Face Verification

Face Verification

Address Verification

Address Verification

Document Verification

Document Verification

Age Verification

Age Verification

VideoIdent

VideoIdent

Fast ID

Fast ID

eIDV

eIDV

Consent Verification

Consent Verification

NFC Verification

NFC Verification

Business Verification

Business Verification

Due Diligence

Due Diligence

Investor Verification

Investor Verification

E-Signature

E-Signature

QES

QES

AML Screening

AML Screening

Transaction Monitoring

Transaction Monitoring

Adverse Media

Adverse Media

Business AML Screening

Business AML Screening

PEP & RCA

PEP & RCA

Sanctions

Sanctions

Watchlist

Watchlist

Behavioural Biometrics

Behavioural Biometrics

Device Fingerprinting

Device Fingerprinting

Biometric Face Authentication

Biometric Face Authentication

MFA

MFA

Fraud Hub

Fraud Hub

Onboarding

Onboarding

Ongoing Monitoring

Ongoing Monitoring

KYC

KYC

KYB

KYB

KYI

KYI

Age Assurance

Age Assurance

Identity Verification

Identity Verification

Workforce IAM

Workforce IAM

Candidate Verification

Candidate Verification

Compliance

Compliance

Fraud prevention

Fraud prevention

Trust & safety

Trust & safety

Global expansion

Global expansion

Product Managers

Product Managers

Compliance Officers

Compliance Officers

Fraud Analysts

Fraud Analysts

Developers

Developers

Deepfake

Deepfake

Bonus Abuse / Promotion Abuse

Bonus Abuse / Promotion Abuse

Account Takeover

Account Takeover

Synthetic Identity Fraud

Synthetic Identity Fraud

Document Fraud

Document Fraud

Impersonation Fraud

Impersonation Fraud

Multi-Accounting

Multi-Accounting

Fraud Networks

Fraud Networks

Chargeback Fraud

Chargeback Fraud

Money Mule Activity

Money Mule Activity

Party Fraud

Party Fraud

Regulatory & Compliance Risks

Regulatory & Compliance Risks

Fintech

Fintech

Crypto

Crypto

iGaming

iGaming

Forex

Forex

Social Network

Social Network

Marketplace

Marketplace

Banking

Banking

Gig Economy

Gig Economy

Blind Spot Audit

Blind Spot Audit

Deepfake Detector

Deepfake Detector

Liveness Spoofs

Liveness Spoofs

Document Originality

Document Originality

Document Deepfake

Document Deepfake

Global Trust Platform

Global Trust Platform

Journey Builder

Journey Builder

Case Management

Case Management

Shufti AI

Shufti AI

Fraud Analytics

Fraud Analytics

Vendor Comparison

Vendor Comparison

Brand Personalisation

Brand Personalisation

IDV Modes

IDV Modes

AI Compliance Co-Pilot

AI Compliance Co-Pilot

OCR

OCR

Secure Capture

Secure Capture

Deployment Options

Deployment Options

Identity Methods

Identity Methods

API Documentation

API Documentation

Mobile SDKs

Mobile SDKs

Service Status

Service Status

Help Center

Help Center

Contact Us

Contact Us

Technical Support

Technical Support

Supported Documents

Supported Documents

Content library

Content library

Blogs

Blogs

News

News

Reports

Reports

Insights

Insights

Knowledgebase

Knowledgebase

ROI calculator

ROI calculator

About

About

Career

Career

Press Release

Press Release

Certifications

Certifications

Partnership

Partnership

Awards

Awards

Events & Webinar

Events & Webinar

Interactive Demo

Interactive Demo

Podcast Studio

Podcast Studio

Spotlight Studio

Spotlight Studio

Online eIDV Solutions: How Businesses Verify Customers Without Physical Documents

- 01 Why document-based onboarding is breaking under its own weight

- 02 How online eIDV actually works

- 03 Regulatory standing of database-level verification

- 04 Preventing identity spoofing in document-free verification

- 05 Coverage in markets with poor document infrastructure

- 06 What happens when a customer won't engage with verification

Every friction point in your onboarding flow has a cost. A document upload prompt that times out, a photo capture that fails in poor lighting, an address form that rejects international postcodes, each one chips away at the conversion rate you worked hard to build.

