Face Verification

Face Verification

Address Verification

Address Verification

Document Verification

Document Verification

Age Verification

Age Verification

VideoIdent

VideoIdent

Fast ID

Fast ID

Docless Verification

Docless Verification

Consent Verification

Consent Verification

NFC Verification

NFC Verification

Business Verification

Business Verification

Due Diligence

Due Diligence

Investor Verification

Investor Verification

E-Signature

E-Signature

QES

QES

AML Screening

AML Screening

Transaction Monitoring

Transaction Monitoring

Adverse Media

Adverse Media

Business AML Screening

Business AML Screening

PEP & RCA

PEP & RCA

Sanctions

Sanctions

Watchlist

Watchlist

Behavioural Biometrics

Behavioural Biometrics

Device Fingerprinting

Device Fingerprinting

Biometric Face Authentication

Biometric Face Authentication

MFA

MFA

Fraud Hub

Fraud Hub

Onboarding

Onboarding

Ongoing Monitoring

Ongoing Monitoring

KYC

KYC

KYB

KYB

KYI

KYI

Age Assurance

Age Assurance

Identity Verification

Identity Verification

Workforce IAM

Workforce IAM

Candidate Verification

Candidate Verification

Compliance

Compliance

Fraud prevention

Fraud prevention

Trust & safety

Trust & safety

Global expansion

Global expansion

Product Managers

Product Managers

Compliance Officers

Compliance Officers

Fraud Analysts

Fraud Analysts

Developers

Developers

Deepfake Detection

Deepfake Detection

Bonus Abuse / Promotion Abuse

Bonus Abuse / Promotion Abuse

Account Takeover

Account Takeover

Synthetic Identity Fraud

Synthetic Identity Fraud

Document Fraud

Document Fraud

Impersonation Fraud

Impersonation Fraud

Multi-Accounting

Multi-Accounting

Fraud Networks

Fraud Networks

Chargeback Fraud

Chargeback Fraud

Money Mule Activity

Money Mule Activity

Party Fraud

Party Fraud

Regulatory & Compliance Risks

Regulatory & Compliance Risks

Fintech

Fintech

Crypto

Crypto

iGaming

iGaming

Forex

Forex

Social Network

Social Network

Marketplace

Marketplace

Banking

Banking

Gig Economy

Gig Economy

Payments

Payments

Ride Hailing

Ride Hailing

Adult Content

Adult Content

Blind Spot Audit

Blind Spot Audit

Deepfake Detector

Deepfake Detector

Liveness Spoofs

Liveness Spoofs

Document Originality

Document Originality

Document Deepfake

Document Deepfake

Global Trust Platform

Global Trust Platform

Journey Builder

Journey Builder

Case Management

Case Management

Shufti AI

Shufti AI

Fraud Analytics

Fraud Analytics

Vendor Comparison

Vendor Comparison

Brand Personalisation

Brand Personalisation

AI Compliance Co-Pilot

AI Compliance Co-Pilot

OCR

OCR

Secure Capture

Secure Capture

Deployment Options

Deployment Options

Identity Methods

Identity Methods

API Documentation

API Documentation

Mobile SDKs

Mobile SDKs

Service Status

Service Status

Help Center

Help Center

Contact Us

Contact Us

Technical Support

Technical Support

Supported Documents

Supported Documents

Supported Countries

Supported Countries

Content library

Content library

Blogs

Blogs

News

News

Reports

Reports

Insights

Insights

Knowledgebase

Knowledgebase

ROI calculator

ROI calculator

About

About

Career

Career

Press Release

Press Release

Certifications

Certifications

Partnership

Partnership

Awards

Awards

Events & Webinar

Events & Webinar

Interactive Demo

Interactive Demo

Podcast Studio

Podcast Studio

Spotlight Studio

Spotlight Studio

A Guide to Deepfake Detection in KYC

-

Add us as a Preferred Source

- 01 What is deepfake detection in KYC?

- 02 How are deepfakes exploiting identity verification systems?

- 03 Types of deepfake attacks that target KYC verification

- 04 How does KYC deepfake detection actually work?

- 05 Why is deepfake fraud a compliance risk, not just a security problem?

- 06 What should compliance teams look for in a deepfake-ready KYC solution?

