AMLR Solutions

AMLR Solutions AMLR Consultation

AMLR Consultation Onboarding

Onboarding Ongoing Monitoring

Ongoing Monitoring FRAML

FRAML KYC

KYC KYB

KYB KYI

KYI Age Assurance

Age Assurance Workforce IAM

Workforce IAM Candidate Verification

Candidate Verification Account Takeover

Account Takeover Bonus/ Promotion Abuse

Bonus/ Promotion Abuse Chargeback Fraud

Chargeback Fraud Deepfake

Deepfake Document Fraud

Document Fraud Fraud Networks

Fraud Networks Impersonation Fraud

Impersonation Fraud Money Mule Activity

Money Mule Activity Multi-Accounting

Multi-Accounting Party Fraud

Party Fraud Regulatory & Compliance Risks

Regulatory & Compliance Risks Synthetic Identity Fraud

Synthetic Identity Fraud Adult Content

Adult Content Banking

Banking Crypto

Crypto Fintech

Fintech Forex

Forex Compliance

Compliance Fraud prevention

Fraud prevention Trust & safety

Trust & safety Global expansion

Global expansion Compliance Officers

Compliance Officers Developers

Developers Fraud Analysts

Fraud Analysts Product Managers

Product Managers Advanced Journey Builder (AJB)

Advanced Journey Builder (AJB) Global Trust Platform

Global Trust Platform Customer Profiles

Customer Profiles Vendor Comparison

Vendor Comparison IDV Case Management

IDV Case Management AML Case Management

AML Case Management Regulatory Reporting

Regulatory Reporting Travel Rule Protocols

Travel Rule Protocols Agentic Rule Builder

Agentic Rule Builder AI Compliance Co-Pilot

AI Compliance Co-Pilot Fraud Analytics

Fraud Analytics Fraud Hub

Fraud Hub OCR

OCR Shufti AI

Shufti AI Bank Account Verification

Bank Account Verification Biometric Duplication

Biometric Duplication Database Checks

Database Checks Document Intelligence

Document Intelligence Government ID

Government ID Mobile Driver's License

Mobile Driver's License NFC

NFC Selfie Liveness

Selfie Liveness Brand Personalisation

Brand Personalisation Deployment Options

Deployment Options Identity Methods

Identity Methods IDV Modes

IDV Modes Multi-tenancy

Multi-tenancy On-Premise IDV

On-Premise IDV Secure Capture

Secure Capture

Docless Identity Verification in the Middle East

A practitioner’s guide to the GCC and beyond.

How national digital identity, fragmented regulation, and data-residency rules reshape identity verification across the GCC and beyond, with digital-identity adoption, the regulatory map, and a vendor checklist.

Schedule a DemoWhy The Region Is Nine Markets, Not One

Teams expand into the Middle East and discover it is closer to a dozen markets than one.

A verification flow tuned for the United Arab Emirates will not satisfy a Saudi regulator, accept a Qatari credential, or meet Bahrain’s transfer rules without rework. Each country has its own identity document, its own digital identity system, its own financial regulator, and its own data-protection law, and several of those laws have changed inside the last two years.

This matters to two kinds of reader. The first is a local team, a bank in Riyadh or a fintech in Manama, that must onboard customers under a named domestic regulator. The second is a global team, a payments company in London or an exchange in Singapore, onboarding customers from the region or expanding into it. For both, the failure mode is the same: a control that looks compliant in one Gulf state quietly breaks the audit trail in the next, and the gap usually shows up at the worst moment, during a regulatory review or a spike in onboarding volume. The region rewards teams that treat it as a set of distinct markets rather than a single block.

All 6 GCC states now run a national digital identity system, from UAE Pass to Saudi Arabia’s Nafath. A verification setup that ignores them is already a step behind the markets it serves.

Three things vary market by market, and each can break an onboarding flow on its own.

