Face Verification

Face Verification

Address Verification

Address Verification

Document Verification

Document Verification

Age Verification

Age Verification

VideoIdent

VideoIdent

Fast ID

Fast ID

Docless Verification

Docless Verification

Consent Verification

Consent Verification

NFC Verification

NFC Verification

Business Verification

Business Verification

Due Diligence

Due Diligence

Investor Verification

Investor Verification

E-Signature

E-Signature

QES

QES

AML Screening

AML Screening

Transaction Monitoring

Transaction Monitoring

Adverse Media

Adverse Media

Business AML Screening

Business AML Screening

PEP & RCA

PEP & RCA

Sanctions

Sanctions

Watchlist

Watchlist

Behavioural Biometrics

Behavioural Biometrics

Device Fingerprinting

Device Fingerprinting

Biometric Face Authentication

Biometric Face Authentication

MFA

MFA

Fraud Hub

Fraud Hub

Onboarding

Onboarding

Ongoing Monitoring

Ongoing Monitoring

KYC

KYC

KYB

KYB

KYI

KYI

Age Assurance

Age Assurance

Identity Verification

Identity Verification

Workforce IAM

Workforce IAM

Candidate Verification

Candidate Verification

Compliance

Compliance

Fraud prevention

Fraud prevention

Trust & safety

Trust & safety

Global expansion

Global expansion

Product Managers

Product Managers

Compliance Officers

Compliance Officers

Fraud Analysts

Fraud Analysts

Developers

Developers

Deepfake Detection

Deepfake Detection

Bonus Abuse / Promotion Abuse

Bonus Abuse / Promotion Abuse

Account Takeover

Account Takeover

Synthetic Identity Fraud

Synthetic Identity Fraud

Document Fraud

Document Fraud

Impersonation Fraud

Impersonation Fraud

Multi-Accounting

Multi-Accounting

Fraud Networks

Fraud Networks

Chargeback Fraud

Chargeback Fraud

Money Mule Activity

Money Mule Activity

Party Fraud

Party Fraud

Regulatory & Compliance Risks

Regulatory & Compliance Risks

Fintech

Fintech

Crypto

Crypto

iGaming

iGaming

Forex

Forex

Social Network

Social Network

Marketplace

Marketplace

Banking

Banking

Gig Economy

Gig Economy

Payments

Payments

Ride Hailing

Ride Hailing

Adult Content

Adult Content

Blind Spot Audit

Blind Spot Audit

Deepfake Detector

Deepfake Detector

Liveness Spoofs

Liveness Spoofs

Document Originality

Document Originality

Document Deepfake

Document Deepfake

Global Trust Platform

Global Trust Platform

Journey Builder

Journey Builder

Case Management

Case Management

Shufti AI

Shufti AI

Fraud Analytics

Fraud Analytics

Vendor Comparison

Vendor Comparison

Brand Personalisation

Brand Personalisation

AI Compliance Co-Pilot

AI Compliance Co-Pilot

OCR

OCR

Secure Capture

Secure Capture

Deployment Options

Deployment Options

Identity Methods

Identity Methods

API Documentation

API Documentation

Mobile SDKs

Mobile SDKs

Service Status

Service Status

Help Center

Help Center

Contact Us

Contact Us

Technical Support

Technical Support

Supported Documents

Supported Documents

Supported Countries

Supported Countries

Content library

Content library

Blogs

Blogs

News

News

Reports

Reports

Insights

Insights

Knowledgebase

Knowledgebase

ROI calculator

ROI calculator

About

About

Career

Career

Press Release

Press Release

Certifications

Certifications

Partnership

Partnership

Awards

Awards

Events & Webinar

Events & Webinar

Interactive Demo

Interactive Demo

Podcast Studio

Podcast Studio

Spotlight Studio

Spotlight Studio

KYC vs AML vs KYB: Key Differences Explained

Global compliance penalties tied to KYC, AML, and KYB failures totalled $3.8 billion in 2025, according to the Institute for Financial Integrity, with enforcement shifting sharply from North America to EMEA and APAC. Most of those penalties trace back to one pattern. Compliance teams treat KYC, AML, and KYB as separate programmes rather than as a coordinated stack, and the gaps between them become the liability. This article breaks down what each framework does, where they differ, and why all three need to work together.

