Face Verification

Face Verification

Address Verification

Address Verification

Document Verification

Document Verification

Age Verification

Age Verification

VideoIdent

VideoIdent

Fast ID

Fast ID

Docless Verification

Docless Verification

Consent Verification

Consent Verification

NFC Verification

NFC Verification

Business Verification

Business Verification

Due Diligence

Due Diligence

Investor Verification

Investor Verification

E-Signature

E-Signature

QES

QES

AML Screening

AML Screening

Transaction Monitoring

Transaction Monitoring

Adverse Media

Adverse Media

Business AML Screening

Business AML Screening

PEP & RCA

PEP & RCA

Sanctions

Sanctions

Watchlist

Watchlist

Behavioural Biometrics

Behavioural Biometrics

Device Fingerprinting

Device Fingerprinting

Biometric Face Authentication

Biometric Face Authentication

MFA

MFA

Fraud Hub

Fraud Hub

Onboarding

Onboarding

Ongoing Monitoring

Ongoing Monitoring

KYC

KYC

KYB

KYB

KYI

KYI

Age Assurance

Age Assurance

Identity Verification

Identity Verification

Workforce IAM

Workforce IAM

Candidate Verification

Candidate Verification

Compliance

Compliance

Fraud prevention

Fraud prevention

Trust & safety

Trust & safety

Global expansion

Global expansion

Product Managers

Product Managers

Compliance Officers

Compliance Officers

Fraud Analysts

Fraud Analysts

Developers

Developers

Deepfake

Deepfake

Bonus Abuse / Promotion Abuse

Bonus Abuse / Promotion Abuse

Account Takeover

Account Takeover

Synthetic Identity Fraud

Synthetic Identity Fraud

Document Fraud

Document Fraud

Impersonation Fraud

Impersonation Fraud

Multi-Accounting

Multi-Accounting

Fraud Networks

Fraud Networks

Chargeback Fraud

Chargeback Fraud

Money Mule Activity

Money Mule Activity

Party Fraud

Party Fraud

Regulatory & Compliance Risks

Regulatory & Compliance Risks

Fintech

Fintech

Crypto

Crypto

iGaming

iGaming

Forex

Forex

Social Network

Social Network

Marketplace

Marketplace

Banking

Banking

Gig Economy

Gig Economy

Payments

Payments

Ride Hailing

Ride Hailing

Adult Content

Adult Content

Blind Spot Audit

Blind Spot Audit

Deepfake Detector

Deepfake Detector

Liveness Spoofs

Liveness Spoofs

Document Originality

Document Originality

Document Deepfake

Document Deepfake

Global Trust Platform

Global Trust Platform

Journey Builder

Journey Builder

Case Management

Case Management

Shufti AI

Shufti AI

Fraud Analytics

Fraud Analytics

Vendor Comparison

Vendor Comparison

Brand Personalisation

Brand Personalisation

IDV Modes

IDV Modes

AI Compliance Co-Pilot

AI Compliance Co-Pilot

OCR

OCR

Secure Capture

Secure Capture

Deployment Options

Deployment Options

Identity Methods

Identity Methods

API Documentation

API Documentation

Mobile SDKs

Mobile SDKs

Service Status

Service Status

Help Center

Help Center

Contact Us

Contact Us

Technical Support

Technical Support

Supported Documents

Supported Documents

Supported Countries

Supported Countries

Content library

Content library

Blogs

Blogs

News

News

Reports

Reports

Insights

Insights

Knowledgebase

Knowledgebase

ROI calculator

ROI calculator

About

About

Career

Career

Press Release

Press Release

Certifications

Certifications

Partnership

Partnership

Awards

Awards

Events & Webinar

Events & Webinar

Interactive Demo

Interactive Demo

Podcast Studio

Podcast Studio

Spotlight Studio

Spotlight Studio

KYC During Crisis: How to Keep Compliance Running When Conditions Break Down

|

Key Takeaways

|

The call arrived on a Friday. A KYC provider serving hundreds of financial institutions announced it was exiting the market within 30 days. Compliance teams had to source, integrate, and re-validate an alternative while maintaining uninterrupted customer verification and satisfying regulators who had not paused their expectations.

Provider failures are one category of crisis. Economic downturns, regulatory emergencies, and rapid-growth onboarding surges belong to the same family. KYC (Know Your Customer) programmes are designed for stable operating conditions. When those conditions break down, most programmes show their weaknesses fast.

This article maps what crisis conditions do to KYC operations, what regulators actually permit under those conditions, and what infrastructure decisions separate teams that cope from teams that freeze.

