Banks spent the last decade treating document verification as the anchor of customer onboarding. A passport photograph, a selfie, a match. The approach held up until the fraud tooling around it changed.

Synthetic identities don’t arrive with doctored passports. They’re assembled from real data fragments, fabricated credit trails, and AI-generated biometric proxies. The Deloitte Center for Financial Services projects synthetic identity fraud will generate at least $23 billion in losses by 2030. That projection accounts for the fact that generating a convincing synthetic identity now costs less than a monthly subscription.

Meanwhile, the eIDAS 2.0 regulation requires EU member states to provide digital identity wallets to citizens by November 2026, and large enterprises in regulated sectors must accept those credentials by December 2027. Banks serving European customers face a compliance deadline that is now months away.

This piece examines what those shifts mean for electronic identity verification in banking and what a practical verification architecture looks like going forward.

Three forces reshaping eIDV in banking right now

Regulatory deadlines have moved from the horizon to the calendar. The eIDAS 2.0 framework entered force in May 2024. The EU Council’s adoption of the digital identity framework creates a concrete obligation for banks onboarding EU customers to accept and verify digital identity wallet credentials. Banks that wait for the hard deadline before testing the integration will spend 2027 in remediation.

PSD3 is also changing what identity means in financial services. The revised payment services framework requires banks to share customer data through standardised APIs. Every cross-platform transaction carried over open banking infrastructure depends on identity checks that were done upstream. Without a reliable verified identity layer, the whole model is only as trustworthy as the weakest onboarding decision in the chain.

Banking fraud has also moved to the front of the onboarding flow. Banks running static document checks as their primary defence are checking the wrong asset. The fraud surface is now at account opening, not after it. Early adopters of wallet-based eIDAS 2.0 onboarding are already reporting 40 to 60 percent reductions in abandonment rates. The long-held assumption that more security requires more friction is breaking down.

How eIDV architecture is evolving for banking

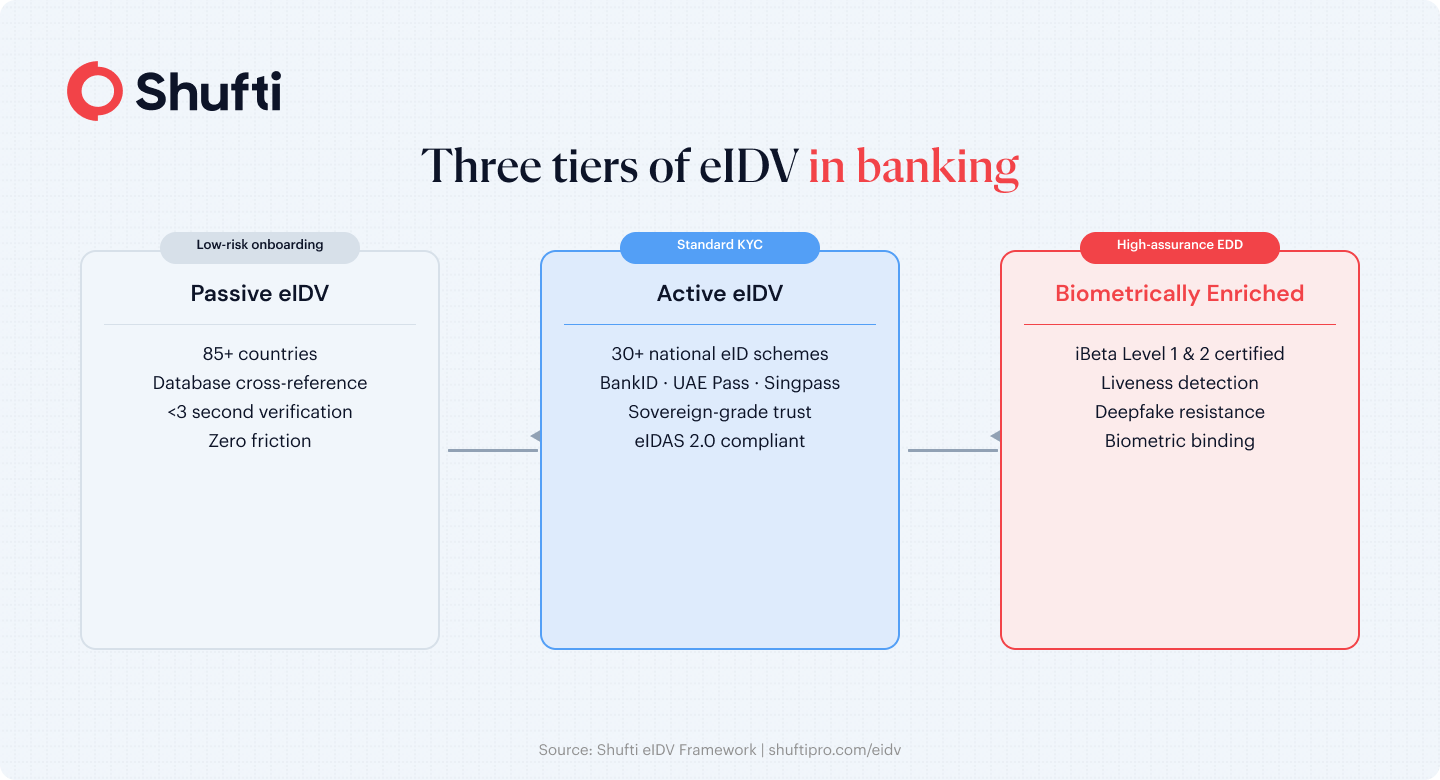

Document checks verify the document. Database checks verify the person. These two approaches are not interchangeable, and the banking sector is drawing that distinction at scale for the first time.