- 07 Practical next steps for compliance teams

- 08 Shufti's approach to deepfake detection

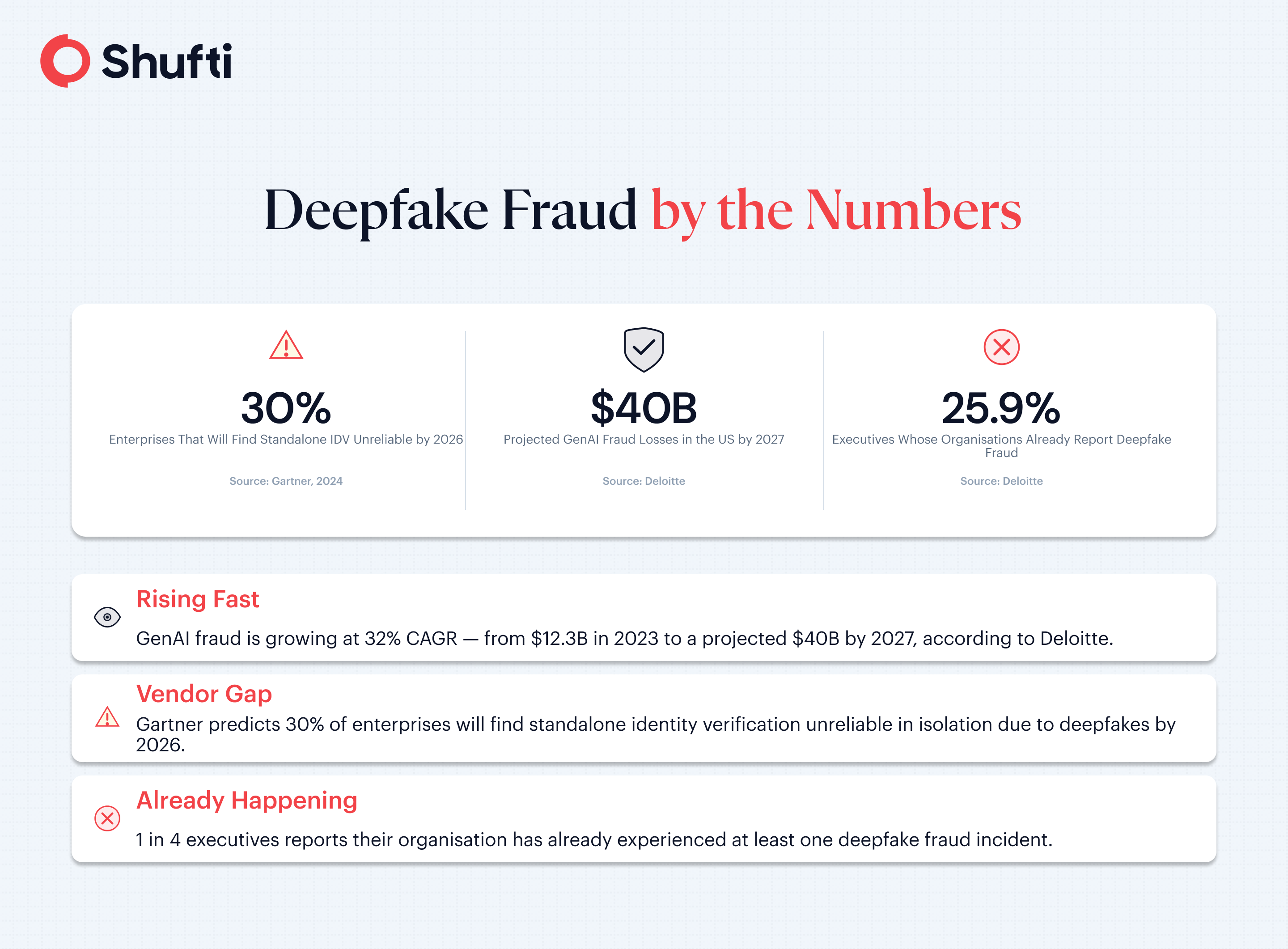

Deloitte’s Center for Financial Services projects that generative AI could push fraud losses in the US to $40 billion by 2027, up from $12.3 billion in 2023. A growing share of those losses trace back to AI-generated deepfakes bypassing Know Your Customer (KYC) verification at account opening. For compliance teams running digital onboarding, the threat is no longer theoretical.

