Face Verification

Face Verification

Address Verification

Address Verification

Document Verification

Document Verification

Age Verification

Age Verification

VideoIdent

VideoIdent

Fast ID

Fast ID

Docless Verification

Docless Verification

Consent Verification

Consent Verification

NFC Verification

NFC Verification

Business Verification

Business Verification

Due Diligence

Due Diligence

Investor Verification

Investor Verification

E-Signature

E-Signature

QES

QES

AML Screening

AML Screening

Transaction Monitoring

Transaction Monitoring

Adverse Media

Adverse Media

Business AML Screening

Business AML Screening

PEP & RCA

PEP & RCA

Sanctions

Sanctions

Watchlist

Watchlist

Behavioural Biometrics

Behavioural Biometrics

Device Fingerprinting

Device Fingerprinting

Biometric Face Authentication

Biometric Face Authentication

MFA

MFA

Fraud Hub

Fraud Hub

Onboarding

Onboarding

Ongoing Monitoring

Ongoing Monitoring

KYC

KYC

KYB

KYB

KYI

KYI

Age Assurance

Age Assurance

Identity Verification

Identity Verification

Workforce IAM

Workforce IAM

Candidate Verification

Candidate Verification

Compliance

Compliance

Fraud prevention

Fraud prevention

Trust & safety

Trust & safety

Global expansion

Global expansion

Product Managers

Product Managers

Compliance Officers

Compliance Officers

Fraud Analysts

Fraud Analysts

Developers

Developers

Deepfake Detection

Deepfake Detection

Bonus Abuse / Promotion Abuse

Bonus Abuse / Promotion Abuse

Account Takeover

Account Takeover

Synthetic Identity Fraud

Synthetic Identity Fraud

Document Fraud

Document Fraud

Impersonation Fraud

Impersonation Fraud

Multi-Accounting

Multi-Accounting

Fraud Networks

Fraud Networks

Chargeback Fraud

Chargeback Fraud

Money Mule Activity

Money Mule Activity

Party Fraud

Party Fraud

Regulatory & Compliance Risks

Regulatory & Compliance Risks

Fintech

Fintech

Crypto

Crypto

iGaming

iGaming

Forex

Forex

Social Network

Social Network

Marketplace

Marketplace

Banking

Banking

Gig Economy

Gig Economy

Payments

Payments

Ride Hailing

Ride Hailing

Adult Content

Adult Content

Blind Spot Audit

Blind Spot Audit

Deepfake Detector

Deepfake Detector

Liveness Spoofs

Liveness Spoofs

Document Originality

Document Originality

Document Deepfake

Document Deepfake

Global Trust Platform

Global Trust Platform

Journey Builder

Journey Builder

Case Management

Case Management

Shufti AI

Shufti AI

Fraud Analytics

Fraud Analytics

Vendor Comparison

Vendor Comparison

Brand Personalisation

Brand Personalisation

AI Compliance Co-Pilot

AI Compliance Co-Pilot

OCR

OCR

Secure Capture

Secure Capture

Deployment Options

Deployment Options

Identity Methods

Identity Methods

API Documentation

API Documentation

Mobile SDKs

Mobile SDKs

Service Status

Service Status

Help Center

Help Center

Contact Us

Contact Us

Technical Support

Technical Support

Supported Documents

Supported Documents

Supported Countries

Supported Countries

Content library

Content library

Blogs

Blogs

News

News

Reports

Reports

Insights

Insights

Knowledgebase

Knowledgebase

ROI calculator

ROI calculator

About

About

Career

Career

Press Release

Press Release

Certifications

Certifications

Partnership

Partnership

Awards

Awards

Events & Webinar

Events & Webinar

Interactive Demo

Interactive Demo

Podcast Studio

Podcast Studio

Spotlight Studio

Spotlight Studio

Cyprus’s 2026 KYC Pass Rate Guide

Cyprus clears about 73 of every 100 identity checks on the first try. The other 27 are not all fraud. Many are real customers held up by bilingual ID cards, ageing document formats, and capture habits that generic verification engines read as errors. This guide shows operators where those rejections come from and how to close the gap.

