Key Takeaways:

- Reusable KYC separates the verification event from the ongoing KYC obligation, letting a prior compliant verification satisfy the identity requirements of a new service.

- Three architecture models are in active use today: centralised credential stores, federated identity networks, and decentralised wallets built on W3C Verifiable Credentials.

- FATF’s 2020 Guidance on Digital Identity explicitly accommodates third-party reliance on prior verification, subject to assurance-level matching and access to the underlying evidence.

- Regulation (EU) 2024/1183 (eIDAS 2.0) requires all 27 EU member states to provide citizens with Digital Identity Wallets by end of 2026, making portable identity a regulatory obligation rather than a product decision.

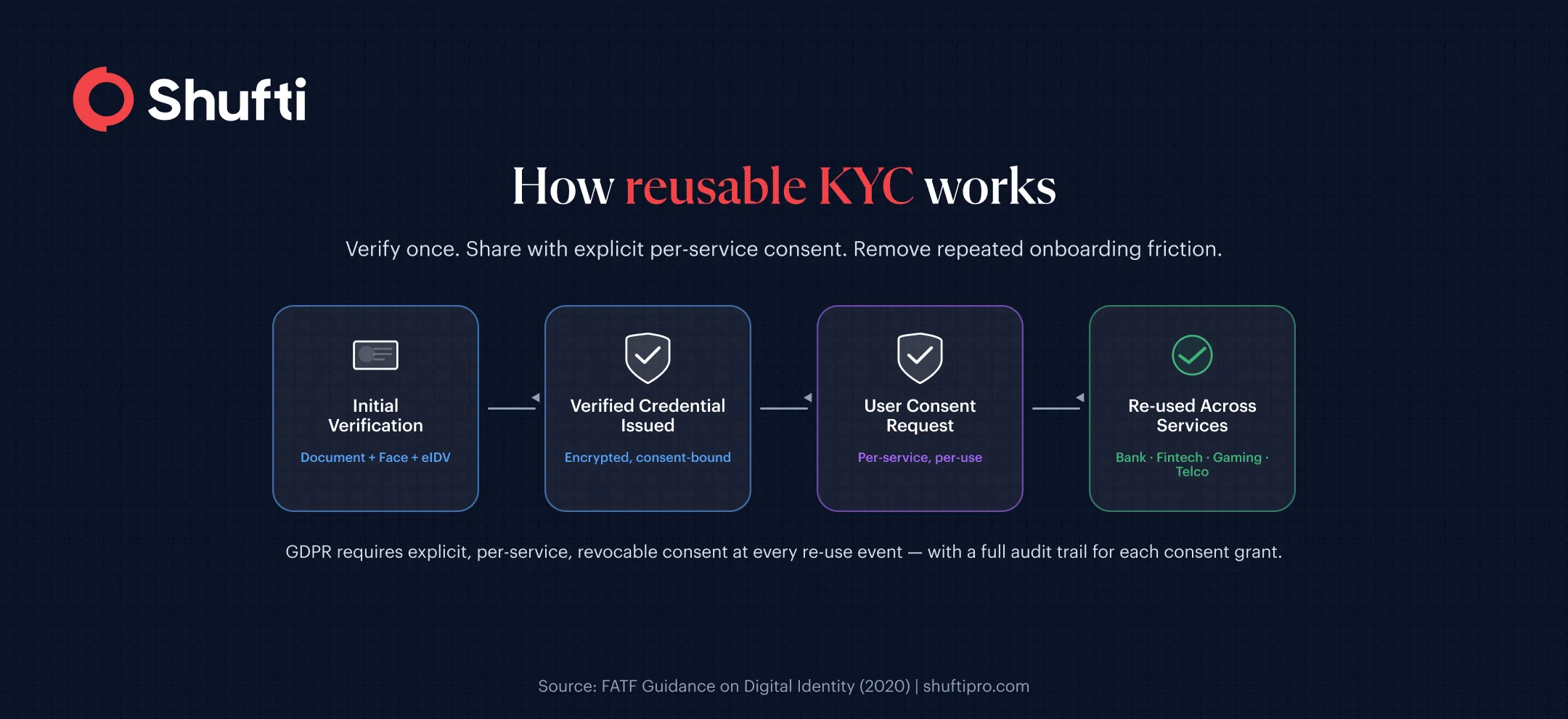

- GDPR requires explicit, per-service, revocable consent for every use of a reusable credential, with full audit logging for each consent event.