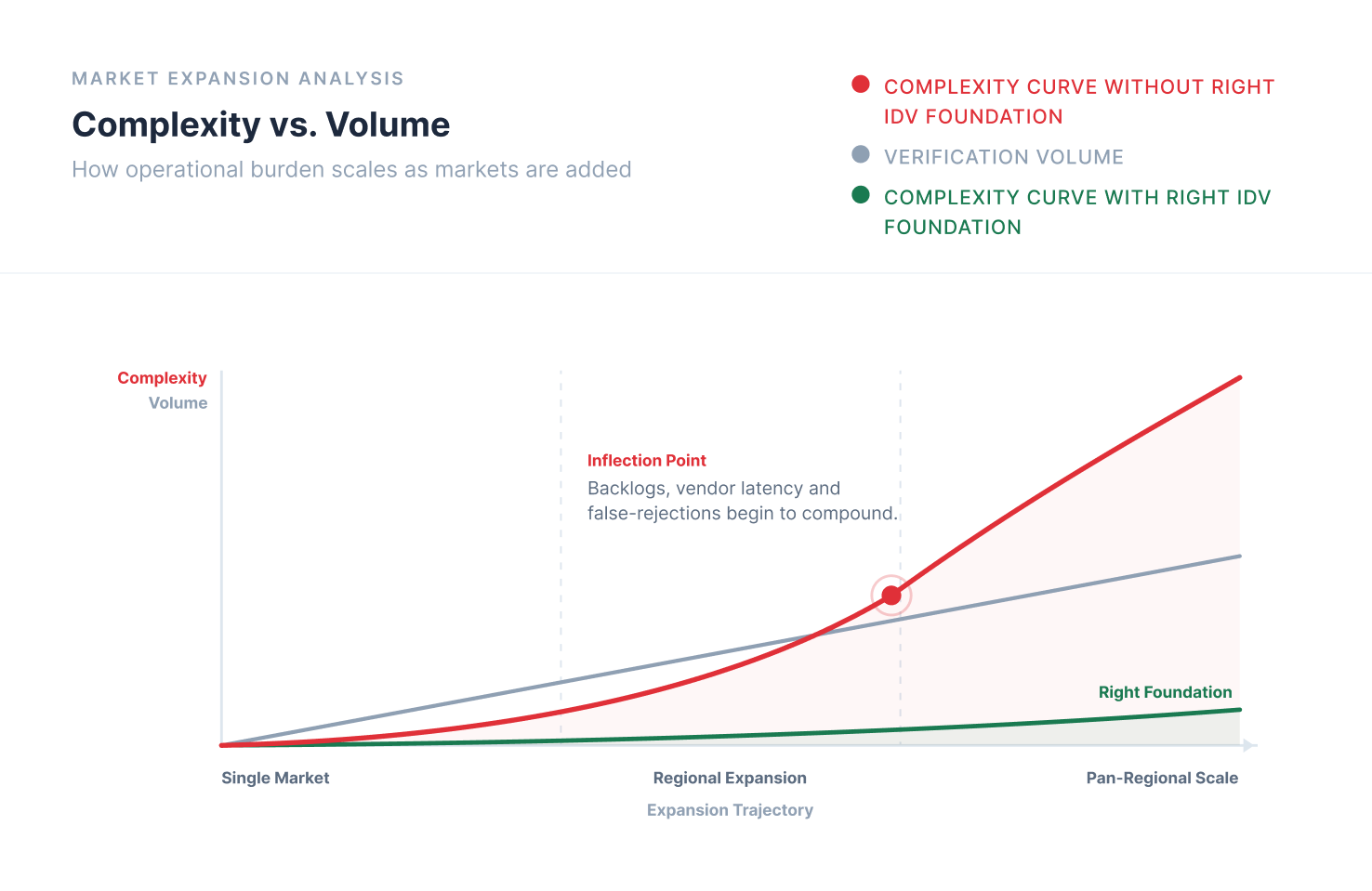

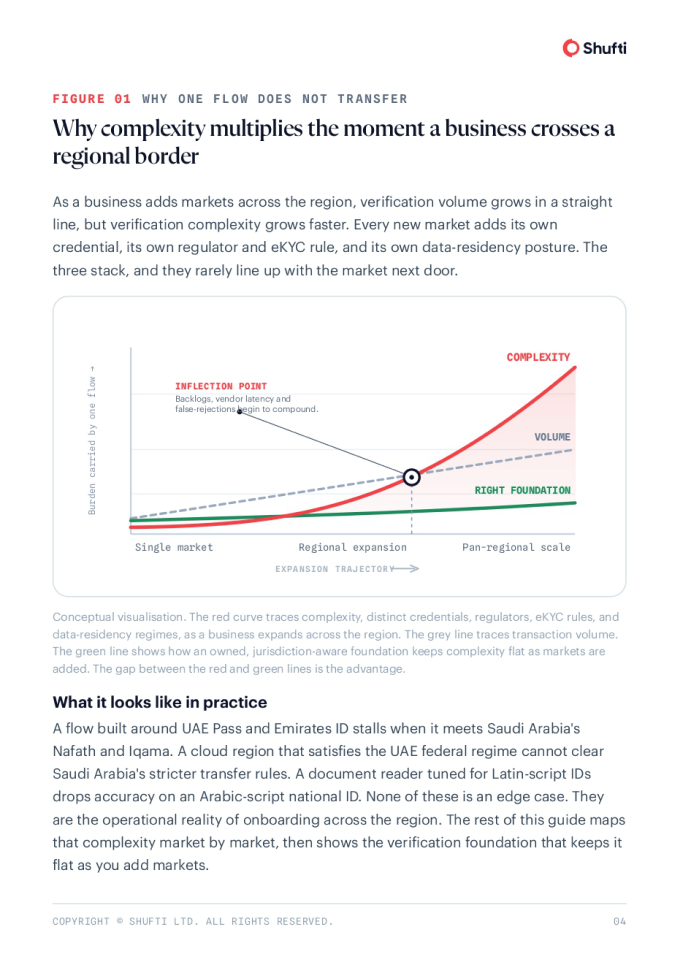

Figure 01 · Why One Flow Does Not Transfer

Identity verification complexity multiplies the moment a business crosses a regional border

As a business adds markets across the region, verification volume grows in a straight line, but verification complexity grows faster. Every new market adds its own credential, its own regulator and eKYC rule, and its own data-residency posture. The three stack, and they rarely line up with the market next door.

Conceptual visualisation. The red curve traces complexity, distinct credentials, regulators, eKYC rules, and data-residency regimes, as a business expands across the region. The grey line traces transaction volume. The green line shows how an owned, jurisdiction-aware foundation keeps complexity flat as markets are added. The gap between the red and green lines is the advantage.

What does identity verification complexity look like in practice

A flow built around UAE Pass and Emirates ID stalls when it meets Saudi Arabia’s Nafath and Iqama. A cloud region that satisfies the UAE federal regime cannot clear Saudi Arabia’s stricter transfer rules. A document reader tuned for Latin-script IDs drops accuracy on an Arabic-script national ID. None of these is an edge case. They are the operational reality of onboarding across the region. The rest of this guide maps that complexity market by market, then shows the verification foundation that keeps it flat as you add markets.

