Face Verification

Face Verification

Address Verification

Address Verification

Document Verification

Document Verification

Age Verification

Age Verification

VideoIdent

VideoIdent

Fast ID

Fast ID

eIDV

eIDV

Consent Verification

Consent Verification

NFC Verification

NFC Verification

Business Verification

Business Verification

Due Diligence

Due Diligence

Investor Verification

Investor Verification

QES

QES

E-Signature

E-Signature

AML Screening

AML Screening

Transaction Monitoring

Transaction Monitoring

PEP & RCA

PEP & RCA

Sanctions

Sanctions

Watchlist

Watchlist

Adverse Media Screening

Adverse Media Screening

Business AML Screening

Business AML Screening

Behavioural Biometrics

Behavioural Biometrics

Device Fingerprinting

Device Fingerprinting

1:1 Authentication

1:1 Authentication

Fraud Hub

Fraud Hub

MFA

MFA

Onboarding

Onboarding

Ongoing Monitoring

Ongoing Monitoring

Age Assurance

Age Assurance

Identity Verification

Identity Verification

KYC

KYC

KYB

KYB

KYI

KYI

Workforce IAM

Workforce IAM

Candidate Verification

Candidate Verification

Compliance

Compliance

Fraud prevention

Fraud prevention

Trust & safety

Trust & safety

Global expansion

Global expansion

Product Managers

Product Managers

Compliance Officers

Compliance Officers

Fraud Analysts

Fraud Analysts

Developers

Developers

Global Trust Platform

Global Trust Platform

Case Management

Case Management

Journey Builder

Journey Builder

Shufti AI

Shufti AI

Fraud Analytics

Fraud Analytics

Vendor Comparison

Vendor Comparison

Brand Personalisation

Brand Personalisation

IDV Modes

IDV Modes

AI Compliance Co-Pilot

AI Compliance Co-Pilot

OCR

OCR

Secure Capture

Secure Capture

Deployment Options

Deployment Options

Identity Methods

Identity Methods

Banking

Banking

Fintech

Fintech

Crypto

Crypto

Gaming

Gaming

Forex

Forex

Social Networks

Social Networks

Marketplace

Marketplace

Gig Economy

Gig Economy

Payments

Payments

Ride Hailing

Ride Hailing

Adult Content

Adult Content

Blind Spot Audit

Blind Spot Audit

Deepfake Detector

Deepfake Detector

Liveness Detection

Liveness Detection

Document Originality

Document Originality

Document Deepfake

Document Deepfake

Deepfake

Deepfake

Account Takeover

Account Takeover

Synthetic Identity Fraud

Synthetic Identity Fraud

Document Fraud

Document Fraud

Impersonation Fraud

Impersonation Fraud

Multi-Accounting

Multi-Accounting

Bonus Abuse / Promotion Abuse

Bonus Abuse / Promotion Abuse

Fraud Networks

Fraud Networks

Chargeback Fraud

Chargeback Fraud

Money Mule Activity

Money Mule Activity

Party Fraud

Party Fraud

Regulatory & Compliance Risks

Regulatory & Compliance Risks

API Documentation

API Documentation

Mobile SDKs

Mobile SDKs

Service Status

Service Status

Help Center

Help Center

Contact Us

Contact Us

Technical Support

Technical Support

Supported Documents

Supported Documents

Content library

Content library

Blogs

Blogs

News

News

Reports

Reports

Insights

Insights

Knowledgebase

Knowledgebase

ROI calculator

ROI calculator

About

About

Career

Career

Press Release

Press Release

Certifications

Certifications

Partnership

Partnership

Awards

Awards

Events & Webinar

Events & Webinar

Interactive Demo

Interactive Demo

Podcast Studio

Podcast Studio

Spotlight Studio

Spotlight Studio

A Basic Guide to Smurfing and the Role of AML in Combating It

- 01 Key Takeaways:

- 02 What is Smurfing?

- 03 How Does Smurfing Work?

- 04 What are the differences between smurfing and structuring?

- 05 What is Smurfing in Banking?

- 06 Examples of smurfing

- 07 What is smurfing in gaming?

- 08 How to detect and prevent smurfing

- 09 How Shufti helps financial institutions stop smurfing

Key Takeaways:

- Smurfing breaks large illicit sums into many small transactions to slip below AML reporting thresholds.

- Unlike structuring, smurfing uses multiple people to distribute and move the funds simultaneously.

- Cuckoo smurfing hijacks legitimate international transfers to insert dirty money undetected.

- In gaming, smurfing means creating fake secondary accounts to exploit platforms or rankings.

- Real-time transaction monitoring and behavioural analytics are the frontline defence against smurfing today.