Why KYC risk multiplies in a crisis?

Crises do not suspend the need for identity verification. They amplify it. Fraud rates accelerate whenever normal verification channels are disrupted. Financial institutions face heavier onboarding volumes, tighter staff capacity, and in some cases provider gaps that force manual fallback procedures. Each pressure compounds the others, and they tend to arrive simultaneously.

Financial crime accelerates in a downturn

When economic conditions deteriorate, financial crime rates rise in parallel. In 2023, approximately $3.1 trillion in illicit funds circulated within the global financial system, according to the Nasdaq Verafin 2024 Global Financial Crime Report. The IMF estimates that between 2% and 5% of global GDP is laundered annually. These figures describe baseline conditions. Under crisis conditions, the pressure on KYC programmes as a first line of defence becomes substantially heavier.

Fraudsters exploit the same disruptions that stress compliance teams. Strained staff, overloaded systems, and the temporary relaxation of verification checks all factor in together. A team that has made permissible simplifications under pressure is more exposed when the crisis resolves and regulators begin reviewing what happened during the period. For more on how financial crime pressures interact with KYC obligations, the KYC and AML compliance overview covers the structural relationship between the two disciplines.

Single points of failure in the vendor chain

Operational risk inside a KYC programme is easy to underestimate when nothing has gone wrong. A PwC 2024 Global Economic Crime Survey of 2,500 respondents across 63 territories found that 42% of companies lack a third-party risk management programme or any form of vendor risk scoring. That means nearly half of the organisations surveyed had no structured way to assess what would happen if a verification provider failed, got acquired, or exited a market.

For teams that have never had to invoke a contingency plan, the first crisis becomes an expensive governance lesson rather than a managed transition.

What do regulators actually allow in an emergency?

One of the most persistent assumptions in compliance is that KYC rules are immovable. In practice, the major regulatory frameworks include specific provisions for risk-based simplification under exceptional circumstances. Understanding what is actually permitted, and what remains non-negotiable, allows a compliance team to maintain operations without either pausing onboarding or quietly dropping below acceptable thresholds. Teams managing verification across multiple jurisdictions face additional complexity here, which the cross-border KYC compliance guide addresses in detail.

FATF and simplified due diligence

FATF’s Recommendations, specifically Recommendation 10, allow financial institutions to apply simplified customer due diligence where the risk of money laundering or terrorist financing is demonstrably lower. This is not a blanket exemption. It is a risk-based permission, available when the institution has documented the reduced risk and the jurisdiction’s supervisory framework supports the simplification.

Applying simplified CDD in a crisis typically means reduced document requirements for lower-risk customer segments, extended timelines for certain verification steps, or the use of alternative identity evidence where primary documents are unavailable. The key requirement in all cases is documentation. The institution must be able to demonstrate, after the fact, that each simplification was justified by the risk profile of the individual customer.

Regulatory relief in the United States

During the COVID-19 pandemic, the US Federal Reserve issued guidance allowing financial institutions to apply flexible CDD measures while maintaining full AML obligations. The New York Department of Financial Services similarly provided temporary regulatory relief, including extended timelines for certain compliance filings.

The consistent thread across both responses was that AML monitoring obligations were not suspended. Regulators relaxed the mechanics of identity verification. Accepted document types, available channels, and turnaround timelines could all flex. What did not flex was the underlying obligation to verify and screen. Institutions that treated the guidance as permission to reduce financial crime controls entirely found themselves in difficulty when supervisory examinations resumed.

How should you handle a KYC onboarding surge?

A crisis does not only mean contraction. For fintechs entering a market under deadline, betting platforms launching with regulatory KYC requirements, or financial institutions absorbing customers from a failing competitor, a crisis can arrive as a flood of new onboarding requests at exactly the moment when internal capacity is most stretched.

Triage by risk profile

Not all customers require the same depth of verification on day one. A risk-tiered approach lets a compliance team under pressure run full standard due diligence on higher-risk segments, apply simplified CDD where permissible to demonstrably lower-risk applicants, and queue enhanced due diligence cases for resolution within a defined window rather than as a condition of onboarding.

The triage logic needs to exist as a written policy before a surge arrives. Teams that build the risk matrix during the crisis spend time on governance decisions instead of customer verification.

Automation as a surge buffer

Manual workflows break under volume. A KYC automation approach converts the high-volume, lower-complexity layer of verification into a systems problem rather than a staffing problem. Document capture, liveness checks, sanctions screening, and data extraction can all be handled without a manual reviewer for standard cases, reserving analyst capacity for edge cases and enhanced due diligence that require human judgment.