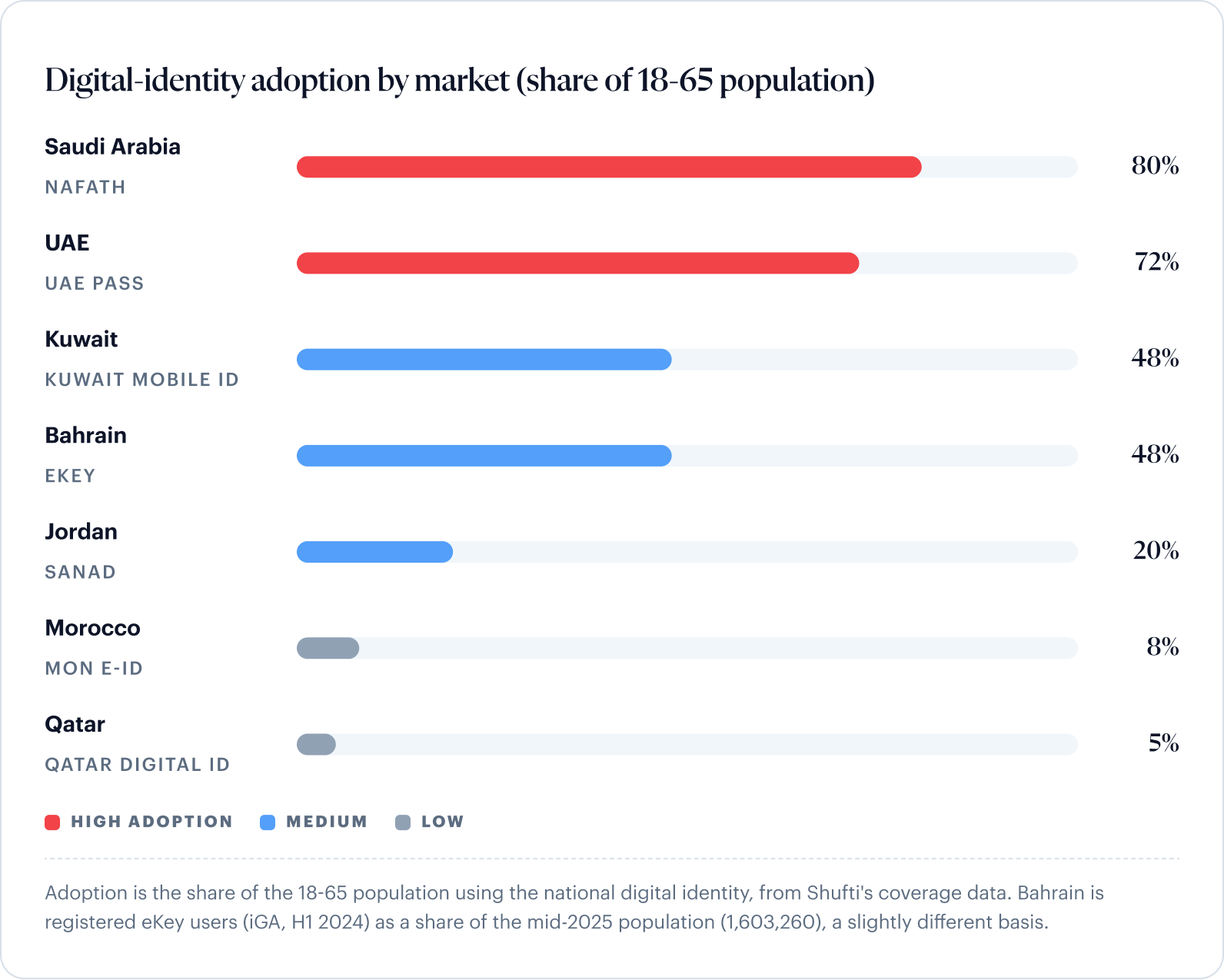

Digital Identity Adoption, Market By Market

National digital-identity adoption across the region

The Gulf is moving fastest on national digital identity, and the spread is wide. In Shufti’s coverage data, adoption of the national digital identity, measured as the share of the 18-65 population, ranges from the low single digits to around 80%. The markets with the highest adoption are the ones where a digital-identity route into onboarding is already the default rather than the exception. Adoption decides which route leads, not whether a market can be served: where it is high a docless route can run first, and where it is still building, document verification carries more of the volume, with a document and biometric fallback either way.

Three things that vary by market

Onboarding in this region turns on three questions, and the answer to each changes as you cross a border. A verification setup that handles all three, market by market, is the one that holds up under audit.

The credential

Which national ID and digital identity?

UAE Pass, Nafath, Qatar Digital ID, Kuwait Mobile ID, and others are distinct systems with distinct enrolment and verification paths. A flow built around one does not automatically accept another.

The rule

Has the regulator published eKYC rules?

Some regulators have explicit electronic KYC rules or platforms, the UAE, Saudi Arabia, Qatar, Bahrain, and Jordan among them. Others have none on the public record, so onboarding rests on the general AML framework.

The residency

Where must the data sit?

Most regimes allow cross-border transfer under conditions. Saudi Arabia is stricter and often points towards in-country processing. It can differ between Riyadh and Dubai for the same company.

Reading the pattern

The Gulf states lead on national digital identity and on explicit eKYC rules, while the Levant and North Africa are catching up fast, with Jordan and Egypt scaling national platforms. Adoption and regulatory clarity tend to move together.

Regional coverage is not a single integration decision but a sequence of market-by-market calls on credential, rule, and residency, and the vendor that absorbs all three without a separate build per border is the one that scales.

“A control that looks compliant in one Gulf state can quietly break the audit trail in the next.”

UAE and Saudi Arabia: The Anchor Markets

The region’s two most developed markets, and its strictest data regime.

The Anchor Markets · UAE

United Arab Emirates

The UAE is the region’s most developed digital identity market. The mandatory national credential is the Emirates ID, issued by the Federal Authority for Identity, Citizenship, Customs and Port Security to every citizen and resident. On top of it sits UAE Pass, the unified national digital identity and signature platform, with adoption around 72% of the 18-65 population on Shufti’s coverage data.

