Face Verification

Face Verification

Address Verification

Address Verification

Document Verification

Document Verification

Age Verification

Age Verification

VideoIdent

VideoIdent

Fast ID

Fast ID

Docless Verification

Docless Verification

Consent Verification

Consent Verification

NFC Verification

NFC Verification

Business Verification

Business Verification

Due Diligence

Due Diligence

Investor Verification

Investor Verification

E-Signature

E-Signature

QES

QES

AML Screening

AML Screening

Transaction Monitoring

Transaction Monitoring

Adverse Media

Adverse Media

Business AML Screening

Business AML Screening

PEP & RCA

PEP & RCA

Sanctions

Sanctions

Watchlist

Watchlist

Behavioural Biometrics

Behavioural Biometrics

Device Fingerprinting

Device Fingerprinting

Biometric Face Authentication

Biometric Face Authentication

MFA

MFA

Fraud Hub

Fraud Hub

Onboarding

Onboarding

Ongoing Monitoring

Ongoing Monitoring

KYC

KYC

KYB

KYB

KYI

KYI

Age Assurance

Age Assurance

Identity Verification

Identity Verification

Workforce IAM

Workforce IAM

Candidate Verification

Candidate Verification

Compliance

Compliance

Fraud prevention

Fraud prevention

Trust & safety

Trust & safety

Global expansion

Global expansion

Product Managers

Product Managers

Compliance Officers

Compliance Officers

Fraud Analysts

Fraud Analysts

Developers

Developers

Deepfake Detection

Deepfake Detection

Bonus Abuse / Promotion Abuse

Bonus Abuse / Promotion Abuse

Account Takeover

Account Takeover

Synthetic Identity Fraud

Synthetic Identity Fraud

Document Fraud

Document Fraud

Impersonation Fraud

Impersonation Fraud

Multi-Accounting

Multi-Accounting

Fraud Networks

Fraud Networks

Chargeback Fraud

Chargeback Fraud

Money Mule Activity

Money Mule Activity

Party Fraud

Party Fraud

Regulatory & Compliance Risks

Regulatory & Compliance Risks

Fintech

Fintech

Crypto

Crypto

iGaming

iGaming

Forex

Forex

Social Network

Social Network

Marketplace

Marketplace

Banking

Banking

Gig Economy

Gig Economy

Payments

Payments

Ride Hailing

Ride Hailing

Adult Content

Adult Content

Blind Spot Audit

Blind Spot Audit

Deepfake Detector

Deepfake Detector

Liveness Spoofs

Liveness Spoofs

Document Originality

Document Originality

Document Deepfake

Document Deepfake

Global Trust Platform

Global Trust Platform

Journey Builder

Journey Builder

Case Management

Case Management

Shufti AI

Shufti AI

Fraud Analytics

Fraud Analytics

Vendor Comparison

Vendor Comparison

Brand Personalisation

Brand Personalisation

AI Compliance Co-Pilot

AI Compliance Co-Pilot

OCR

OCR

Secure Capture

Secure Capture

Deployment Options

Deployment Options

Identity Methods

Identity Methods

API Documentation

API Documentation

Mobile SDKs

Mobile SDKs

Service Status

Service Status

Help Center

Help Center

Contact Us

Contact Us

Technical Support

Technical Support

Supported Documents

Supported Documents

Supported Countries

Supported Countries

Content library

Content library

Blogs

Blogs

News

News

Reports

Reports

Insights

Insights

Knowledgebase

Knowledgebase

ROI calculator

ROI calculator

About

About

Career

Career

Press Release

Press Release

Certifications

Certifications

Partnership

Partnership

Awards

Awards

Events & Webinar

Events & Webinar

Interactive Demo

Interactive Demo

Podcast Studio

Podcast Studio

Spotlight Studio

Spotlight Studio

Identity Verification Technology Explained: How AI, Biometrics, and OCR Work Together

Global losses from identity fraud exceeded $50 billion in 2025, and deepfake-powered attacks are growing faster than most compliance teams can track. For businesses running customer onboarding at scale, the question is no longer whether to automate identity checks, it’s whether the technology behind those checks can actually keep up with the attacks.

