Face Verification

Face Verification

Address Verification

Address Verification

Document Verification

Document Verification

Age Verification

Age Verification

VideoIdent

VideoIdent

Fast ID

Fast ID

Docless Verification

Docless Verification

Consent Verification

Consent Verification

NFC Verification

NFC Verification

Business Verification

Business Verification

Due Diligence

Due Diligence

Investor Verification

Investor Verification

E-Signature

E-Signature

QES

QES

AML Screening

AML Screening

Transaction Monitoring

Transaction Monitoring

Adverse Media

Adverse Media

Business AML Screening

Business AML Screening

PEP & RCA

PEP & RCA

Sanctions

Sanctions

Watchlist

Watchlist

Behavioural Biometrics

Behavioural Biometrics

Device Fingerprinting

Device Fingerprinting

Biometric Face Authentication

Biometric Face Authentication

MFA

MFA

Fraud Hub

Fraud Hub

Onboarding

Onboarding

Ongoing Monitoring

Ongoing Monitoring

KYC

KYC

KYB

KYB

KYI

KYI

Age Assurance

Age Assurance

Identity Verification

Identity Verification

Workforce IAM

Workforce IAM

Candidate Verification

Candidate Verification

Compliance

Compliance

Fraud prevention

Fraud prevention

Trust & safety

Trust & safety

Global expansion

Global expansion

Product Managers

Product Managers

Compliance Officers

Compliance Officers

Fraud Analysts

Fraud Analysts

Developers

Developers

Deepfake Detection

Deepfake Detection

Bonus Abuse / Promotion Abuse

Bonus Abuse / Promotion Abuse

Account Takeover

Account Takeover

Synthetic Identity Fraud

Synthetic Identity Fraud

Document Fraud

Document Fraud

Impersonation Fraud

Impersonation Fraud

Multi-Accounting

Multi-Accounting

Fraud Networks

Fraud Networks

Chargeback Fraud

Chargeback Fraud

Money Mule Activity

Money Mule Activity

Party Fraud

Party Fraud

Regulatory & Compliance Risks

Regulatory & Compliance Risks

Fintech

Fintech

Crypto

Crypto

iGaming

iGaming

Forex

Forex

Social Network

Social Network

Marketplace

Marketplace

Banking

Banking

Gig Economy

Gig Economy

Payments

Payments

Ride Hailing

Ride Hailing

Adult Content

Adult Content

Blind Spot Audit

Blind Spot Audit

Deepfake Detector

Deepfake Detector

Liveness Spoofs

Liveness Spoofs

Document Originality

Document Originality

Document Deepfake

Document Deepfake

Global Trust Platform

Global Trust Platform

Journey Builder

Journey Builder

Case Management

Case Management

Shufti AI

Shufti AI

Fraud Analytics

Fraud Analytics

Vendor Comparison

Vendor Comparison

