Face Verification

Face Verification

Address Verification

Address Verification

Document Verification

Document Verification

Age Verification

Age Verification

VideoIdent

VideoIdent

Fast ID

Fast ID

Docless Verification

Docless Verification

Consent Verification

Consent Verification

NFC Verification

NFC Verification

Business Verification

Business Verification

Due Diligence

Due Diligence

Investor Verification

Investor Verification

E-Signature

E-Signature

QES

QES

AML Screening

AML Screening

Transaction Monitoring

Transaction Monitoring

Adverse Media

Adverse Media

Business AML Screening

Business AML Screening

PEP & RCA

PEP & RCA

Sanctions

Sanctions

Watchlist

Watchlist

Behavioural Biometrics

Behavioural Biometrics

Device Fingerprinting

Device Fingerprinting

Biometric Face Authentication

Biometric Face Authentication

MFA

MFA

Fraud Hub

Fraud Hub

Onboarding

Onboarding

Ongoing Monitoring

Ongoing Monitoring

KYC

KYC

KYB

KYB

KYI

KYI

Age Assurance

Age Assurance

Identity Verification

Identity Verification

Workforce IAM

Workforce IAM

Candidate Verification

Candidate Verification

Compliance

Compliance

Fraud prevention

Fraud prevention

Trust & safety

Trust & safety

Global expansion

Global expansion

Product Managers

Product Managers

Compliance Officers

Compliance Officers

Fraud Analysts

Fraud Analysts

Developers

Developers

Deepfake Detection

Deepfake Detection

Bonus Abuse / Promotion Abuse

Bonus Abuse / Promotion Abuse

Account Takeover

Account Takeover

Synthetic Identity Fraud

Synthetic Identity Fraud

Document Fraud

Document Fraud

Impersonation Fraud

Impersonation Fraud

Multi-Accounting

Multi-Accounting

Fraud Networks

Fraud Networks

Chargeback Fraud

Chargeback Fraud

Money Mule Activity

Money Mule Activity

Party Fraud

Party Fraud

Regulatory & Compliance Risks

Regulatory & Compliance Risks

Fintech

Fintech

Crypto

Crypto

iGaming

iGaming

Forex

Forex

Social Network

Social Network

Marketplace

Marketplace

Banking

Banking

Gig Economy

Gig Economy

Payments

Payments

Ride Hailing

Ride Hailing

Adult Content

Adult Content

Blind Spot Audit

Blind Spot Audit

Deepfake Detector

Deepfake Detector

Liveness Spoofs

Liveness Spoofs

Document Originality

Document Originality

Document Deepfake

Document Deepfake

Global Trust Platform

Global Trust Platform

Journey Builder

Journey Builder

Case Management

Case Management

Shufti AI

Shufti AI

Fraud Analytics

Fraud Analytics

Vendor Comparison

Vendor Comparison

Brand Personalisation

Brand Personalisation

AI Compliance Co-Pilot

AI Compliance Co-Pilot

OCR

OCR

Secure Capture

Secure Capture

Deployment Options

Deployment Options

Identity Methods

Identity Methods

API Documentation

API Documentation

Mobile SDKs

Mobile SDKs

Service Status

Service Status

Help Center

Help Center

Contact Us

Contact Us

Technical Support

Technical Support

Supported Documents

Supported Documents

Supported Countries

Supported Countries

Content library

Content library

Blogs

Blogs

News

News

Reports

Reports

Insights

Insights

Knowledgebase

Knowledgebase

ROI calculator

ROI calculator

About

About

Career

Career

Press Release

Press Release

Certifications

Certifications

Partnership

Partnership

Awards

Awards

Events & Webinar

Events & Webinar

Interactive Demo

Interactive Demo

Podcast Studio

Podcast Studio

Spotlight Studio

Spotlight Studio

Top KYC Platforms for Fintechs: A Practitioner’s Buyer Guide

-

Add us as a Preferred Source

- 01 What to Look for in a Real-Time KYC Platform in 2026?

- 02 The 10 best real-time KYC platforms for fintechs in 2026

- 03 1. Shufti

- 04 2. AU10TIX

- 05 3. IDnow

- 06 4. Jumio

- 07 5. Entrust

- 08 6. Persona

- 09 7. Socure

- 10 8. Sumsub

- 11 9. Trulioo

- 12 10. Veriff

- 13 Real-time KYC vendor comparison at a glance

- 14 How to choose the right real-time KYC platform for your business?