Identity verification technology is the combination of software and algorithms that confirms a person is who they claim to be during a digital interaction. It typically pulls together document scanning, facial matching, and AI-driven risk analysis into a single real-time decision.

The challenge is that many businesses still treat these components OCR, biometrics, and AI as separate tools bolted together from different vendors. That approach creates gaps. A document might pass OCR extraction but never get matched against the person holding it, or a biometric check might run without any AI layer flagging the submission as a deepfake.

Below is how each technology works on its own, and how they function as a single pipeline that catches what individual checks miss.

What Is Identity Verification Technology and Why Does It Matter Now?

At its core, identity verification technology is the system that sits between a user submitting their credentials and a business deciding whether to trust those credentials. It replaces manual review with automated, multi-layered checks.

The urgency is real. Over 620 million pounds have been lost to fraud in the first half of 2025. Fraud attempts using deepfakes have increased by 2,137% over the last three years. And the FATF updated its standards in February 2025 to formally acknowledge that digital identity verification is no longer inherently higher-risk than in-person checks regulators now expect it as standard practice.

For compliance officers and product teams, identity verification technology is the mechanism that makes KYC, AML, and age verification enforceable without creating onboarding friction that kills conversion rates.

The Three Core Technologies Powering Modern IDV

OCR: Reading the Document

Optical Character Recognition is the first step in the verification chain. When a user uploads a passport, national ID, or driver’s licence, OCR technology extracts the printed and machine-readable text name, date of birth, document number, expiry date, MRZ codes and converts it into structured data.

Modern OCR goes beyond simple text extraction. AI-enhanced OCR detects tampering signals: font inconsistencies, pixel-level edits around date fields, mismatches between the visual zone and MRZ data. It also handles documents in nearly 100 languages, including non-Latin scripts like Arabic, Mandarin, and Cyrillic.

The accuracy of OCR extraction cascades through everything downstream. If the document data is wrong, the biometric match runs against bad information, and the AI decision engine scores a fraudulent profile as clean.

Biometrics: Confirming the Person

Where OCR handles the document, biometric verification handles the person. Facial biometrics capture a live selfie or video from the user and match it against the photo extracted from the identity document, a 1:1 comparison that answers one question: is the person holding this document the same person pictured on it?

The sophistication lies in liveness detection. Passive liveness analyses texture, depth, and micro-expressions without requiring the user to perform actions. Active liveness asks the user to blink, turn, or respond to prompts. Multi-layered systems combine both approaches to defend against 3D masks, video replays, and AI-generated deepfakes.

The metric that matters is FAR (False Acceptance Rate). A system with a high FAR lets fraudsters through. Independent government testing programmes like the DHS RIVR programme provide third-party benchmarks that hold vendors accountable beyond self-reported claims.

AI: Orchestrating the Decision

AI is the layer that ties OCR and biometrics together. It doesn’t just run checks it makes the call.

Machine learning models score the combined evidence: Does the document data match the biometric data? Does the selfie show signs of injection attacks? Does the document exhibit known forgery patterns for that issuing country?

AI also handles edge cases that binary pass/fail systems miss. A partially obscured document that fails standard OCR can be flagged for hybrid AI + human review rather than outright rejection reducing false positives without letting fraud slip through.

How AI, Biometrics, and OCR Work Together in One Pipeline

Running these technologies in isolation creates blind spots. The real security advantage comes from the handoff between them.