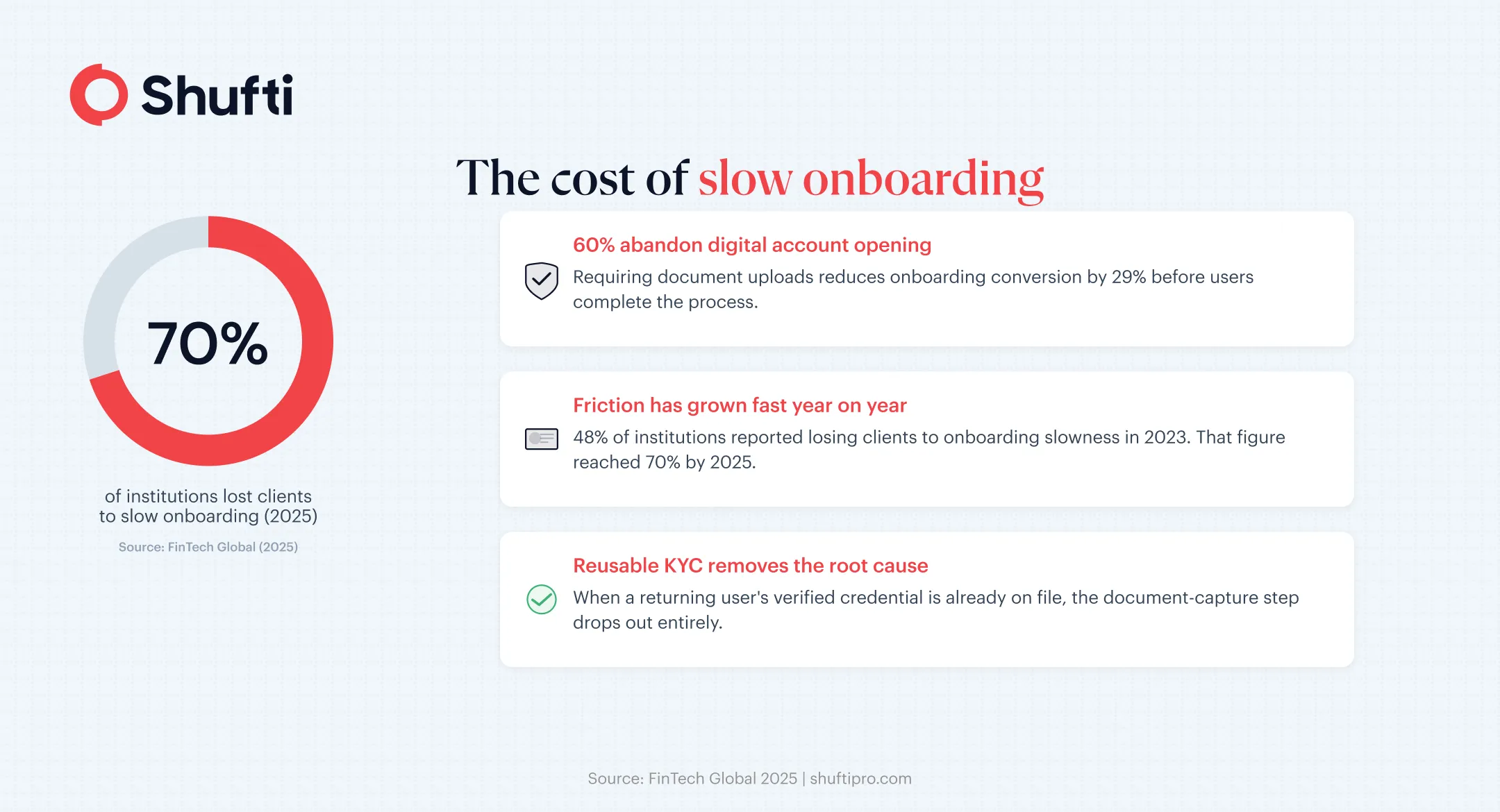

- Up to 60% of digital bank account applicants abandon the process before completion, and requiring document uploads alone reduces conversion by 29%.