Regulator & AML rules

Federal Decree-Law No. 10 of 2025 came into force on 14 October 2025, replacing the long-cited Federal Decree-Law No. 20 of 2018, so any policy still citing the 2018 law is now out of date. Electronic KYC is expressly permitted, with Central Bank guidance on using digital identification for customer due diligence.

Data & free-zone regimes

The federal Personal Data Protection Law (Decree-Law No. 45 of 2021) imposes no blanket localisation. The complication is parallel regimes: the DIFC (Law No. 5 of 2020) and the ADGM (Regulations 2021) each have their own commissioner, so a deployment that satisfies the federal law may still answer to a free-zone regulator.

A large share of the population are expatriate residents whose Emirates ID and supporting documents differ from a citizen’s. A flow built only around the national-citizen path will stall on the resident case, which is the majority case.

For Dubai virtual-asset businesses there is a further layer, the Virtual Assets Regulatory Authority, established under Dubai Law No. 4 of 2022.

The Anchor Markets · Saudi Arabia

Saudi Arabia

Saudi Arabia pairs the region’s highest eID adoption with its strictest data regime. Its identity infrastructure is anchored on Nafath, the national single sign-on operated under SDAIA, alongside Absher, the Ministry of Interior’s e-services platform. Adoption is the highest of any Gulf eID, around 80% of the 18-65 population. The underlying credentials are the National ID for citizens and the Iqama for residents.

Regulator & AML rules

The Saudi Central Bank supervises banks, payments, and finance companies, under the Anti-Money Laundering Law issued by Royal Decree No. M/20 of 2017. Remote KYC is permitted: the rulebook sets the KYC requirements and recognises approved electronic services, with Nafath as the principal verification rail.

The Personal Data Protection Law, Royal Decree No. M/19 of 2021, came into force in 2023 and was enforced from September 2024. Its cross-border transfer regime is stricter than the UAE federal regime: outbound transfers must fit a permitted basis and may need safeguards and a risk assessment. The law states no blanket localisation rule, but in practice that can make in-Kingdom processing the lower-friction architecture. Saudi Arabia has also not published a broad dedicated crypto-asset regime, so virtual currencies remain outside the recognised local framework.

“A global team cannot assume its existing cloud region will satisfy the Saudi regulator.”

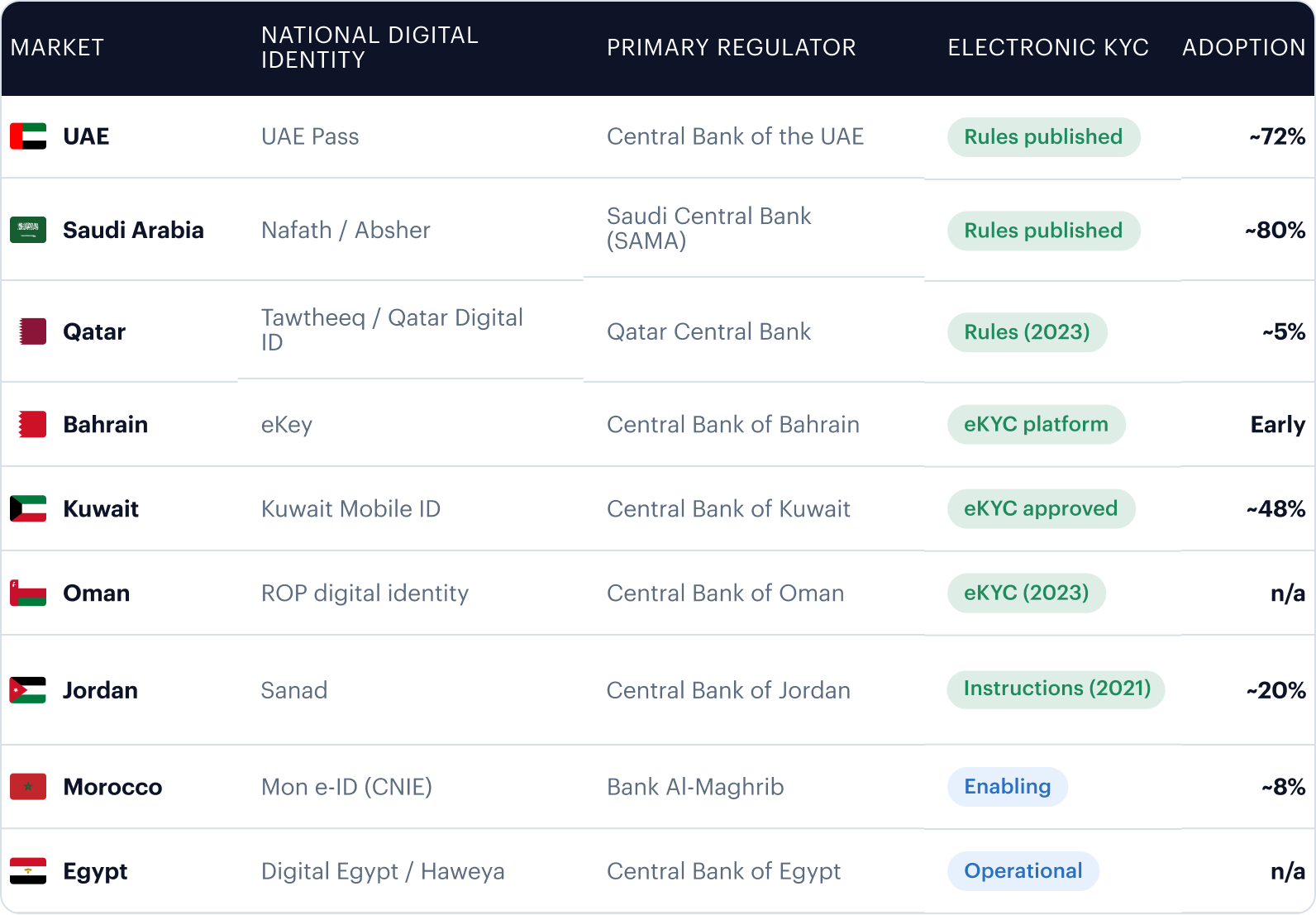

Who Regulates What

Who regulates what, market by market

The primary financial regulator and the named AML statute differ by market, and so does whether the regulator has published explicit electronic KYC rules. Read it as the orientation map.