The Financial Action Task Force (FATF) Horizon Scan on AI and Deepfakes, published in December 2025, identified deepfakes as a direct threat to anti-money laundering (AML) and customer due diligence (CDD) controls worldwide. This guide covers what deepfake detection in KYC actually involves, why compliance teams face growing regulatory exposure, and what to look for in a solution that holds up under scrutiny.

Deepfake detection in KYC refers to the methods and controls used to identify AI-synthesised or AI-manipulated facial images, video streams, and identity credentials within digital onboarding and re-verification processes. The goal is to confirm that the person presenting for verification is a live, real individual rather than a generated or manipulated representation.

|

Key Takeaways

|

What is deepfake detection in KYC?

KYC processes moved online gradually over the past decade and then almost entirely at once, which meant the industry replaced in-person face-to-face checks with remote verification. That substitution works when the verification systems are sound. The problem is that most systems in production were designed before generative AI reached its current capability, and the attack surface has shifted faster than deployed stacks have adapted. Deepfake detection sits at that gap: the point in the verification flow where a system must confirm the face it sees is real, not rendered.

A deepfake, in an identity verification context, is any AI-generated or AI-manipulated representation of a face, voice, or credential designed to pass as a real person during a verification event. Face swaps use one person’s facial geometry mapped onto a different person’s likeness. Generative AI models can produce entirely new facial identities that have never existed. Deepfake video streams replay pre-recorded or generated footage in place of a live camera feed.

Traditional KYC systems were designed to catch printed photos and static images. They were not designed for AI-generated media. A presentation attack detection (PAD) layer blocks physical attacks like masks and images held up to a camera. Passive liveness analysis confirms that the presented face shows genuine skin texture, depth, and micro-movement. Neither control, deployed alone, is sufficient against current-generation synthetic media.

A compliance team’s starting point is understanding how deepfakes are constructed and what detection methods exist before assessing whether their current vendor’s architecture is operating on pre-AI assumptions.

How are deepfakes exploiting identity verification systems?

Identity verification systems were designed before generative AI reached its current capability. The liveness checks, document scanners, and face-matching algorithms built between 2015 and 2022 were tested against printed photos, masks, and simple video replays. The attack surface has since shifted faster than most deployed stacks have adapted, and two specific categories now account for the majority of deepfake fraud attempts at KYC.

Gartner’s February 2024 research predicted that by 2026, 30% of enterprises would find standalone identity verification and authentication solutions unreliable in isolation due to AI-generated deepfakes. Deloitte’s research shows that 25.9% of executives already report deepfake-related fraud incidents at their organisation. The Gartner prediction was already materialising by the time the threshold year arrived.

Presentation attacks

Presentation attacks arrive through the camera layer of a verification system. A fraudster presents an AI-generated face on a screen, a high-resolution printed image, or a 3D mask to the device camera during liveness capture. PAD systems analyse texture, depth, and micro-movements to identify non-genuine media. These controls were the first line of defence against deepfakes and remain effective against basic attacks. Against current-generation generative AI, however, RGB-only pixel analysis can be defeated by synthetic faces that include convincing texture and depth cues.

Injection attacks

Injection attacks bypass the camera entirely. A synthetic video stream is fed directly into the verification API, between the device camera and the server. The camera layer never sees the fraud attempt. Injection attack detection (IAD) requires the system to analyse data integrity signals, device attestation metadata, and frame-level consistency patterns that a genuine camera feed would not produce. Most liveness systems built before 2022 do not include IAD by design, which creates a gap for compliance teams whose vendors have not updated their detection architecture.

Types of deepfake attacks that target KYC verification

Compliance teams typically encounter deepfake fraud through one of four attack types, and each exploits a different control gap in standard KYC workflows. The attack vectors your current verification stack is equipped to detect determine the questions you ask a vendor and the answers you should treat as credible.

Face swap attacks

A face swap takes an existing piece of video footage and replaces the original face with a different one using generative AI. The resulting video can pass basic RGB liveness checks, which examine colour patterns and pixel consistency. Face swaps are among the most common deepfake types used in KYC fraud attempts. The research on how fraudsters bypass face verification and liveness checks is well-documented and the methods have become accessible through commercially available tools.