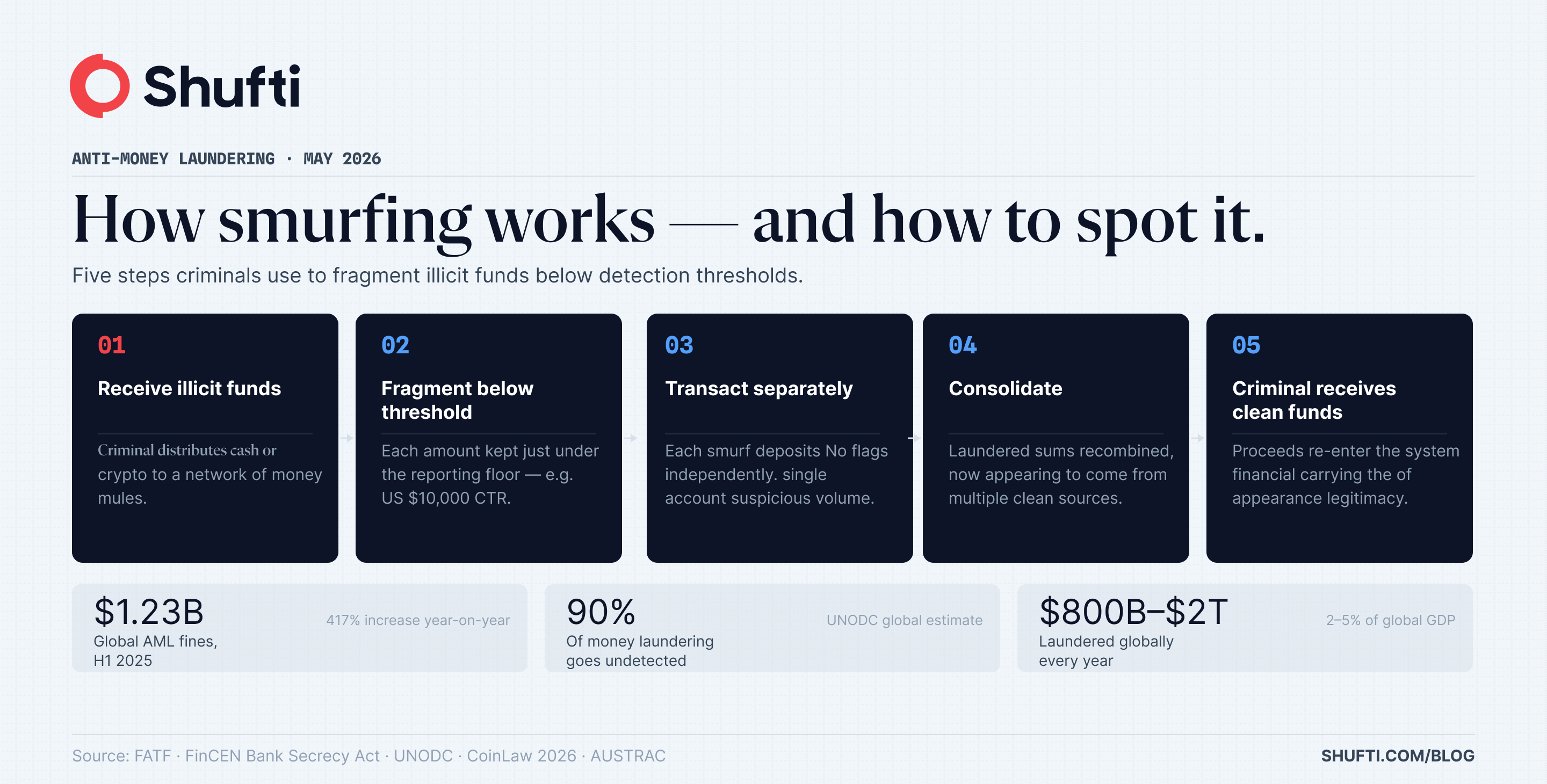

In H1 2025, global AML fines reached $1.23 billion, according to financial crime tracking data. Behind many of those enforcement actions sits a deceptively simple technique: breaking large amounts of illicit money into dozens of smaller transactions, each just below the threshold that would trigger a report. That technique is smurfing, and it remains one of the most common and most misunderstood methods in financial crime.

Not all money laundering involves smurfing, and not all smurfs are career criminals. Some are coerced. Some are simply unaware of what they are facilitating. Understanding what smurfing actually is, how it works, where it shows up, and how it differs from related tactics is the starting point for any compliance team trying to detect and prevent it.

What is Smurfing?