Schedule a Cyprus Verification DemoOverview

Cyprus’s first-pass gap is real, and recoverable

Cyprus’s average KYC first-pass rate is 72.90%, and it reaches 98.67% with Shufti on the same applicant traffic. The fraud rate on attempted checks is only 4.90%, so most of the rejection gap is genuine users who can be recovered, not fraud being kept out. The sections below show where the other 27% goes and how each loss is closed.

The Market Context

Why do Cyprus rejections cost more than they look?

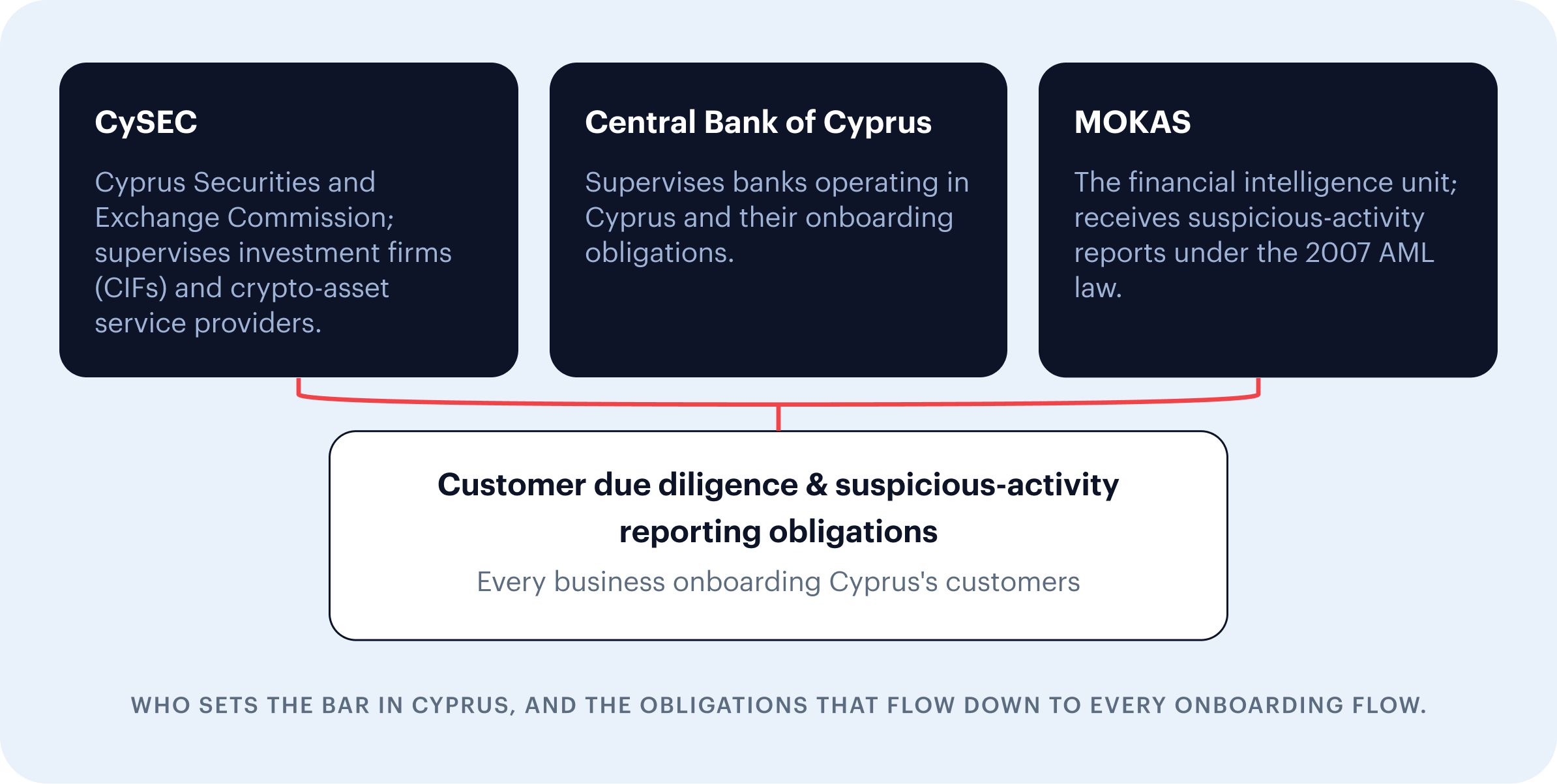

A rejected check in Cyprus usually means a lost cross-border account, not a blocked fraudster. The island runs a small market with outsized onboarding volume, hosting one of the European Union’s larger populations of licensed investment firms plus a growing roster of crypto-asset service providers, and both live on international customer flows.

Cyprus Investment Firms are supervised by the Cyprus Securities and Exchange Commission, banks answer to the Central Bank of Cyprus, and suspicious activity reporting runs through the financial intelligence unit, MOKAS, under the 2007 anti-money laundering law. Identity in Cyprus is recorded in Greek and rendered in English, so documents arrive in mixed scripts and across two generations of design at once.

Coming next: EU AMLA direct supervision of selected entities from 2028.

That supervision is about to tighten. Selected obliged entities move under the EU Anti-Money Laundering Authority for direct supervision from 2028, and crypto firms are completing their move to full authorisation under the EU markets-in-crypto-assets rules. A 72.90% first-pass rate is workable today. It looks expensive once every rejected applicant is a manual review, a delayed deposit, or a customer who never comes back.

Where Pass Rates Leak

Why does one in four good users get stuck in Cyprus?