Defence against face swaps requires frequency-domain analysis and 3D depth modelling, not surface-level pixel inspection. An RGB-only liveness system sees a realistic face. A frequency-domain analysis sees patterns of inconsistency in how pixels were generated that no physical face would produce.

Fully synthetic identity attacks

Generative AI models can now produce photorealistic facial images of individuals who have never existed. These synthetic identities are paired with AI-generated or manipulated documents to create what appears to be a complete customer profile. They are particularly dangerous in account-opening scenarios because there is no real person to trace the fraud back to, and a synthetic identity that passes onboarding leaves no physical trail.

Detection requires cross-validation between the document and the biometric. The face extracted from the document must match the live face presented, and both must pass independent authenticity checks. A system that verifies documents and faces as separate checks, without cross-validating the outputs, cannot catch this attack type reliably.

Video replay and deepfake injection attacks

Video replay attacks pre-record a real person and replay that footage during a liveness check. A more sophisticated version uses real-time deepfake synthesis, generating video on the fly and injecting it directly into the verification API without going through the device camera at all. Against a system that relies on camera-level liveness alone, neither replay nor live injection is detectable without additional signal layers at the server side.

How does KYC deepfake detection actually work?

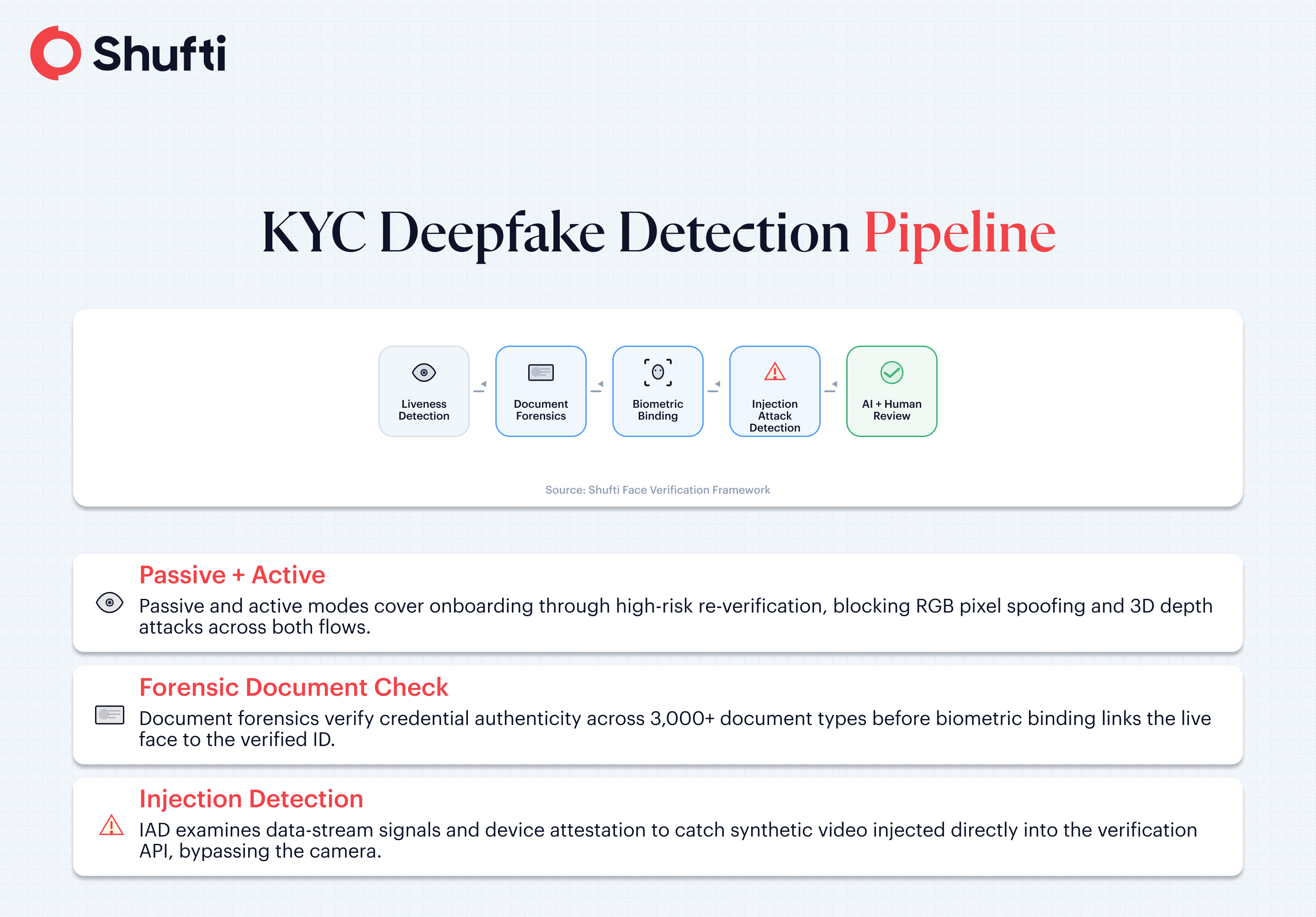

Deepfake detection in production KYC systems operates in layers, not as a single check. No individual signal is sufficient to confirm that a presented face is real. The pipeline works by combining multiple independent signals and requiring them to agree before a verification passes. A synthetic face that defeats one detection layer will typically fail at another, which is what makes layered detection architecturally more resilient than any single method deployed alone.

Passive liveness detection

Passive liveness detection runs in the background without requiring any action from the user. The verification system captures a face image or short video clip and analyses it for signs of genuine biological presence: natural micro-expressions, skin-texture variation, and 3D depth that flat images cannot replicate. Passive liveness can catch most printed-photo and basic screen-replay attacks without adding friction to the onboarding flow.

The limitation of passive liveness is that it operates primarily at the pixel level. AI-generated faces produced by current generative models can pass pixel-level analysis because they include synthesised texture, depth cues, and micro-movement patterns. Passive liveness is a necessary component of a detection pipeline but not a sufficient one when facing current attack methods.

Active liveness detection