Law numbers and dates are exact. Egypt’s non-bank financial sector is supervised by the Financial Regulatory Authority (FRA).

The markets with published eKYC rules are, with few exceptions, the markets with the highest digital-identity adoption. The detail for each sits in the anchor and core sections.

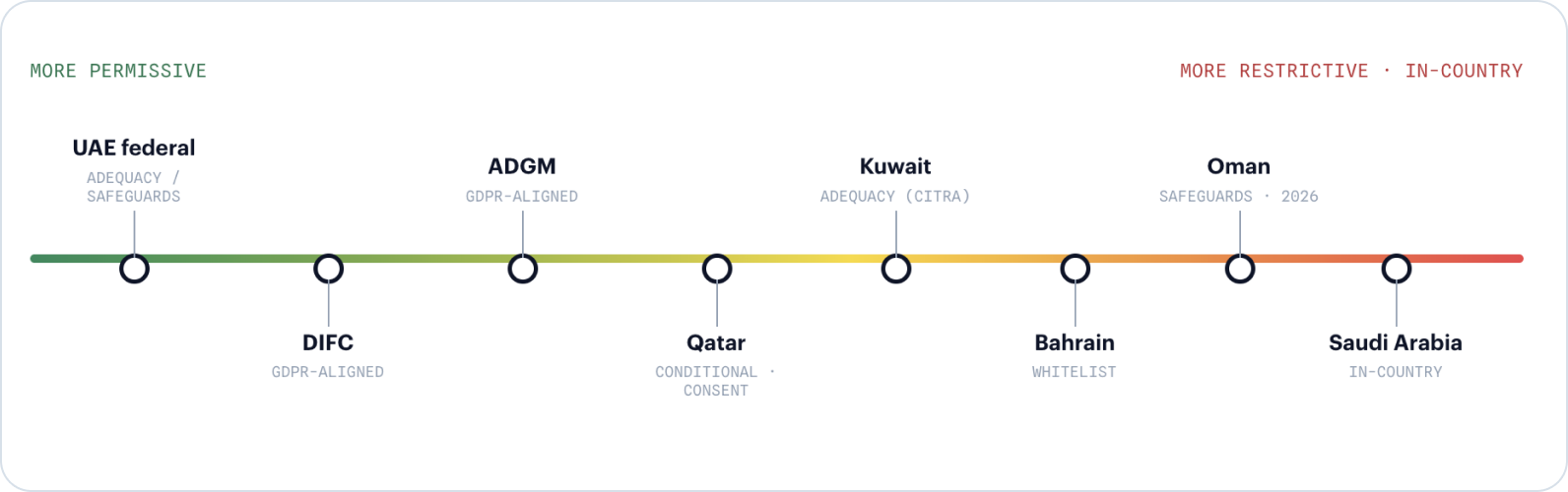

Why transfer rules push businesses toward in-country data

With one main exception, the region’s data rules are not blanket localisation mandates. The legal position is a conditional cross-border-transfer model: personal data may leave the country if the destination offers adequate protection, or under approved safeguards, or with the data subject’s consent. The exception is Saudi Arabia, whose regime is stricter: outbound transfers must fit a permitted basis and may need safeguards, which can make in-country processing the lower-friction choice.

Where a regime permits transfer only under conditions, those conditions still have to be demonstrated to a regulator if the deployment is audited, and the burden sits with the business. This is why many businesses decide to keep the data in country. One of the first filters teams apply when choosing a vendor is whether a verification solution can deploy on-premises or in-country and keep personal data inside the border. A SaaS-only solution with no in-region option often cannot clear that bar.

Qatar, Kuwait, Bahrain, and Beyond

Qatar, Kuwait, and Bahrain

Beyond the two anchors, three more Gulf markets carry real onboarding activity, each with its own digital identity and its own regulatory posture.

The Numbers At A Glance

The QCB E-KYC Regulation took effect, with prior approval needed to deploy. The market runs two systems: Tawtheeq for login and the Qatar Digital ID app as a credential wallet.

Kuwait Mobile ID adoption among the 18-65 population. The CBK has issued digital-onboarding instructions and approved electronic KYC, so remote onboarding is permitted and live.

Bahrain eKey reach, registered users against the mid-2025 population. Its national eKYC platform went live under the Central Bank in 2021, after a regulatory sandbox (2017) and open banking rules (2018).

Qatar’s two-system split is the common trap: Tawtheeq, the National Authentication System, is the federated login layer, while the Qatar Digital ID app is the credential wallet, enabled for airport e-gate use by early 2025. Kuwait has moved on too: the Central Bank has issued digital-onboarding instructions and approved electronic KYC, so remote onboarding is live. Bahrain has the cleanest documented story in the Gulf, with the platform operated by BENEFIT alongside the Information and eGovernment Authority.

