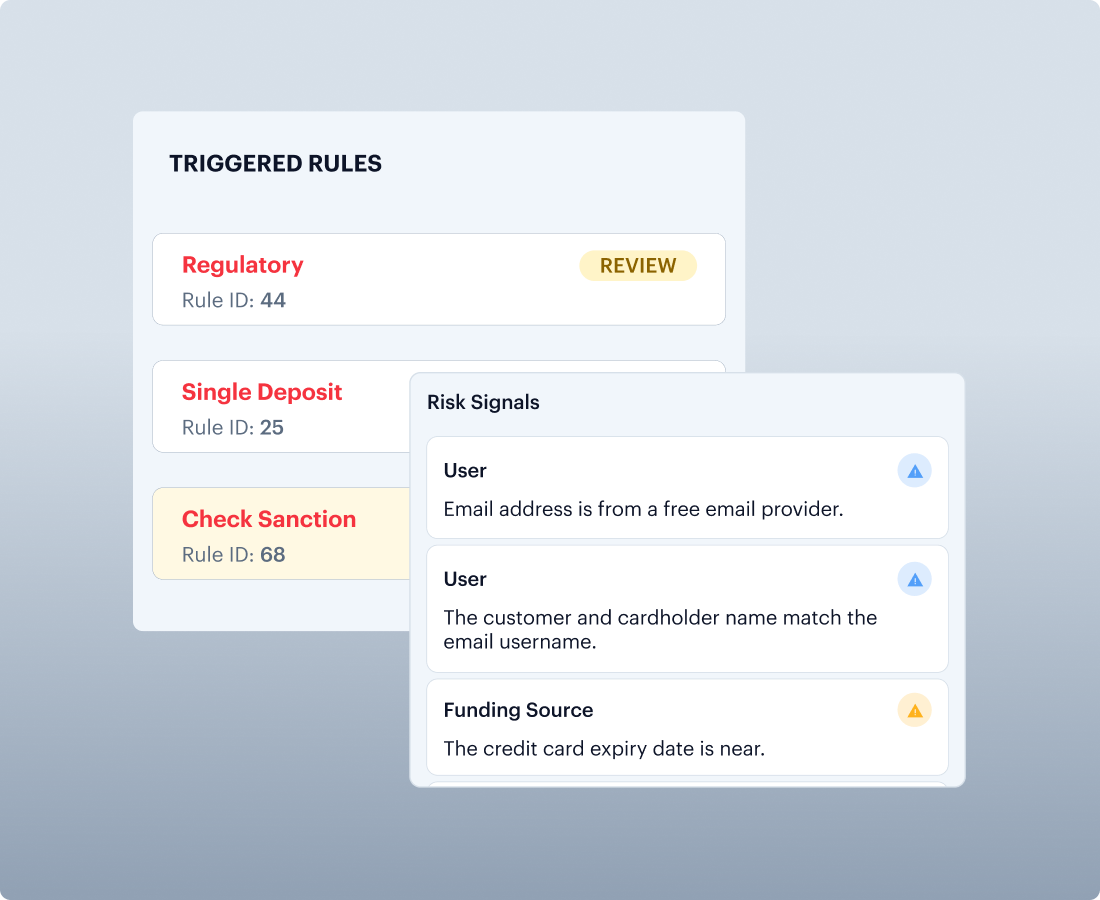

Supporting Signals

Shows which rules triggered and why the transaction was flagged, specific, traceable, defensible.

Composite FRAML Risk Score

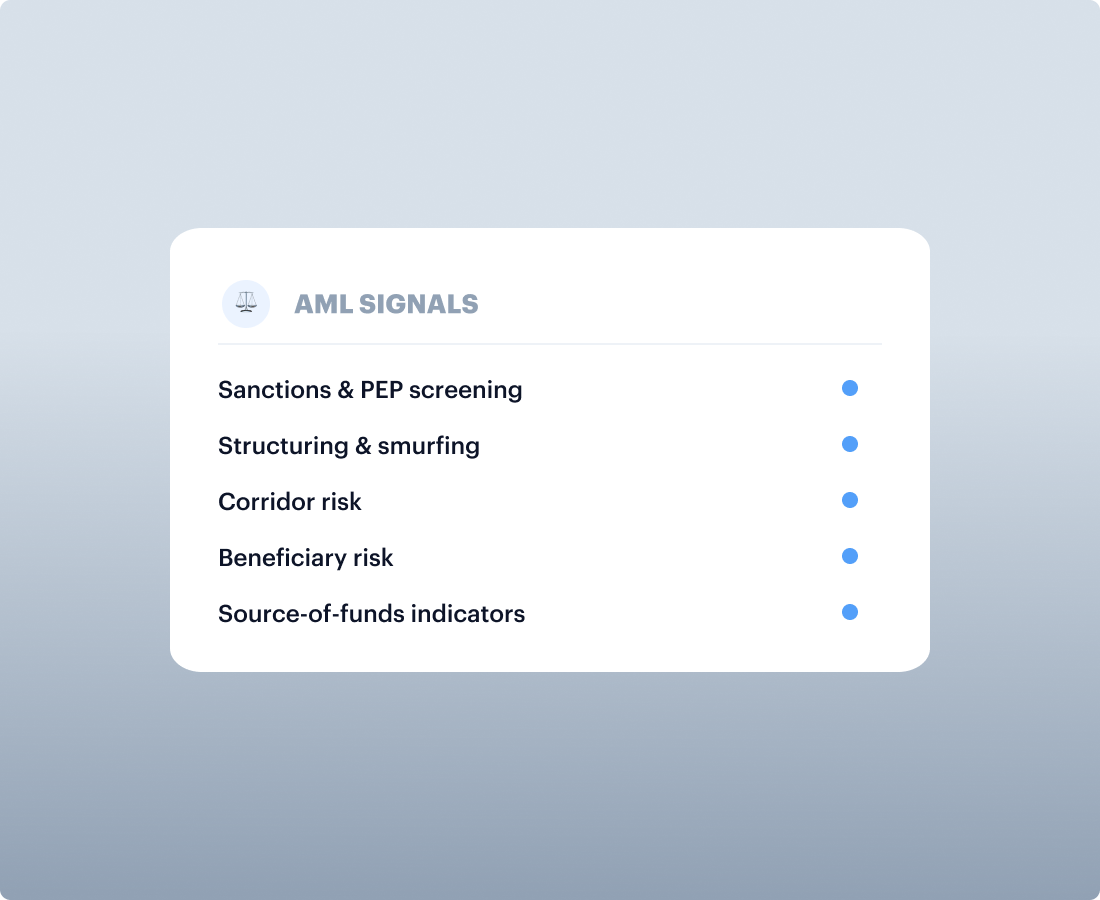

AML Signals

Sanctions, PEP, structuring, smurfing, corridor risk, beneficiary risk and source-of-funds indicators.