|

What is reusable KYC? Reusable KYC is a model in which an identity is verified once through a compliant process, and the resulting verified credential is stored in a form that allows other services to confirm that identity without repeating the full verification. Each subsequent use requires explicit per-service consent from the user, and the original verification evidence must remain accessible to relying parties on regulatory request. |

Your user has already verified their identity three times this year — once for a neobank, once for a crypto exchange, and once for a payment wallet. Each time they uploaded a passport photo, completed a liveness check, and waited for the result. Now they are opening an account with your platform, and your onboarding flow is about to ask them to do it again. According to FinTech Global, 70% of financial institutions worldwide lost clients over the past year due to slow and inefficient onboarding, up from 48% in 2023. The repeated identity check is not a minor friction point. For a substantial share of those users, it is the reason they left.

Reusable KYC addresses that structural problem. A user’s identity is verified once through a compliant, evidence-based process, and the resulting verified credential travels with the user, allowing subsequent services to confirm identity without repeating the full document and biometric sequence. Consent is granted per service, credentials are auditable, and the original verification evidence stays accessible to relying parties on regulatory request.

This guide explains what reusable KYC means, walks through the three architecture models currently in active use, maps each to its regulatory footing under FATF guidance and eIDAS 2.0, and covers the GDPR consent lifecycle that makes portable identity defensible in practice. If you are evaluating whether this model is legally sound and operationally viable for your platform, start here.

What reusable KYC actually means

Traditional KYC compliance treats every institution as its own verification silo. A bank verifies a customer. A payment platform verifies the same customer. A gambling operator verifies that customer again. Each institution holds a separate copy of documents, biometric data, and verification outcomes. None of that prior work transfers. None of the assurance built by the first verifier benefits the second.

Reusable KYC breaks the silo by separating two functions that traditional KYC bundles together. The first is the verification event — the process of collecting and validating evidence about an identity, typically a government-issued document, a biometric match, and in some cases a database cross-reference against government or financial records. The second is the ongoing KYC obligation, which covers managing risk for a specific customer relationship over time.

Under a reusable model, the verification event can be delegated to a trusted prior verifier. The relying party still holds its own KYC obligation, but it can discharge part of that obligation by relying on a credential and audit trail from the prior verification. What the relying party receives is not raw document imagery but a signed attestation describing the verification method, date, assurance level reached, and the determination that the evidence met the required standard. The relying party then decides whether that assurance level meets its own risk threshold for the specific product or customer category.

How reusable KYC differs from traditional KYC

The practical difference surfaces in the second, third, and fourth onboarding events. A user already verified to a high assurance level by a regulated institution can, with their consent, present that credential to a new platform. The new platform receives a machine-readable, cryptographically signed assertion rather than a document image for review. No manual queue. No re-capture. No waiting.

Compliance obligations for the relying party do not disappear. They still need to assess the risk profile of the new relationship, log the verification event with the credential details, and retain the ability to retrieve the underlying evidence if a regulator asks. What changes is the source of that evidence, from a fresh, duplicated verification effort to a trusted prior one.

Why conversion data makes this a product priority

Research from Markswebb found that up to 60% of users abandon digital bank account applications before completing them, and that requiring identity document uploads reduces conversion by 29%. For a high-volume consumer platform, recovering even five percentage points of that abandonment translates directly into revenue. When a returning user’s credential is already on file and their per-service consent is a single acknowledgment step, the document-capture and liveness friction that drives most abandonment drops out of the flow entirely.

Three architecture models for reusable identity

51% of digital identity providers are now involved in issuing reusable or portable digital identities, according to the UK Government’s 2025 Digital Identity Sectoral Analysis. How those identities are issued, stored, and shared varies across three structurally distinct approaches, each with its own trust model, liability profile, and regulatory fit.

Centralised credential store

In the centralised model, a single organisation holds verified credentials for enrolled users. That organisation may be a regulated entity, a bank-owned utility, or a third-party IDV provider. When a relying party needs to verify someone, it queries the central store. The user authenticates, grants per-service consent, and the store returns the verification result.