Oman, the Levant, and North Africa

Oman is often assumed to lack a national digital identity, and that is no longer accurate. The Royal Oman Police operates a digital identity service, and from September 2025 certified mobile versions of the national ID carry the same legal validity as the physical card for many official uses. The Central Bank issued digital-onboarding and e-KYC instructions in 2023, with a national eKYC registry (Mala’a), so remote onboarding is supported by national infrastructure as well as that digital identity.

eKYC Is Permitted And Scaling

Beyond the Gulf, three markets are worth covering for teams whose footprint reaches the Levant and North Africa, and electronic KYC is permitted and actively scaling in each. Jordan has the strongest documented position: the Central Bank’s binding E-KYC Instructions of 2021 authorise remote onboarding and set the minimum controls, and the national Sanad app added instant in-app activation in January 2026. Morocco provides for remote account opening under Bank Al-Maghrib Circular Letter No. 1/W/2020, alongside the CNIE card and the Mon e-ID app. Egypt runs the Central-Bank-backed Haweya platform, which delivers remote eKYC and account opening across dozens of banks. The common thread is that national digital identity and remote eKYC are now the direction of travel across the whole region, not only the Gulf.

Where each market stands today

The national digital identity, the electronic-KYC basis, and the data-protection law for Oman and the Levant and North Africa trio.

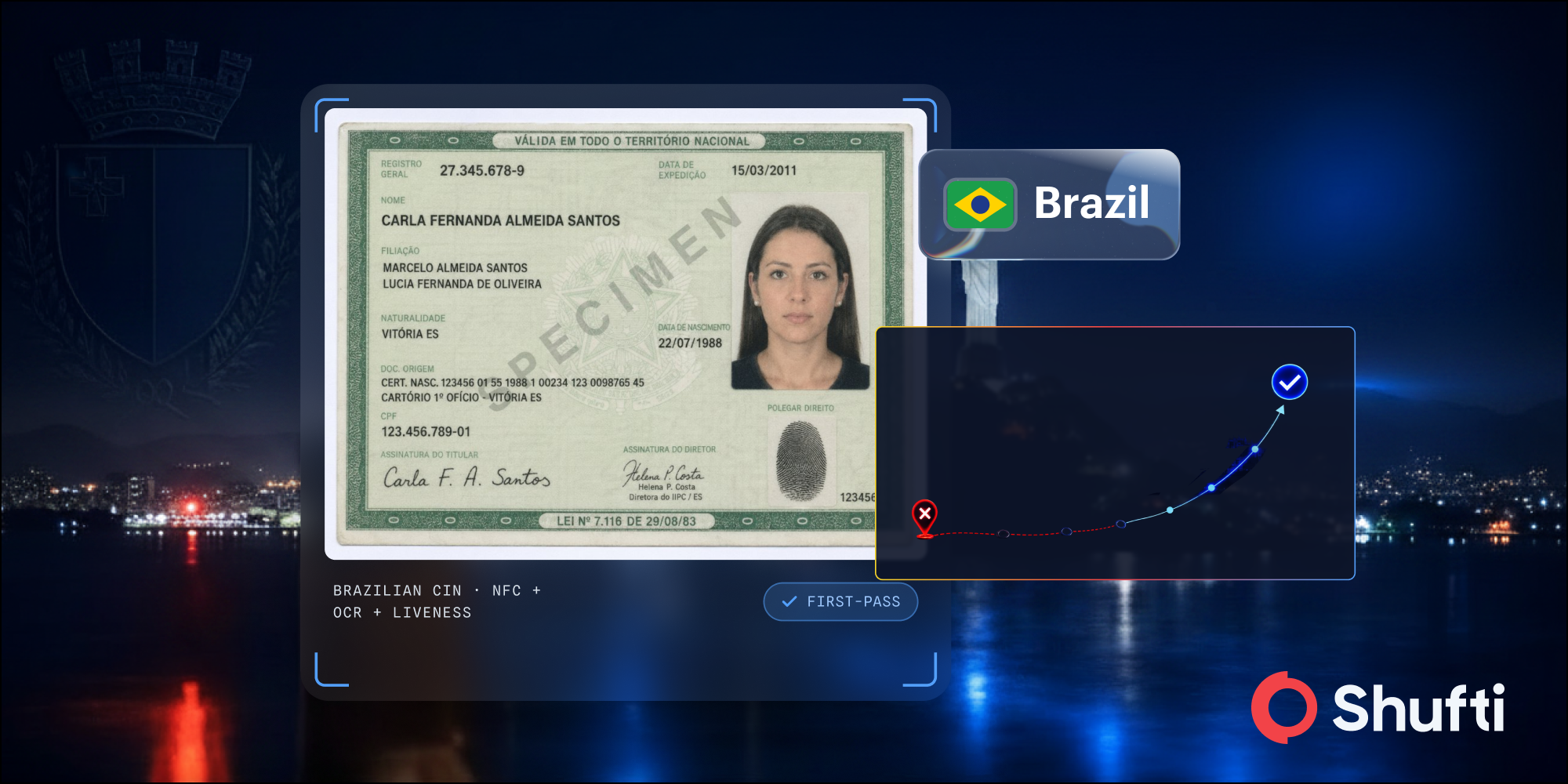

Because national-eID adoption is still building in these markets, document verification is the primary onboarding lane here and the docless route the accelerator: Shufti reads Arabic-script IDs with proprietary OCR at 94% accuracy, against 64% for Google’s general-purpose engine, so the document lane stays reliable where the eID has not yet scaled.