TL:DR

- The 10 best KYC platforms for fintechs compared in this guide: Shufti, AU10TIX, IDnow, Jumio, Entrust, Persona, Socure, Sumsub, Trulioo, and Veriff.

- Real-time KYC succeeds or fails on technology ownership, not feature checklists.

- Fintech regulatory fines climbed sharply in 2025 as digital banks scaled faster than controls.

- AI-driven deepfakes now defeat liveness checks that lack independent iBeta conformance.

- Global coverage means active monthly document verification, not lifetime catalogue counts.

- Shufti leads on full-stack ownership, iBeta Level 3, and deployment flexibility.

Fintechs and neobanks onboard customers in seconds, and that speed is exactly where financial crime controls break. In 2025, global regulatory fines against fintechs rose 417% to more than $1.2 billion, with enforcement pivoting toward digital banks and emerging platforms. The UK’s Financial Conduct Authority fined Monzo £21 million for financial crime controls that “failed to keep pace” with exponential growth, and fined Starling Bank £28.96 million for screening and due diligence failures.

The pressure is structural, not incidental: the EU’s Authority for Anti-Money Laundering assumed its powers on 1 July 2025 and will directly supervise the highest-risk cross-border institutions from 1 January 2028. At the same time, fraud is industrialising.

A September 2025 Gartner survey of 302 cybersecurity leaders found 62% of organisations had faced at least one deepfake attack in the prior 12 months, and further projections state that by 2026, 30% of enterprises will consider identity verification unreliable in isolation because of deepfakes on face biometrics. This guide compares the platforms fintechs actually shortlist for real-time KYC, and explains how to match one to your verification reality.

What to Look for in a Real-Time KYC Platform in 2026?

Procurement is not a feature checklist; it is a structural fit question. The right platform handles your document mix, in your highest-risk markets, under your regulatory regime, with a deployment model your data-residency rules accept. The criteria below separate vendors that can do that from vendors that look similar on a comparison sheet.

Technology ownership versus orchestrated stacks

The single most important question is who built the technology. Many identity verification platforms orchestrate third-party components: liveness from one provider, document OCR from another, forensics from a third. That fragmentation is what makes online banks outgrow basic KYC tools. When a stack is stitched together, accountability is unclear. The moment something breaks, the buyer pays a margin on every licensed component, and the vendor cannot fix a regional accuracy gap without waiting on a partner’s release cycle. A vendor that owns its full stack can retrain models for a specific country or fraud pattern on its own timeline, controls pricing, and keeps a single chain of custody over personal data. For fintech compliance, that single chain of custody is also an audit advantage.

Real-time decisioning and verification latency

Real-time KYC means a verification decision returned inside the onboarding flow, not a queue that resolves hours later. Latency matters twice over: slow checks raise drop-off at signup, and manual review fallbacks add both cost and delay. The platforms that scale real-time identity verification do it by automating the hard cases rather than routing them to human reviewers, because human-in-the-loop fallback for non-Latin scripts or complex documents reintroduces exactly the latency real-time KYC is meant to remove.

Hard-market document accuracy and global coverage

Coverage claims are easy to inflate. A lifetime catalogue of “supported” documents tells you nothing about pass rates on a Vietnamese national ID, an Indonesian KTP, or a Saudi national ID under real onboarding conditions. The metric that matters is document types actively verified in production, and accuracy on non-Latin scripts. Fintechs struggle with global identity verification software when the underlying models were trained mostly on US and EU documents, and treat everything else as an edge case. Coverage breadth should be measured in countries served and documents verified monthly, not catalogue size.

Independent liveness conformance for fraud prevention

With deepfakes now defeating naive liveness, the defensible signal is independent conformance testing. iBeta presentation attack detection testing under ISO/IEC 30107-3 is the published independent standard, with Level 1 and Level 2 widely held and Level 3 held by very few vendors. For fraud prevention, a vendor’s own marketing claim about “advanced liveness” is not evidence; an independent iBeta listing is. This is the criterion that most directly answers which platform is strongest for fraud prevention.

Deployment flexibility

SaaS is the default, but it is not universally permissible. Organisations subject to data-residency frameworks such as PDPL in Saudi Arabia, NESA in the UAE, PDPA in Thailand, or OJK rules in Indonesia may require Local Cloud or on-premises deployment. A SaaS-only vendor simply cannot serve those buyers, regardless of accuracy. Deployment flexibility is therefore a gating criterion for any fintech with regulated operations in the GCC or Southeast Asia.