Online eIDV solutions, electronic identity verification systems that check identity against authoritative data sources rather than requiring document uploads, are one of the most direct answers to this problem. They’re also fast becoming a regulatory expectation. Under eIDAS 2.0 (EU Regulation 2024/1183), every EU member state must provide citizens with a digital identity wallet by December 2026, and regulated private-sector entities must accept them from 2027. Businesses that aren’t thinking about document-free verification now will be reacting under pressure in twelve months.

This article explains how online eIDV works, what verification approaches are available, how to match the right tier to your risk level, and which compliance frameworks give database-level verification a green light. It also addresses the questions compliance teams most frequently raise when considering a move away from document-centric onboarding.

Why document-based onboarding is breaking under its own weight

The standard onboarding flow, photograph a document, submit a selfie, wait for a match, made sense when identity fraud was relatively unsophisticated. It no longer maps well to the threat and user-expectation environments of 2026.

A workflow that relies on inspecting document photos is not more secure than one that cross-references government-held identity records; it’s often less secure, because the attack surface is a JPEG rather than a live database query.

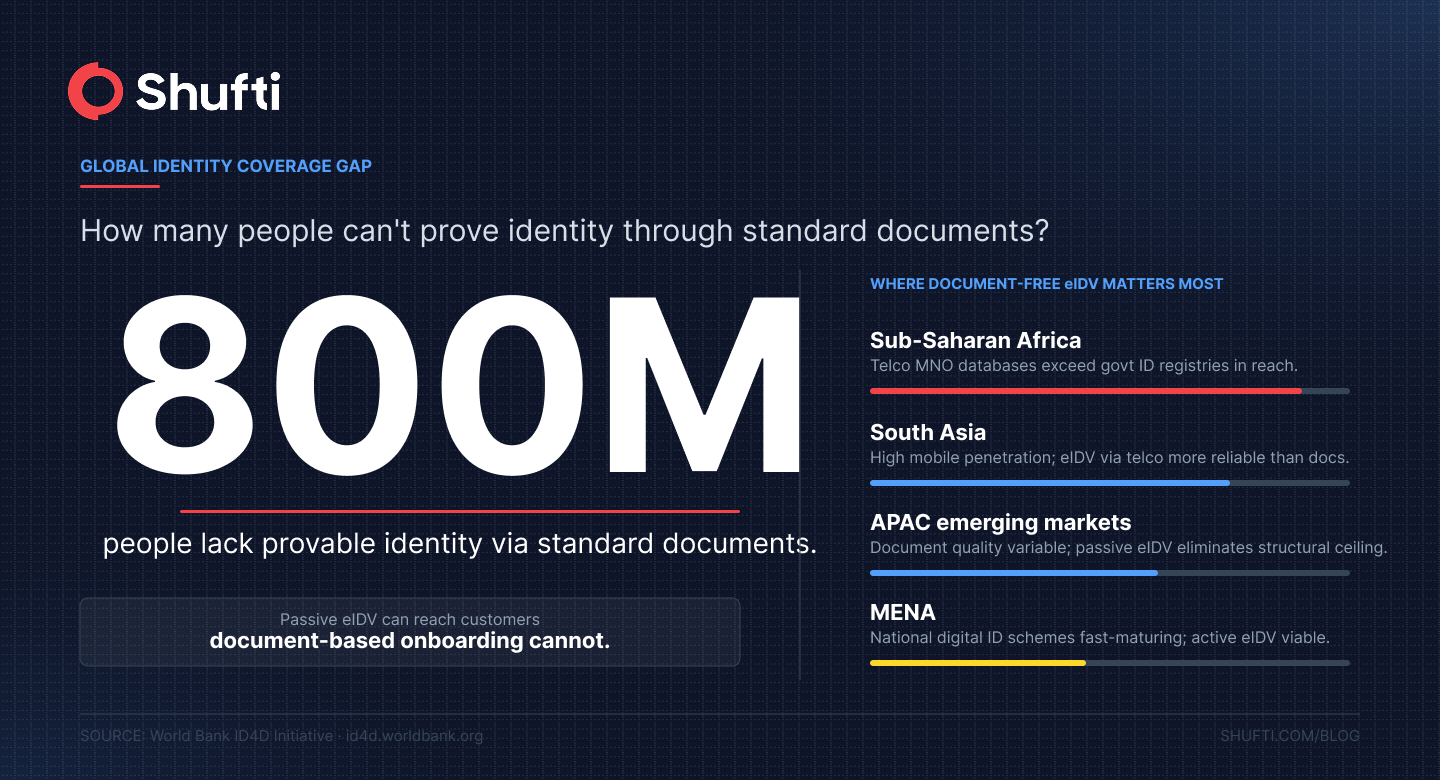

On the user side, the World Bank’s ID4D dataset estimates that more than 800 million people worldwide cannot prove their identity through standard documents, with the majority in Sub-Saharan Africa and South Asia. For platforms operating in APAC, MENA, or Africa, document upload isn’t just friction; it actively excludes a significant portion of the addressable market.

How online eIDV actually works

Electronic identity verification works by querying structured, authoritative data sources, telco records, credit bureau files, government identity registers, electoral rolls, and matching the attributes a user supplies at sign-up against what those sources hold. No document upload required. The check typically completes in under three seconds.

The logic isn’t binary. Most production eIDV deployments layer two or more independent data sources simultaneously, a cross-referencing technique designed to catch synthetic identities (fabricated credentials that no single source will flag as fraudulent because they were never issued as fraudulent). FATF Recommendation 10 explicitly supports a risk-based approach to customer due diligence, which means database-level verification can satisfy the CDD obligation where the risk tier is appropriate; it doesn’t require a physical document if the data cross-reference is sufficiently robust.