Brand Personalisation

Brand Personalisation

AI Compliance Co-Pilot

AI Compliance Co-Pilot

OCR

OCR

Secure Capture

Secure Capture

Deployment Options

Deployment Options

Identity Methods

Identity Methods

API Documentation

API Documentation

Mobile SDKs

Mobile SDKs

Service Status

Service Status

Help Center

Help Center

Contact Us

Contact Us

Technical Support

Technical Support

Supported Documents

Supported Documents

Supported Countries

Supported Countries

Content library

Content library

Blogs

Blogs

News

News

Reports

Reports

Insights

Insights

Knowledgebase

Knowledgebase

ROI calculator

ROI calculator

About

About

Career

Career

Press Release

Press Release

Certifications

Certifications

Partnership

Partnership

Awards

Awards

Events & Webinar

Events & Webinar

Interactive Demo

Interactive Demo

Podcast Studio

Podcast Studio

Spotlight Studio

Spotlight Studio

The Markets Your KYC Vendor Hopes You Never Expand Into

TL;DR

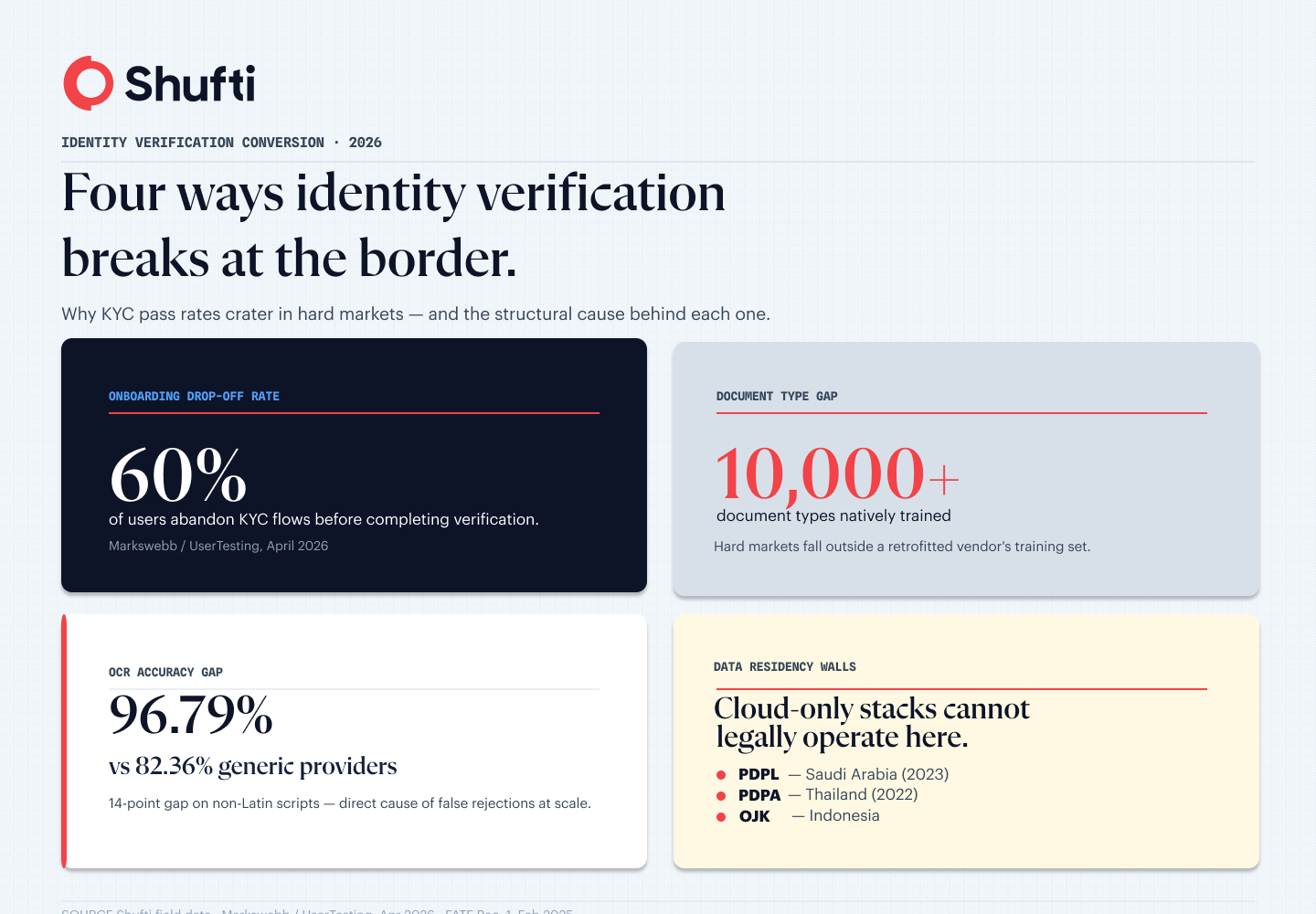

- Up to 60% of users abandon KYC flows before completing identity verification.

- In hard markets, document type gaps and OCR failures push that number even higher.

- Vendors built on Western ID types retrofit non-Latin scripts the difference shows at the border.

- Data residency laws in Saudi Arabia, Thailand, and Indonesia block cloud-only stacks entirely.

- Your KYC conversion rate in APAC or the Gulf reflects your vendor’s training data, not your product.

Your Southeast Asia launch is ready. Licences filed. Marketing live. The product team spent six months localising the UI. Then the first onboarding numbers come in from Jakarta and Ho Chi Minh City, and the drop-off rate is nearly double what you saw in Germany. Support tickets climb. The vendor says it’s a “user education issue.”

It isn’t. It’s a training-data problem that your vendor chose not to surface before you signed the contract.

This pattern plays out every time a fintech or financial services company expands into what the industry calls hard markets Vietnam, Indonesia, Brazil, South Asia, the Gulf and discovers that their identity verification conversion rate, which looked healthy in the West, does not survive the crossing. The failure is not random. It is structural, predictable, and almost entirely a function of how your vendor built their stack. Understanding it before you expand is the difference between a successful market entry and six months of quietly bleeding revenue while your team optimises the wrong variables.

