Face Verification

Face Verification

Address Verification

Address Verification

Document Verification

Document Verification

Age Verification

Age Verification

VideoIdent

VideoIdent

Fast ID

Fast ID

Docless Verification

Docless Verification

Consent Verification

Consent Verification

NFC Verification

NFC Verification

Business Verification

Business Verification

Due Diligence

Due Diligence

Investor Verification

Investor Verification

E-Signature

E-Signature

QES

QES

AML Screening

AML Screening

Transaction Monitoring

Transaction Monitoring

Adverse Media

Adverse Media

Business AML Screening

Business AML Screening

PEP & RCA

PEP & RCA

Sanctions

Sanctions

Watchlist

Watchlist

Behavioural Biometrics

Behavioural Biometrics

Device Fingerprinting

Device Fingerprinting

Biometric Face Authentication

Biometric Face Authentication

MFA

MFA

Fraud Hub

Fraud Hub

Onboarding

Onboarding

Ongoing Monitoring

Ongoing Monitoring

KYC

KYC

KYB

KYB

KYI

KYI

Age Assurance

Age Assurance

Identity Verification

Identity Verification

Workforce IAM

Workforce IAM

Candidate Verification

Candidate Verification

Compliance

Compliance

Fraud prevention

Fraud prevention

Trust & safety

Trust & safety

Global expansion

Global expansion

Product Managers

Product Managers

Compliance Officers

Compliance Officers

Fraud Analysts

Fraud Analysts

Developers

Developers

Deepfake

Deepfake

Bonus Abuse / Promotion Abuse

Bonus Abuse / Promotion Abuse

Account Takeover

Account Takeover

Synthetic Identity Fraud

Synthetic Identity Fraud

Document Fraud

Document Fraud

Impersonation Fraud

Impersonation Fraud

Multi-Accounting

Multi-Accounting

Fraud Networks

Fraud Networks

Chargeback Fraud

Chargeback Fraud

Money Mule Activity

Money Mule Activity

Party Fraud

Party Fraud

Regulatory & Compliance Risks

Regulatory & Compliance Risks

Fintech

Fintech

Crypto

Crypto

iGaming

iGaming

Forex

Forex

Social Network

Social Network

Marketplace

Marketplace

Banking

Banking

Gig Economy

Gig Economy

Payments

Payments

Ride Hailing

Ride Hailing

Adult Content

Adult Content

Blind Spot Audit

Blind Spot Audit

Deepfake Detector

Deepfake Detector

Liveness Spoofs

Liveness Spoofs

Document Originality

Document Originality

Document Deepfake

Document Deepfake

Global Trust Platform

Global Trust Platform

Journey Builder

Journey Builder

Case Management

Case Management

Shufti AI

Shufti AI

Fraud Analytics

Fraud Analytics

Vendor Comparison

Vendor Comparison

Brand Personalisation

Brand Personalisation

IDV Modes

IDV Modes

AI Compliance Co-Pilot

AI Compliance Co-Pilot

OCR

OCR

Secure Capture

Secure Capture

Deployment Options

Deployment Options

Identity Methods

Identity Methods

API Documentation

API Documentation

Mobile SDKs

Mobile SDKs

Service Status

Service Status

Help Center

Help Center

Contact Us

Contact Us

Technical Support

Technical Support

Supported Documents

Supported Documents

Supported Countries

Supported Countries

Content library

Content library

Blogs

Blogs

News

News

Reports

Reports

Insights

Insights

Knowledgebase

Knowledgebase

ROI calculator

ROI calculator

About

About

Career

Career

Press Release

Press Release

Certifications

Certifications

Partnership

Partnership

Awards

Awards

Events & Webinar

Events & Webinar

Interactive Demo

Interactive Demo

Podcast Studio

Podcast Studio

Spotlight Studio

Spotlight Studio

How Your Identity Verification Vendor is Costing You Customers You Don’t Know You’ve Lost

- 01 TL;DR

- 02 What is the KYC conversion rate, and why is everyone measuring it now?

- 03 Where does the drop actually happen and who owns it?

- 04 Why is KYC conversion rate now a compliance metric?

- 05 What fragmented IDV stacks do to your conversion numbers?

- 06 How does Shufti fit in the conversion conversation?

TL;DR

- 60% of users abandon digital bank account applications before completing identity verification.

- The drop-off usually happens inside the vendor’s model, not your UX design.

- FATF’s 2025 guidance explicitly frames excessive onboarding friction as a financial exclusion risk.

- KYC conversion rate is now both a growth metric and a regulatory one.

- Fixing the form doesn’t fix the vendor.