The appeal is operational simplicity. Credential freshness, audit logging, and consent management sit in a single system. The liability for the underlying verification stays with the issuing organisation, creating a clear accountability chain for regulators. One system to audit is easier than a distributed web of bilateral agreements.

Concentration risk is the main trade-off. A central credential store is a high-value target for data breaches, and any outage affects all relying parties at once. Regulators in heavily scrutinised sectors, particularly banking and payments, sometimes require the store to be operated by a regulated entity whose governance matches the sensitivity of the data it holds.

Federated identity network

A federated model distributes credential issuance and verification across multiple institutions that agree on a shared standard. No single organisation holds the master repository. Institutions that have already verified a user can attest to that verification for other institutions in the network.

The banking sectors work on KYC utilities reflects this model. Several jurisdictions have built or are exploring national KYC-sharing registries, where licensed banks can confirm whether another licensed institution has already completed a satisfactory verification for a given customer. The electronic identity verification infrastructure underpinning these registries varies by market, but the principle holds. Verification performed to an agreed standard by an approved institution satisfies the obligations of other network members, subject to each member’s own risk-based assessment.

Federation scales well across peer institutions sharing a regulatory framework. Its challenge is governance. Agreeing on shared assurance standards across institutions with different risk appetites and different compliance cultures is slow. Networks spanning jurisdictions face the additional complication of mapping regulatory requirements that do not align neatly across borders.

Decentralised wallet and W3C Verifiable Credentials

The decentralized model puts control of the credential with the user. After a compliant verification, the issuing organization creates a signed digital credential and delivers it to the user’s personal wallet. The credential is encoded in a machine-readable format, typically defined by the W3C Verifiable Credentials Data Model v2.0, which specifies how identity claims are structured, cryptographically signed, and presented to verifying parties.

When a relying party needs verification, the user presents the relevant credential from their wallet. The relying party checks the cryptographic signature, confirms the credential has not been revoked, and assesses whether the assurance level and recency satisfy its requirements. Only the attributes the user selects are disclosed. No central store is involved, and the raw identity data stays in the user’s wallet rather than being transmitted to the relying party in full.

The data minimisation alignment with GDPR is strong. The user controls which attributes travel to which relying parties. Breach risk is distributed rather than concentrated in a single store.

Adoption and trust present the main practical challenge. A relying party receiving a credential from an issuer they have never interacted with must trust that issuer’s verification methodology and governance. Without a recognised accreditation scheme, it is difficult to build trust at scale. This is precisely the problem that eIDAS 2.0 addresses at the EU level, by mandating a common wallet standard and an accreditation framework that creates enforceable trust in EUDI Wallet credentials across member states.

Is reusable KYC legally defensible?

This question determines whether reusable KYC is a viable compliance tool or a liability. Three factors shape the answer. The first is the assurance level of the original verification. The second is the relying party’s risk assessment of the new relationship. The third is the regulatory framework governing the jurisdiction.

FATF guidance and the tiered assurance model

FATF’s Guidance on Digital Identity (2020) maps digital identity verification onto assurance levels that run from low — covering basic data collection and cross-referencing — to high, covering biometric matching against a government-issued document combined with liveness detection. For AML compliance purposes, the guidance permits relying parties to rely on third-party identity verification when three conditions are satisfied. The original verification must have reached an assurance level appropriate to the risk profile of the new relationship. The relying party must be able to access the underlying evidence on regulatory request. The verifying party must itself be subject to AML/CFT obligations.

The tiered structure means reusable KYC does not constitute an automatic compliance pass. A credential issued for a standard-risk retail product may satisfy the due diligence requirements for another standard-risk relationship. That same credential does not automatically satisfy enhanced due diligence requirements without additional checks. The compliance officer’s central task is mapping each new use case to the credential’s assurance tier and confirming the match.

Each relying party’s risk assessment still operates independently. An institution cannot discharge its FATF obligations by accepting any credential from any source. The assurance level, the identity of the issuing entity, and the recency of the underlying verification are all inputs to a risk-based determination that the relying party must make for itself.

eIDAS 2.0 and the EU Digital Identity Wallet

Regulation (EU) 2024/1183, which updated the eIDAS framework, transforms portable digital identity from a technical option into a regulatory obligation across the EU. Every member state must provide citizens with an EU Digital Identity Wallet by the end of 2026, and regulated private sector entities, including banks, telecoms operators, and payment service providers, must accept those wallets by the end of 2027.