What your KYC conversion rate is actually measuring

KYC conversion rate is the share of users who start an identity verification flow and complete it successfully. Most product teams track completion rate. Fewer track pass rate, the share of users whose documents are accepted on the first attempt. The gap between those two metrics is where hard-market failure hides.

Pass rate vs. completion rate: the metric your vendor conflates

A user who retries their document upload three times before giving up registers as a completion attempt, not a pass. A user who hits a “document not recognised” error on a valid Thai national ID and closes the app registers as a drop-off without explanation. Vendors report completion rate because it looks better. What you actually need to watch is first-attempt pass rate, segmented by document type and issuing country.

The two metrics diverge sharply in markets where the vendor’s document library is thin. A vendor with strong coverage for US driver’s licences and EU passports will show you healthy global numbers until you look at the country-level breakdown. Vietnam, Indonesia, and the Gulf will look different. Sometimes dramatically so.

Where conversion breaks down in a typical verification flow

Identity verification conversion drops at three specific moments: document capture, OCR processing, and biometric match. In Western markets, the most common drop-off point is document capture: lighting, angle, blur. In hard markets, the larger failure is OCR processing, where the model encounters a script or document structure it was not trained on and returns a rejection.

Research published by Markswebb in April 2026, citing UserTesting data, found that up to 60% of users abandon digital account opening flows before completing identity verification. The same research notes that requiring document uploads can reduce conversion by 29% compared to flows that do not. In markets where documents are frequently rejected on the first attempt, these effects compound: you add the rejection friction on top of the baseline abandonment rate, and the result lands well below any reasonable pass-rate target.

Why identity verification breaks at the border

Three structural failure modes account for most of the hard-market KYC conversion loss. None of them is inherent to the market. They are vendor architecture choices.

|

Failure mode |

Root cause |

Markets most affected |

|

Document type gap |

Vendor trained on Western IDs; hard markets fall outside the training set |

Indonesia, Vietnam, South Asia |

|

OCR failure on non-Latin scripts |

Latin-first OCR engine with retrofitted non-Latin support |

MENA, Southeast Asia, LATAM |

|

Data residency walls |

Cloud-only architecture cannot legally process biometric data in-country |

Saudi Arabia, Thailand, Indonesia |

The document type gap

Most identity verification vendors built their document intelligence on a foundation of Western government IDs US driver’s licences, UK passports, German Personalausweis and expanded outward from that base. The result is a library that skews heavily toward document types that were easy to acquire training data for.

A vendor covering 3,000 document types will pass most EU and North American users without incident. That same vendor, deployed in Indonesia, faces over 300 distinct regional ID card variants across the archipelago’s provinces, each with different layouts, security features, and field positions. If those variants are not in the training set, the model rejects documents that regulators and the issuing government recognise as entirely valid.

The failure is invisible in demo environments. Vendors test against their training data. The gap only surfaces at scale, in production, in the specific market you just launched into.

OCR failure on non-Latin scripts

Optical character recognition on non-Latin scripts is a training data problem. Arabic, Thai, Vietnamese diacritics, and Cyrillic all require models that were trained on those specific character forms in the context of identity documents, not on generic text corpora lifted from the web.

Vendors who retrofitted non-Latin OCR onto a Latin-first engine produce models with high accuracy on Latin-script documents and degraded accuracy on everything else. The degradation shows up where it hurts most: name fields that transpose characters, date fields that misread calendar formats, and address fields that fail on diacritic-heavy text.

Shufti’s own field data from emerging market deployments illustrates the gap: proprietary OCR trained natively on non-Latin scripts achieves approximately 96.79% accuracy, compared to 82.36% for generic OCR providers on the same document set. That 14-point difference translates directly into false rejections for legitimate users. At high volume, it compounds into millions of lost onboarding sessions, and millions of dollars in customer acquisition spend that produces no customers.

Data residency walls that make cloud-only stacks illegal

The third failure mode does not show up in pass rates at all, because the vendor’s stack never reaches legal production. Several of the fastest-growing markets require by law that personal data and biometric information stay within their borders during processing.

|

Regulation |

Market |

Active Since |

What it requires |

|

Personal Data Protection Law (PDPL) |

Saudi Arabia |

2023 |

Data localisation for personal data processed in-country |

|

Personal Data Protection Act (PDPA) |

Thailand |

2022 |

Data localisation for biometric data |

|

OJK data regulations |

Indonesia |

Ongoing |

Locally compliant infrastructure for regulated financial institutions |

Saudi Arabia’s Personal Data Protection Law (PDPL), active since 2023, requires data localisation for personal data processed within the Kingdom. Thailand’s Personal Data Protection Act (PDPA), enforced since 2022, applies equivalent requirements to biometric data. Indonesia’s OJK financial services regulator mandates that regulated institutions process customer data through locally compliant infrastructure.