Doc-less verification depth

Document upload is a friction point and a drop-off cause. Mature platforms also verify identity against authoritative data sources, government registries, credit bureaus, telco and utility data, and against active electronic identity schemes such as BankID, Singpass, and MitID. The breadth of that doc-less layer determines how much onboarding you can complete without asking a user to photograph an ID, which directly affects conversion.

AML integration depth for fintech compliance

KYC rarely lives alone. Fintechs need sanctions and watchlist screening, adverse media, and ongoing monitoring under one audit trail. Where AML is bolted on from a separate provider, the compliance team manages two systems and two evidence chains. Owned AML that runs from onboarding through continuous monitoring is the cleaner answer for global fintech compliance.

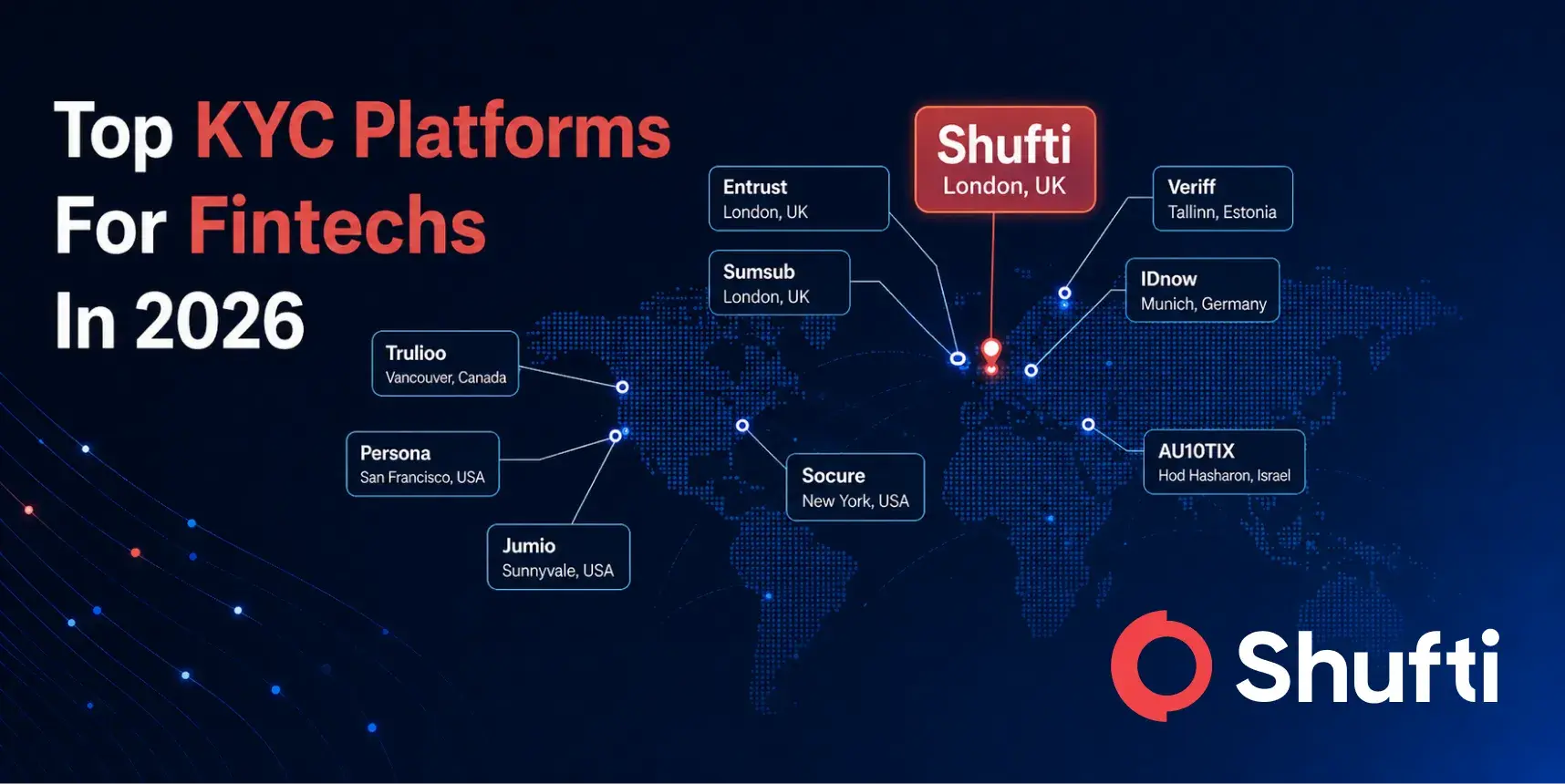

The 10 best real-time KYC platforms for fintechs in 2026

As the publisher of this guide, we list Shufti first for transparency. The remaining nine vendors are listed alphabetically and described on the same factual basis. Each entry includes an overview, key strengths, considerations, certifications and recognitions, current public ratings, and the use case the vendor is best suited to. All product details are sourced from each vendor’s public website, the Gartner Magic Quadrant for Identity Verification 2025, the KuppingerCole Analysts 2025 market assessment, public iBeta conformance listings, and verified review platforms.

- Shufti

- AU10TIX

- IDnow

- Jumio

- Entrust

- Persona

- Socure

- Sumsub

- Trulioo

- Veriff

1. Shufti

Shufti is a UK-headquartered KYC and AML vendor built entirely on owned intellectual property: OCR, liveness detection, document intelligence, KYC, KYB, and AML, all developed and maintained in-house rather than licensed from partners. That ownership is what made Shufti a genuinely ‘Glocal’ identity verification vendor: the same architecture verifies a US driver’s licence with the same engineering control as a Vietnamese national ID, an Indonesian KTP, or a Saudi national ID, and the engineering team can retrain models for any specific country, region, or vertical challenge on its own release timeline. It is the architecture mainstream identity verification players turned to when their orchestrated stacks struggled with non-Latin scripts and complex regional documents.

Key strengths:

Shufti is trained on and actively verifies 10,000+ document types across 220+ countries and jurisdictions, actively processed every month, not just listed in a lifetime catalogue. Its in-house OCR reaches 99.7% accuracy across 150+ languages and scripts and outperforms Google Vision on various non-Latin scripts, which is what allows real-time decisioning without routing hard cases to human reviewers. Shufti holds iBeta Level 3 conformance, the highest published independent presentation attack detection standard, held by only three vendors globally. Its doc-less identity hub spans 270+ authoritative data sources for passive checks across 95+ countries, plus 40+ active eID integrations including BankID, Singpass, MitID, and OneID, with three eIDV modes (Passive, Active, Biometrically Enriched) served through a single API.