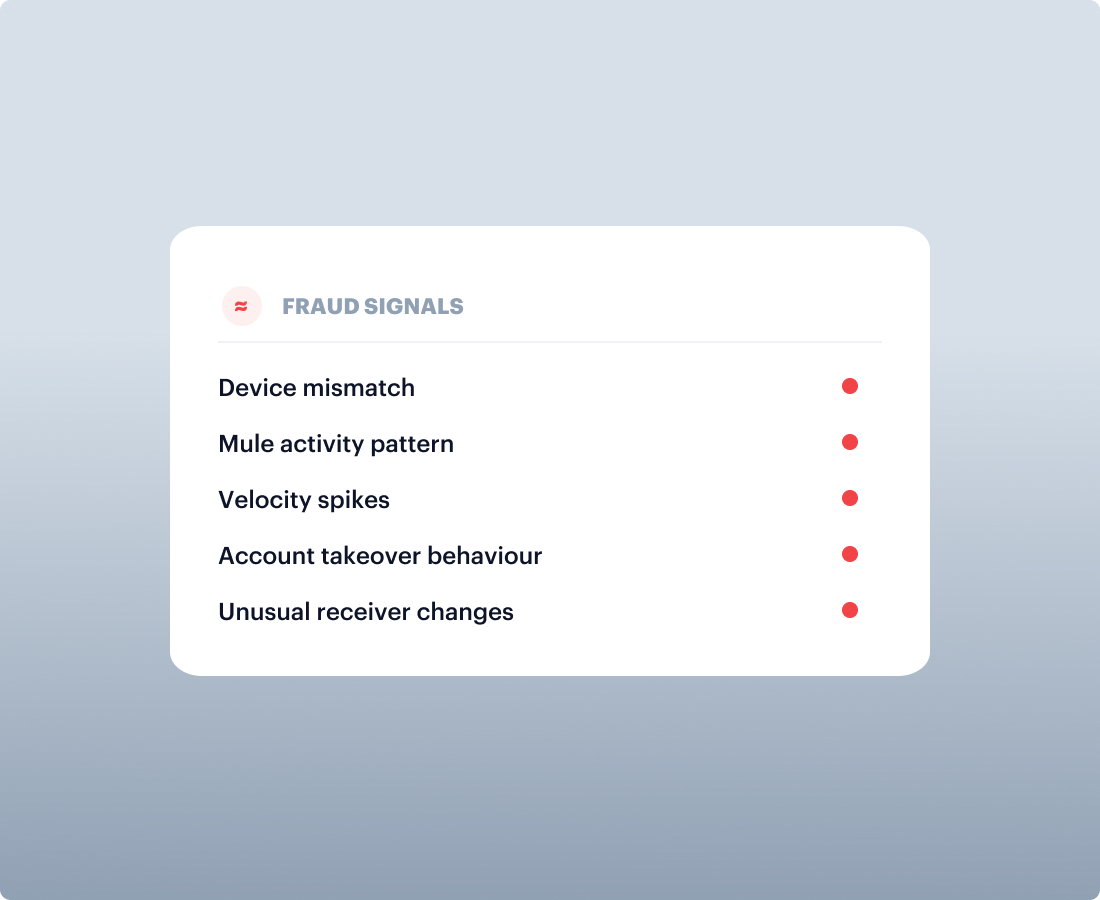

Fraud Signals

Device mismatch, mule patterns, velocity spikes, account takeover behaviour and unusual receiver changes.