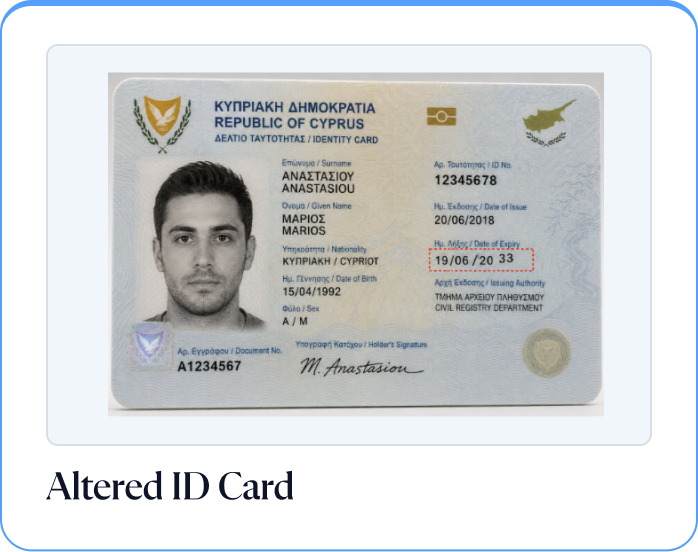

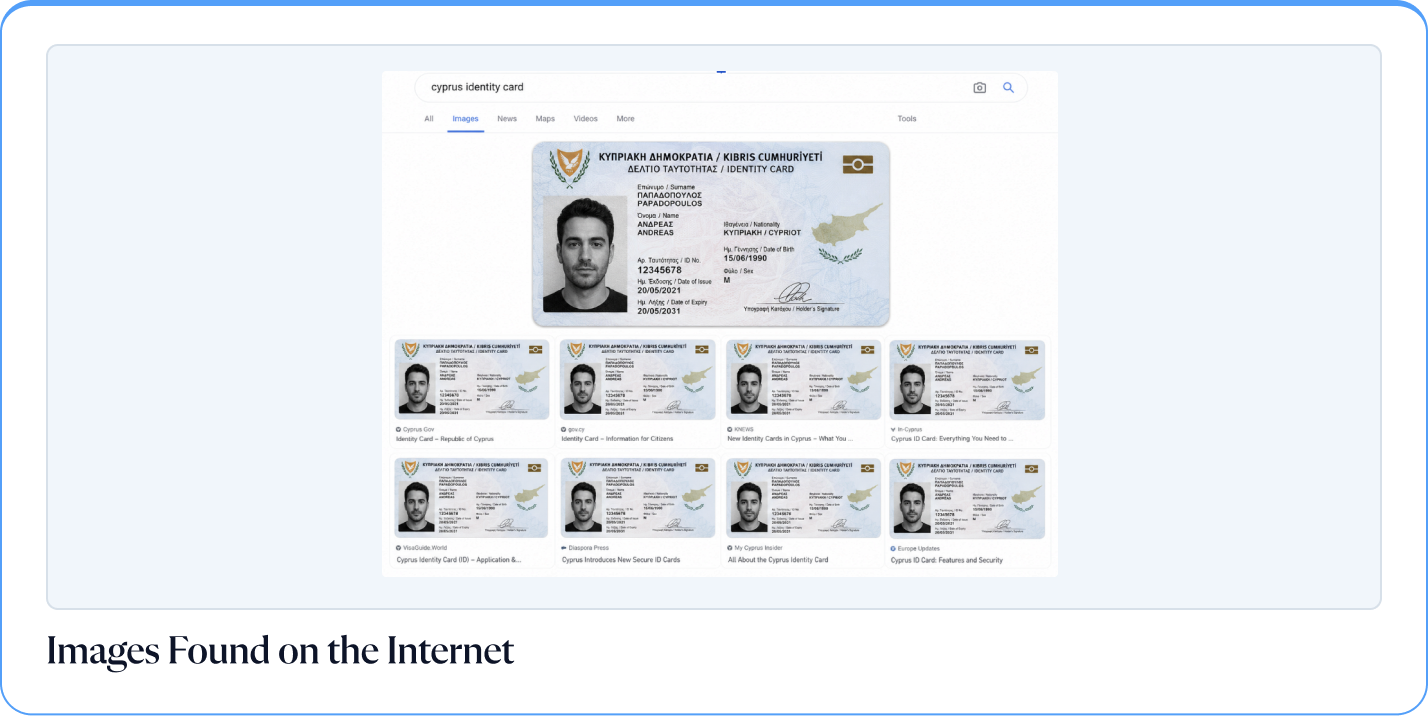

Most Cyprus rejections are not fraud. They fall into two groups, the structural quirks of Cypriot identity documents and the way people capture and submit them. The three reasons that show up most often in declined checks, a screenshot instead of a live capture, an altered document, and an image already found on the internet, sit across both groups. Here are the five causes and what drives each.

The cost lands quickly. Investment firms, banks, and crypto platforms onboard a cross-border base under bank-grade due diligence, so every first-attempt failure either pushes a genuine customer toward a competitor or into a manual review queue.