Active liveness detection asks the user to perform a small, real-time action: a head turn, a blink, or a gaze movement in a specific direction. The system confirms that the movement corresponds to a live human being and that the face performing it is consistent across frames. Active liveness is more resistant than passive liveness to replay attacks because pre-recorded footage cannot respond to real-time prompts.

The trade-off is onboarding friction. On mobile devices with variable lighting and connection quality, active liveness creates measurable drop-off. Most modern KYC deployments use passive liveness as the baseline and escalate to active liveness for higher-risk verification events, account changes, or re-authentication triggers.

Injection attack detection

IAD examines the integrity of the data arriving at the verification server rather than the visual content of the face itself. When a synthetic video stream is injected directly into a verification API, it leaves forensic traces in the data signal, the device attestation metadata, and the frame-level consistency patterns that a genuine camera feed would not produce. The camera layer was never involved, so camera-level analysis alone cannot find the fraud.

IAD is the control that closes the gap left by camera-level liveness checks. Without it, an attacker who routes synthetic media around the camera will pass liveness undetected. For compliance teams reviewing current deepfake detection approaches, the presence or absence of IAD is a reliable indicator of whether a vendor has updated their detection architecture for post-2022 attack methods.

Biometric binding

Biometric binding links the verified live face to the identity document captured in the same session. The extracted face from the document is compared to the live biometric, and the data from both must be consistent for verification to pass. A deepfake that produces a plausible live face but cannot supply a matching document face fails at this step.

Biometric binding is not standard in all KYC verification flows. Platforms that verify documents and faces through separate API calls, without cross-validating the outputs, leave an exploitable gap between the two checks. For compliance teams evaluating how facial recognition integrates into KYC verification workflows, biometric binding is the control that separates a liveness check from a complete identity confirmation.

Why is deepfake fraud a compliance risk, not just a security problem?

Security teams and compliance teams often approach deepfake fraud from different starting points. Security teams focus on detection rates and attack vector coverage. Compliance teams need to know whether a failure to detect deepfake fraud constitutes a breach of AML or KYC obligations and whether it would survive a regulator examination. The answer to both questions, as of 2025 and 2026, is clearly yes.

As of December 2025, FATF’s December 2025 Horizon Scan explicitly identifies deepfakes as a tool capable of bypassing AML controls, CDD systems, and digital ID verification at onboarding. The report calls for a standardised, risk-based approach to AI and synthetic media risks and signals that supervisors will scrutinise deepfake controls as part of standard AML reviews.