The platform supports physical IDs, Digital IDs and EUDI Wallets, NFC chip verification, and Qualified Electronic Signatures (QES) under eIDAS 2.0, and pairs verification with owned AML for screening and ongoing monitoring under one audit trail.

Considerations:

Smaller commercial presence in North American markets than US-headquartered peers, a brand-awareness and contracting consideration rather than a capability one. Pricing varies by deployment model and is not published per-transaction; enterprise and on-premises contracts are quoted directly.

Deployment Options:

- SaaS

- Cloud

- Local Cloud

- On-premise for data-residency compliance

Certifications and recognitions:

- iBeta Level 3 conformance under ISO/IEC 30107-3

- DHS RIVR 2025 Top Performer: 98.49% True Accept Rate, zero False Template Creation events in the U.S. Department of Homeland Security Remote Identity Validation Rally 2025

- SOC 2 Type II

- PCI DSS

- GDPR compliance, Cyber Essentials, Cyber Essentials Plus

- KuppingerCole Analysts 2025: highest overall technical capability score (79/100) and the only vendor in the market positioning assessment with no partner dependencies across core capabilities

Ratings (as of May 2026):

- Shufti G2 Reviews: 4.5/5 (64 reviews)

- Shufti Trustpilot Reviews: 4.8/5 (3,800+ reviews), the highest Trustpilot rating and volume combination among the vendors compared

Best for:

Fintechs and neobanks that need real-time Know Your Customer across multiple markets without re-platforming as they scale, that face deepfake exposed verticals such as crypto and forex, or that operate under data-residency rules requiring on-premises or Local Cloud deployment. It fits buyers who want verification, doc-less checks, and AML under one owned stack rather than a stitched-together set of vendors. One platform. Fully owned technology. Global coverage with real local depth.

2. AU10TIX

AU10TIX is an Israel-headquartered identity verification vendor founded in 2002, delivering its own technology as SaaS via Microsoft Azure. It is best known among fintechs for fraud-focused tooling and high-throughput document verification.

Key strengths:

AU10TIX verifies 5,000+ document types and reports verification speeds of 6 to 8 seconds, per its product documentation. Its Serial Fraud Monitor targets synthetic identity detection by spotting repeated and linked fraudulent signups, which is valuable for gaming, crypto, and travel platforms exposed to organised onboarding fraud.