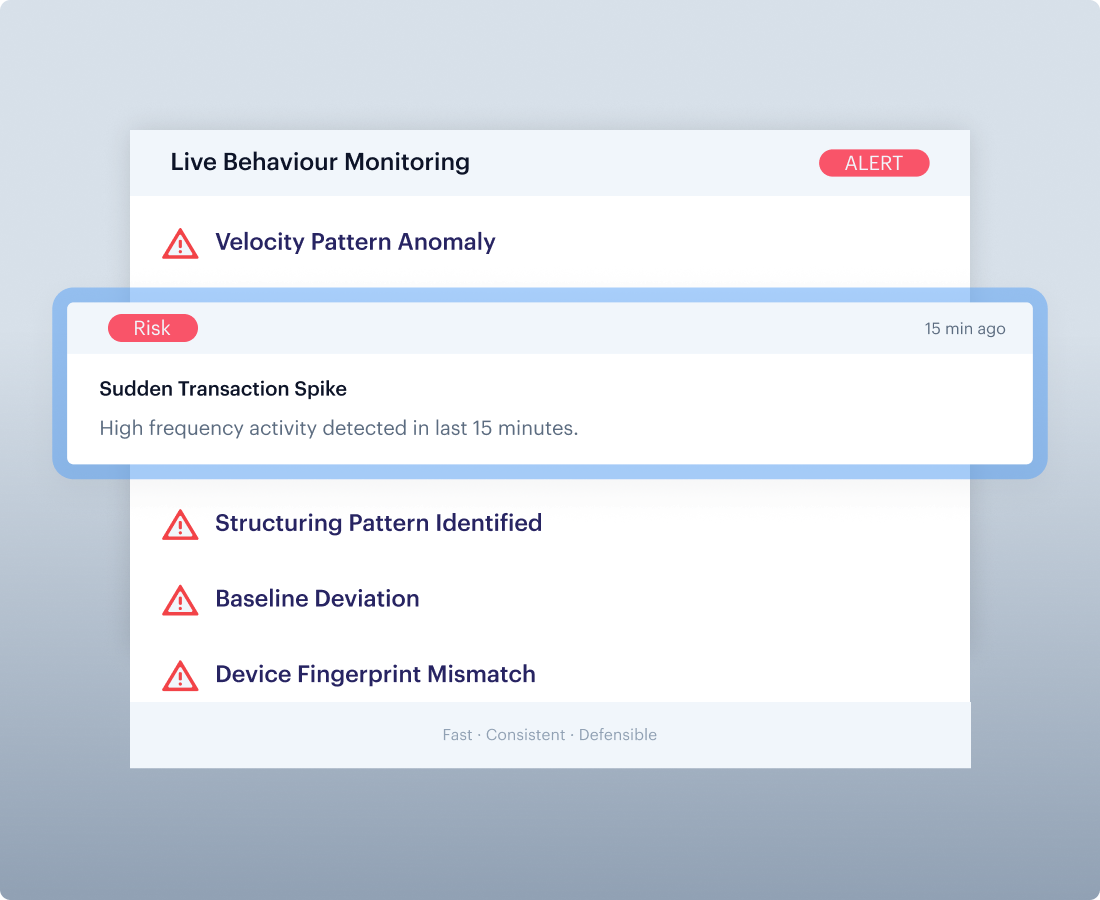

Ring Detection and Behavioural Baselining

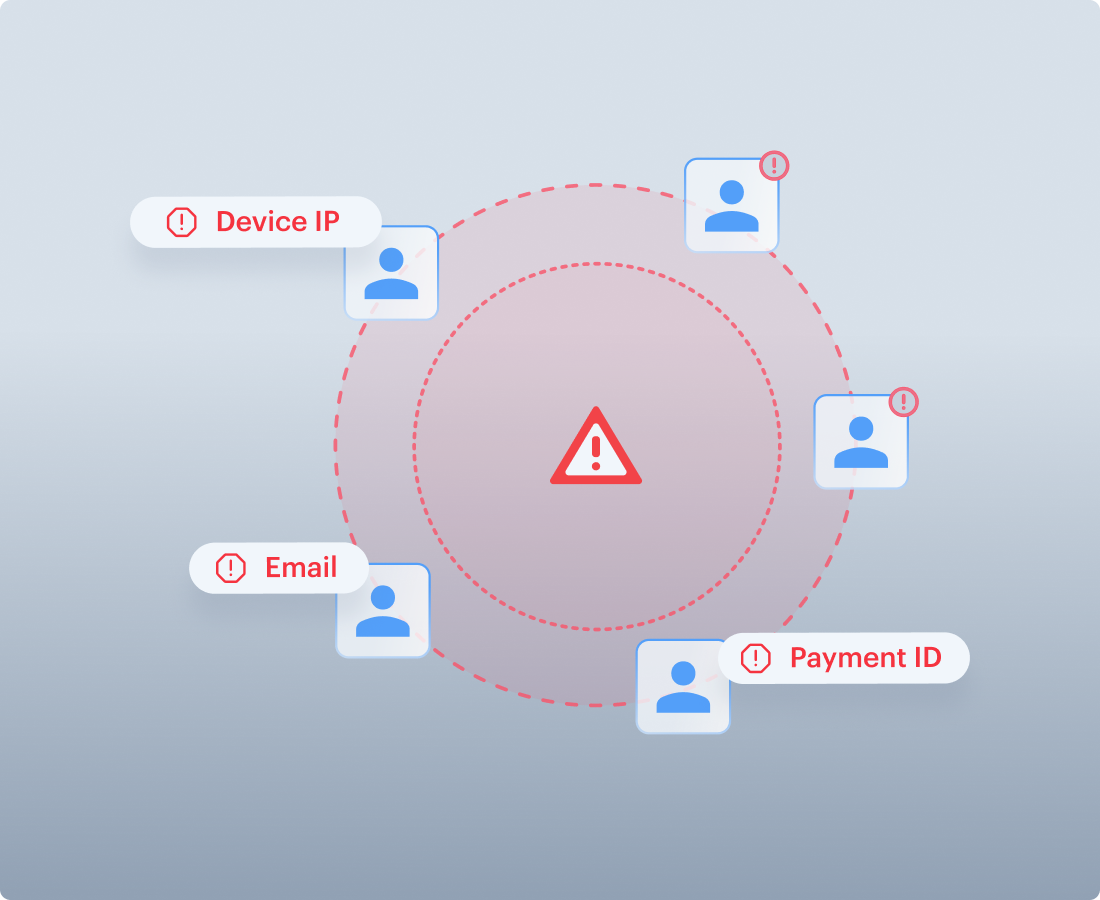

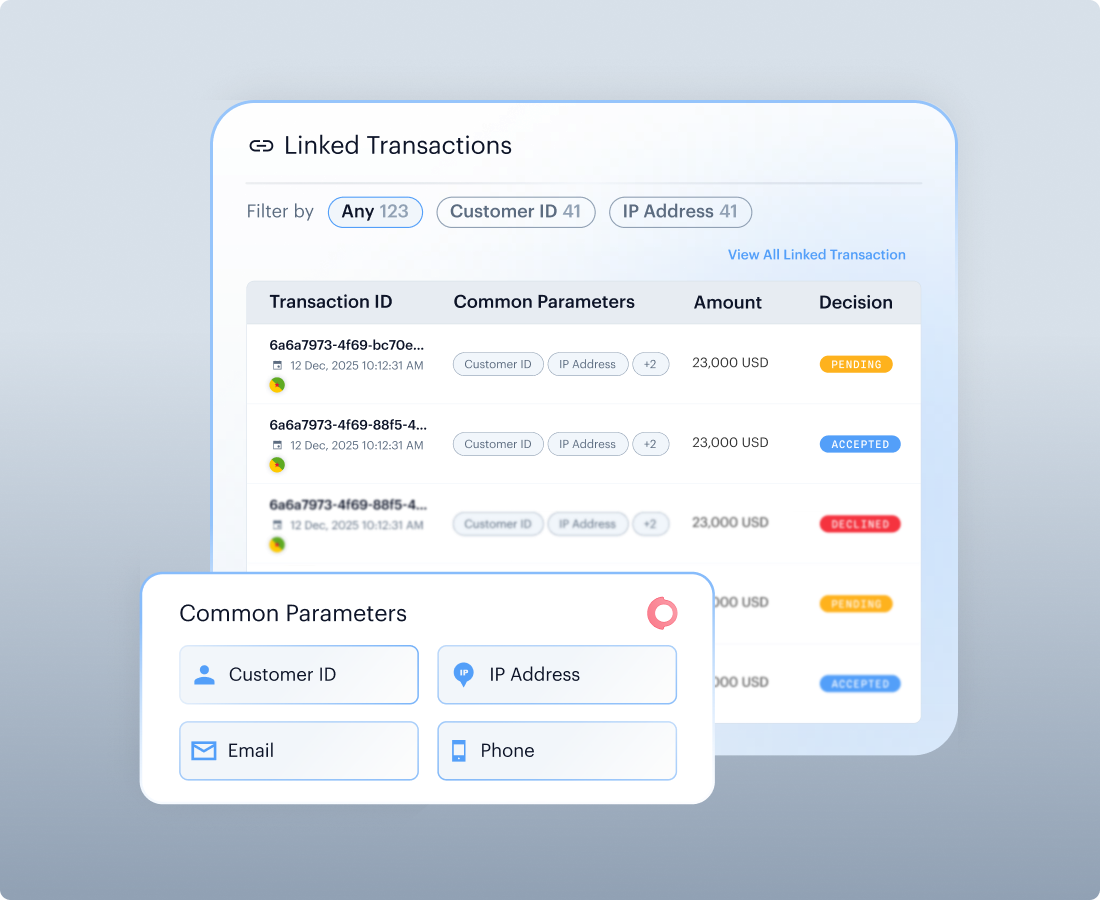

Ring Detection

Flags coordinated activity across accounts linked by email, phone, IP, device, payment identifiers or beneficiary overlap.

Transaction History

Provides the longitudinal context that distinguishes a suspicious pattern from an isolated anomaly.

Behavioural Baselining

Compares amount, frequency, timing, device consistency and transaction type against the customer's established profile.

90-Day Memory

Adds time and context so repeat safe patterns do not create unnecessary senior-review noise.

Categories of AML Transaction Monitoring System

Regulatory & Jurisdiction Risk

Sanctions, PEP, adverse media, watchlist exposure, embargoes and corridor risk.

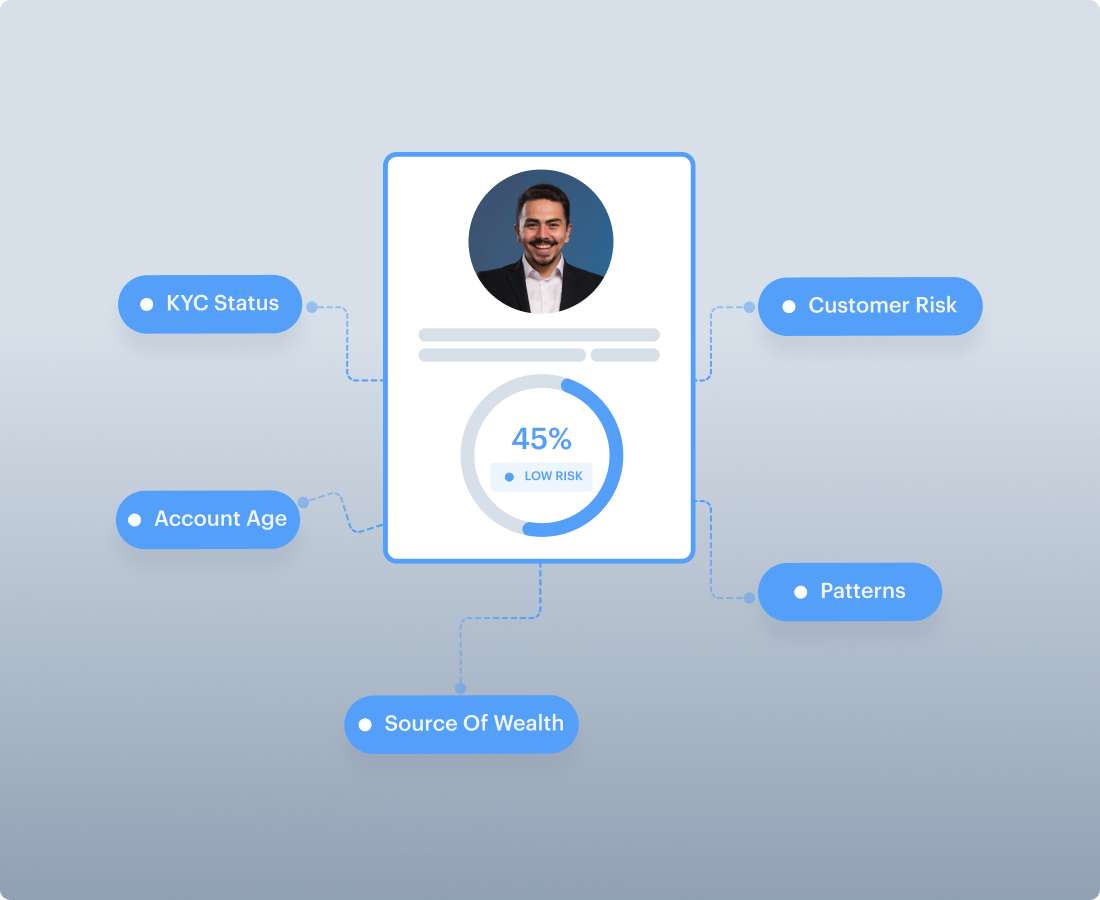

Customer Risk Profile

KYC status, account age, risk rating, source of wealth, screening outcome and prior approval history.

Transaction & Behavioural Patterns

Velocity, structuring, amount spikes, frequency anomalies, time-zone shifts and baseline deviations.

Beneficiary, IP & Location Intelligence

New recipient risk, relationship mapping, geolocation consistency, VPN or TOR indicators and address matching.