The EU AI Act, which entered into force in August 2024, classifies remote biometric identification systems under Annex III as high-risk AI systems. That classification triggers documentation, safety testing, and human oversight obligations. KYC face verification systems in EU-regulated institutions fall within that designation, which means firms must demonstrate that their deepfake detection controls meet the Act’s requirements for high-risk AI.

Beyond the EU, the legal and regulatory landscape around deepfakes is still forming. The Financial Conduct Authority (FCA) has signalled through its Digital Sandbox programme and its 2024 AI and Digital Finance discussion paper that AI-generated fraud risks are within scope of existing AML obligations. The absence of deepfake-specific legislation in most jurisdictions does not create a compliance safe harbour. A deepfake that succeeds at account opening is a failure in the firm’s customer identification programme regardless of whether the regulator has written a rule specifically addressing it.

The compliance exposure is direct. A synthetic identity that passes KYC at onboarding can be used for money laundering, sanctions evasion, or fraud. The regulated firm that onboarded that identity bears the exposure. Deepfake detection is therefore a component of a firm’s legal obligation to conduct reliable customer identification, not an optional security enhancement.

What should compliance teams look for in a deepfake-ready KYC solution?

Vendor marketing in the identity verification market has adopted deepfake terminology broadly. Whether a vendor’s system detects the full range of current attack vectors requires asking questions that go beyond claims about AI-powered liveness. These criteria give compliance teams a way to evaluate vendors on substance rather than positioning.

Attack vector coverage

The baseline question is which specific attack types the system detects and how many distinct vectors are covered. A system that detects presentation attacks but not injection attacks is half-covered against current methods. A system with independent third-party testing across multiple attack vectors is more defensible under regulatory scrutiny than one with only internal benchmark data.

Ask for the false acceptance rate (FAR) and the true acceptance rate (TAR). Certification from iBeta under ISO 30107-3 for PAD provides independent confirmation of presentation attack coverage, though it does not cover injection attacks. For injection attack detection, ask specifically which data signals the system analyses and whether the vendor can demonstrate detection against known injection tools.

Deployment flexibility

Many regulated financial institutions operate under data residency and sovereignty requirements that dictate where biometric data can be processed. A vendor with cloud-only deployment may be architecturally disqualified for a bank under certain jurisdictional requirements before the capability conversation even begins. On-premises and hybrid deployments are a procurement requirement for many regulated institutions, not a premium feature.

Ask explicitly where biometric data is processed, how long it is retained, and whether a zero-trust on-premises deployment is available. The compliance implications of cloud, on-premises, and hybrid configurations for AI-driven KYC verification vary by jurisdiction and data classification regime, and the answer has direct bearing on whether a vendor can be deployed at all.

Human oversight and escalation pathways

The EU AI Act’s high-risk AI classification requires that systems include meaningful human oversight for consequential decisions. In KYC verification, this means a defined escalation pathway for cases where the automated decision is uncertain or contested, with documented audit trails. Vendors that offer hybrid AI and human review with structured escalation workflows are better positioned to demonstrate compliance with both the EU AI Act and standard AML supervisory expectations.

Independent certification and government validation

Vendor-reported benchmark data and internal testing are not the same as independent certification. Ask which third-party testing programmes the vendor’s technology has been assessed under, and which government evaluation programmes it has participated in. Government-body evaluations are independent and publicly documented, which makes them more credible under regulatory scrutiny than any figure the vendor has published about its own performance.

Practical next steps for compliance teams

Most compliance teams with a deepfake detection gap do not need to replace their entire KYC vendor. A structured assessment of what your current solution covers, where the gaps are, and which controls close them is usually the right starting point. These five steps give compliance teams a working framework.

- Map your current liveness detection type. Confirm whether your vendor uses active liveness, passive liveness, or both, and ask explicitly whether injection attack detection is included in your current integration. Most legacy systems do not include it, and many vendors do not surface this distinction unless asked directly.

- Check your certification evidence. Confirm whether your vendor’s deepfake detection has been independently certified, and to which standard. ISO 30107-3 covers presentation attacks. Injection attack testing is a separate question that requires a separate answer.