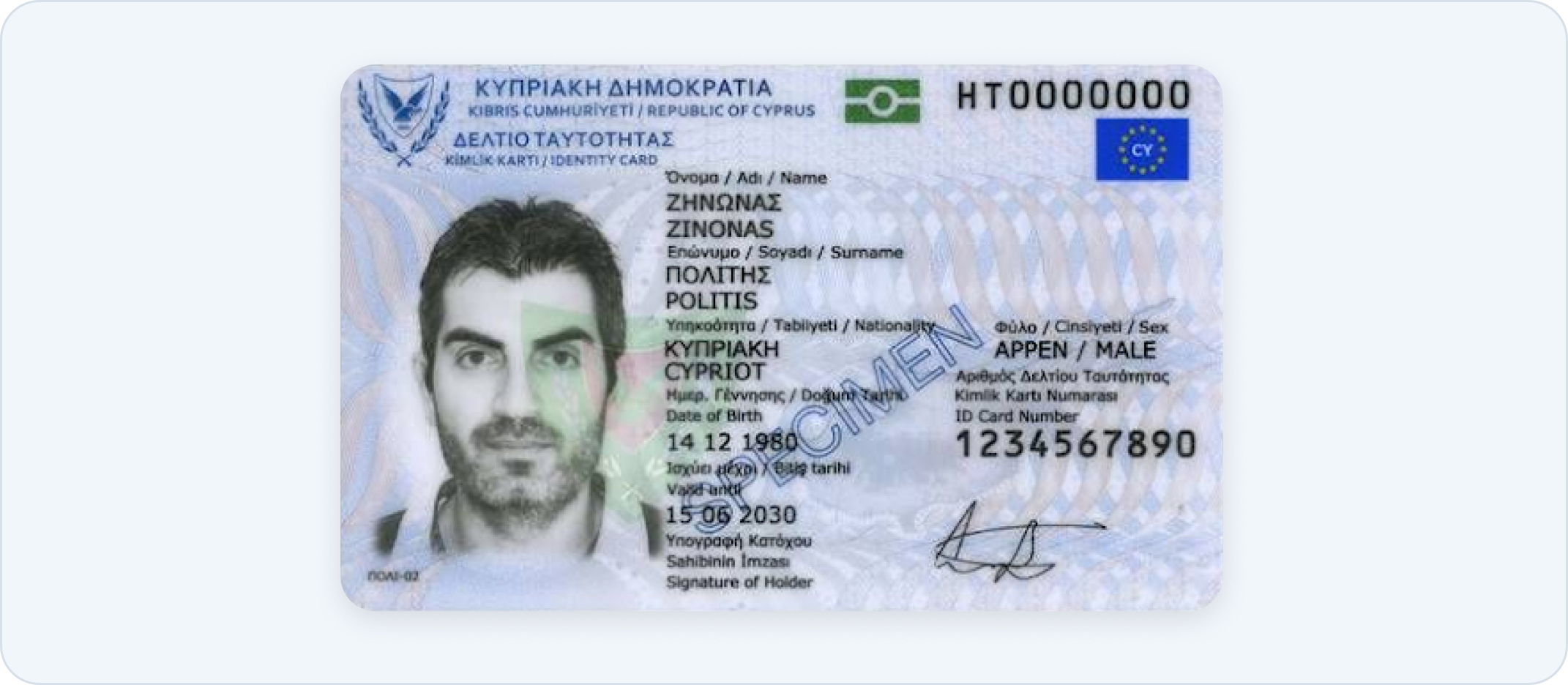

Multilingual text and mixed character sets

Key fields on Cyprus ID cards and passports are routinely printed in both Greek and Latin characters, because identity is recorded in Greek and rendered in English for cross-border use. An OCR engine without specialised multi-script training merges these distinct alphabets into one string, which corrupts the extracted text or makes it fail to match against Latin-only registries and watchlists.

Transliteration adds a second problem. A Greek name can be rendered more than one way in Latin, so when both versions sit in close proximity the engine struggles to separate the localised name from the standardised English one. The same person reads as two identities, which drives needless false positives in AML and sanctions screening.