For compliance teams operating in Europe or serving European users, this regulation answers the legal validity question directly. EUDI Wallet credentials, issued under the national frameworks mandated by the regulation, are legally recognised identity instruments that satisfy the verification requirements in financial services and AML directives.

Two forward-looking implications follow. Any identity verification architecture built today for European markets should have a clear path to EUDI Wallet interoperability by 2027. And the trust infrastructure for those wallets, including the accreditation framework for issuers and the technical specification for credential exchange, is being defined now. Following that work actively keeps your implementation aligned with the standard rather than requiring a retrofit later.

GDPR and the consent lifecycle

The data protection dimension of reusable KYC is separate from the AML compliance question, and it receives less attention than it deserves in most implementation discussions.

GDPR (Regulation (EU) 2016/679) requires a lawful basis for sharing personal data, including verified identity claims, between data controllers. For reusable KYC in consumer contexts, the practical lawful basis is explicit, informed consent from the user. That consent must be specific to the purpose, freely given, and revocable at any time.

A user who enrolled their verified credential for one service cannot have that credential automatically shared with a second service without a new consent event. Each time a reusable credential is presented to a new relying party, the user must be shown a clear disclosure of which attributes will be read, which organisation will receive them, and for what purpose. That consent event must be logged with a timestamp, the relying party’s identity, and the specific attributes disclosed.

The consent lifecycle is what makes portable identity defensible under GDPR. Not a one-time enrolment consent, but an auditable chain of per-service authorisations. Any reusable identity architecture handling European users without this per-service consent layer is non-compliant, regardless of how rigorous the original verification was.

How to deploy reusable KYC in your platform

What a real deployment looks like

First-time users go through a full verification covering document capture, biometric matching or database cross-referencing, and any enhanced due diligence your risk policy requires for the product category. On successful completion, a verified credential is issued. Depending on your chosen architecture, it may be held in your central store, submitted to a federated network you participate in, or delivered to the user’s personal wallet.

For returning users, or users arriving from a partner service whose credential your platform trusts, the flow contracts. You request a presentation of the credential, check its validity, assurance level, and recency, and make a risk-based determination about whether it meets your requirements for this specific product. When it does, onboarding reduces to a consent grant and a risk-scoring step. The document-capture and liveness stages drop out entirely.

Jurisdictional requirements vary, and your compliance team needs to map them before deployment. KYC compliance regulations across major markets treat third-party reliance differently, and some regulators have not yet issued specific guidance on reusable credential acceptance. An assurance level that satisfies standard requirements in one market may not satisfy them in another.

A credential expiry policy is also necessary. Most regulated deployments treat credentials as valid for 12 months for standard-risk users and require reverification at shorter intervals for higher-risk categories. A credential that predates a material change in the user’s risk profile — such as moving to a higher transaction tier or triggering enhanced due diligence indicators — should prompt a fresh verification event regardless of its age.

Consent and audit trail requirements

On the consent side, implementation means building a per-service consent layer into every onboarding flow that accepts a reusable credential. When a user presents their credential, a clear disclosure should specify which attributes will be read, which entity will receive them, and for what purpose. That consent event must be recorded in a log queryable by your compliance team on demand.

The audit trail extends to the verification event itself. You need to demonstrate, for any given customer, what the original verification evidence was, who conducted it, when, and to what assurance level. If your architecture relies on a credential from a third-party issuer, you need a contractual arrangement giving you access to the underlying evidence on request. Without it, a regulator asking for verification records finds a gap you cannot fill from your own systems.

A verification workflow design that supports variable assurance-level requirements and integrates consent logging reduces the engineering effort required to build this infrastructure from scratch.

Where reusable KYC delivers the clearest return

Fintech and multi-product financial platforms

Neobanks and embedded finance platforms routinely offer multiple products to the same user base, from current accounts to lending to investment services. Each product carries its own KYC and AML obligation. Without a reusable model, a user opening a second product with the same provider may be asked to complete the full verification process again.

