European union’s another anti-money laundering directive is in the pipeline. And this time the union is aiming for uniformity in AML/CFT practices across member countries while keeping up with changing international regimes.

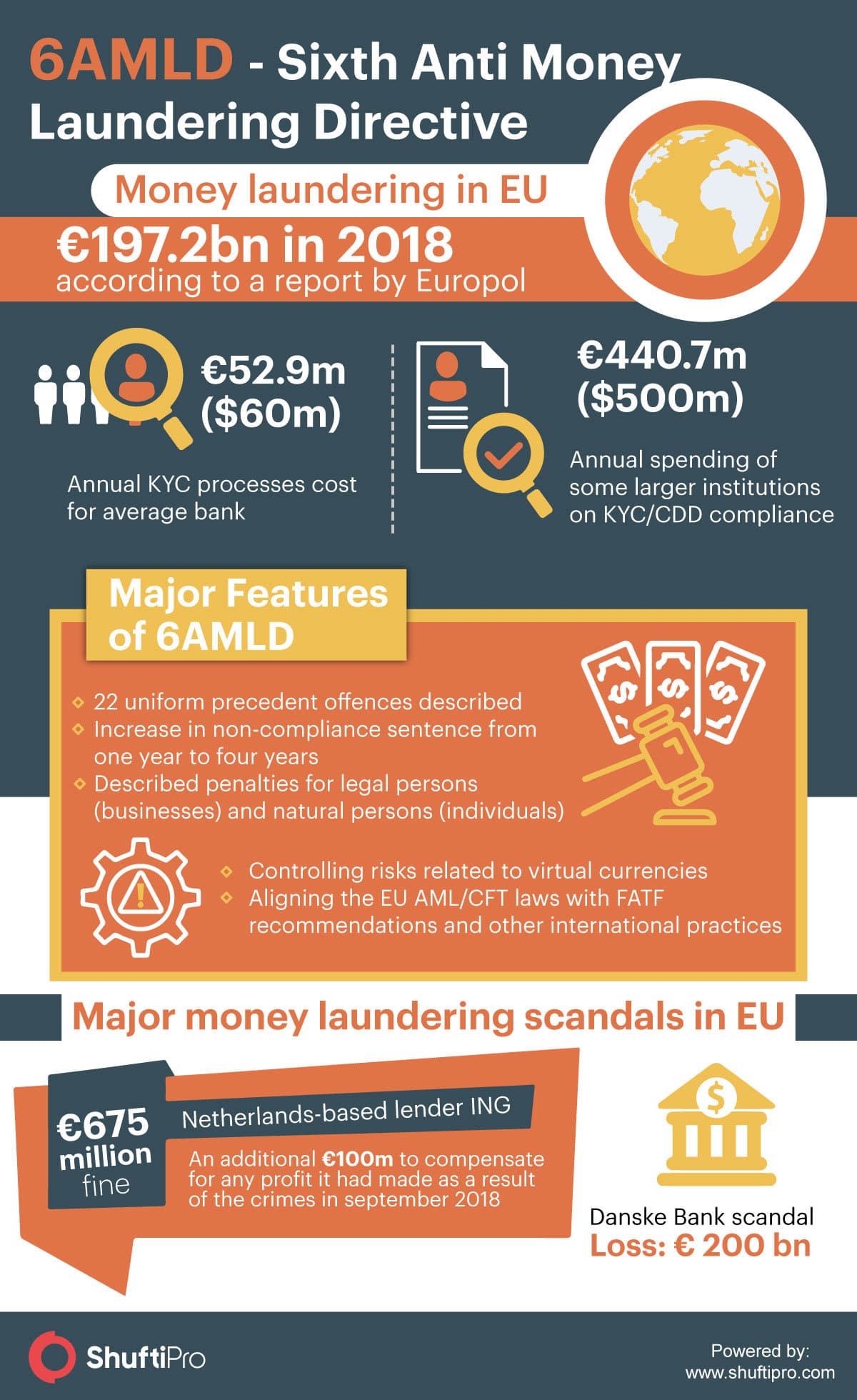

The estimated amount of money laundered globally in one year is 2 – 5% of global GDP, or $800 billion. And in the EU money laundering accounts for up to 1.2 % of the EU’s annual GDP, or around $225.2bn (€197.2bn) in 2018, according to a 2017 report by Europol.