High variation between legacy and modern formats

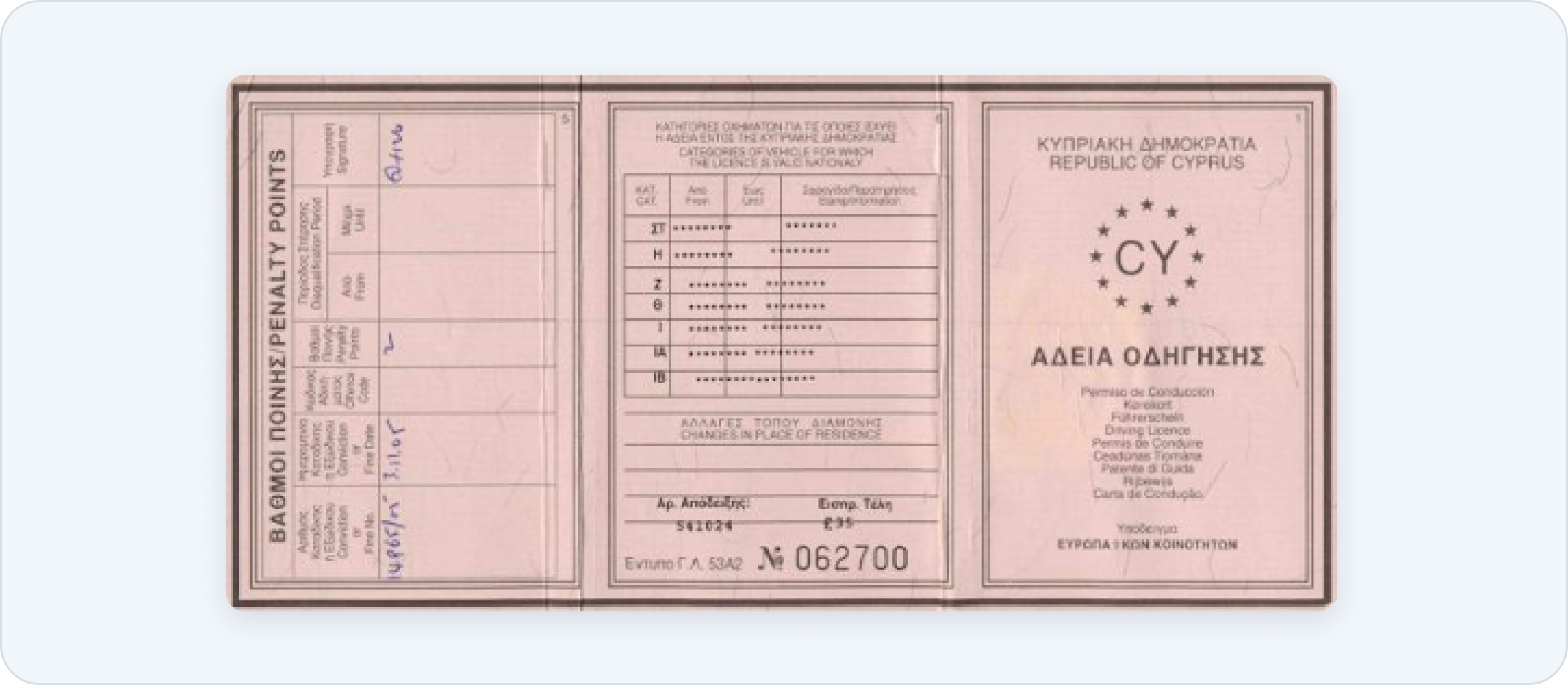

A Cyprus verification engine has to support two generations of documents at once for years to come. EU-standard biometric ID cards with an embedded chip have been issued since August 2020, and under EU Regulation 2019/1157 the older non-compliant national IDs stay valid until they expire or until 3 August 2031, whichever comes first. Older paper driving licences run even longer, with some valid until 2033.

Those older formats are exactly the ones that fail capture. Paper-based Cypriot driving licences degrade fast, with crumpled edges, fading ink, and tearing that wreck OCR readability and trigger poor-document-quality rejections.

Older laminated national ID cards carry the opposite problem. Thick lamination throws extreme glare and reflections under a phone camera, and that glare frequently hides key data points like the document number or date of birth, so the extraction comes back incomplete.

Extraction challenges and field proximity

Essential data on Cypriot documents, including issuance details and dual-language names, is printed in extremely close proximity with no clear machine-readable delimiters. Without localised layout awareness, the engine misclassifies adjacent fields. It maps an issuance date as a date of birth, or appends a stray character from the neighbouring field onto the holder’s name. Either error breaks the downstream match against the applicant’s typed input and ends in a decline, even though the document is genuine.

Vulnerability in older document generations

The newest Cypriot cards are hard to forge. The legacy ones are not. Older versions of the Cyprus ID and driving licence lack modern security features like dynamic holograms, optically variable ink, and embedded microchips, which makes them prime targets for basic spoofing, physical tampering, and photo-substitution attacks that bypass standard visual checks. A verification engine that only checks whether text extracts cleanly will pass these forgeries, because there is no dynamic security feature to test. These are the same documents behind the altered and found-on-the-internet rejection flags.

