Face Verification

Face Verification

Address Verification

Address Verification

Document Verification

Document Verification

Age Verification

Age Verification

VideoIdent

VideoIdent

Fast ID

Fast ID

Docless Verification

Docless Verification

Consent Verification

Consent Verification

NFC Verification

NFC Verification

Business Verification

Business Verification

Due Diligence

Due Diligence

Investor Verification

Investor Verification

E-Signature

E-Signature

QES

QES

AML Screening

AML Screening

Transaction Monitoring

Transaction Monitoring

Adverse Media

Adverse Media

Business AML Screening

Business AML Screening

PEP & RCA

PEP & RCA

Sanctions

Sanctions

Watchlist

Watchlist

Behavioural Biometrics

Behavioural Biometrics

Device Fingerprinting

Device Fingerprinting

Biometric Face Authentication

Biometric Face Authentication

MFA

MFA

Fraud Hub

Fraud Hub

Onboarding

Onboarding

Ongoing Monitoring

Ongoing Monitoring

KYC

KYC

KYB

KYB

KYI

KYI

Age Assurance

Age Assurance

Identity Verification

Identity Verification

Workforce IAM

Workforce IAM

Candidate Verification

Candidate Verification

Compliance

Compliance

Fraud prevention

Fraud prevention

Trust & safety

Trust & safety

Global expansion

Global expansion

Product Managers

Product Managers

Compliance Officers

Compliance Officers

Fraud Analysts

Fraud Analysts

Developers

Developers

Deepfake Detection

Deepfake Detection

Bonus Abuse / Promotion Abuse

Bonus Abuse / Promotion Abuse

Account Takeover

Account Takeover

Synthetic Identity Fraud

Synthetic Identity Fraud

Document Fraud

Document Fraud

Impersonation Fraud

Impersonation Fraud

Multi-Accounting

Multi-Accounting

Fraud Networks

Fraud Networks

Chargeback Fraud

Chargeback Fraud

Money Mule Activity

Money Mule Activity

Party Fraud

Party Fraud

Regulatory & Compliance Risks

Regulatory & Compliance Risks

Fintech

Fintech

Crypto

Crypto

iGaming

iGaming

Forex

Forex

Social Network

Social Network

Marketplace

Marketplace

Banking

Banking

Gig Economy

Gig Economy

Payments

Payments

Ride Hailing

Ride Hailing

Adult Content

Adult Content

Blind Spot Audit

Blind Spot Audit

Deepfake Detector

Deepfake Detector

Liveness Spoofs

Liveness Spoofs

Document Originality

Document Originality

Document Deepfake

Document Deepfake

Global Trust Platform

Global Trust Platform

Journey Builder

Journey Builder

Case Management

Case Management

Shufti AI

Shufti AI

Fraud Analytics

Fraud Analytics

Vendor Comparison

Vendor Comparison

Brand Personalisation

Brand Personalisation

AI Compliance Co-Pilot

AI Compliance Co-Pilot

OCR

OCR

Secure Capture

Secure Capture

Deployment Options

Deployment Options

Identity Methods

Identity Methods

API Documentation

API Documentation

Mobile SDKs

Mobile SDKs

Service Status

Service Status

Help Center

Help Center

Contact Us

Contact Us

Technical Support

Technical Support

Supported Documents

Supported Documents

Supported Countries

Supported Countries

Content library

Content library

Blogs

Blogs

News

News

Reports

Reports

Insights

Insights

Knowledgebase

Knowledgebase

ROI calculator

ROI calculator

About

About

Career

Career

Press Release

Press Release

Certifications

Certifications

Partnership

Partnership

Awards

Awards

Events & Webinar

Events & Webinar

Interactive Demo

Interactive Demo

Podcast Studio

Podcast Studio

Spotlight Studio

Spotlight Studio

What is the difference between Face Verification vs Face Recognition – Guide

-

Add us as a Preferred Source

- 01 TL;DR

- 02 What Is Face Verification?

- 03 What Is Face Recognition?

- 04 Face Verification vs Face Recognition: Key Differences

- 05 How Do Security Levels Compare?

- 06 Accuracy and Error Rates: What's the Difference?

- 07 Privacy Considerations

- 08 Why Is Face Verification Preferred in Banking and KYC?

- 09 Which One Do You Need?