The three verification tiers

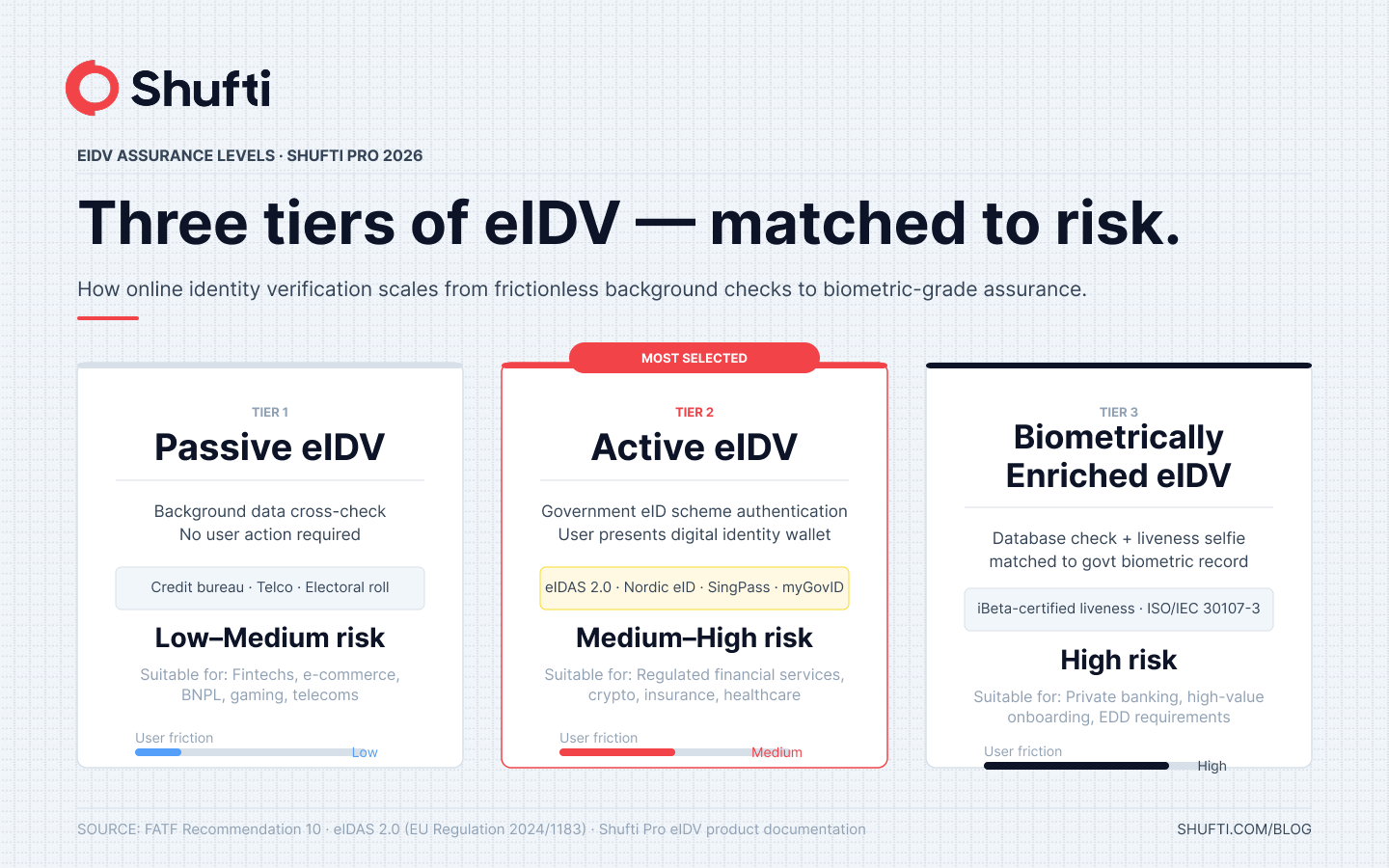

Not every customer or every transaction carries the same risk. Online eIDV solutions that calibrate to risk typically offer three assurance levels:

Passive eIDV

A frictionless background check against commercial and government data sources — credit bureau records, telco subscriber files, electoral rolls, national registries. The user supplies only basic personal data; the system verifies it in the background without any user action. Suited to low-to-medium risk onboarding where the applicant pool is predominantly legitimate. Regulatory audit trails are generated automatically.

Active eIDV

Direct authentication against a national eID scheme — a government-issued digital identity that the user actively presents, typically through a mobile app or a chip-read. These schemes (such as those operating under eIDAS 2.0 in Europe, or established national frameworks in Nordic countries, Australia, and Singapore) carry higher assurance because the government has already identity-proofed the credential holder.

Biometrically Enriched eIDV

A database check combined with a liveness-verified selfie match against the government-held photo on file. This tier is appropriate where regulations demand a high assurance level, regulated financial institutions onboarding high-value customers, for instance, and require iBeta-certified liveness technology to resist deepfake and injection attacks. It produces the same audit trail as a document-based biometric check but without the document upload friction.

Regulatory standing of database-level verification