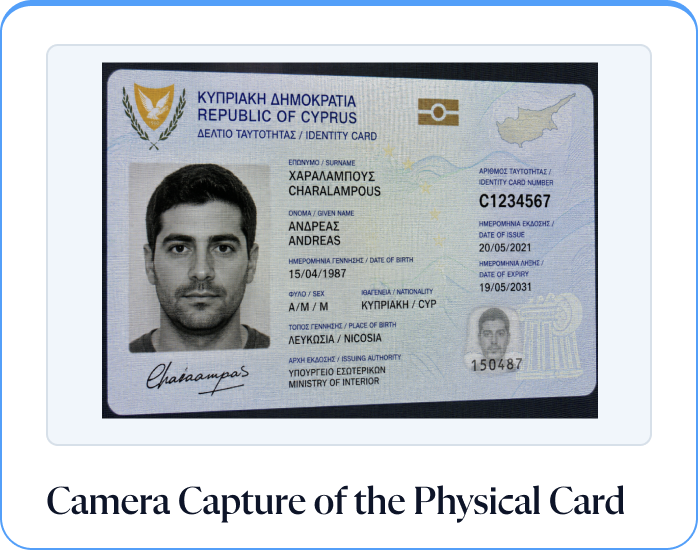

Capture habits and document reuse

The three most common rejection reasons in Cyprus, a screenshot, an altered document, and an image found on the internet, are about how a document is submitted as much as the document itself. People photograph a screen that shows the ID, upload a saved screenshot, or reuse an image that already exists online. A verification engine reads the screen glare, the compression, or the prior provenance as tampering or poor visibility and declines it. Some of these are genuine users taking a shortcut, and some are fraud attempts recycling a leaked image, so a check that cannot tell a live capture from a recycled one rejects both.

The top three Cyprus rejection reasons are capture and reuse problems, not document defects.

None of these are exotic. They are the daily reality of verifying a bilingual, document-transitional market through a phone camera. A rejected genuine applicant either abandons onboarding or lands in a manual review queue, and every case in that queue costs analyst time and slows the customer down. A high first-attempt failure rate is a revenue and staffing problem before it is ever a compliance one.

Close the gaps that pull Cyprus pass rates down

Each failure point above has a matching control. The Cyprus page shows how document verification, liveness and AML screening cover them for CySEC-regulated onboarding.

Explore Shufti for CyprusHow does Shufti move Cyprus from 72.90% to 98.67%?

Shufti raises the Cyprus first-pass rate from 72.90% to 98.67% on the same applicant traffic by fixing the document problems above instead of pushing them to manual review. The platform runs on fully owned technology across OCR, document intelligence, liveness, and AML screening, tuned for hard markets rather than clean Western templates.

Liveness-guided, blocks screen-in-screen.

Greek and Latin in one pass.

Maps crowded fields by meaning.

Face liveness and chip read.

Sanctions, PEP, adverse media.

Reading documents in both Greek and Latin script

Shufti’s in-house OCR is trained on multi-script documents and supports more than 150 languages across 10,000+ document types, so a Cypriot card printed in Greek and Latin reads as one record, not a merged string. The engine keeps the Greek field and the Latin transliteration as distinct, linked values, which removes the duplicate-identity false positives that hit watchlist screening. Document verification handles the extraction.

Accepting legacy formats without waving through forgeries

Shufti reads the full Cyprus spread, from a 1990s laminated card to a 2020 biometric one, and reads the chip directly through NFC verification where it exists. Glare correction and quality handling rescue captures that generic engines reject as poor quality, while document intelligence still flags real tampering. iBeta Level 3 conformance liveness checks confirm a present, live person, so a screenshot, a screen-on-screen capture, or an image pulled from the internet is caught rather than onboarded.