Oman

- ROP digital identity, legally recognised from Sept 2025

- CBO digital-onboarding and e-KYC instructions (2023), Mala’a registry

- AML Royal Decree 30/2016 · PDPL enforceable Feb 2026

Jordan

- Sanad national app, ~20% adoption; instant activation Jan 2026

- Binding CBJ E-KYC Instructions (2021)

- PDPL Law No. 24 of 2023

Morocco

- CNIE card + Mon e-ID, ~8% adoption

- Remote accounts under BAM Circular 1/W/2020

- AML under Law 43-05 (amended 2021)

Egypt

- Digital Egypt + CBE-backed Haweya, remote eKYC across banks

- AML under Law No. 80 of 2002

- PDPL executive regulations, Nov 2025

Where The Compliance Pressure Lands

Which industries feel the onboarding pressure most

The pressure this guide has mapped, explicit eKYC mandates, data-residency rules, and fast-changing regulation, does not fall evenly. Three industries absorb it most directly, and it takes a different shape in each.

The eKYC Mandate

The eKYC MandateBanking and fintech

Central banks have made remote KYC explicit and prescriptive. Qatar’s QCB requires prior approval to deploy an eKYC solution, and Jordan’s CBJ Instructions specify biometrics, liveness, and tamper checks. National eID rails like UAE Pass and Nafath are becoming the expected route, and with expatriate-majority populations a flow must handle both citizen and resident credentials.

A Regulatory Patchwork

A Regulatory PatchworkCrypto and virtual assets

Rules differ within countries, not just between them. In the UAE alone a provider may answer to VARA in Dubai, the FSRA in ADGM, or the DFSA in the DIFC, each with its own due-diligence bar, with the FATF Travel Rule on top. Orchestration resolves this: one flow reads the VASP’s licensing zone and applies the matching Travel Rule data set from one integration instead of three builds.

Data Residency First

Data Residency FirstGovernment and large enterprise

For public bodies and large regulated enterprises, the national eID is both the verification method and the residency constraint, and procurement often calls for in-country or on-premises deployment a SaaS-only model cannot meet. A cross-border enterprise meets the full fragmentation at once: nine markets, nine regulators, nine credential sets.

Docless Onboarding Via National eID Rails

Why move to docless identity verification?

Electronic identity verification checks a person against an authoritative national identity source rather than a submitted document, and that switch changes both the economics and the risk of onboarding. Querying a source of truth is structurally harder to beat than inspecting an uploaded image, so the attack surface for template forgery and for deepfaked or AI-generated documents largely collapses. It also removes the document-capture step where much onboarding drop-off happens, so a user with a national digital identity finishes in seconds, and Shufti’s eIDV deployments achieve a pass rate of nearly 99%. It pairs with document and biometric verification rather than replacing them, so coverage is never capped by how many people hold the eID.

MENA pass rate: how docless compares

2025 dataOther-vendor figures are typical industry ranges, not a named-vendor comparison. Shufti overall is the blended document- and-docless pass rate across the nine markets; docless is the eIDV deployment figure. Shufti data, 2025.