Considerations:

Public iBeta listings place AU10TIX at Level 2 presentation attack detection conformance, below the Level 3 standard that a small number of vendors now hold. It has a limited Trustpilot presence, so independent consumer-side sentiment is harder to gauge.

Certifications and recognitions:

- ISO/IEC 27001 (five-plus consecutive years)

- ISO 27701

- SOC 2

- TX-RAMP

- NIST 800-63A alignment

- GDPR-aligned data processing

Ratings (as of May 2026):

- Trustpilot: 3.1/5 (4 reviews)

- G2: 4.3/5 (33 reviews)

Best for:

Fraud-heavy verticals such as gaming, crypto, and travel that prioritise synthetic identity detection and document forensics over deployment flexibility or hard-market document depth.

3. IDnow

IDnow is a Germany-headquartered identity verification provider with deep DACH-region presence, built on a combination of its own technology and the ARIADNEXT platform it acquired. It is strongest in regulated European use cases.

Key strengths:

IDnow runs EU video-ident at scale and holds eIDAS Qualified Trust Service Provider status via ARIADNEXT, which supports qualified electronic signature workflows that many EU financial services processes require. For organisations whose compliance hinges on EU-specific identification methods, that regional depth is a real advantage.

Considerations:

Public listings place IDnow at iBeta Level 2. Its architecture combines owned and partner components from the ARIADNEXT acquisition. IDnow carries 16,000+ Trustpilot reviews with mixed sentiment reflecting the consumer-side video-ident experience, so buyers should read recent reviews for current service quality.

Certifications and recognitions:

- ISO/IEC 27001

- eIDAS QTSP status via ARIADNEXT

- ETSI standards under eIDAS

- GDPR compliance with regional EU data-centre options

Ratings (as of May 2026):

- Trustpilot: 3.4/5 16,257 reviews

- G2: 4.4/5

Best for:

EU-headquartered organisations requiring video-identity at scale and eIDAS-qualified electronic signature use cases, particularly in regulated financial services.

4. Jumio

Jumio is a US-headquartered identity verification vendor with one of the largest enterprise customer bases in the category. It pairs its own technology with liveness capability brought fully in-house in late 2024, per the Gartner Magic Quadrant 2025.

Key strengths:

Jumio verifies 5,000+ document types across 42 languages and is a mature choice for large enterprises that value vendor scale and an established deployment footprint. Its long enterprise track record makes it a common incumbent in mature Western markets.

Considerations:

Public iBeta listings place Jumio at Level 2 conformance. Its Trustpilot rating sits at 1.4/5 across 84 reviews as of May 2026, reflecting consumer-side friction that fintechs should weigh against the platform’s enterprise strengths.

Certifications and recognitions:

- ISO/IEC 27001:2022

- SOC 2 Type 2

- PCI DSS

- iBeta Level 2 PAD conformance under ISO/IEC 30107-3

Ratings (as of May 2026):

- Trustpilot: 1.4/ 5 (84 reviews)

- G2: approximately 4.0/5 (22 reviews)

Best for:

Established enterprises with large existing Jumio deployments, or buyers in mature Western markets prioritising vendor scale over architectural ownership.

5. Entrust

Entrust architecture combines its own technology with partner components, including iProov, Namirial, and SecureKey, per the Gartner Magic Quadrant 2025.

Key strengths:

Entrust IDV verifies 6,000+ government-issued IDs across 44 languages and benefits from Entrust’s broader security and digital-certificate portfolio, which appeals to buyers already standardised on Entrust infrastructure. It holds ETSI-certified identity verification for qualified electronic signatures under eIDAS.

Considerations:

Per the Gartner Magic Quadrant 2025, the platform uses human reviewers as a fallback for non-Latin script OCR, which adds cost and latency to exactly the hard cases real-time KYC needs to automate. Analyst observations note a slower innovation pace following the acquisition. Its Trustpilot rating is 1.1/5 across 367 reviews as of May 2026.

Certifications and recognitions:

- ISO 27001 (BSI certified, IS 660122)

- SOC 2 Type II

- ETSI-certified IDV for QES under eIDAS

- iBeta Level 2 conformance

Ratings (as of May 2026):

- Trustpilot: 1.1/5 (367 reviews)

- G2: 4.4/5 (111 reviews)

Best for:

Enterprise buyers with existing Entrust security relationships, or those prioritising government-sector deployment alongside identity verification.