Your onboarding funnel looks healthy. Acquisition is solid, the landing page converts, and the form is clean. But somewhere between “submit your ID” and “you’re verified,” a meaningful share of your applicants stop. They don’t file a complaint. They do not call for support. They close the tab and go somewhere else or nowhere at all.

The cost never shows up as a line item. It shows up as customers you never acquired.

That’s the identity verification conversion problem. And for most businesses, the instinctive response is redesigning the form, reducing the steps, and adding a progress bar which still does not move the number because the problem isn’t in the form. It lies in the vendor behind it.

Regulators are now converging on the same conclusion from a different direction. When a verification flow rejects too many legitimate users, it doesn’t just hurt your conversion rate. It creates an exclusion pattern that financial regulators flag as a compliance risk under the proportionality obligations of a risk-based approach. The Financial Action Task Force (FATF) made this explicit in its 2025 guidance on Anti-Money Laundering and Financial Inclusion.

This article unpacks what KYC conversion rate actually measures, where the drop-off originates in the vendor stack, and why your compliance function now has a stake in the same metric your product team watches.

What is the KYC conversion rate, and why is everyone measuring it now?

KYC conversion rate is the percentage of users who complete identity verification without abandoning or failing on their first attempt. It sounds like a product metric, and it is. But it also measures something deeper: how well your verification infrastructure handles the range of real users it encounters in production.

The metric most vendors don’t show you

Most identity verification vendors report a “pass rate” the share of completed verification sessions that return a successful result. That number presents well in a pitch. What it doesn’t reveal is how many users tried and gave up before a session was counted, how many cycled through two or three retries before passing, and how many abandoned after a document rejection with no path forward.

Pass rate and identity verification conversion rate are not the same metric. A vendor can report a 94% pass rate on completed sessions while losing a third of your users before those sessions ever finish. The conversion number of users who initiated verification divided by users who completed it successfully on the first attempt is what maps to your actual revenue.

How does a 60% pass rate differ from a 60% conversion rate?

A 60% pass rate means four in ten completed sessions ended in rejection. A 60% conversion rate means four in ten people who started the process never became customers. The second figure is the one that belongs in your board pack next to acquisition cost and lifetime value.