Automation also creates an audit trail that manual processes cannot match. Every verification decision is logged with timestamps, the data examined, and the outcome recorded. During a crisis, that record becomes the documentation regulators expect to see during post-event review.

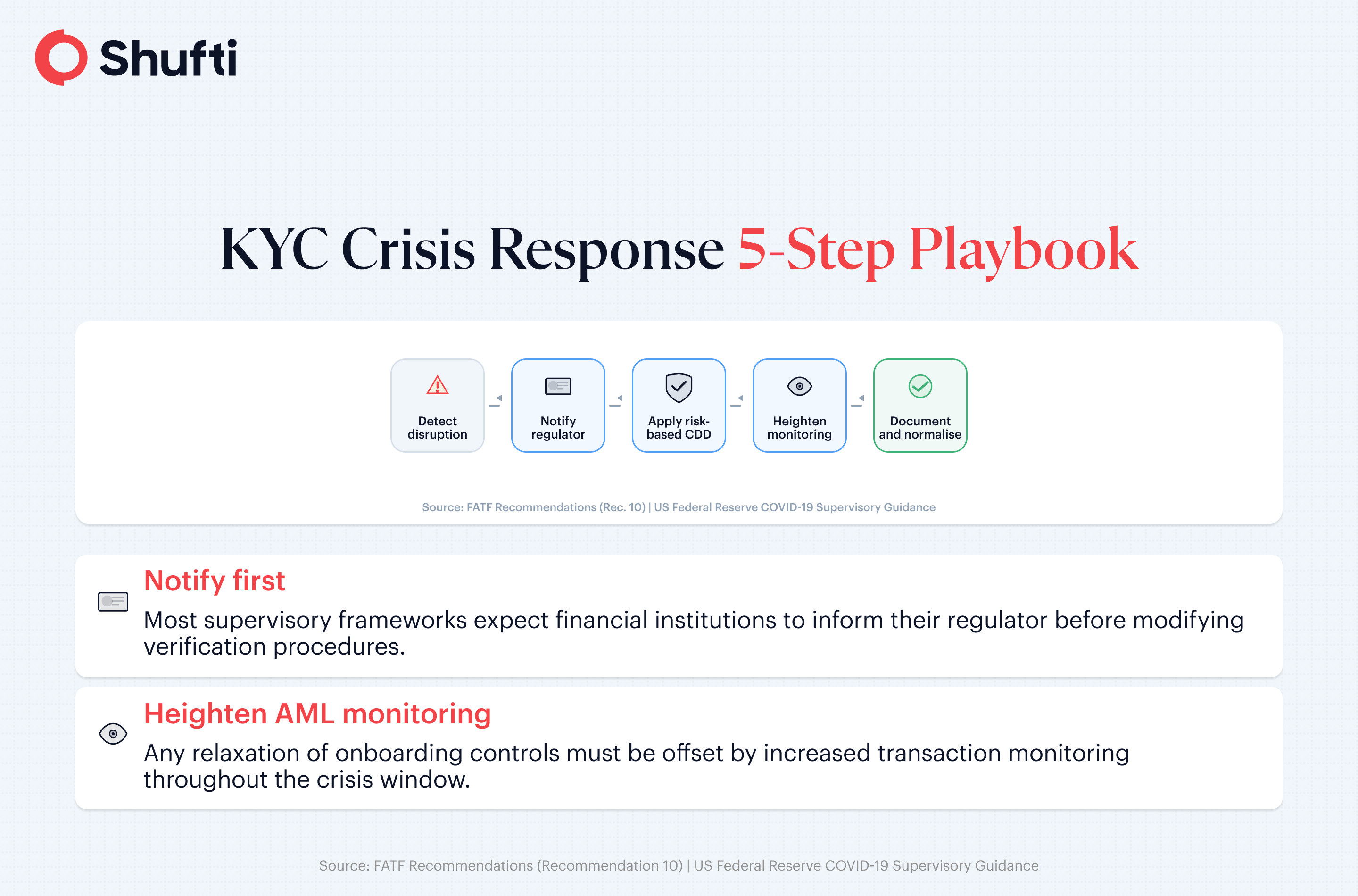

How to run KYC during a crisis: a practical playbook?

Documenting a crisis response framework before a crisis arrives is the single most undervalued task in compliance programme management. Most teams know, in general, what they would do. Fewer have written it down, tested it, and assigned ownership to each step. The five-step framework below reflects the FATF risk-based approach and is consistent with the regulatory guidance issued during recent periods of financial disruption.