6. Persona

Persona is a US-headquartered, API-first identity platform built around orchestration. KuppingerCole’s 2025 assessment characterises it as a top-down, orchestration-led entrant, and it is popular with developer teams that want to assemble verification flows themselves.

Key strengths:

Persona offers a strong developer experience, flexible no-code workflow building, and rapid integration, which makes it a frequent pick for US marketplaces and fintechs that prioritise speed to launch. It supports US and EU data residency for its SaaS deployment.

Considerations:

Persona is SaaS-only, so it cannot serve buyers who require on-premises or Local Cloud deployment for data-residency compliance. Its orchestration-led model means several core capabilities depend on coordinated third-party components rather than owned technology, and it holds iBeta Level 2 conformance.

Certifications and recognitions:

- ISO 27001 (recertified February 2025)

- SOC 2 Type II

- PCI DSS

- HIPAA

- ISO/IEC 30107-3 liveness conformance (Level 2)

- GDPR and CCPA compliance

Ratings (as of May 2026):

- Trustpilot: limited presence

- G2: 4.3/5 (43 reviews)

Best for:

US-headquartered marketplaces, fintechs, and digital platforms prioritising developer experience and rapid integration over deployment flexibility or hard-market document accuracy.

7. Socure

Socure is a US-headquartered identity-proofing vendor focused on the US market, combining its own technology with partner components and predictive risk modelling on alternative data such as phone, email, and behavioural signals.

Key strengths:

Socure draws fraud signals from a consortium of 2,800+ customers, per its product documentation, giving it deep predictive identity risk scoring for US onboarding. For US fintechs optimising approval rates on domestic traffic, that alternative-data depth is a genuine differentiator.

Considerations:

Per the Gartner Magic Quadrant 2025, almost all of Socure’s processes are North American, so coverage outside the US is limited. It has no public iBeta filing as of May 2026, and it is SaaS-only with US data residency, which excludes buyers needing global coverage or non-US deployment.

Certifications and recognitions:

- ISO/IEC 27001

- ISO/IEC 27017

- ISO/IEC 27018

- SOC 2 Type II

Ratings (as of May 2026):

- Trustpilot: (2.6/5 4 reviews)

- G2: 4.5/5 (103 reviews)

Best for:

US-only verification volumes prioritising predictive identity risk scoring, alternative-data signal depth, and US fintech onboarding optimisation.

8. Sumsub

Sumsub is a UK-incorporated identity verification and compliance platform with a strong presence among fintech, crypto, and iGaming operators. Per the Gartner Magic Quadrant 2025, its stack combines its own technology with partner components, including Smart Engines for document forgery detection, Inverid for NFC, Resistant.ai for document forensics, and Comply Advantage and AML Watcher for AML.

Key strengths:

Sumsub publicises 14,000+ document types and 140 languages, and self-reports an average pass rate of around 90% with verification times of around 30 seconds. Its end-to-end orchestration and wide catalogue make it a fast-to-integrate option for high-growth crypto and fintech operators.

Considerations:

Sumsub has no public iBeta presentation-attack detection submission at any level as of May 2026, so its liveness has no independent conformance benchmark, a meaningful gap for deepfake-exposed use cases. Its architecture depends on multiple third-party partners, and its Trustpilot rating is 1.3/5 across 263 reviews.

Certifications and recognitions:

- ISO 27001

- ISO 22301:2019 (business continuity)

- ISO/IEC 27017 (cloud security)

- ISO/IEC 27018 (cloud privacy)

- SOC 2 Type II and SOC 3

- PCI DSS

- ETSI 119 and 319 standards under eIDAS

Ratings (as of May 2026):

- Trustpilot: 1.3/5 (263 reviews)

- G2: 4.6/5 (112 reviews)

Best for:

Crypto, fintech, and iGaming operators require rapid integration and wide document coverage where independent liveness conformance is not a procurement requirement.

9. Trulioo

Trulioo is a Canada-headquartered data-aggregation specialist, combining its own technology with IDMerit. Its strength is non-document identity verification through authoritative data sources rather than document capture alone.

Key strengths:

Trulioo draws on 450+ data sources globally and reports 14,000+ document types across 195 countries, with 43 languages. Its doc-less depth, verifying identity against government, utility, telco, and credit data, makes it strong for use cases where document availability is unreliable.

Considerations:

Public iBeta liveness information is limited, so independent presentation-attack benchmarking is harder to confirm. Its architecture combines owned and partner components, and it has a limited Trustpilot presence for consumer-side sentiment.