TL;DR

|

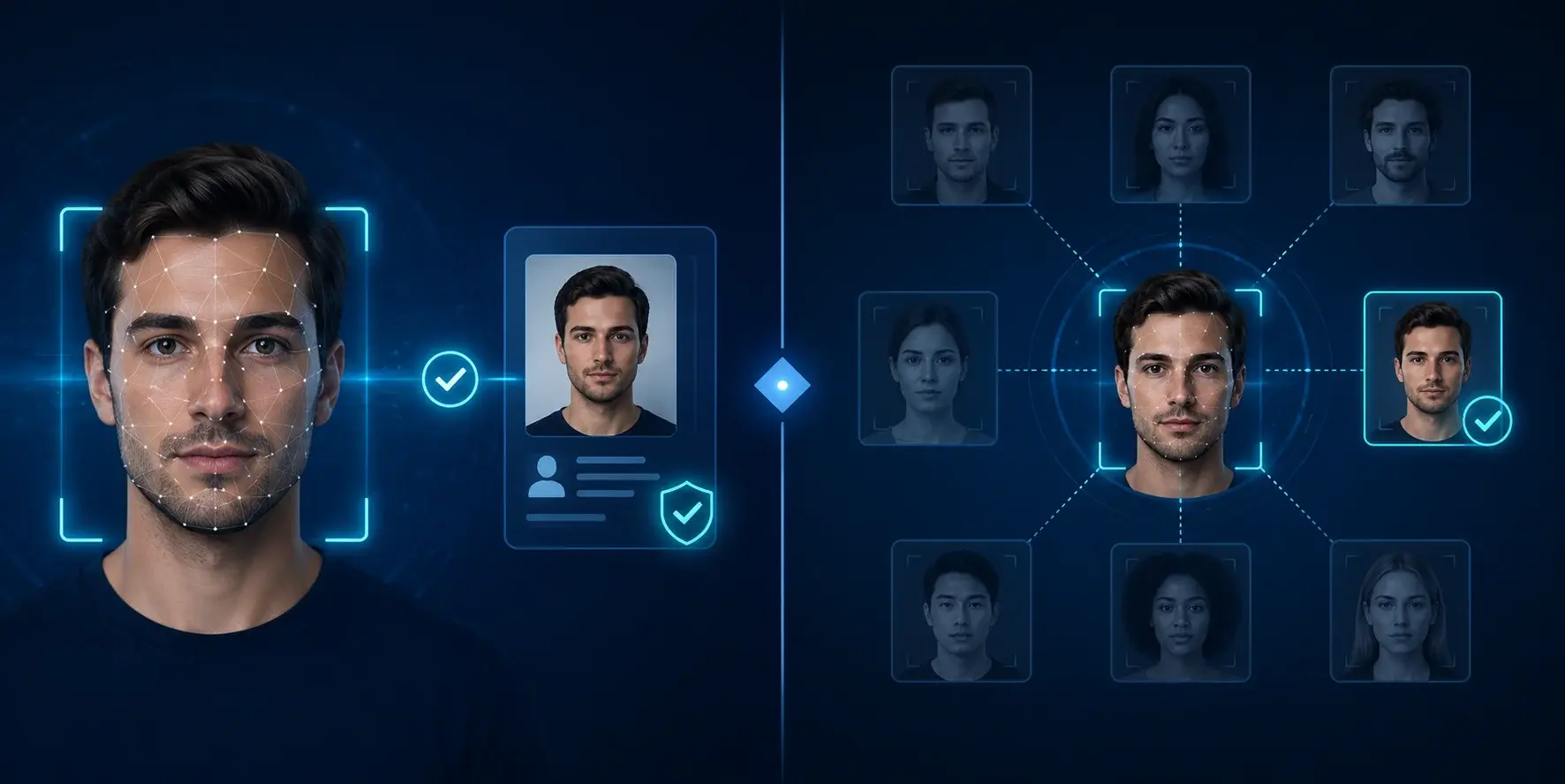

Ask ten people what face recognition means, and you will likely get ten different answers. Some pictures of unlocking a phone. Others think of police lineups or airport security gates. In reality, face recognition and face verification describe two distinct technologies, and this face verification vs recognition comparison starts with a single technical distinction: how many faces the system checks against.

Face verification checks one face against another face. Face recognition checks one face against many. That difference shapes where each technology fits, how private it is, and how accurate it can realistically be.

What Is Face Verification?