The admissibility question, whether eIDV outputs are accepted as proof of due diligence in a regulatory audit, depends on jurisdiction and risk classification. Still, the regulatory direction of travel is clearly supportive. FATF Recommendation 10 establishes the risk-based approach as the global standard for CDD: obligated entities must apply measures proportionate to identified risk, and those measures may include electronic verification of identity where appropriate. FATF guidance does not require a physical document check as a universal baseline.

In Europe, eIDAS 2.0 goes further: it creates a legal framework for digital identity wallets that, once issued by a member state, carry the same legal weight as a physical document for any regulated transaction. From 2027, regulated businesses must accept these wallets. Businesses with no eIDV infrastructure in place will face both a compliance gap and a conversion gap when that deadline arrives.

For compliance officers concerned about audit admissibility: the answer is that properly implemented eIDV, with documented data sources, cross-reference logic, and a full audit trail, is defensible and increasingly expected. The risk of a failed audit comes not from choosing eIDV over document checks, but from choosing eIDV without adequate documentation of the sources used, the match thresholds applied, and the risk classification underpinning the decision.

Preventing identity spoofing in document-free verification

The most common objection to document-free verification is spoofing: if there’s no document to inspect, what stops someone from supplying stolen credentials and passing a database check? The answer lies in the combination of data sources and the cross-reference logic applied to them.