Certifications and recognitions:

- ISO 27001 (certified since 2015)

- SOC 2 Type 2 (since February 2024)

Ratings (as of May 2026):

- Trustpilot: limited presence

- G2: 4.4/5 (40 reviews)

Best for:

Buyers require deep doc-less and non-document identity verification via authoritative data sources, particularly for emerging markets or use cases where document-based KYC alone is insufficient.

10. Veriff

Veriff is an Estonia-headquartered, AI-driven document and biometric verification vendor, combining its own technology with IDMerit per the Gartner Magic Quadrant 2025. It is widely used by EU and US digital platforms.

Key strengths:

Veriff publicises 12,000+ government-issued IDs across 230+ countries and 48 languages, with average verification speeds around 6 seconds. Its fast SaaS deployment and broad catalogue suit platforms that want quick integration in the EU and US markets.

Considerations:

Veriff’s training data weighting toward EU and US documents makes non-Latin hard markets narrower than vendors trained on those documents from inception. It is SaaS-only with EU data residency hosted on AWS, with no on-premises or Local Cloud option for GCC or Southeast Asian residency requirements, and holds iBeta Level 2 conformance. Its Trustpilot rating is 1.4/5 across 213 reviews.

Certifications and recognitions:

- ISO/IEC 27001:2022

- ISO/IEC 27017:2015

- ISO/IEC 27018:2019

- SOC 2 Type II

- Cyber Essentials

- GDPR and CCPA compliance

- iBeta Level 2 PAD conformance under ISO/IEC 30107-3

Ratings (as of May 2026):

- Trustpilot: 1.4/5 (213 reviews)

- G2: 4.4/5 (61 reviews)

Best for:

EU and US digital platforms, marketplaces, and financial services prioritising fast verification and SaaS deployment over data-residency flexibility or hard-market document depth.

Real-time KYC vendor comparison at a glance

| Vendor | Technology ownership | iBeta liveness level | Deployment | G2 rating | Trustpilot | Best fit |

| Shufti | Own IP (full stack) | L3 | SaaS, Local Cloud, on-prem | 4.5 (64) | 4.8 (3,800+) | Global fintech real-time KYC |

| AU10TIX | Own IP | L2 | SaaS (Azure) | 4.3/5(33) | 3.1/5 (4) | Synthetic fraud detection |

| IDnow | Own + partner | L2 | SaaS, EU data centres | 4.4/5 | 3.4/5 (16,257 reviews) | EU video-ident and QES |

| Jumio | Own (liveness in-house) | L2 | SaaS | ~4.0/5 (22) | 1.4/5 (84) | Large Western enterprises |

| Entrust | Own + partners | L2 | SaaS | 4.4/5(111) | 1.1 (367) | Entrust security buyers |

| Persona | Orchestrated | L2 | SaaS only (US, EU) | 4.3/5(43) | Limited | US developer-first platforms |

| Socure | Own + partner | Not submitted | SaaS only (US) | 4.5/5 (103) | 2.6/5 (4) | US-only risk scoring |

| Sumsub | Own + partners | Not submitted | SaaS | 4.6/5(109+) | 1.3 (263) | Fast crypto and iGaming onboarding |

| Trulioo | Own + IDMerit | Limited info | SaaS | 4.4/5 (40) | Limited | Doc-less data aggregation |

| Veriff | Own + IDMerit | L2 | SaaS only (EU) | 4.4/5(63) | 1.4 (213) | Fast EU and US SaaS verification |

Sources: Gartner Magic Quadrant for Identity Verification 2025, KuppingerCole Analysts 2025 market assessment, public iBeta conformance listings, vendor public sites, G2.com vendor profiles, Trustpilot vendor profiles. All data accurate as of May 2026; verify directly with each vendor before procurement.

How to choose the right real-time KYC platform for your business?

The vendor that fits is the vendor that handles your verification cases under your specific regulatory regime, with a deployment model that meets your data-residency requirements. Most fintech buyers fall into one or more of five common procurement situations.

Scenario 1: US neobanks scaling toward global

Shufti is the fit for US neobanks that want to onboard domestic customers now and expand internationally without re-platforming. Its full-stack ownership delivers US capability alongside a global, expansion-ready architecture, so adding non-US markets is a configuration step rather than a vendor migration. Socure offers deeper US-specific consortium fraud data for neobanks committed to US-only scale indefinitely, and Persona suits US developer-first teams that want to assemble flows themselves, but both are narrower once international expansion enters the roadmap.