Face verification, sometimes called face matching, answers a narrow question: is this the same person? The system takes a live image, usually a selfie, and compares it against a single reference image, such as the photo on a passport or ID card already on file.

Because it only ever compares two images, face verification does not need to search a large database. This keeps the process fast and reduces the storage and privacy burden compared with recognition-based systems.

Common use cases for face verification:

- Confirming identity during account onboarding (KYC)

- Re-authenticating a user before a high-risk action, such as changing payment details

- Matching a traveller’s face to their passport photo at an automated border gate

What Is Face Recognition?

Face recognition, sometimes described as face search or face identification, works the opposite way. Instead of comparing two images, it takes one face and searches it against a database that may hold thousands or millions of stored faces to find a possible match.

This one-to-many search is what makes face recognition useful for spotting people rather than confirming a claim they have already made.

Common use cases for face recognition:

- Flagging known fraudsters or repeat offenders already in a database

- Detecting the same person attempting to open multiple accounts under different names

- Screening against watchlists at airports, casinos, or secure facilities

Face Verification vs Face Recognition: Key Differences

| Type | Face verification |

Face recognition |

|

Comparison type |

One-to-one (1:1) | One-to-many (1:N) |

| Question it answers | Is this the person they claim to be? |

Has this face appeared in our records before? |

|

Data required |

A single reference image | A database of enrolled faces |

| Typical setting | Onboarding, KYC, step-up authentication |

Fraud detection, watchlists, surveillance |

|

Consent model |

Usually permission-based |

Often runs without active user consent |

When comparing face recognition verification systems, this one distinction, one face versus many, is the deciding factor behind almost every other difference in this article.

How Do Security Levels Compare?

Security in face verification comes from narrowing the check to a single, known claim. There is no ambiguity about who the system is checking against, which lowers the chance of a false match slipping through unnoticed.

Face recognition carries a different risk profile. Searching across a large database increases the odds of a false match simply because there are more faces to compare against. Well-built systems offset this with larger, higher-quality training data and stricter matching thresholds, but the underlying risk is different from a straightforward 1:1 check.

Accuracy and Error Rates: What’s the Difference?

Both technologies are measured using two error types: false acceptance (matching two different people as the same person) and false rejection (failing to match the same person to themselves).

Face verification tends to report lower false acceptance rates because it only ever compares against one known image. Face recognition, working across larger galleries, becomes more exposed to false acceptance as the database grows, though tighter similarity thresholds help manage this. Both are affected by the same environmental factors: lighting, camera quality, ageing, and obstructions such as glasses or face coverings.

| NIST’s latest 1:N face recognition benchmark tested algorithms against a database of 12 million enrolled faces. The top-performing system still achieved a 0.07% identification error rate, showing that a larger database does not have to come at the cost of accuracy. |

Privacy Considerations

Face verification is generally the more privacy-friendly of the two. Most implementations compare, return a match decision, and do not need to retain a searchable gallery of faces long-term.

Face recognition depends on maintaining a database of enrolled faces to search against, which raises different regulatory and consent questions, particularly where the system runs without the individual actively opting in, such as in public surveillance. This is part of why face recognition faces tighter scrutiny under data protection rules in several jurisdictions.

Why Is Face Verification Preferred in Banking and KYC?

Financial institutions favour face verification for onboarding and authentication for a few practical reasons:

- It is permission-based. The customer knows a check is happening and takes an active step, usually a selfie, to complete it

- It does not require building or maintaining a facial database, which reduces compliance overhead

- It ties directly to a single claimed identity, which fits regulatory expectations for proving a customer is who they say they are

Face recognition can still play a supporting role in banking, for example, flagging repeat fraud attempts, but it is rarely the primary tool for onboarding a new customer.

Which One Do You Need?

If the goal is to confirm a claimed identity at a single point in time, such as opening an account or approving a transaction, face verification is the right fit. If the goal is to detect whether a face has appeared before, whether that means catching a repeat fraudster or matching someone against a watchlist, face recognition is the better tool.

Many identity programmes end up combining face recognition verification workflows: verification at the point of onboarding, and recognition running quietly in the background to catch duplicate or fraudulent accounts.

| See how Shufti’s face verification fits your KYC and onboarding flow. Request a demo to see it in action. |

: Meaning, Requirements, and When You Need One")

Fraud: What It Is, How It Works, and How to Stop It")