A single-source check is relatively easy to spoof: if a fraudster has a victim’s name, date of birth, and address, they might pass a check against a single credit bureau. A dual-source check, cross-referencing a credit bureau against a government electoral roll simultaneously, narrows that attack significantly, because the data sets are maintained independently and updated on different schedules. Synthetic identities that have fabricated a credit profile often haven’t been registered to vote; stolen identities that show on the electoral roll often don’t show consistent address histories on credit files.

Coverage in markets with poor document infrastructure

For platforms operating in markets where document quality is variable, faded text, folded creases, non-machine-readable formats, or where a significant share of the addressable market simply doesn’t carry a national ID, document-centric verification creates a structural conversion ceiling.

The World Bank ID4D data quantifies the scale of this problem: more than 800 million people lack a provable identity through standard documents. In many markets in APAC and Africa, telco subscriber databases and national mobile identity registries are actually more comprehensive than government-issued document registries, which means that passive eIDV against telco sources can reach customers that document-based onboarding cannot.

For teams evaluating coverage, the relevant metric isn’t “how many countries support document verification” (nearly all do), it’s “how many countries have mature, queryable identity data sources at the passive tier, and how many have live national eID schemes at the active tier.” Those two numbers tell you where document-free onboarding is viable and where a document fallback is still necessary.

What happens when a customer won’t engage with verification

If a customer actively refuses to submit to verification, whether document-based or database-based, the obligation under most regulatory frameworks is straightforward: you cannot onboard them for a regulated service. FATF Recommendation 10 is explicit that if a customer fails or refuses CDD, the institution must not open the account, must consider filing a suspicious activity report if circumstances warrant, and must terminate any existing relationship if it cannot be remediated.

The more common scenario isn’t outright refusal; it’s passive abandonment, where a customer simply doesn’t complete the flow. That’s where eIDV addresses a real product problem: by removing the document upload step entirely and completing the background check on data the customer has already supplied (name, date of birth, address, phone number), the passive tier eliminates the most common drop-off trigger. The customer doesn’t experience a verification step at all.

Conclusion

Shufti’s eIDV Pro covers 85+ countries for passive verification and connects to 30+ national eID schemes for active verification, all through a single API with sub-3-second response times and a 99% pass rate. Businesses using it have reported 30%+ reductions in onboarding drop-off. It supports cloud, on-premises, and hybrid deployment, and includes a full audit trail for regulatory reporting.

If you’re evaluating document-free verification options, request a demo to see how the three-tier framework maps to your specific onboarding flows and risk profile. Or explore the eIDV product page for a full breakdown of country coverage, data sources, and integration options.

Frequently Asked Questions

How do online eIDV solutions handle customers without standard identity documents?

At the passive tier, eIDV works without any document at all, it queries telco records, credit bureau files, electoral rolls, and national registries using basic personal data the customer supplies during sign-up. For markets where document coverage is thin but telco subscriber bases are large (common in parts of APAC and Africa), passive eIDV against mobile network operator data can reach customers that document-based onboarding cannot.

How secure is online identity verification compared to in-person checks?

At the passive and active tiers, online eIDV is comparable to in-person verification for most regulated use cases. At the biometrically enriched tier, live selfie match against a government-held photo using iBeta-certified liveness detection, it can exceed the assurance level of a standard in-person branch check, because a branch staff member cannot access the government biometric database directly and relies on visual inspection of a physical document.

Are online eIDV solutions admissible as proof of due diligence during regulatory audits?

Yes, where properly implemented. FATF Recommendation 10 permits a risk-based approach that allows electronic verification where appropriate. The audit defensibility depends on documentation: which data sources were queried, what match thresholds were applied, how the risk classification was determined, and what the audit trail shows. A well-configured eIDV deployment with a complete audit log is defensible; an eIDV check with no documented methodology is not, regardless of whether it involved a document or not.

How do online eIDV solutions prevent identity spoofing?

Through cross-referencing. Querying two independent authoritative sources simultaneously, credit bureau and electoral roll, or telco and government registry, dramatically narrows the attack surface compared to a single-source check. Synthetic identities that pass one source typically fail against an independent source with a different data provenance. At the biometrically enriched tier, iBeta-certified liveness detection closes the remaining spoofing vector.