Smurfing meaning: a money laundering technique in which large sums of illicit funds are deliberately broken into multiple smaller transactions, each kept just below a regulatory reporting threshold, and distributed across several individuals or accounts to avoid detection.

The people carrying out these transactions are called “smurfs” a term that entered financial crime terminology in the 1980s and has since become a standard AML typology recognised by the Financial Action Task Force (FATF).

The name itself reflects the tactic. Just as the fictional blue characters operated as a collective of small individuals doing coordinated work, financial smurfs operate in networks each handling a small piece of the total, none of them individually drawing attention.

Smurfing meaning in Financial Crime

In financial crime, smurfing sits at the placement or layering stage of money laundering. In smurfing money laundering, the goal is twofold: keep each individual transaction below reporting thresholds (such as the US $10,000 Currency Transaction Report threshold under the Bank Secrecy Act), and spread the activity across enough accounts and actors to make the pattern hard to spot in any single account’s history.

What separates smurfing from plain structuring is coordination. Structuring is typically done by one person, alone. Smurfing involves a network of individuals, some willing, some recruited, some entirely unaware each handling one slice of the operation.

How Does Smurfing Work?

Step 1: The smurf receives unlawfully acquired funds

A criminal organisation or individual passes illicit cash, crypto, or digital funds to a network of smurfs, also called money mules. Each smurf receives a portion of the total. Some smurfs are willing participants. Others are recruited through romance scams, job offers, or coercion.

Step 2: Funds are divided below detection thresholds

The total sum is fragmented into amounts that fall below the thresholds that trigger automatic reporting. In the US, the trigger is $10,000 for a Currency Transaction Report (CTR). In parts of the EU, the threshold sits at €5,000 for certain transaction types. Smurfs target these floors deliberately; the amounts are set not to maximise efficiency but to minimise the probability of a suspicious activity report (SAR) being filed.

Step 3: Smurfs execute the transactions separately

Each smurf deposits, transfers, or moves their portion independently, treating each smaller amount as a distinct financial event. This fragmentation is what makes smurfing harder to detect than simple structuring: no single account or actor shows a suspicious volume, and the pattern only becomes visible when transactions are aggregated across accounts and actors.

Step 4: Funds are consolidated if necessary

Once laundered through separate channels, the smaller sums can be recombined into a single account now appearing to originate from multiple legitimate-looking sources rather than one large criminal inflow.

Step 5: The criminal receives clean funds

The original criminal receives funds that now carry the appearance of legitimacy, making them easier to spend, invest, or move internationally without triggering further scrutiny.

Modern smurfing has evolved beyond cash deposits. Criminals increasingly spread micro-transactions across digital wallets, prepaid cards, cryptocurrency exchanges, and peer-to-peer payment platforms, each channel adding another layer of distance from the original source.

What are the differences between smurfing and structuring?

Smurfing and structuring are closely related, often confused, and legally distinct. Both involve splitting large sums into smaller transactions. The goal and execution, however, make them different in ways that matter for detection, prosecution, and compliance response.

| Attribute | Smurfing | Structuring |

| Goal | Conceal the origin and nature of illicit funds | Avoid reporting requirements without necessarily hiding the source |

| Who does it | Multiple individuals (smurfs/money mules) acting in coordination | Typically one individual acting alone |

| Legal classification | Money laundering typology under FATF and most national AML laws | A standalone offence under laws such as the US Bank Secrecy Act (31 USC §5324) |

| Detection difficulty | Higher transactions are spread across multiple people and accounts | Lower patterns appear within a single customer’s account history |

| Common channels | Bank deposits, crypto, digital wallets, wire transfers across multiple actors | Cash deposits, ATM withdrawals, money orders at a single institution |

| Regulatory response | SAR + law enforcement referral, often involving network investigation | SAR filing, account restriction, potential prosecution of individual |

The practical consequence for compliance teams: structuring alerts fire at the individual account level; smurfing alerts require cross-account, cross-channel pattern recognition. Static rules catch structuring. Smurfing demands behavioural and network analytics running across your full customer base simultaneously.

What is Smurfing in Banking?

In banking, smurfing surfaces through two primary mechanisms: the use of money mules to execute distributed transactions, and a more sophisticated variant known as cuckoo smurfing. Financial institutions encounter both, and each demands a distinct detection approach.

Money mules and their role in smurfing

Money mules are individuals who allow their personal bank accounts, identities, or payment credentials to be used by criminals for the purpose of moving illicit funds. Some mules are conscious participants paid for their cooperation. Many are recruited unknowingly through fake job postings, social media romance scams, or fraudulent investment schemes and only discover their involvement when law enforcement or their bank contacts them.