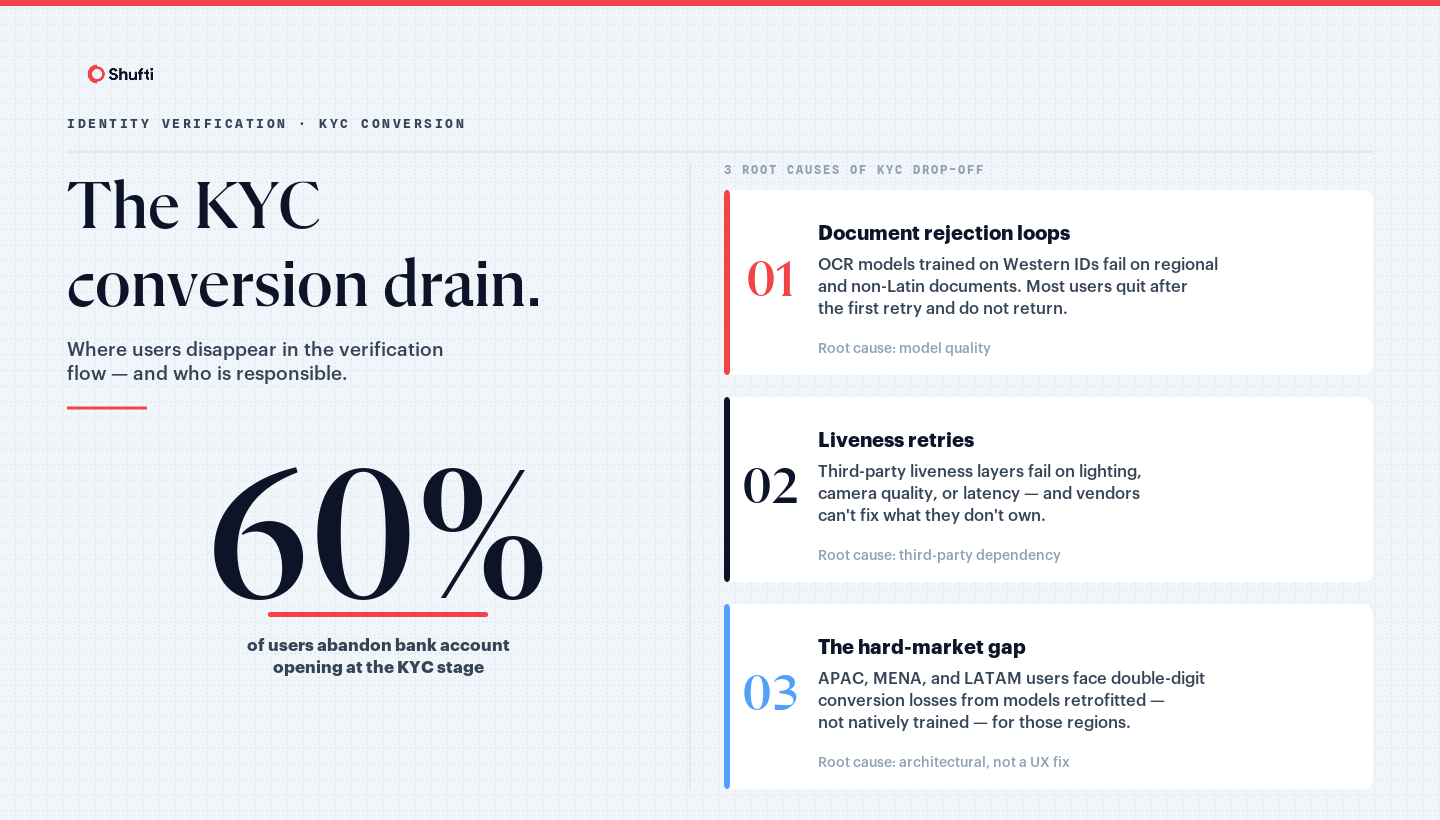

Markswebb’s research on digital banking UX found that 60% of users abandon the process of opening a digital bank account before completing the KYC stage. That figure is not a form-design failure. It is a vendor infrastructure failure and for most businesses, it remains invisible until someone maps the funnel end-to-end.

Where does the drop actually happen and who owns it?

The default response to high abandonment is a UX audit. Simplify the instructions. Reduce fields. These interventions can move the margin. They cannot fix the underlying cause, because the majority of KYC abandonment happens inside the verification engine during document processing and biometric checks, not at the form layer that sits above it.

Document rejection loops

The most common trigger for abandonment is a document rejection that has nothing to do with fraud. The document is genuine. The user is legitimate. The verification engine simply cannot read it with sufficient confidence and returns a failure.

This is a model quality problem. When a Thai national ID, a Brazilian CPF card, or a Gulf-issued residence permit comes back flagged as “unreadable” or “low confidence,” the flow asks the user to retry. Some do while most don’t. Each additional retry sharply reduces completion probability. By the third retry, the user isn’t experiencing a technical glitch; they are experiencing a system that appears to have decided they don’t qualify.

The structural cause is consistent across most vendors: document recognition was built on Western identity documents and retrofitted for everything else. The OCR accuracy on non-Latin scripts, dual-language documents, and newer regional ID formats reflects that retrofitted history in every session that touches them.

Liveness retries

Liveness detection is the second major failure point. A liveness check that asks a user to blink, turn their head, or hold a pose introduces abandonment the moment it fails for reasons outside the user’s control: ambient lighting, mobile camera compression, background movement, or connection latency triggering a session timeout.

When the liveness layer is sourced from a third-party provider sitting inside the vendor’s managed flow, the vendor cannot improve it on their own timeline. Failure modes that are reproducible and documented can persist for weeks while the subprocessor prioritises a fix. During that window, every affected user session is a lost conversion.

The hard-market gap

For businesses with users in Vietnam, Indonesia, Brazil, South Asia, or the Gulf, the abandonment rate runs measurably higher than the global average often without a clear explanation appearing in vendor reporting.

The reason is consistent: models trained primarily on Western documents perform worse on regional document types. In these markets, the conversion gap between a vendor with native training data and one that retrofitted coverage can reach double digits in completion rate. That gap is not a temporary calibration issue. It is an architectural one, baked in at the training stage, and it cannot be closed by improving the form.

For businesses targeting these markets, identity verification conversion becomes a strategic variable. A vendor that cannot convert your APAC or MENA users is not costing you individual sessions. It is costing you entire addressable markets.

Why is KYC conversion rate now a compliance metric?

Your product team has owned conversion rate since your first onboarding funnel. Your compliance team has owned KYC pass rate since your first regulatory audit. These two metrics have historically lived in different dashboards, reported to different people, with different consequences when they move.

That separation is ending.

In 2025, FATF published updated guidance on the relationship between Anti-Money Laundering controls and Financial Inclusion. The guidance does something compliance teams need to take seriously: it explicitly identifies over-exclusion, rejecting or discouraging legitimate customers through disproportionately burdensome verification as a failure of the risk-based approach, not merely a UX shortcoming. A proportionate approach means calibrating verification controls so they do not systematically exclude customers who pose no material risk. FATF’s 2025 guidance on AML and Financial Inclusion names this proportionality obligation directly.