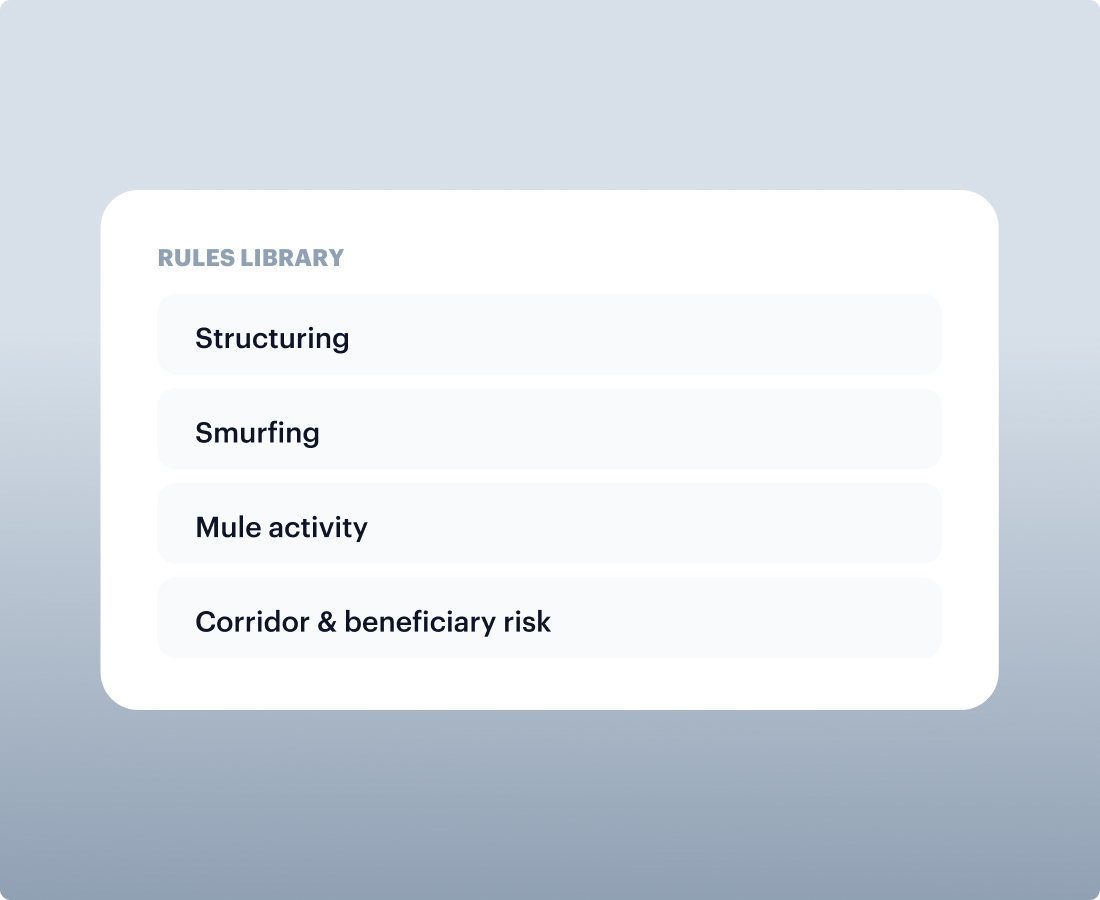

AI Rule Builder With Rules-Library Depth

Rules Library

Start from typology rules for structuring, smurfing, mule activity, corridor risk, beneficiary risk and fraud patterns.

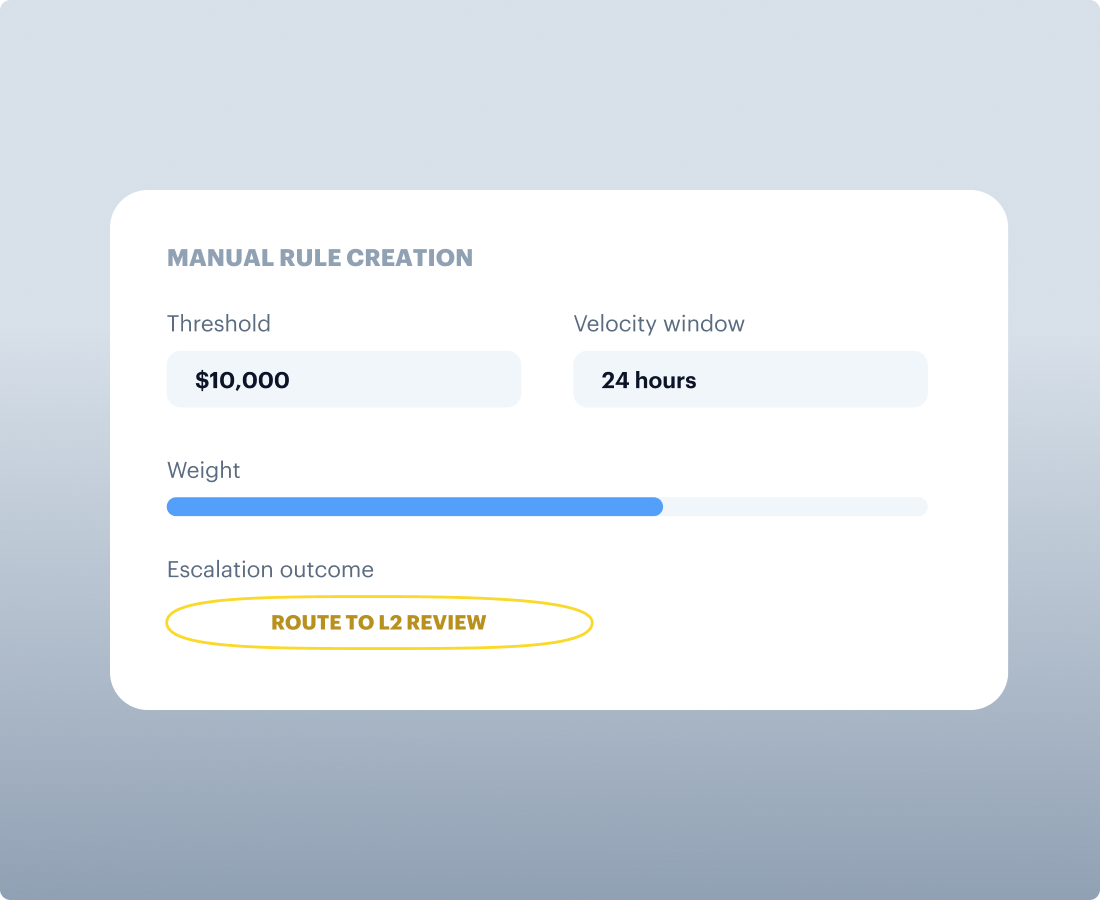

Manual Rule Creation

Set thresholds, weights, filters, velocity windows, scoring impact and escalation outcomes with governance.

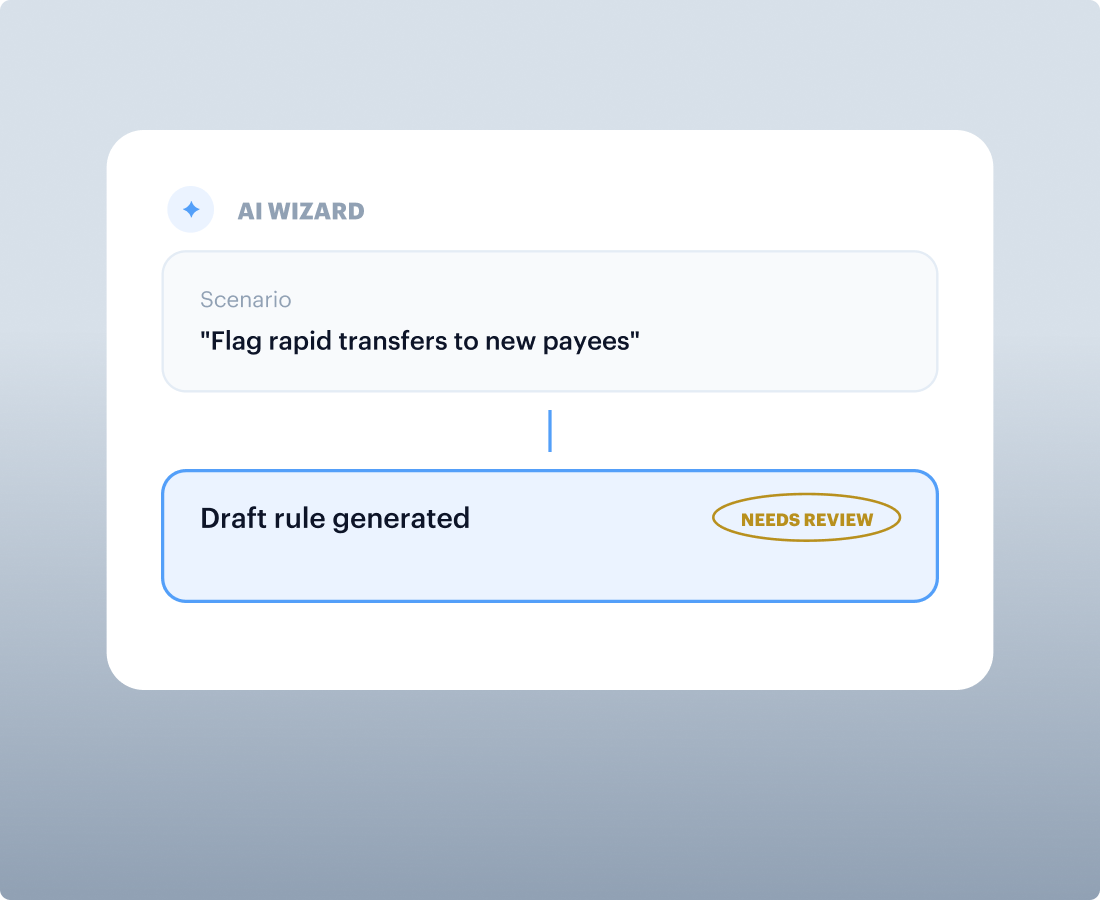

AI Wizard

Draft rule logic from risk scenarios, then require compliance review before deployment.