In a smurfing network, money mules serve as the operational layer. They open accounts, accept deposits, execute transfers, and withdraw cash each acting on instructions from the criminal coordinator. Because their individual transaction volumes may fall within normal behavioural ranges, they are difficult to distinguish from ordinary customers using standard threshold-based monitoring alone.

What is Cuckoo Smurfing?

Cuckoo smurfing is a specific money laundering technique that exploits legitimate international wire transfer channels to insert illicit funds into the financial system without detection. The name comes from the cuckoo bird’s practice of laying its eggs in another bird’s nest while someone else unknowingly carries the burden.

Here is how it works. A criminal network identifies a legitimate remittance for example, a person in Australia waiting for a wire transfer of A$15,000 from a family member overseas. A corrupt money transfer agent or intermediary intercepts the instruction. Instead of forwarding the legitimate funds, the criminal network deposits the equivalent amount in illicit cash into the recipient’s Australian bank account in small installments, across several transactions. The legitimate sender’s funds are diverted elsewhere. The recipient receives money that appears to be the expected remittance but is actually laundered criminal proceeds.

Australia’s financial intelligence agency, AUSTRAC, has documented cuckoo smurfing extensively and requires financial institutions to file suspicious matter reports when the pattern is identified. Key red flags include multiple cash deposits to a single account from different individuals occurring close together, deposits that closely match an expected inward international transfer, and depositors who have no apparent relationship to the account holder.

Examples of smurfing

Smurfing appears across industries and transaction types. These real-world examples show how the tactic adapts to different environments.

The Hoggan bonus case

In 2016, Kelly Hoggan, the former head of the US Transportation Security Administration, split an improper $90,000 bonus into nine payments of exactly $10,000 each precisely at the Currency Transaction Report threshold to avoid generating a single suspicious transaction alert. Federal investigators identified the pattern and he was removed from his role. The case is now a textbook example of structuring that carries hallmarks of smurfing logic.

Retail banking cash deposits

A drug trafficking network pays street-level couriers to deposit cash into a network of accounts at different bank branches on the same day. Each deposit is under $9,000. No single account shows unusual volume. Aggregated across the network, $500,000 clears the banking system in a week. This is the classic smurfing model that prompted the Bank Secrecy Act’s reporting requirements.

Cryptocurrency Micro-Laundering

Criminal proceeds are broken into hundreds of transactions of under $1,000 each and moved through multiple cryptocurrency wallets across different exchanges before being consolidated into a single wallet and converted to fiat. The FATF’s 2023 report on virtual asset risks identifies this micro-structuring across crypto channels as one of the fastest-growing smurfing typologies.

Trade-Based Smurfing

An import business invoices a foreign counterpart for a consignment of goods at a price slightly below reporting thresholds. Multiple such invoices are raised across multiple shipments. The over- or under-valuation of goods conceals the transfer of value across borders, a form of smurfing that exploits trade documentation rather than direct cash transfers.

What is smurfing in gaming?

Smurfing gaming means creating secondary accounts to compete, participate, or transact at a level that does not reflect your true skill, status, or identity. The term applies across two distinct contexts iGaming (real-money online gambling and betting) and competitive video games or esports with very different implications for platforms and regulators.

Smurfing in iGaming bonus abuse and multi-accounting

In the iGaming sector, which includes online casinos, poker platforms, sports betting, and other real-money gaming environments, smurfing typically takes the form of multi-accounting. A player creates multiple accounts often using different email addresses, payment methods, or identity details to claim first-time deposit bonuses, free spins, or promotional credits repeatedly. Bonus abuse accounts for approximately 64% of all fraud in the iGaming sector, and multi-accounting is its primary mechanism.

Beyond bonus abuse, iGaming smurfs may use secondary accounts for matched betting (placing opposing bets across platforms to guarantee returns), arbitrage (exploiting odds differences between bookmakers), or chip dumping in poker (deliberately losing to a confederate to transfer funds). Most iGaming platforms prohibit multiple accounts per person. Detection relies on device fingerprinting, IP analysis, payment method cross-referencing, and behavioural pattern matching across account clusters.

Unlike smurfing in banking, iGaming smurfing does not typically constitute criminal money laundering. It is, however, a breach of platform terms of service and, depending on jurisdiction, may attract regulatory action under gambling licence conditions.

Smurfing in esports and video games skill manipulation

In competitive multiplayer video games and esports, smurfing refers to skilled players creating alternate accounts to compete against lower-ranked or less experienced opponents. Motivations range from the benign practising a new character or game mode without affecting a main account’s ranking to the harmful: intentionally stomping beginners, selling boosted accounts, or manipulating leaderboards.

