TL;DR

- Customer identity verification confirms a user is real and who they claim, at onboarding.

- It uses documents, biometrics, and database checks, ending in an accept or reject decision.

- It is legally required across banking, fintech, iGaming, crypto, and insurance.

- It is the first step of KYC, not the whole compliance process.

- Account takeover and identity fraud rose 244% in 2025, raising the stakes.

A new customer reaches your sign-up screen. Before they move money, place a bet, or access sensitive data, you have one chance to confirm they are a real person who is who they claim to be. That confirmation is customer identity verification, and getting it wrong is expensive. Account takeover and identity fraud incidents rose 244% in 2025 as generative AI made fake identities easier to produce (Biometric Update, June 2026). This guide explains what customer identity verification is, how the process works, the methods involved, who is legally required to do it, and the challenges teams run into. It is written for the onboarding, compliance, and fraud teams who own the decision.

What is customer identity verification?

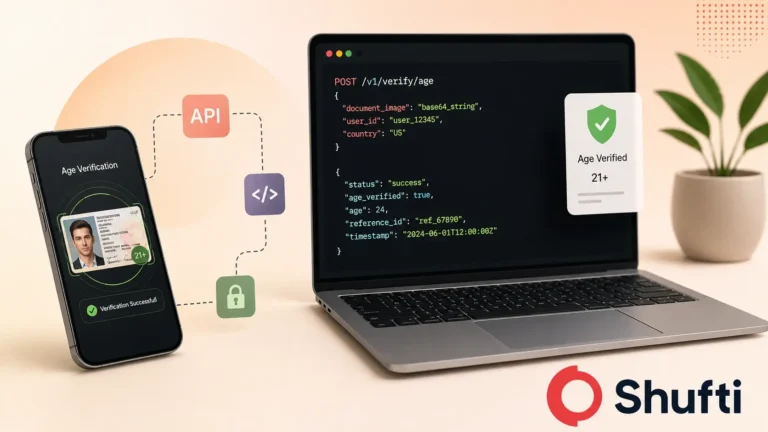

Customer identity verification is the process of confirming that a customer is a real, live person who matches the identity they present, using documents, biometrics, or authoritative database checks. It happens at onboarding, before the customer gains access to a regulated product, and again at risk-trigger events such as a large transaction or a change of account details. The output is a decision: accept, reject, or refer to a human reviewer. Depending on the sector, the same process is called client identity verification or user identity verification, but the goal is identical, confirming a genuine person sits behind the application.

There is an important distinction between verifying a new customer and re-verifying an existing one. Verifying a new customer establishes identity from scratch, proving the person behind the application is genuine. Re-verifying an existing customer confirms the person returning is the same one you onboarded, usually triggered by a risk event rather than routine login. The first answers “is this person real?” The second answers “is this still the same real person?” Both sit inside the broader complete guide to identity verification that governs regulated onboarding.

The customer identity verification process

The customer verification process runs as a five-step flow that moves from data capture to a logged decision in seconds. Each step closes a gap the previous one leaves open, and the audit record produced at the end is what proves to a regulator that verification actually happened.

First, the customer captures their identity evidence, typically a photo of a government-issued document plus a live selfie or short video. Second, forensic checks authenticate the document by reading its machine-readable zone, NFC chip where present, and security features. Third, a biometric step matches the live face to the document photo and runs liveness detection to confirm a real person is present rather than a photo or deepfake. Fourth, the verified identity is cross-checked against authoritative databases and, where AML rules apply, sanctions and watchlist sources. Fifth, the system returns an accept, reject, or refer decision and logs every check into an auditable record. Strong identity document verification at the second step is what catches manipulated documents that a basic photo match would pass.

Methods used in customer identity verification

There is no single method that fits every customer, market, or risk level, so most onboarding flows layer two or more. The table below compares the four core methods plus the step-up triggers that decide when to escalate. Reading them side by side shows why a single check rarely holds up against a determined fraudster.

| Method | What it does | When to use it |

| Document verification | Authenticates a government ID and reads its security features | Default for most onboarding where a document is available |

| Face verification | Matches a live selfie to the document photo with liveness detection | Remote onboarding and higher-fraud channels |

| Electronic IDV (eIDV) | Checks identity data against authoritative databases | Markets with strong civil registries or national digital IDs |

| KYC database check | Screens the identity against sanctions, PEP, and watchlists | AML-regulated relationships and risk screening |

| Step-up triggers | Adds checks when risk signals appear mid-session | High-value transactions, mismatched data, anomalous behaviour |

The pattern is consistent. Documents prove the credential, biometrics prove the person, electronic checks prove the identity exists, and screening proves the customer is not a sanctioned or high-risk actor. Layering them means no single point of failure decides who gets through.