What is the difference between KYC, AML, and KYB?

Understanding what KYC, AML, and KYB each require starts with recognising that they operate at different layers of your compliance programme. KYC covers individual identity at the point of onboarding; KYB extends that logic to corporate clients; AML is the broader framework that governs both and that continues well beyond onboarding into ongoing risk surveillance. Treating any one of the three as the whole is what produces the audit gaps regulators flag most consistently.

What is KYC (Know Your Customer)?

Know Your Customer (KYC) is the process of verifying the identity of individual customers before or during onboarding. It covers document verification, including passports, national IDs, and driver’s licences, alongside biometric checks such as facial matching and liveness detection, and a customer due diligence (CDD) assessment that assigns an initial risk rating. KYC requirements derive from frameworks such as the Financial Action Task Force (FATF) Recommendations and national legislation including the Bank Secrecy Act (BSA) in the United States. The outcome is a verified identity record tied to a customer risk profile.

What is AML (Anti-Money Laundering)?

Anti-Money Laundering (AML) is the regulatory framework inside which KYC sits. AML obliges financial institutions and regulated businesses to detect, prevent, and report transactions that may represent proceeds of crime. In practice, that means sanctions screening, Politically Exposed Persons (PEP) checks, adverse media monitoring, and transaction surveillance across the full customer lifecycle. FATF estimates that money laundering represents 2 to 5 percent of global GDP annually, an exposure that explains why AML obligations extend far beyond the initial onboarding check. The difference between KYC and AML matters most when scoping a compliance programme. KYC delivers the verified identity data that AML monitoring depends on, but AML does not stop when KYC is done.

What is KYB (Know Your Business)?

Know Your Business (KYB) applies KYC-level scrutiny to corporate entities rather than individuals. When onboarding a business client or a B2B counterparty, KYB requires verifying company registration, ownership structure, and the Ultimate Beneficial Owners (UBOs) who control the entity. FinCEN’s beneficial ownership reporting rules, reinforced by the US Corporate Transparency Act, reflect the global push to surface the real individuals behind corporate structures, a risk layer that standard KYC cannot reach. KYB sits inside AML obligations but targets the corporate layer that consumer-grade identity checks leave unverified.

How do KYC vs AML and KYB work as a compliance stack?

Understanding KYC vs AML is most productive when you treat them as layers rather than parallel programmes running independently. AML sets the obligation; KYC and KYB supply the verified identity data that makes AML monitoring meaningful. When a sanctions hit surfaces six months after onboarding, the investigation depends on a clean KYC record from day one. When that record sits in a separate system from the AML alert, the audit trail breaks, and that breakdown is precisely what regulators penalise.

US regulators issued $4.3 billion in financial penalties in 2024, with banks accounting for 82 percent of fines levied, according to Corporate Compliance Insights. The majority of enforcement actions cited gaps between identity verification and ongoing monitoring. This is the gap that opens when KYC vs KYB vs AML compliance runs through disconnected vendors. The EU’s Anti-Money Laundering Authority (AMLA), operational from mid-2025, is designed to close that gap at the regulatory level by standardising how member states implement both the identity-check and the ongoing monitoring layer under one framework.

AI has changed how all three functions operate. Machine learning now drives document forgery detection in KYC, entity graph analysis in KYB, and real-time risk scoring in AML monitoring. These capabilities compound when they share a data layer. A biometric match at onboarding should inform the AML risk score applied to the same customer later. Platforms that connect the three on a single API deliver this. Those that don’t create the fragmented stacks that regulators are most consistently penalising. For how KYC, KYB, and transaction monitoring connect at the workflow level, see the KYC, KYB and KYT compliance overview.