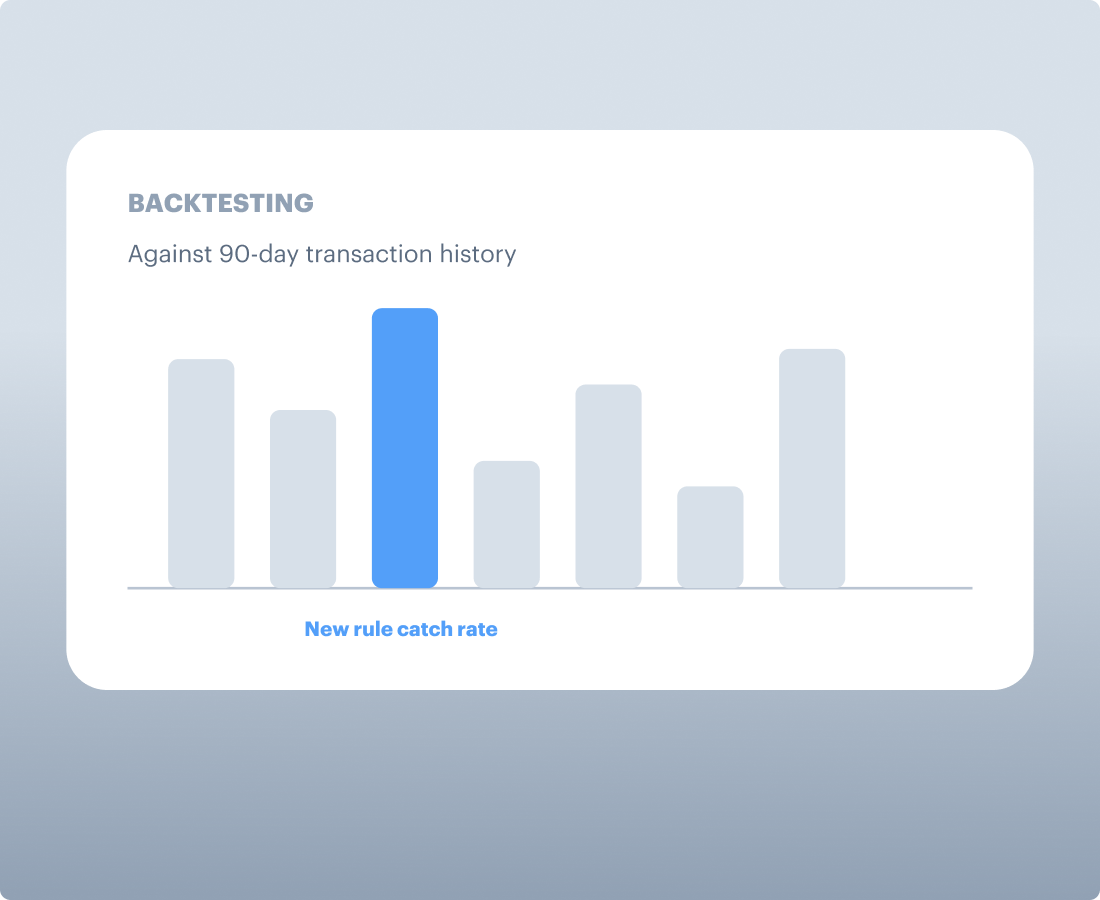

Backtesting

Test changes against historical transaction and customer behaviour before moving rules into production.

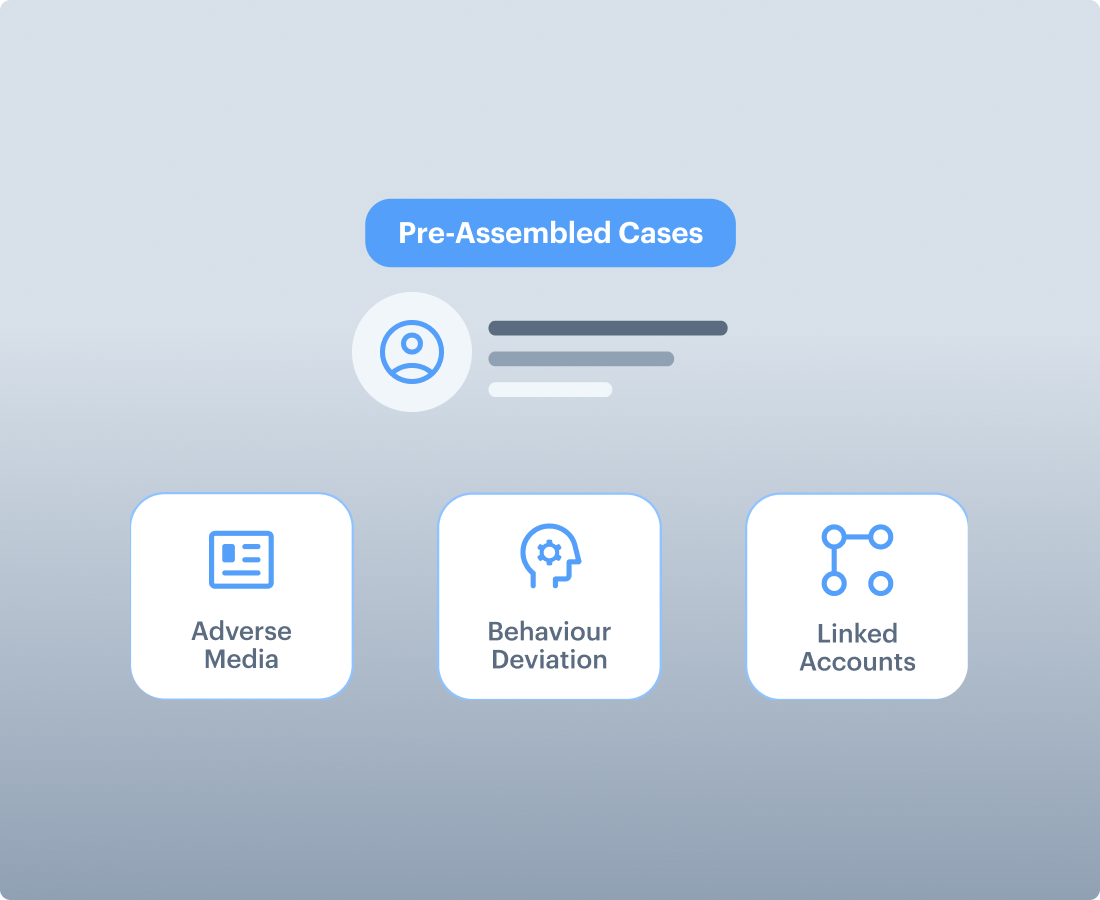

Multiple Agents Delivering One Decision Ready Case

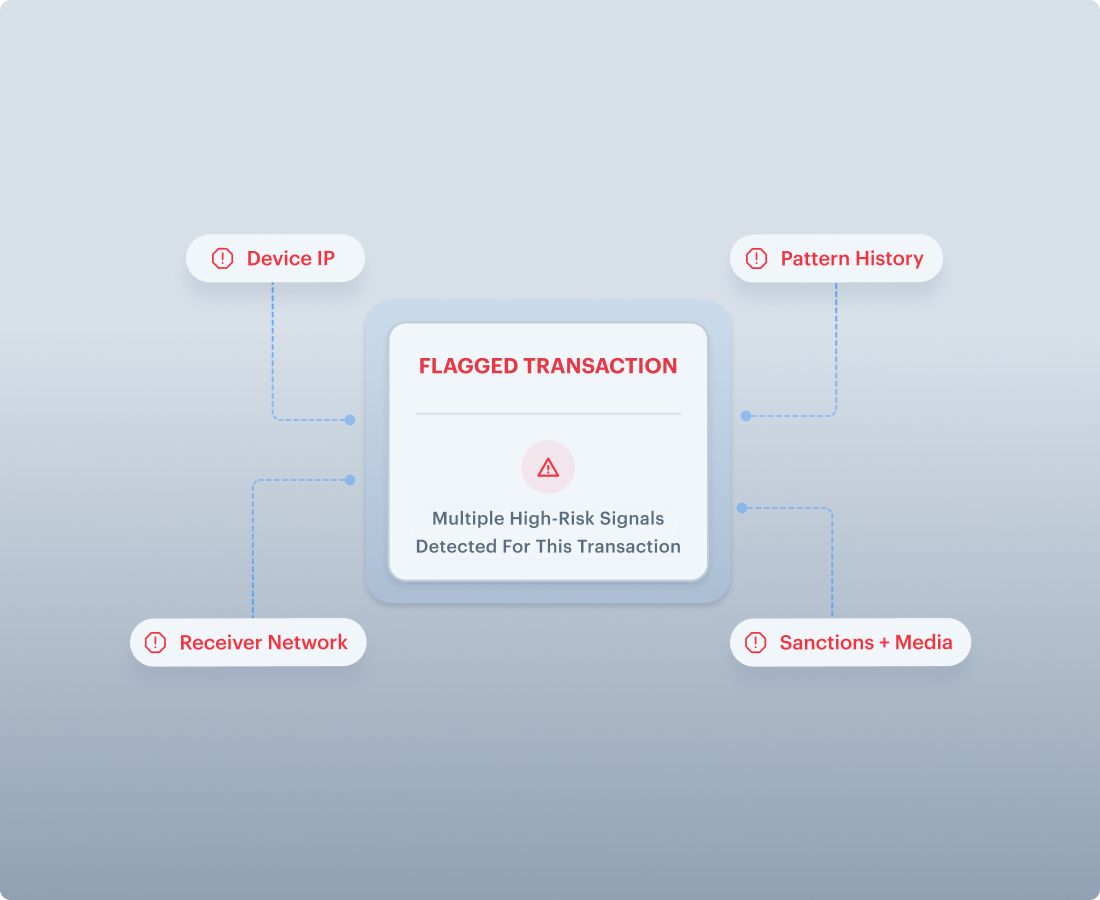

Parallel Agent Investigation

Checks pattern history, screening context, device and IP location, receiver networks and prior cases at the same time.