Passive eIDV cross-references the data a user provides (name, date of birth, address) against national registries, credit bureaus, and telecom records in real time. There is no document upload, no selfie requirement. The user is checked against an authoritative source while completing the form. For standard-risk onboarding, this removes the main friction point without weakening the verification quality.

Active eIDV raises the assurance level by routing authentication through sovereign identity systems, including national digital IDs, government-issued wallets, and bank-confirmed credentials like BankID in the Nordics, UAE Pass in the Gulf, or Singpass in Singapore. The identity is not checked against a database. The issuing authority confirms it in real time. For banks thinking through eIDAS 2.0 readiness, the wallet interaction is the verification event.

Biometrically enriched eIDV adds a certified liveness layer on top of the database confirmation, binding the physical person to the verified data record. Liveness checks certified to iBeta Level 1,2 and Level 3 standards analyse depth signals and physiological cues that AI-generated faces cannot reproduce reliably. This layer is where deepfake threats get absorbed before reaching the core verification result.

The three-tier structure reflects how banks are actually built. Each tier handles the verification scenarios that the previous tier cannot, and together they cover the range from frictionless pre-screening to high-assurance onboarding without requiring separate vendor contracts for each level.

What durable eIDV for banking requires

Banks and fintechs operating across regions routinely manage separate verification vendors per country. The gaps appear at the handoff points between those vendors, and at the edge cases each one doesn’t cover. A verification layer covering 85 or more countries through a single API removes those gaps. eIDAS 2.0 compliance for European customers and Aadhaar-linked verification in India become two configurations of the same system, not separate procurement decisions.

The assurance level also needs to match the transaction risk. A returning customer completing a low-value transfer requires a different verification depth than a new customer applying for a credit facility. The three tiers described above (passive, active, biometrically enriched) should be modes of a single banking identity platform, not separate products requiring separate integrations.

Banks under national data residency rules present a requirement that often doesn’t surface until late in the procurement process. Customer verification cannot be routed through third-party cloud infrastructure when institutions serve government-adjacent clients or operate under strict data sovereignty obligations. A verification platform without on-premises or hybrid deployment support is disqualified before the RFP closes.

What to expect from eIDV in banking by 2030

Digital identity wallets will not replace database verification. They address different things. Sovereign credentials confirm the government’s assertion about an identity. Database checks confirm the current state of the underlying data record. The two layers work together in a tiered architecture, not in competition.

Decentralised and blockchain-anchored identity records reduce the risk of record tampering after the fact, but they cannot validate whether the original enrolment data was accurate. A fraudulent identity enrolled before it reaches a ledger carries that inaccuracy forward permanently. The quality of the initial verification still determines everything downstream.

Quantum computing poses a longer-horizon challenge to the cryptographic protocols underlying digital signatures and secure data transmission. Regulators, including the EU Anti-Money Laundering Authority, are beginning to assess quantum readiness standards. Verification architectures that layer biometric and database-based checks alongside cryptographic methods carry lower exposure because the biometric layer does not depend on the same encryption stack that quantum computing could compromise. Banks’ building verification depth is now better positioned regardless of how quantum regulation lands.

Banking compliance teams managing this much regulatory change while facing more sophisticated fraud need a verification layer that handles both, not one that sacrifices security for conversion or vice versa. Shufti’s eIDV platform covers passive database checks, active sovereign eID authentication, and biometrically enriched liveness verification across 85-plus countries through a single API. Request a demo to map the three verification tiers against your specific onboarding flows.

Frequently Asked Questions

Will biometric verification completely replace passwords in banking by 2030?

Biometrics will replace document uploads as the primary high-assurance check in most regulated markets, but passwords and PINs will persist for returning-user low-risk sessions. The consequential shift is biometrics displacing manual document review, not passwords.

How will open banking regulations shape the future of eIDV in financial services?

PSD3 requires banks to share customer data through standardised APIs. Identity checks will need to produce portable, signed attestations that downstream platforms can reference, rather than requiring a full re-verification at each integration point.

Can blockchain-based identity verification eliminate fraud in banking permanently?

Blockchain can guarantee the integrity of an identity record after enrolment, but it cannot validate whether the original data was accurate. A synthetic identity enrolled before the record reaches a ledger carries that inaccuracy forward.

How will eIDV systems adapt as synthetic identity fraud becomes more advanced?

The adaptation is already happening. Verification is shifting from document checks to cross-referencing multiple independent data sources simultaneously, with biometric binding certified against current deepfake attack patterns added on top. Each additional independent source a synthetic identity must fool reduces its success rate.

How will quantum computing affect the security of electronic identity verification in banking?

Quantum computing threatens cryptographic protocols underlying digital signatures and secure data transmission. Verification architectures that layer biometrics and database checks alongside cryptographic methods carry more resilience, since the biometric layer does not depend on the encryption stack that quantum computing could compromise.