Step 1: Detection

Identify whether normal operating conditions have changed in a way that is material enough to invoke the crisis framework. Triggers might include a provider outage, a regulatory announcement, a volume spike beyond defined thresholds, or an internal systems failure.

Step 2: Regulator notification

Most supervisory frameworks expect financial institutions to inform their regulator when operating under modified conditions. The notification creates a record and, in most jurisdictions, protects the institution against later criticism for the modifications made during the period.

Step 3: Risk-based due diligence adjustment

Apply risk-based CDD adjustments within the limits of the applicable regulatory framework, following the simplified due diligence provisions available in the jurisdiction. Every adjustment should be documented at the individual customer level.

Step 4: Heightened monitoring

Relaxation of onboarding controls must be offset by increased transaction monitoring intensity during the crisis window. The AML compliance framework supports this through continuous screening and real-time alert escalation, precisely the conditions where ongoing monitoring intensity matters most.

Step 5: Normalisation

When operating conditions restore, the institution re-applies its standard verification programme to accounts onboarded under simplified procedures, within a timeline agreed with the regulator. The global KYC compliance guide covers jurisdiction-specific normalisation requirements across major markets.

How Shufti helps compliance teams maintain KYC during a crisis

The teams that cope best during a crisis are the ones whose KYC infrastructure was built to handle variance. That means automated verification that processes identity checks in under 15 seconds regardless of volume, deployment options that continue functioning when cloud infrastructure in a specific region faces disruption, and AML screening that maintains coverage across 3,500+ global watchlists even when other systems are under stress.

Shufti’s Know Your Customer platform processes identity checks with 99.3% fraud detection accuracy, with no manual queue between document capture and the verification decision. For compliance teams managing an onboarding surge, that speed and automation removes the principal bottleneck that breaks manual programmes under volume. For teams managing a provider-failure scenario, Shufti’s cloud, on-premises, and hybrid deployment options mean migration does not require rearchitecting the verification pipeline from scratch.

The AML screening layer runs continuously alongside identity verification, so heightened monitoring during a crisis does not require a separate system or a separate integration project. The compliance programme maintains its posture without adding operational complexity at the moment when complexity is already highest.

|

When a KYC programme depends on manual processes or a single provider with no contingency plan, the first crisis exposes that gap at the worst possible time. Shufti’s AI-powered identity verification infrastructure is built for operational continuity under pressure, with flexible deployment options and fraud detection that holds regardless of how conditions change. To see how Shufti supports compliance teams during high-stress onboarding periods, visit the KYC platform page to request a demo or start a free trial. |

Frequently Asked Questions

What happens to KYC requirements during a crisis?

KYC requirements remain in force during a crisis, but the major regulatory frameworks, including FATF Recommendation 10, permit risk-based simplifications to customer due diligence where the money laundering or terrorist financing risk is demonstrably lower. AML monitoring obligations are not suspended. Any simplification must be documented at the individual customer level and reviewed when normal conditions resume.

Can KYC rules be relaxed in emergencies?

Yes, within defined limits. Regulators including the US Federal Reserve and the New York Department of Financial Services issued guidance during the COVID-19 pandemic allowing flexible CDD measures, such as alternative document types and extended timelines for certain verification steps. These accommodations changed how verification was conducted, not the underlying obligation to verify and screen. Institutions that applied simplifications without documentation faced difficulties during post-crisis supervisory reviews.

How do banks handle KYC during financial crises?

Banks typically apply a risk-tiered approach. Full enhanced due diligence continues for higher-risk customers. Simplified CDD applies where the regulatory framework permits, and complex cases are deferred to a defined resolution window. Prompt notification to the relevant regulator is standard practice. The institutions that managed the 2020 pandemic period most effectively were those with documented crisis procedures and automated KYC infrastructure that could sustain volume without depending on manual reviewer capacity.

How to handle onboarding surges without dropping compliance standards?

Automation is the primary mechanism. Document capture, liveness detection, and sanctions screening handled by an automated KYC system remove the volume bottleneck from the manual review queue. Risk tiering means complex cases receive proportionate scrutiny rather than the same simplified process applied uniformly.

What are the best practices for KYC during global crises?

The most consistent practices across regulated industries include maintaining a documented crisis response framework before conditions change, applying risk-based CDD adjustments within the limits of applicable regulatory guidance, offsetting simplifications with heightened transaction monitoring, notifying the regulator promptly, and running a remediation cycle for accounts verified under simplified procedures once normal conditions restore. © 2026 Shufti Pro. All rights reserved. | shuftipro.com