Pre-Assembled Cases

Delivers adverse media, linked accounts, behavioural deviation, rule trigger and score explanation in one view.

Smarter Alert Triage

Prioritises signals with new risk while logged repeat patterns stay out of unnecessary MLRO review.

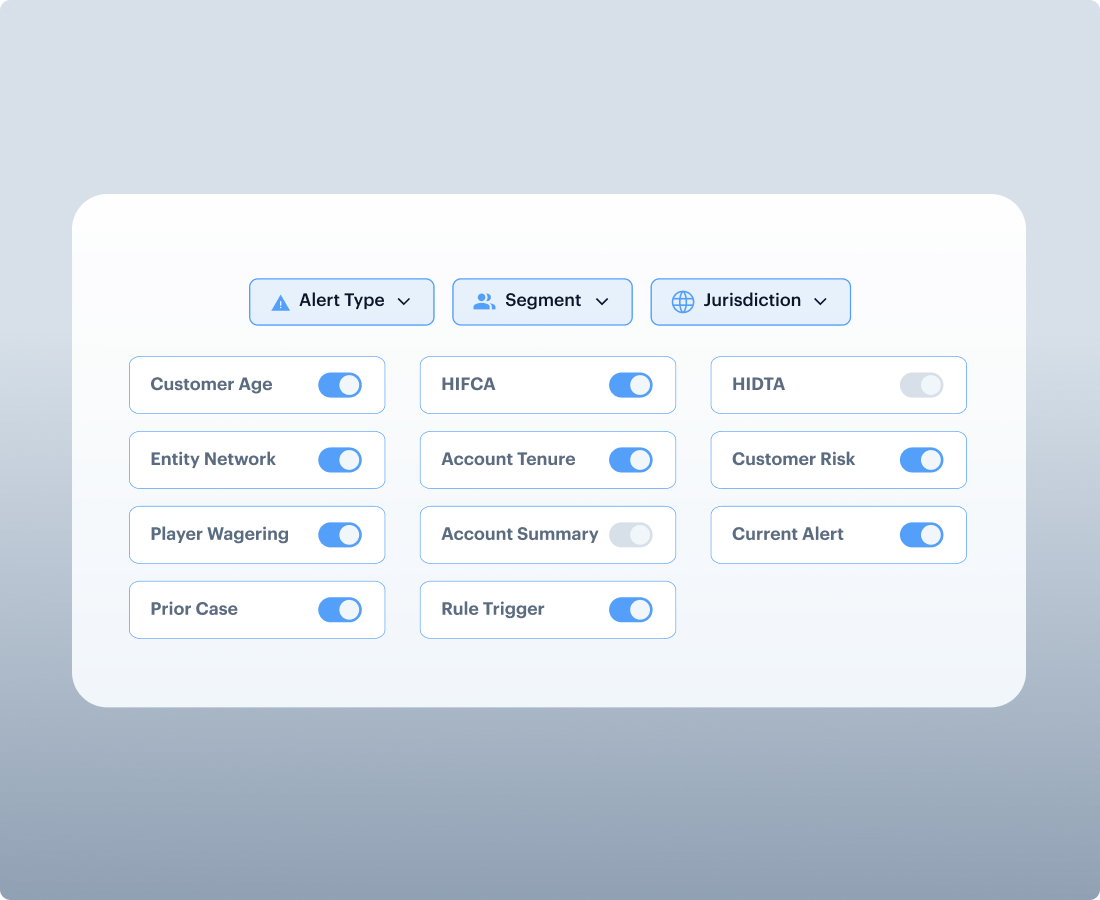

Configurable Agent Library

Toggle investigation agents by alert type, customer segment, jurisdiction or risk policy.

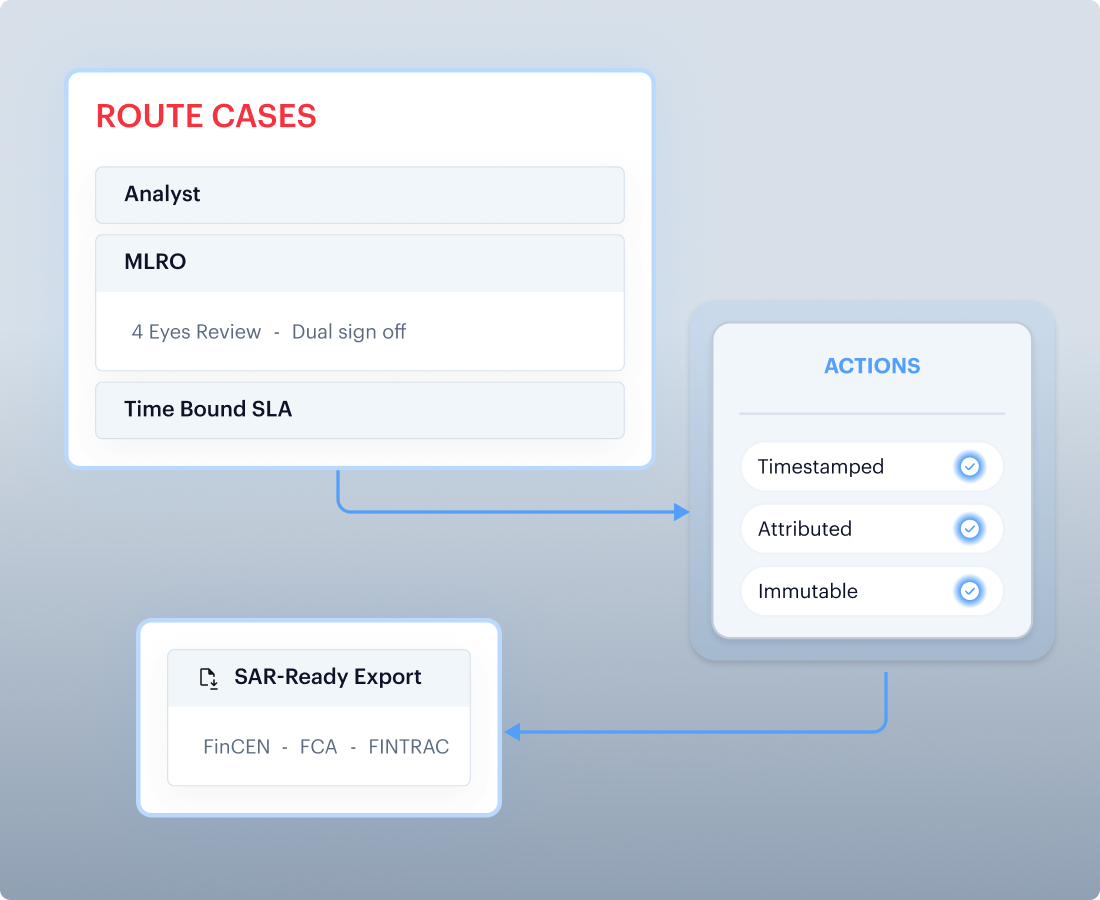

AML Case Management & Escalation Hub

Unified Alert Queue

Route flagged transactions by risk score, typology, jurisdiction, customer tier or field completeness.

Escalation Workflow and Audit Trail

Support L1, L2, MLRO escalation, four-eyes review, SLA tracking, action history and closure rationale.

Structuring, Smurfing, and Mule Detection

Surface transactions broken below thresholds, coordinated smurfing and mule behaviour inconsistent with verified identity.