Recently the 5AMLD was implemented on 10 January 2020. The fifth directive mainly targeted loopholes in certain sectors. It addressed the loopholes in prepaid cards, virtual assets, and precious metal dealing. The major change that came due to 5AMLD is that the identity verification threshold for prepaid cards is reduced from €250 to €150. This threshold for remote transactions is €50.

Now the 6AMLD is in the next big change in the AML/CFT regimes of the EU. The member states are required to integrate the new directive into their national laws by December 2020 and the reporting entities are required to completely implement the new laws by June 2021. The new directive is drafted well to close any left loopholes in AML/CFT regulations.

Key Features of 6AMLD

The 6AMLD is not only about fulfilling minimum regulatory requirements but about changing the attitude towards AML/CFT. The reporting entities need to go another mile to play their role in eliminating money laundering.

1. A list of predicate offences

A list of 22 predicate offences is provided in AMLD6. It includes offences related to environmental crime, cyber crimes, tax crime, and self-laundering. The directive includes ‘aiding and abetting’ and ‘attempting and inciting’, which means that criminal liability will be extended to people or businesses that are used in the criminal offence. Businesses will be liable for penalties if money laundering is channeled through their system due to a lack of preventive measures.

The offenses are clearly defined in the official journal of the 6AMLD. The reason behind this measure is to create uniformity in the AML/CFT measures of member states. Because lack of uniformity is one of the major reasons behind money laundering scandals in EU member states.

2. Increase in non-compliance penalties

The 6AMLD has clearly defined the penalties for businesses and individuals.

Natural persons

The individuals involved in money laundering are called “natural persons” in the 6AMLD. Non-compliance penalty is increased for the natural persons. Now a sentence of four years is non-compliance penalty, it was one year previously. As mentioned in the official journal,

“In order to deter money laundering throughout the Union, Member States should ensure that it is punishable by a maximum term of imprisonment of at least four years.”

Also, the monetary fine is increased to five million Euros.

Legal persons

Businesses are described as “legal person”. In case a business is found to be a part of a financial crime due to lack of AML measures or negligence it will be liable for these below-mentioned penalties:

- Exclusion from entitlement to public benefits or aid

- Permanent or temporary disqualification to perform commercial activities

- Judicial winding up

- Temporary or permanent closure

- Placed under judicial supervision

3. “Aiding and Abetting” and “ inciting and attempting”

The scope of AML regulations is increased to” aiding and abetting” and “ inciting and attempting”. The 6AMLD official journal clearly states, “Member States shall take the necessary measures to ensure that aiding and abetting, inciting and attempting an offence referred to in Article 3(1) and (5) is punishable as a criminal offence.”

4. Alignment with international laws

The Journal states that the member countries are required to implement the 6AMLD while keeping their AML/CFT laws aligned with international laws. It will increase transparency in financial infrastructure.

This means the reporting entities (businesses/ legal persons) will be required to follow the new regulations that will be aligned with international regimes.

Expert insight on 6AMLD

The CEO of Shufti, Victor Fredung, commented on this new directive and said, “6AMLD is more than a directive it is an attempt to initiate a new attitude towards AML/CFT compliance. Businesses and banks must take it as an opportunity to explore new ventures at a global level with the expected alignment of EU AML laws with international AML laws and FATF recommendations.”

5. FATF recommendations EU AML laws

The 6AMLD will require the member countries to align AML laws with the FATF recommendations. The tax crimes are defined as a criminal offence and the preventive measures are required to be designed in light of revised recommendations of FATF.

6. Not missing on the virtual currencies

The sixth anti-money laundering directive requires the member countries to take concrete steps towards elimination of risk coming with these virtual assets. The reporting entities such as crypto exchanges, digital asset exchanges, cryptocurrency dealers, crypto wallet providers and businesses accepting cryptocurrency payments will be facing some major AML/KYC compliance scrutiny in 2021.

How businesses should prepare for the change?

The ultimate effect of changing regimes is on the businesses. The new directive is drafted to change the perspective of businesses towards AML/CFT compliance. The new regulations of “Aiding and abetting”, and “ inciting and attempting” have changed the compliance requirements. Businesses will be liable for heavy penalties if they’re found to be involved in the criminal offence. Even if they’re used as a tool or a channel.

The reporting entities are required to have an in-depth understanding of the risks and threats and to take necessary steps to eliminate the risk of any of the listed criminal offences being channeled from their platform.

The businesses are expected to have a completely updated setup for compliance requirements. Digital identity screening could prove to be a reliable partner of the businesses in this regard. As it provides global coverage in the screening of individuals and businesses it helps reporting entities maintain a global risk cover against bad actors.