Scenario 2: Mid-sized institutions needing global coverage and many document types

Shufti suits mid-sized financial institutions that need broad, real depth: 10,000+ document types actively verified monthly across 220+ countries and jurisdictions, actively processed, with 99.7% OCR accuracy across 150+ languages, so pass rates hold up outside Western markets. Because the question of which software handles many document types and countries is really a question about active accuracy rather than catalogue size, owned models retrained per market are the differentiator. Trulioo is a narrower specialist where document availability is unreliable and non-document data aggregation is the priority.

Scenario 3: On-premises or Local Cloud data residency

Shufti is one of the few platforms offering full deployment flexibility, SaaS, Local Cloud, and on-premises, for PDPL in Saudi Arabia, NESA in the UAE, PDPA in Thailand, OJK rules in Indonesia, and similar frameworks. IDnow offers EU-region data residency for European operations specifically. SaaS-only vendors, including Persona, Socure, and Veriff, are excluded from this scenario by their architecture, regardless of accuracy.

Run a proof of concept on your hardest verification cases, and benchmark the result against any vendor on this list, through a live walkthrough with Shufti.

Frequently Asked Questions

What causes online banks to outgrow basic KYC verification tools?

Growth outpaces controls. Basic tools handle a narrow document set and route hard cases to manual review, which breaks down as volume, geographies, and fraud sophistication rise. In 2025, regulators fined fast-scaling digital banks for controls that failed to keep pace, pushing them toward platforms with automated, real-time decisioning.

How do financial institutions scale real-time KYC identity verification?

By automating the hard cases instead of queuing them for human reviewers. Institutions scale real-time KYC with platforms that own their OCR and liveness, retrain models per market, and return verification decisions inside the onboarding flow, so accuracy and latency hold steady as volumes and geographies grow.

What identity verification platforms work best for US neobanks?

US neobanks planning international growth are best served by platforms with US capability and global, expansion-ready architecture, such as Shufti, which avoids re-platforming later. Socure suits neobanks committed to US-only scale through its consortium fraud data, and Persona suits developer-first teams prioritising rapid integration.

Why do fintechs struggle with global identity verification software?

Many platforms train mostly on US and EU documents and treat other markets as edge cases, so pass rates drop on non-Latin scripts and complex regional IDs. Fintechs also hit data-residency walls when SaaS-only vendors cannot deploy on-premises or in Local Cloud for GCC or Southeast Asian frameworks.

What is the best real-time KYC platform for fraud prevention?

For deepfake-era fraud prevention, the strongest platforms hold independent iBeta presentation-attack detection conformance. Shufti holds iBeta Level 3, held by only three vendors globally, plus full-stack ownership for on-timeline defence updates. AU10TIX is a specialist for synthetic-identity fraud. Confirm with a proof of concept on your own traffic.

Which KYC solution suits mid-sized financial institutions needing global coverage?

Mid-sized institutions needing global coverage should prioritise active document accuracy over catalogue size. Shufti verifies 10,000+ document types monthly across 220+ countries and jurisdictions, actively processed with 99.7% OCR accuracy across 150+ languages. Trulioo is a narrower fit where non-document data aggregation matters more than document verification.

Which KYC verification software handles many document types and countries?

Several vendors publicise large catalogues, but actively verified volume matters more. Shufti actively verifies 10,000+ document types across 220+ countries and jurisdictions, actively processed monthly; Sumsub publicises 14,000+ document types and Trulioo 14,000+ across 195 countries. Compare active accuracy on your specific markets, not lifetime catalogue counts.

What are the top real-time identity verification tools for banks?

Banks typically shortlist Shufti, AU10TIX, IDnow, Jumio, Entrust, Persona, Socure, Sumsub, Trulioo, and Veriff. The right choice depends on coverage, independent liveness conformance, deployment flexibility, and AML integration depth, weighed against the bank's markets and regulatory regime.

What is the best KYC software for global fintech compliance?

For global fintech compliance, the cleanest answer is a platform with owned KYC and AML under one audit trail, broad real-world coverage, and deployment flexibility. Shufti combines full-stack ownership, 220+ countries and jurisdictions, actively processed, iBeta Level 3 conformance, and SaaS, Local Cloud, and on-premises deployment, supporting eIDAS 2.0 and AMLA-aligned monitoring.

: Meaning, Requirements, and When You Need One")