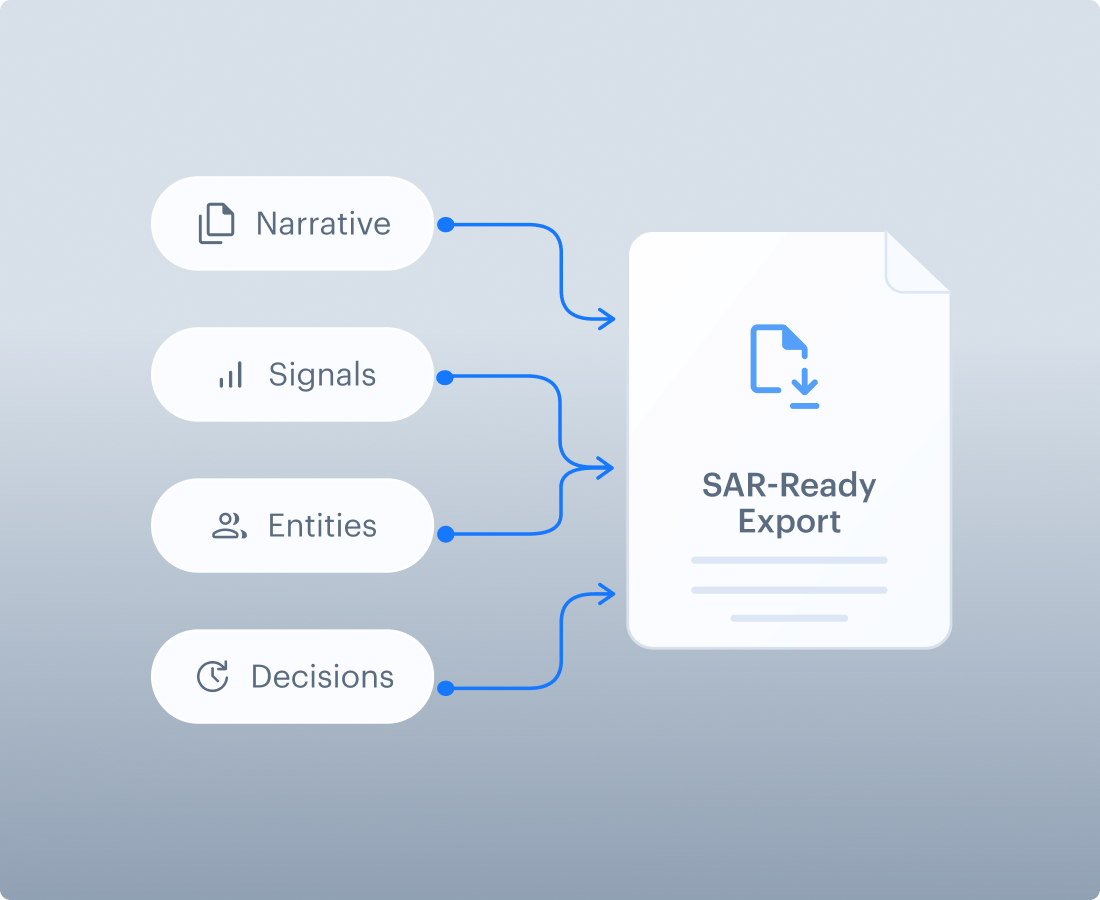

SAR-Ready Documentation

Export case files with narrative, supporting signals, linked entities, decision history and analyst notes.

REGULATORY COVERAGE

Reporting Coverage For Regulated Transaction Monitoring Teams

GoAML-Ready Reporting Workflows

goAML support is critical for markets such as UAE, Pakistan and India where FIU reporting expectations are strict and operational teams need structured case data, party details, transaction history, narrative fields and attachments ready for submission workflows.

SAR, STR, and CTR Report Packs

Generate report-ready case bundles with subject details, transaction chronology, triggered typologies, connected parties, analyst rationale, supporting documents and decision history for suspicious activity and threshold reporting workflows.

Supported Frameworks and Market Alignment

Configure reporting operations around jurisdiction-specific evidence expectations, including FIU-led frameworks, FinCEN-style suspicious activity workflows, NFIU requirements, CBI reporting needs and local compliance policies.

Identity Assurance Behind Every Report

Reports can carry verified identity, KYC status, screening outcome, beneficiary details and liveness-backed onboarding context, supported by Shufti trust credentials such as iBeta Level 3 PAD and SOC 2 Type II.

Machine-Readable Exports and Evidence Packages

Package transaction logs, party data, linked entities, attachments, analyst notes, rule metadata, score explanations and timestamps into exportable formats for internal audit, regulator requests and downstream compliance systems.

Retention, Access, and Governance Controls

Maintain review-ready records with attributed actions, role-based access, versioned configuration, deployment controls and retention policies that help compliance, security and procurement teams defend how monitoring decisions were made.

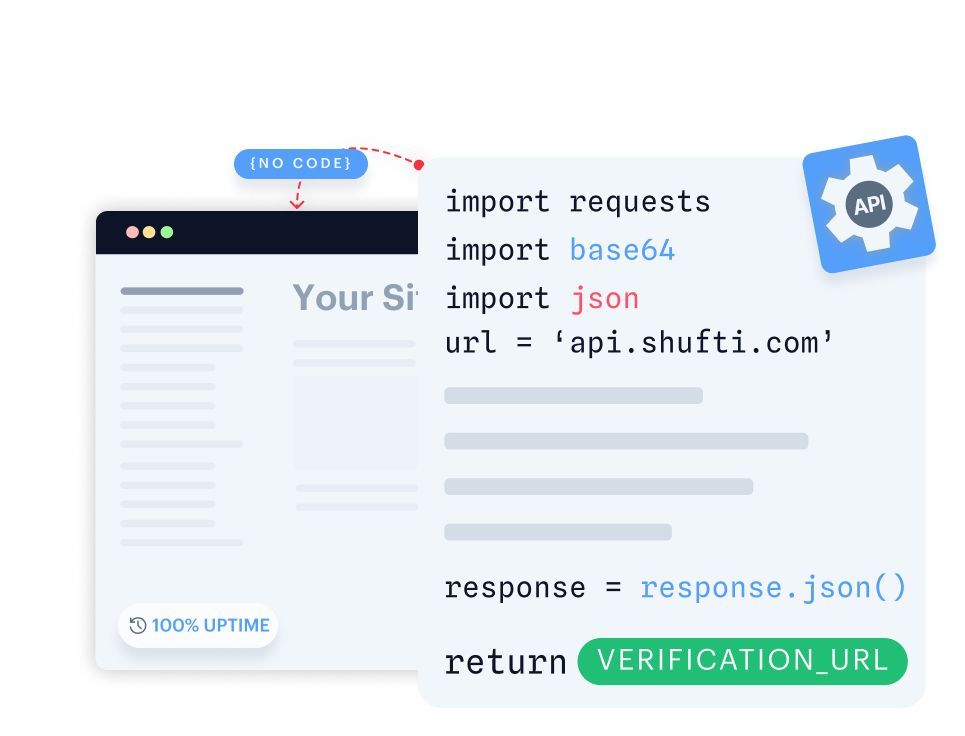

Single API, Seamless Integration

Build fully customisable verification flows with seamless backend integration.

- Gain full control by customising verification flows end-to-end.

- Integrate seamlessly with your backend for quick implementation.

- Design flexible verification journeys tailored to your users.

Launch a native verification experience in your mobile app within minutes.

- Launch native verification within minutes on iOS or Android.

- Use ready-made UI with camera, capture, and real-time feedback.

- Customise flows to fit seamlessly into your mobile app.