The compliance implication follows clearly. If your identity verification flow consistently rejects a statistically significant share of legitimate users from a specific geography, demographic, or document type even if no individual rejection is wrong on its face the aggregate pattern constitutes disproportionate exclusion. Your MLRO now has a stake in your conversion rate, broken down by region and document type, not just in your fraud rate.

|

Lens |

What a low KYC conversion rate signals |

Who owns the consequence |

|

Business |

Lost customers, lost revenue, damaged brand trust |

Product, Growth |

|

Compliance |

Disproportionate exclusion, breach of proportionality under risk-based approach |

MLRO, Compliance |

|

Vendor accountability |

Model quality failure, not surfaced in pass-rate reporting |

Technology, Procurement |

Vendors who present a pass rate without a conversion breakdown are giving you incomplete information for a decision that now carries compliance dimensions. Procurement conversations that used to live entirely in the product team now belong in the compliance function too.

What fragmented IDV stacks do to your conversion numbers?

The conversion problem has a structural cause most businesses don’t see when evaluating a vendor. Most identity verification platforms are not built end-to-end. They are assembled from third-party components OCR from one supplier, liveness from another, AML screening from a third connected by orchestration logic that no single party fully owns.

That architecture creates a failure surface at every handoff.

No single owner means multiple points of failure

When a user’s liveness check clears one layer but the document is processed by a separate system with different confidence thresholds, the result can be an inconsistent outcome that no single vendor can debug end-to-end. There is no single point of accountability. The vendor managing the overall flow depends on a subprocessor’s response time to investigate and fix any recurring failure mode.

This is why assembled stacks tend to produce worse conversion rates in aggregate than fully owned ones even when each individual component reports a healthy pass rate in isolation. The gaps between components are where users fall, and where accountability disappears.

Why do hard markets expose stitched-together stacks fastest?

The hard-market stress test is the clearest diagnostic. A vendor that sources its OCR from a supplier trained predominantly on Western documents will produce higher rejection rates in APAC and MENA. Because the OCR layer is external, improving it requires the subprocessor to act, not the vendor you contracted. The update timeline runs on someone else’s roadmap.

For businesses expanding into Vietnam, Indonesia, Brazil, South Asia, or the Gulf, this is the explanation for why conversion rates in those markets lag the global average and why the vendor’s published accuracy figures, measured on test sets that over-represent Western documents, do not predict what happens in production at scale.

How does Shufti fit in the conversion conversation?

If your conversion rate underperforms in APAC, MENA, or LATAM or if your vendor reports a healthy pass rate but cannot show you a conversion breakdown by region and document type the cause is usually structural. Most vendors were not built to own the full decision.

Shufti built and owns its entire verification stack: OCR, liveness detection, document intelligence, and AML screening, with no third-party components on the critical path. Shufti’s document models were trained natively on 10,000+ document types across 240+ countries from the start, not retrofitted which is why clients in Vietnam, Indonesia, Brazil, South Asia, and the Gulf see higher pass rates than they achieved with previous vendors. Binance uses Shufti specifically for non-Latin document accuracy in global markets where other stacks underperform.

One platform. Fully owned technology. Global coverage with real local depth.

|

See how Shufti’s identity verification performs on your actual document mix book a demo. |

Frequently Asked Questions

What is a good KYC conversion rate?

A first-attempt completion rate below 70% typically signals a vendor or model quality issue rather than a UX problem. Businesses in APAC and MENA often see lower rates because of document type coverage gaps, an issue that traces to the vendor's training data, not the flow design. Best-in-class flows on well-supported document types can reach 85–90% first-attempt completion.

Is KYC drop-off a UX problem or a vendor problem?

Both contribute, but the majority of abandonment happens inside the verification engine during document processing or liveness checks, not at the form level. Redesigning the UI improves margins. Replacing an underperforming vendor changes the underlying rate. If your UX has been optimised and drop-off persists, the vendor model is the most likely culprit.

How does FATF's financial inclusion guidance affect onboarding design?

FATF's 2025 guidance on AML and Financial Inclusion asks regulated firms to apply a proportionate, risk-based approach that avoids systematically excluding legitimate customers through overly burdensome verification. A persistent pattern of high rejection rates for specific geographies or document types can constitute disproportionate exclusion under this framework, making KYC conversion rate a compliance concern alongside a product one.

What causes high false-rejection rates in identity verification?

False rejections are most commonly caused by three factors: document recognition models trained on insufficient document diversity (failing on regional or non-Latin IDs), liveness detection sensitive to environmental variables (lighting, camera quality, connection speed), and verification flows where components from different vendors process the same session independently. Each adds a failure surface. The aggregate effect is a conversion rate that performs well in a controlled test environment but underperforms in production at scale.