Parsing crowded bilingual fields correctly

Context-aware field mapping reads Cypriot layouts by meaning, not by fixed coordinates, so an issuance date stays an issuance date and a name keeps its own characters. That single correction removes a large share of the date and name errors that otherwise break the match against an applicant’s typed details and trigger a needless decline. Cleaner extraction also feeds electronic identity verification against authoritative data.

Meeting Cyprus’s AML bar

Accurate name parsing is what makes screening trustworthy. Shufti runs sanctions, politically exposed person, and adverse-media watchlist screening on a correctly structured identity, so Cypriot and transliterated Greek names are matched once and matched right, instead of generating repeat false positives that bury analysts in review.

What higher pass rates are worth

Each recovered first-pass check is a customer who funds an account today and an applicant who never reaches a manual queue. A move from 72.90% to 98.67% turns nearly 26 of every 100 previously rejected attempts into completed onboardings, the difference between an onboarding funnel that leaks and one that converts. Shufti runs on proprietary AI across documents from 240+ actively processed countries and territories, so a single configuration covers Cypriot citizens, residents, and the cross-border base that investment and crypto firms onboard. Teams comparing volumes and tiers can review the options on the pricing page.

Which Cyprus Document Problems Lower Pass Rates, and How Are They Fixed?

Five problems explain most of Cyprus’s first-pass gap: bilingual Greek and Latin cards, the mix of legacy paper and laminated IDs with 2020 biometric cards, crowded fields with no delimiters, weak security on older generations, and capture habits like screenshots and reused images. Each maps to a specific Shufti control, and together they move the first-pass rate from 72.90% to 98.67%.

What fails today

Merged strings, transliteration false positives.

How Shufti resolves it

Multi-script OCR keeps both fields linked and distinct. Clean match, fewer AML false hits.

What fails today

Glare, fading, poor-quality rejections.

How Shufti resolves it

Reads all formats, NFC chip read, glare correction. Old and new cards both pass.

What fails today

Issuance date read as DOB, stray characters on names.

How Shufti resolves it

Context-aware field mapping by meaning. Correct fields, no needless decline.

What fails today

Photo-substitution and tamper slip through.

How Shufti resolves it

Document intelligence with Level 3 liveness. Forgeries caught, real users pass.

What fails today

Screenshots, screen-on-screen, and web images read as tampering.

How Shufti resolves it

Liveness-guided capture and Level 3 face liveness. Live users pass, recycled images caught.

Certifications

Independently audited and certified for enterprise-grade security and data protection.

Frequently Asked Questions

Most verification stacks assume a single national alphabet, a few document formats, and one or two regulators per country. APAC breaks all of those at once. Names appear in Latin, Devanagari, Khmer, Burmese, Thai, Hangul, Chinese, Japanese, Urdu and Cyrillic scripts; date and address conventions vary; and regulators issue new technical mandates each quarter. A stack built for one market rarely survives expansion into three or four.

Because most rejections are not fraud. A large part of the gap comes from bilingual Greek and Latin cards, ageing paper and laminated documents, and capture habits like screenshots that generic engines misread as errors. The fraud rate on attempted verifications is only 4.90%, far smaller than the rejection gap.

Cyprus uses EU-standard biometric ID cards issued since August 2020, older laminated national ID cards that stay valid until expiry or 3 August 2031, the Cypriot passport, and driving licences that range from modern EU photocards to older paper versions valid in some cases until 2033. A verification flow has to accept all of these at once.

The most common causes are glare from thick lamination, fading or creasing on paper documents, dual-language Greek and Latin fields that a generic engine maps to the wrong place, and submitting a screenshot or a photo of a screen instead of a live capture. These produce poor document quality and data-mismatch declines even when the document and the person are real.

Cyprus prints names in both Greek and Latin script on the same card. Engines without multi-script training merge the two into a single garbled value or fail to separate first and last names, and transliteration variants make one person read as two identities, which causes mismatches and false positives during AML and sanctions screening.

Turn rejected Cypriot applicants into funded accounts

See how Shufti reads every Cyprus document, old and new, and moves your first-pass rate from 72.90% to 98.67%.