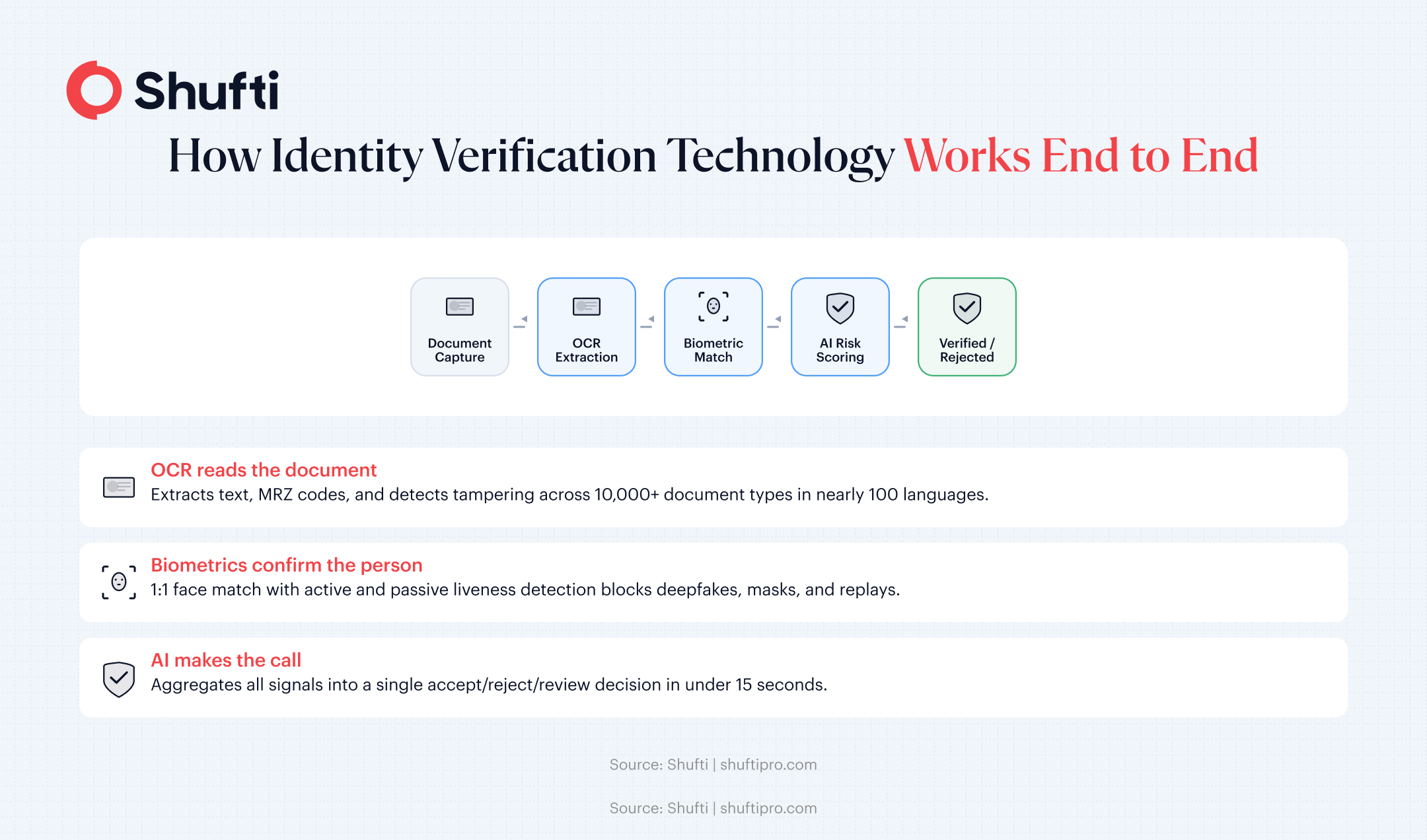

Here is how a typical verification flow works end to end:

1. Document capture: The user photographs or uploads their identity document via web or mobile SDK.

2. OCR extraction: The system reads the document, extracts structured data, detects tampering, and classifies the document type (passport, national ID, driving licence) across 10,000+ supported templates.

3. Biometric capture: The user takes a live selfie. Liveness detection confirms a real person, not a photo printout, mask, or deepfake injection.