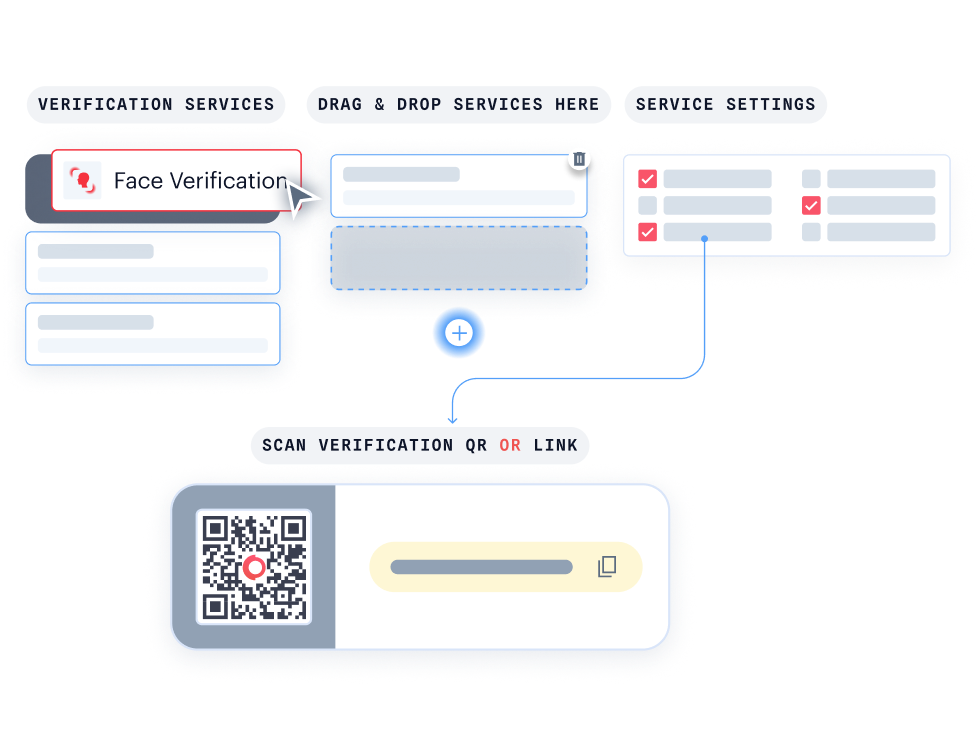

With KYC Journey Builder, create personalised verification journeys without writing a single line of code.

- Customise your journey effortlessly with drag-and-drop functionality.

- Instantly see how your verification flow looks for your users.

- Easily connect with Hosted Verification for a consistent, branded experience.

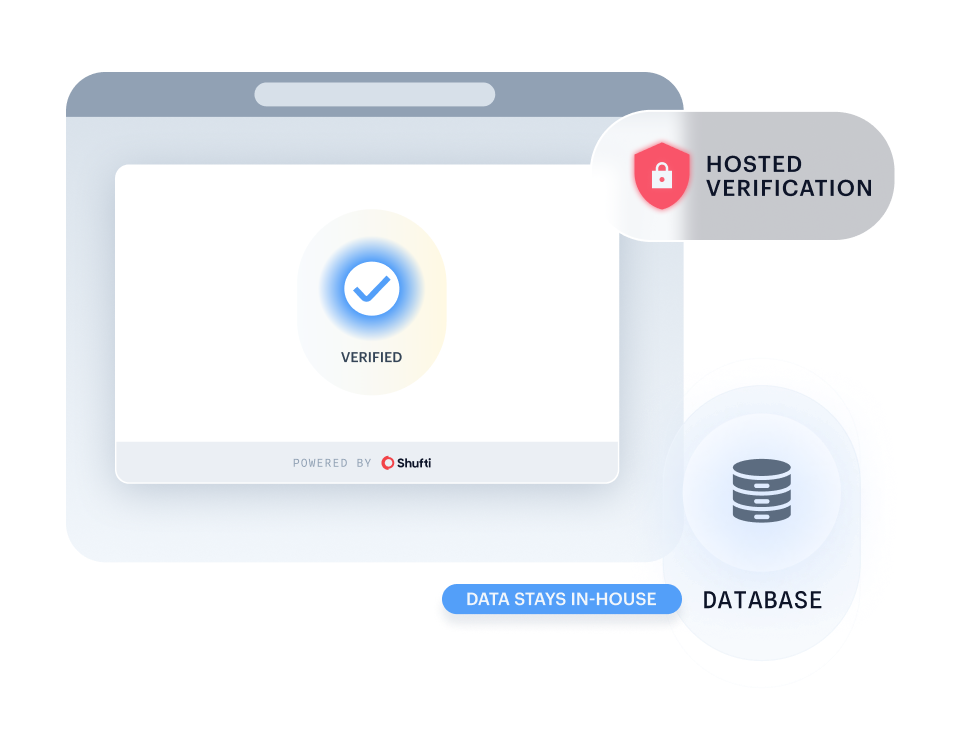

Run Shufti within your own identical-capability infrastructure for maximum data control and privacy.

- Keep all sensitive information in-house to meet strict governance and data residency requirements.

- Keep sensitive information fully private and secure in-house.

- Deploy in highly regulated sectors without compromising compliance.

EVIDENCE-BASED AML MONITORING FOR EVERY REGULATED BUSINESS

Real-world scenarios where TTM monitors for AML risk

Onboarding Context in Every Case

Fast onboarding invites synthetic identities and account takeover. Cases read from the verified identity and the live risk score, so new accounts are treated as unproven until a baseline forms.

Don’t just take our word for it, hear from our customers

The Confidence Our Clients Share

The future of digital identity is defined by trust, interoperability, and regulatory alignment, so our partnership with Shufti reinforces DevCode Identity’s commitment to supporting our global customers with the most secure, best-in-class, compliant identity verification solutions available today.

Combining our Conversion Driven Compliance Orchestration Platform with Shufti’s global KYC and IDV capabilities allows our customers not only to navigate complex regulatory demands but also to maintain a seamless customer onboarding experience with the highest achievable conversion rates.

We’re proud to continue our partnership with Shufti as we expand into new jurisdictions.

Shufti’s verification technology not only strengthens our compliance framework but also ensures our players enjoy a smooth, secure onboarding experience.

We ain to offer our clients and their traders the very best tools with which to do their jobs, we’re excited to be able to work with Shufti.

They’re a leading company, and we’re looking forward to offering their solutions to our clients through our CRM.

The relationship with Shufti was born out of frustration with an existing provider, so we started our discussion with Shufti.

The reponse time was excellent, from the start of speaking to sales to getting up and running with the demo.

Everything you need to know in one place

Frequently Asked Questions

What is transaction monitoring software?

Transaction monitoring software reviews deposits, withdrawals, transfers, payouts, refunds and other money movements to detect suspicious activity, fraud indicators, policy violations and AML risk after onboarding.

How is AML transaction monitoring different from AML screening?

AML screening checks people and entities against sanctions, PEP, RCA and adverse media sources. AML transaction monitoring evaluates ongoing behaviour and transaction patterns after onboarding, such as velocity, structuring, corridor risk, beneficiary changes and deviations from a customer's own baseline.

How does Shufti unify fraud and AML monitoring?

Shufti brings fraud and AML signals into one FRAML composite risk score, so analysts can see how account takeover, mule activity, sanctions exposure, structuring, beneficiary risk and transaction velocity interact in one decision.

Does Shufti support real-time and batch transaction monitoring?

Yes. Shufti can score transactions in real time and support batch review workflows depending on integration, transaction volume and operational model.

Can compliance teams build and test rules without engineering support?

Teams can create rules manually, start from a rules library, or use an AI wizard to draft reviewable logic. Detection windows, filters, thresholds, rule weights and escalation behaviour can be configured in governed workflows and tested against 90-day customer and transaction history before deployment.

What is Not Assessable in transaction monitoring?

Not Assessable means the system cannot complete a check because a required field or data point is missing. Instead of passing the transaction as low risk, Shufti flags the gap so analysts, MLROs and auditors can see what could not be assessed.

How does Shufti move from alert to case?

A flagged transaction can be routed into an AML case with the transaction record, customer profile, beneficiary context, triggered rules, composite risk score, AI analysis report, MLRO summary, audit trail and analyst actions attached.

Does Shufti support SAR, STR, CTR and goAML reporting?

Shufti structures case evidence into SAR, STR, CTR, FIU and goAML-ready report packs for supported jurisdictions and frameworks, including workflows relevant to UAE, Pakistan, India, FinCEN, NFIU and CBI implementation needs.

How long does API integration take?

API integration typically takes 2 to 5 business days. SDK integration takes 1 to 3 business days. Sandbox access is provisioned within 24 hours. These timelines reflect actual enterprise deployment experience, not estimates. A dedicated integration support team is available throughout the process.

How does Shufti reduce false positives without hiding risk?

Shufti correlates customer identity, historical behaviour, screening context, rule triggers, suppression conditions, field completeness and escalation logic before review. Recurring low-risk patterns can be suppressed under governed conditions, while hard-risk events and every suppressed decision remain auditable.

Which industries does Shufti's transaction monitoring solution support?

Shufti supports regulated businesses including remittance and money transfer operators, PSPs, fintechs, neobanks, crypto exchanges and VASPs, iGaming operators, marketplaces, forex platforms and banking teams monitoring deposits, withdrawals, transfers and payouts.

What deployment options are available?

Shufti supports SaaS, private cloud and on-premise deployment options for organisations with strict security, procurement or data residency requirements.

Evaluate The Transaction Monitoring Solution Built For Defensible Decisions

Bring verified identity, AML screening, fraud signals, configurable monitoring logic, case management and regulatory reporting into one governed decision trail. Shufti helps teams prioritise genuine risk, reduce review noise, and explain every transaction decision with confidence.