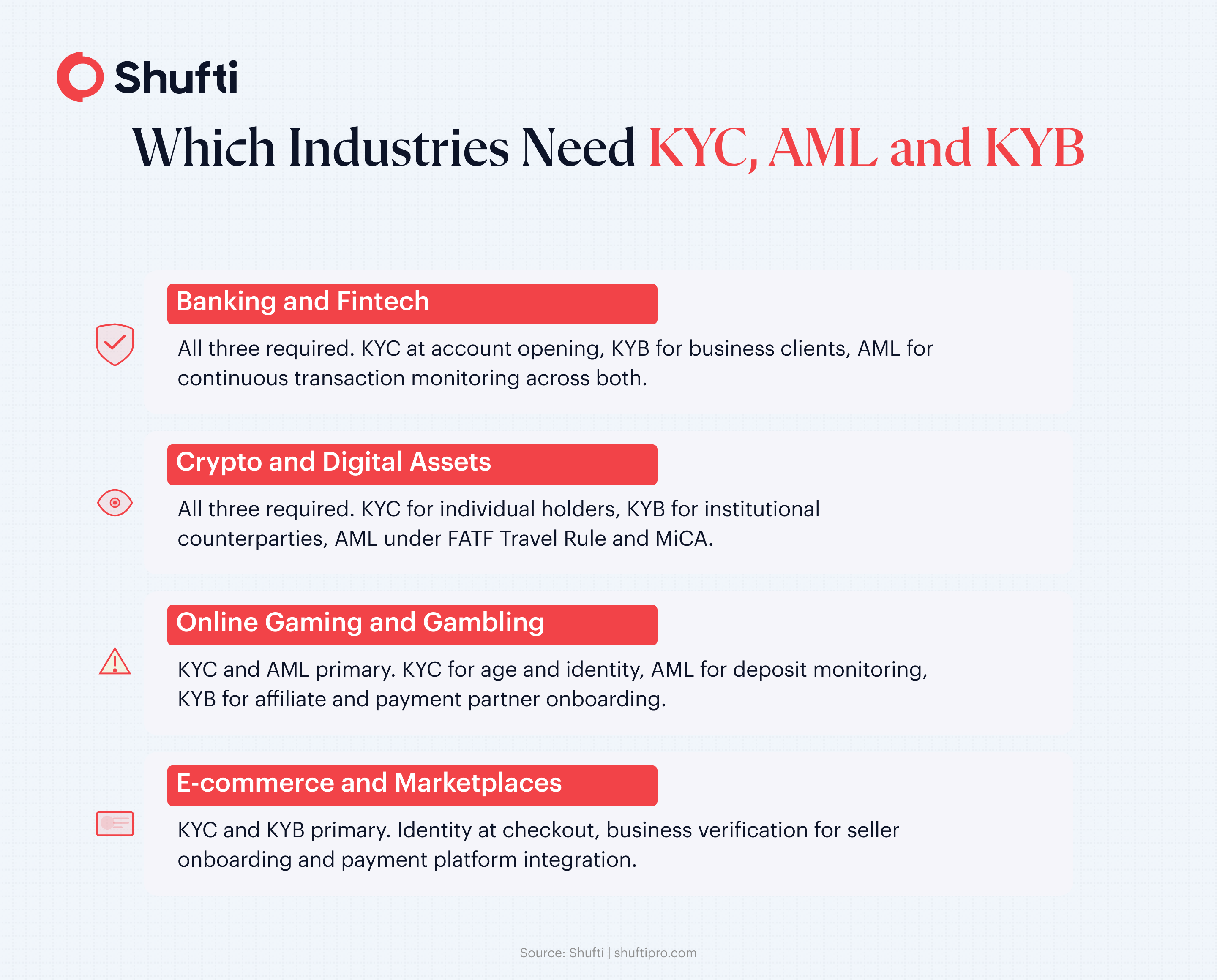

Which industries need KYC, AML, and KYB compliance?

The KYB vs KYC distinction determines which verification process applies to a given onboarding flow, and that split varies by sector. Most regulated industries globally must run some combination of all three frameworks, but the balance shifts depending on whether you are onboarding individuals, corporate entities, or both. Understanding where your regulator places the most weight helps compliance teams sequence their programmes without over-engineering every flow.