This form of smurfing carries no financial crime dimension but does create a poor experience for newer players and has driven several major gaming platforms to implement device-level detection alongside account-level monitoring to identify and link smurf accounts to their primary profile.

How to detect and prevent smurfing

Detecting smurfing requires a shift away from single-account, threshold-based monitoring toward cross-account, behavioural, and network-based analysis. The FATF’s guidance on money laundering typologies consistently identifies static detection rules as insufficient against smurfing specifically because the tactic is designed to defeat them.

Transaction monitoring and threshold alerts

The foundational layer is automated transaction monitoring that aggregates activity across accounts, not just within them. Key alert triggers include high-frequency deposits of amounts just below the reporting threshold; identical or near-identical deposit amounts appearing across multiple accounts within short time windows; transactions occurring outside normal business hours; and inward remittances that are quickly fragmented and moved outward again. Financial institutions in the US are required under the Bank Secrecy Act to file a SAR if they suspect a customer is structuring or smurfing, even if no individual transaction meets the CTR threshold.

Behavioural analytics and pattern detection

Static rules catch known patterns. Behavioural analytics catch deviations from an individual’s or cohort’s established baseline. Modern AML platforms use machine learning to flag accounts whose transaction rhythm, counterparty geography, or value distribution shifts in ways consistent with smurfing even when each individual transaction looks unremarkable in isolation. Network graph analysis links accounts that share device IDs, IP addresses, beneficiary details, or timing clusters, surfacing the coordinated rings that underpin smurfing operations.

KYC and identity verification controls

Strong onboarding controls are the first line of defence. When smurfs open accounts, identity verification that cross-references submitted documents against watchlists, confirms liveness, and screens for adverse media reduces the pool of recruitable accounts criminals can build their networks from. Enhanced due diligence on high-risk customers those with unusual account opening behaviour, mismatched identity signals, or accounts opened in bulk from the same device or IP catches smurf recruiters before the network becomes operational.

SAR filing obligations

When smurfing is identified or suspected, financial institutions in most jurisdictions carry a mandatory obligation to file a suspicious activity report with the relevant Financial Intelligence Unit FinCEN in the US, the NCA in the UK, AUSTRAC in Australia. Filing obligations apply even where no individual transaction breaches a reporting threshold. Failure to file where smurfing is suspected carries its own regulatory risk, separate from the underlying crime.

How Shufti helps financial institutions stop smurfing

Smurfing thrives in the gaps between onboarding and ongoing monitoring where a customer who looked clean at sign-up is later used as a conduit for distributed transactions a compliance team never connects to each other.

Shufti’s AML screening solution addresses both ends of that gap. At onboarding, identity verification cross-references each applicant against sanctions lists, PEP databases, and adverse media across 1,200+ sources reducing the number of smurf accounts that make it into a platform in the first place. In ongoing monitoring, transaction pattern analysis flags the structural signatures of smurfing: near-threshold deposits, unusual frequency, coordinated timing across account clusters, and remittance flows inconsistent with a customer’s verified profile. Decisions are explainable because the models are Shufti’s own compliance teams see the specific signals behind each alert, not a black-box score they cannot defend to a regulator.

| See how Shufti’s AML monitoring detects smurfing patterns across your customer base. Book a demo. |

Frequently Asked Questions

What is smurfing in AML?

In Anti-Money Laundering (AML), smurfing is a technique where large illicit sums are split into many smaller transactions each kept below regulatory reporting thresholds and executed through a network of individuals to conceal the funds' origin. FATF classifies it as a core money laundering typology, and most national AML frameworks require financial institutions to file suspicious activity reports when smurfing patterns are identified.

Why do players use smurf accounts?

Players create smurf accounts primarily to compete against less skilled opponents without affecting their main account's ranking, to practise new characters or strategies anonymously, or to exploit welcome bonuses and promotional offers on gaming and betting platforms. In iGaming, the financial motivation of repeated bonus claiming is the dominant driver. In competitive games, the motivation is typically skill-based, though account selling and rank manipulation are also common secondary uses.

Is smurfing allowed in gaming or iGaming platforms?

Almost universally, no. The vast majority of iGaming operators and competitive gaming platforms explicitly prohibit multiple accounts per user in their terms of service. iGaming platforms that hold gambling licences may face regulatory consequences if multi-accounting is not actively detected and prevented. In esports, repeated smurfing on major platforms typically results in account bans. Unlike smurfing in banking, gaming smurfing is not a criminal offence in most jurisdictions but it is a breach of platform rules and increasingly subject to active enforcement through device fingerprinting and identity verification at sign-up.