Who is required to verify customer identity?

Any business that provides a regulated financial, gambling, or high-trust service is legally required to verify customer identity, with the specific obligation set by sector. The requirement traces back to global anti-money-laundering standards and is enforced through national law.

Banks and lenders operate under national AML laws built on the Financial Action Task Force standard, which requires customer due diligence at account opening (FATF Recommendations, updated October 2025). Fintech and neobanks carry the same AML duties plus, in the EU, the European Banking Authority’s remote onboarding guidelines that make liveness mandatory for unattended verification. iGaming operators must verify both identity and age under licensing regimes. Crypto exchanges and virtual asset service providers are bound by FATF’s travel rule and national VASP registration before transactions. Insurance firms verify identity to prevent policy and claims fraud. Across all of them, verification is the precondition for operating legally, and the AML dimension is covered in depth under AML identity verification.

Customer identity verification vs KYC

Customer identity verification is one step inside Know Your Customer (KYC), not a synonym for it. Verification proves who the customer is at a point in time. KYC is the wider, ongoing compliance programme that starts with verification and adds risk assessment, AML screening, and continuous monitoring throughout the relationship.

The practical difference matters for how teams build their stack. Verification is a discrete event with a clear pass or fail. KYC is a lifecycle obligation that never fully closes, because a customer who was low-risk at onboarding can become high-risk later. Treating verification as if it were the whole of KYC is a common compliance gap, since it leaves the monitoring and re-screening duties unaddressed after the account opens.

Common challenges in customer identity verification

Even well-resourced teams hit four recurring challenges in customer identity verification, and each one trades off against the others. Solving for fraud tends to add friction, and solving for friction tends to add fraud, which is why the balance is hard.

The first is onboarding friction. Every extra step costs conversion, and genuine customers abandon flows that feel slow or intrusive. The second is document fraud, now amplified by generative AI that produces convincing fake and manipulated documents at scale. The third is global coverage gaps, where a provider reads documents well in some markets but fails in others, blocking legitimate customers in the regions a business most wants to grow. The fourth is the false rejection rate, where overly strict checks turn away real people, quietly costing revenue every day they run. The teams that handle these well measure all four together rather than optimising one in isolation.

How Shufti handles customer identity verification

If your customers are in Vietnam, Indonesia, Brazil, South Asia, or the Gulf, you have probably watched good users fail verification that should have passed. Most vendors trained their models on Western documents and retrofitted the rest, so pass rates drop in exactly the markets where you want growth. Shufti built and owns its full verification stack, with document intelligence trained on 10,000+ document types across 240+ countries and proprietary OCR reading 150+ languages natively. Document, biometric, and database checks run in one auditable flow, and the liveness engine holds iBeta Level 3 conformance under ISO/IEC 30107-3, so the same integration that onboards a customer in London works for one in Jakarta.

See how Shufti runs customer identity verification across document and biometric checks in one integration — book a demo.

Frequently Asked Questions

What is customer identity verification?

Customer identity verification is the process of confirming that a customer is a real, live person matching the identity they present, using documents, biometrics, or database checks. It happens at onboarding and at risk-trigger events, returning an accept, reject, or refer decision before the customer accesses a regulated product.

Is customer identity verification the same as KYC?

No. Customer identity verification is the first step within Know Your Customer (KYC). Verification proves who the customer is at onboarding, while KYC is the wider, ongoing programme that adds risk assessment, AML screening, and continuous monitoring throughout the customer relationship.

What information is needed for customer identity verification?

Typically a government-issued document such as a passport, national ID, or driver's licence, plus a live selfie or short video for biometric matching. Depending on the market and risk level, providers may also check identity data against authoritative databases and sanctions or watchlist sources.

How do businesses verify customer identity remotely?

Businesses verify customer identity remotely by having the user capture their document and a live selfie, then running automated document authentication, biometric face matching, and liveness detection, followed by a database cross-check. EU rules under the EBA remote onboarding guidelines make liveness detection mandatory for unattended remote verification.

What happens if customer identity verification fails?

A failed verification is usually routed to a human reviewer or asked to retry, rather than rejected outright, since many failures come from poor image capture rather than fraud. Genuine customers can re-attempt with a clearer document or better lighting, while flagged high-risk cases are escalated for compliance review.