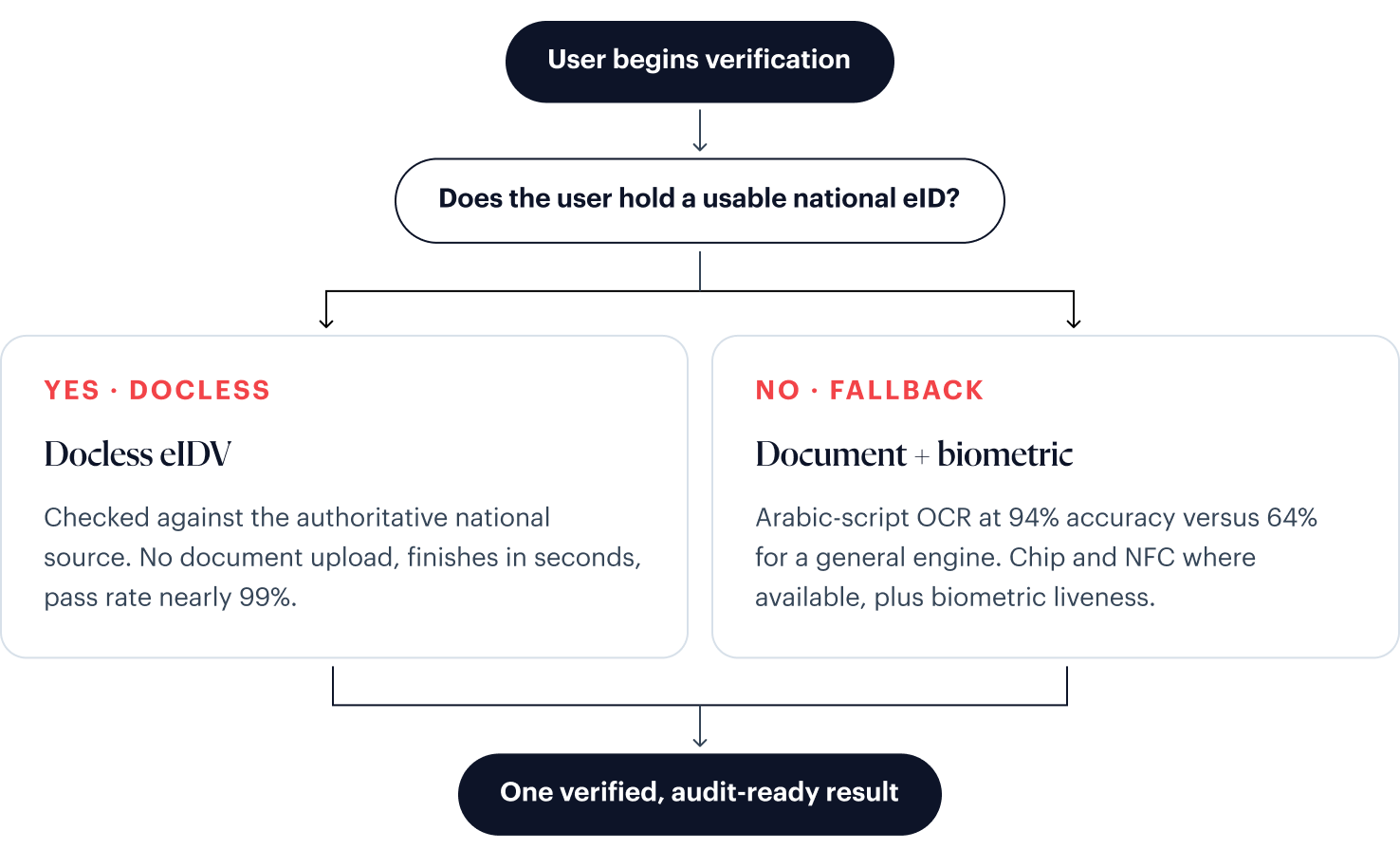

Figure 02 · How Routing Works

One platform decides the route per user

Docless leads wherever it can. The platform checks whether each user holds a usable national digital identity, then routes accordingly, so a high-assurance result is reached either way and coverage never depends on how many people in a market hold the eID.

Figure 02 · Routing is per user, not per market. Where national-eID adoption is high the docless path carries most users; where it is still building the document path does, with docless applied for those who can use it. The same integration covers both.

Why Most IDV Vendors Fall Short Here

Two reasons most IDV vendors struggle in the region

Against this combination of distinct credentials, divergent data rules, and Arabic-script documents, most identity verification vendors are structurally disadvantaged in two compounding ways.

Cannot meet in-country data residency

A SaaS-only solution with no in-region or on-premises option cannot keep personal data inside the border. In a region where transfer rules are hard to demonstrate under audit and Saudi Arabia points towards in-Kingdom processing, that is a hard ceiling. The vendor either cannot serve the market or forces the customer into a transfer arrangement that may not survive a regulator’s review.

Retrofitted for Western documents

Many verification systems were built around Western documents and retrofitted for everything else. That shows up as a failed read on an Arabic-script national ID or a rejected residence permit at the worst moment, when a genuine customer is mid-onboarding. A vendor that stitches together third-party engines is also always a step behind, waiting on someone else’s roadmap when a regional requirement changes.

“The two compound: a vendor that cannot keep data in-country and cannot read the region’s documents is not one fix away from fit, it is the wrong architecture for the region.”

Seven questions for your verification vendor

Seven questions every regional compliance and product team should put to their identity verification vendor, current or prospective.

Can the vendor deploy on-premises or in-country and keep personal data inside the border?

Does the vendor read Arabic-script national IDs and regional residence permits accurately?

Does the vendor cover the region’s national digital identities, live or available for integration?

Can the vendor meet each market’s electronic KYC rules without a separate build per country?

Does the vendor own its liveness and deepfake detection, with independent validation?

Does the vendor handle both citizen and expatriate-resident onboarding paths?

Does the vendor adapt quickly when a regional regulator changes the requirement?

What The Right IDV Foundation Looks Like

Owned end to end, built for the region it serves

The verification problem in this region is not solved by a longer feature list. It is solved by an architectural decision: own the core verification technology end to end, accept the full range of identity inputs the region actually uses, and be deployable where each regulator needs the data to sit.

This is what flattens the curve in Figure 01: one owned, jurisdiction-aware platform that takes on a new market as a configuration change, not a rebuild. The same platform decides the route per user rather than per market, so a holder of a usable national eID goes through the docless route first while anyone else is sent automatically to document and biometric verification (Figure 02).

Owned end to end · One roadmap

Deployable where the data must live · One API

Shufti’s approach

Document reading, document authentication, biometric matching, liveness, and deepfake detection are all developed in-house, on one roadmap. Shufti actively verifies 10,000+ document types each month across 240+ countries and territories, with proprietary OCR reading 150+ languages including Arabic, and no human fallback for low-confidence reads. A Saudi deployment can keep processing in-Kingdom while a Dubai deployment runs differently, without standing up a second vendor.

“One platform, fully owned technology, deployable where the data must live, rather than a stack assembled from parts no one fully controls.”

Certifications

Independently audited and certified for enterprise-grade security and data protection.

Frequently Asked Questions

Largely yes. The UAE, Saudi Arabia, Qatar, and Bahrain have published explicit electronic KYC rules or platforms, Jordan has binding E-KYC instructions, and Kuwait and Oman have since issued digital-onboarding and electronic KYC instructions of their own. Remote onboarding is now permitted across the Gulf, though conditions differ by market, so confirm the current position with the relevant regulator before launch.

All of them. UAE Pass, Saudi Arabia’s Nafath, Qatar’s Tawtheeq and Qatar Digital ID, Kuwait Mobile ID, Bahrain’s eKey, and Oman’s Royal Oman Police digital identity are all live national systems, though their maturity and adoption differ.

Mostly no. Most regimes allow cross-border transfer under adequacy, safeguards, or consent. Saudi Arabia is the main exception, with a stricter transfer regime that often points towards in-Kingdom processing. In practice, because transfer conditions are hard to demonstrate under audit, many businesses choose in-country residency anyway.

It must, because residents are a large share of the population in the Gulf. Citizen and resident credentials differ, and a flow built only around the national-citizen path will fail on the resident case.

Yes. Federal Decree-Law No. 10 of 2025 came into force on 14 October 2025 and replaced the earlier 2018 law. Onboarding policies that still cite the 2018 law should be updated.

Form submitted successfully!

Thank you for your interest — your report is loading now.

Verification built for the region it serves

Get the full 20-page guide: the regional landscape, the regulatory map for nine markets, the data-residency response, and the vendor checklist. Or start with a short conversation about your own onboarding data.