Under a centralised or federated reusable model, the initial verification for the first product satisfies the base-level requirements for the next, subject to a risk assessment of the incremental risk the new product introduces. The user grants per-service consent, the event is logged, and the product opens without the friction that drives a meaningful share of upgrade-funnel abandonment.

The electronic identity verification layer underpinning these flows is shifting in markets with mature national eID infrastructure. Database-driven verification replaces document-driven verification at the initial stage, making the first verification faster and the resulting credential more amenable to machine-to-machine sharing with subsequent relying parties.

Gaming, crypto, and other regulated platforms

Online gaming and gambling operators face a concentrated version of this problem. Players verified at registration for age and identity then interact with affiliate platforms, join third-party-hosted tournaments, or move between brands within the same group. Each context can trigger a fresh verification obligation under the relevant licensing authority.

A reusable credential recognised across affiliated brands or issued by an accredited third party can satisfy those obligations without requiring a player to submit documents repeatedly. The regulatory condition, consistent across jurisdictions, is that the credential must have been issued to an assurance level matching the highest-risk use case it will be applied to. A credential issued for age verification at standard risk does not automatically satisfy enhanced identity checks required for high-value transaction monitoring.

Crypto exchanges with EU users operating under MiCA face a parallel challenge in cross-platform trading. NIST IAL2 assurance standards and the emerging European digital asset identity frameworks sit at the high-assurance end of the reusable KYC spectrum, and platforms that build to those standards today position their credentials for broad acceptance as the regulatory landscape consolidates.

|

Manual, repeated onboarding is a direct conversion threat, with 70% of financial institutions losing clients to it last year and up to 60% of applicants abandoning the process before completion. Shufti’s Fast ID gives returning users a reusable, biometric-backed identity credential that works alongside document and face verification in a single unified flow, so your platform reduces friction at every onboarding touchpoint without sacrificing audit-trail integrity. To see how portable identity fits your compliance architecture, request a demo. |

Frequently Asked Questions

What is the difference between reusable KYC and traditional KYC?

Traditional KYC requires each regulated institution to independently verify a customer's identity, holding its own copy of documents and verification outcomes. Reusable KYC separates the verification event from the onboarding event, so a credential produced by one compliant verification can satisfy the identity requirements of subsequent services with explicit per-service consent. The relying party retains its own KYC obligation but discharges part of it by relying on a prior, trusted verification instead of repeating the full evidence-collection process.

Is reusable KYC legally compliant for AML?

It can be, under specific conditions. FATF's risk-based approach permits reliance on third-party identity verification when the original check reached an assurance level appropriate to the risk profile, the relying party can access the underlying evidence on regulatory request, and the original verifier was itself subject to AML/CFT obligations. Compliance is not automatic. The credential's assurance level must match the risk profile of the new relationship. Enhanced due diligence scenarios generally require supplementary verification steps regardless of what credentials the user already holds.

What regulations support reusable digital identity?

Several frameworks are now directly relevant. FATF's 2020 Guidance on Digital Identity provides the AML/CFT framing for third-party credential reliance. Regulation (EU) 2024/1183 (eIDAS 2.0) mandates EU Digital Identity Wallets across all 27 member states by the end of 2026, with private sector acceptance required by the end of 2027. The W3C Verifiable Credentials Data Model v2.0 provides the technical standard for cryptographically signed, machine-readable credentials. GDPR governs the consent and data-sharing requirements for credential use in European contexts. National frameworks, including the UK digital identity trust framework and sovereign eID schemes such as BankID, Singpass, and UAE Pass, add jurisdiction-specific requirements on top of the international layer.

How is user consent handled in reusable KYC?

GDPR and equivalent data protection frameworks require that sharing verified identity claims between services rests on explicit, per-service consent from the user. Each time a reusable credential is presented to a new relying party, the user must see a clear disclosure of which attributes will be shared, with which organisation, and for what purpose. That consent event must be logged with a timestamp, the relying party's identity, and the specific attributes disclosed. Consent is revocable. A user can withdraw it for any service at any time, and the relying party must stop processing the shared data from that point forward. An architecture that automates credential sharing without per-service consent creates a GDPR liability even when the underlying verification was fully compliant.