4. 1:1 face match: The AI compares the selfie against the document photo. This binds the person to the document in real time.

5. AI risk scoring: The decision engine aggregates all signals like OCR data quality, biometric confidence score, document authenticity, liveness result and produces a single accept/reject/review decision in under 15 seconds.

Each step feeds into the next. OCR provides the baseline data. Biometrics provide the human anchor. AI weighs the combined evidence and makes the call. If any single layer is missing or disconnected, say, OCR runs through one vendor and biometrics through another. The evidence chain has a seam. And seams are exactly where sophisticated fraud lives.

The biometric identity verification market is projected to reach $17.81 billion by 2030, up from $8.88 billion in 2025. That growth is being driven by businesses moving from fragmented point solutions to unified platforms that run the full pipeline under one roof.

How Shufti Brings AI, Biometrics, and OCR Into a Single Platform

Shufti runs the entire verification pipeline document verification, facial biometrics, liveness detection, and AI risk scoring through a single API. There is no third-party dependency for any layer.

What that means in practice: the OCR engine, the biometric models, and the AI decision layer are all proprietary and talk to each other natively. There is no data handoff between vendors, no latency from cross-platform API calls, and no gap in the evidence chain.

Shufti’s internal benchmarks reflect this: 98.72% facial biometrics accuracy (iBeta Level 1 & 2 certified), coverage of 10,000+ document types across 230+ countries, and OCR in nearly 100 languages. Full KYC completes in under 15 seconds. Deployment options include cloud, on-premises, or hybrid through the same API.

For compliance teams navigating eIDAS 2.0 wallet requirements and tightening KYC mandates, a single-platform approach reduces audit complexity. One vendor, one data processor, one evidence trail.

See how Shufti’s identity verification technology works for your use case — request a demo.

Conclusion

Identity verification technology works best as a unified pipeline OCR reads the document, biometrics confirm the person, and AI weighs the combined evidence in real time. When those layers run under one roof, fraud has fewer seams to exploit and compliance teams get a single audit trail to defend.

The businesses pulling ahead are consolidating their verification stack now, before regulators and fraudsters force the issue.

Frequently Asked Questions

How do banks use identity verification technology for KYC?[e][f][g][h]

Banks use identity verification technology to confirm that customers are who they claim to be during onboarding and ongoing account management. This typically involves document verification (scanning and authenticating government-issued IDs), biometric checks like facial recognition or liveness detection, and database cross-referencing against sanctions lists, PEPs, and adverse media. The technology automates what was once a manual process, allowing banks to meet regulatory KYC requirements at scale while reducing onboarding friction for legitimate customers.

How does identity verification technology help prevent online fraud?

Identity verification technology creates multiple layers of friction that fraudsters struggle to bypass. Document verification detects forged or tampered IDs. Liveness detection prevents spoofing attacks using photos or deepfakes. Biometric matching ensures the person presenting the document is its legitimate owner. Combined with device intelligence and behavioral signals, these checks catch synthetic identities, account takeover attempts, and fraudulent registrations before bad actors.

Can identity verification technology detect fake IDs?

Yes. AI-enhanced OCR detects font inconsistencies, pixel-level edits, and mismatches between visual zones and MRZ data. Biometric liveness detection blocks deepfakes, 3D masks, and photo replays. Combined, these layers catch forgeries that any single check would miss.

How does identity verification technology support KYC compliance?

It automates the customer due diligence process mandated by regulations like FATF standards, eIDAS 2.0, and local KYC laws. Document verification confirms the credential, biometrics confirm the person, and AI maintains the auditable evidence trail regulators require.

What is the difference between in-house identity verification technology and third-party AI?

In-house technology means the provider built and owns the OCR, biometric, and AI models. Third-party stacks license components from external vendors, creating data handoff risks and integration gaps. In-house systems offer tighter security, faster processing, and a single point of accountability.

: Meaning, Requirements, and When You Need One")

Fraud: What It Is, How It Works, and How to Stop It")