Banking and fintech

Banks and fintech platforms carry the most comprehensive obligations across all three areas. KYC applies to individual account opening. Business verification requirements govern corporate accounts, SME lending, and business banking relationships. AML governs continuous transaction monitoring across both. The FCA, the European Banking Authority (EBA), and FinCEN each publish guidance that treats the three as a unified compliance obligation, not a menu. For digital banks, elevated identity fraud risk at the application stage and stricter beneficial ownership checks for corporate clients make a connected compliance stack a licensing requirement rather than a strategic choice.

Crypto and digital assets

Crypto exchanges and virtual asset service providers (VASPs) operate under AML obligations in every major jurisdiction, including the FATF Travel Rule, the EU’s Markets in Crypto-Assets Regulation (MiCA), and BSA requirements administered by FinCEN. KYC applies to individual account holders; KYB applies to institutional clients and corporate counterparties. Transaction monitoring in crypto carries the added complexity of wallet anonymity and cross-chain flows, which makes continuous AML screening harder to automate than in traditional finance. For a full breakdown of regulatory timelines across regions, the KYC compliance regulations guide covers current global requirements.

Online gaming and gambling

Gaming and gambling operators require KYC for age verification and identity confirmation, AML for monitoring deposit and withdrawal patterns that signal layering, and KYB when onboarding affiliates, payment processors, or game publishers as business partners. Regulators including the UK Gambling Commission treat AML failures in this sector as a priority enforcement area, given its documented exposure to layering and placement schemes. Operators that apply KYC rigour at the player level without equivalent scrutiny on business partners carry a compliance gap that regulators increasingly flag.

How Shufti helps businesses run KYC, AML, and KYB

A fragmented KYC, AML, and KYB stack creates an audit trail problem that becomes a regulatory liability. When an AML screening hits the surface on a customer who passed identity verification six months earlier, the compliance team needs a single record connecting both events. Disconnected systems rarely produce one.

Shufti connects identity verification and AML screening on one platform. The KYC identity record from onboarding feeds directly into ongoing sanctions, PEP, and adverse media monitoring without requiring a separate system lookup. The AML layer covers 100,000+ data sources and 3,500+ global watchlists, updated every 15 minutes, so a risk change post-onboarding surfaces in the same workflow the compliance team already uses. KYB checks reach across 250+ countries, covering UBO identification, company registry lookups, and corporate structure mapping without a manual handoff. The result is a connected compliance record, not three separate reports.

When fragmented compliance stacks create audit gaps between identity verification and ongoing risk monitoring, regulators treat it as a systemic failure, not an oversight. Shufti connects KYC, KYB, and AML monitoring through a single API so compliance teams have one audit trail, not three. Request a demo to see how the full stack runs on your own onboarding volumes.

Frequently Asked Questions

How do KYC, KYB, and AML relate to each other?

AML is the overarching regulatory obligation. KYC and KYB are how businesses fulfil the identity-verification portion of that obligation. After identity is confirmed, AML requires continuous monitoring, including sanctions, PEP checks, and adverse media, that applies to both individual customers verified through KYC and corporate clients verified through KYB.

Is AML the same as KYC, or is it a broader framework?

AML is broader. KYC covers the identity-verification step at onboarding. AML extends to transaction monitoring, suspicious activity reporting, sanctions screening, and adverse media checks that run throughout the customer relationship, not just at sign-up.

Why do businesses need KYC, AML, and KYB together?

Each framework covers a different risk layer. KYC confirms who an individual is. KYB confirms who controls a business. AML monitors for financial crime signals across both. A single platform for all three prevents audit gaps where a risk event in one layer is invisible in another.

How is AI used in KYC, AML, and KYB processes?

AI powers document forgery detection in KYC, entity graph analysis in KYB, and real-time risk scoring in AML monitoring. Platforms that share a data layer across all three allow a biometric flag at KYC onboarding to inform the AML risk score applied to the same customer. CMS Note: FAQPage schema markup required.

: Meaning, Requirements, and When You Need One")