A cloud-only vendor with servers in Ireland or Virginia cannot meet these requirements without building new regional infrastructure or partnering with a local operator. Most do not. The practical result: if you launch in Saudi Arabia or Indonesia with a SaaS-only identity verification stack, your legal and compliance team will eventually discover the architecture is non-compliant, and you will be rearchitecting your verification layer mid-launch, at the worst possible time.

What hard-market expansion failure actually costs

The commercial case against a vendor with hard-market gaps is concrete. Every rejected document is a user who either retries with friction or abandons entirely. Every abandoned session is a customer acquisition cost that produces no customer.

At scale, identity method mismatch compounds the loss further. Users in APAC increasingly rely on national digital identity schemes India’s Aadhaar, Singapore’s Singpass, Thailand’s national e-ID rather than physical document capture. Users in the Gulf hold Emirates ID smart cards with NFC chips that can be verified directly, without a document photo. A verification flow that forces these users into a document-upload path designed for US driver’s licences creates unnecessary friction for people who hold faster, more reliable credentials.

The Financial Action Task Force (FATF) amended Recommendation 1 in February 2025 to strengthen digital identity’s role in financial inclusion, explicitly recognising that rigid document-upload flows exclude legitimate users who hold digital credentials rather than physical IDs. Regulators are moving toward digital-first identity methods. Vendors built around legacy document capture are moving in the opposite direction.

The cost is not just measured in KYC conversion rate. It shows up in customer acquisition efficiency, in lifetime value from high-growth markets that are expanding faster than Western books of business, and in the regulatory exposure that comes with a verification infrastructure that cannot legally operate in markets you are already in. Getting the vendor wrong does not just hurt your onboarding metrics. It costs you the market.

How Shufti handles hard-market expansion

If your users are in Vietnam, Indonesia, Brazil, South Asia, or the Gulf, you have probably already felt the gap this article describes. Most vendors built their document verification on Western training data and retrofitted everything else. The gap shows up exactly where it matters at the moment a legitimate customer presents a valid document and gets rejected.

Shufti’s document intelligence was trained on 10,000+ document types across 220+ countries from the start, with proprietary OCR reading 150+ languages natively and no human fallback for low-confidence reads. Deployment runs as cloud, Local Cloud in-region for GCC and SEA data residency, or fully on-premises for organisations subject to PDPL, PDPA, or OJK requirements, all through a single API integration. Stripe uses Shufti specifically for MENA and APAC documents despite running its own verification capability. Binance relies on Shufti for non-Latin document accuracy across global markets where standard solutions fall short.

One platform. Fully owned technology. Global coverage with real local depth.

See how Shufti’s document intelligence performs on your hard-market documents. Book A Demo

Frequently Asked Questions

What is a good KYC conversion rate?

A healthy KYC conversion rate sits above 85% on a first-attempt basis for your primary markets, though benchmarks vary by document type and jurisdiction. The more useful metric is first-attempt pass rate segmented by issuing country: a global average can mask severe drop-off in specific hard markets while still reading well in aggregate.

Why does identity verification fail more often in Southeast Asia and the Gulf?

The primary cause is document type and OCR training data. Most vendors built their models on Western government IDs and retrofitted non-Latin scripts, producing degraded accuracy on Thai, Arabic, Vietnamese, and Indonesian document variants. Secondary causes include identity method mismatch users with digital IDs or NFC-chip credentials being forced into document-upload flows and data residency requirements that block cloud-only infrastructure from operating legally.

What data residency regulations affect identity verification in APAC and MENA?

The main frameworks are Saudi Arabia's Personal Data Protection Law (PDPL, active since 2023), Thailand's Personal Data Protection Act (PDPA, enforced since 2022), and Indonesia's OJK financial services data regulations. Each requires that personal and biometric data processed in-country remain within approved regional infrastructure. Cloud-only identity verification vendors without local or on-premises deployment options cannot legally serve customers in these jurisdictions.

: Meaning, Requirements, and When You Need One")