- Audit your biometric binding. Confirm whether document verification and face verification outputs are cross-validated in the same session. If they run as separate API calls without linking the outputs, the gap between the two checks is exploitable.

- Review your human oversight workflow. Confirm that your system includes a defined escalation pathway for high-risk verification decisions with documented audit trails. This is a specific requirement under the EU AI Act for high-risk AI systems, and it needs to be documented before a regulator asks for it.

- Document your deepfake controls for regulatory review. As of December 2025, the FATF Horizon Scan signals that supervisors will expect firms to demonstrate documented AI-specific AML controls. That documentation starts by mapping your deepfake detection controls to your customer identification programme, and your approach to remote identity verification compliance is the framework that ties them together.

Shufti’s approach to deepfake detection

Verification failures at the liveness layer carry direct regulatory exposure, not just financial loss. The architecture of a deepfake detection system determines whether it holds up against current attack vectors or only against the attack vectors that were common when the system was first designed. These are not the same set.

Shufti’s deepfake detection covers 56+ anti-spoofing attack vectors, including AI-generated faces, face swaps, video replay attacks, 3D masks, and injection attacks. The system operates across multiple analysis layers. Passive liveness, active liveness, frequency-domain analysis, 3D depth modelling, and IAD run in parallel rather than as sequential checks. When one layer is deceived, the others provide redundant coverage rather than a pass-through.

Detection performance is validated externally, not self-reported. Shufti holds the US Department of Homeland Security (DHS) RIVR 2025 top performer designation, meeting 100% of the DHS verification goals across diverse demographics. The FAR is below 0.001%, meaning fewer than one in 100,000 verification attempts results in an incorrect pass. For compliance teams, government-body validation carries more weight than vendor-published benchmarks precisely because the testing conditions are independent and publicly documented.

Shufti’s architecture also addresses the compliance team’s practical requirement for deployment flexibility. The same system deploys across cloud, on-premises, and hybrid configurations, which addresses the data residency and sovereignty requirements that disqualify cloud-only platforms in certain regulated environments. Hybrid AI and human review is available for high-risk or contested cases, providing the human oversight pathway required under the EU AI Act’s high-risk AI classification.

For compliance teams responding to FATF Horizon Scan requirements for deepfake controls in AML frameworks, Shufti’s detection pipeline produces an audit trail mapped to each layer of the verification process, which is the structure a regulatory review of AI-specific AML controls will expect to see.

|

Deepfake fraud is reaching KYC systems through channels that standard liveness checks were not designed to handle, and the regulatory pressure to demonstrate adequate controls is coming from both FATF and the EU AI Act. Shufti’s deepfake detection covers 56+ anti-spoofing attack vectors across passive and active liveness, injection attack detection, and biometric binding, with government-validated performance and deployment options across cloud, on-premises, and hybrid environments. Request a demo to see the detection pipeline run against current deepfake attack types on your own onboarding flow. |

Frequently Asked Questions

What is deepfake detection in KYC?

Deepfake detection in KYC refers to the technical controls used to identify AI-synthesised or AI-manipulated faces, video, and identity credentials during digital onboarding and re-verification. The goal is to confirm the person presenting is real and live, not a generated or manipulated representation designed to pass an automated check.

How do deepfakes affect identity verification?

Deepfakes can defeat liveness checks that rely on pixel-level analysis alone. Face swaps produce realistic textures that pass basic RGB inspection. Injection attacks bypass the camera layer entirely by feeding synthetic video directly into a verification API. Both methods allow fraudulent accounts to be opened under false identities that pass automated KYC checks without triggering alerts.

Why is deepfake fraud a risk for compliance teams?

A deepfake that passes KYC onboarding creates a synthetic identity that can be used for money laundering, sanctions evasion, or fraud. The regulated firm that accepted the synthetic identity bears the regulatory exposure. FATF's December 2025 Horizon Scan identifies this as a direct failure of CDD obligations, not merely a technical security lapse.

Can KYC systems detect deepfake videos?

Yes, but only if the system includes the right detection layers. Passive and active liveness detection alone is insufficient against injection attacks, where synthetic video bypasses the camera layer entirely. Effective deepfake video detection requires IAD in addition to PAD, plus biometric binding to cross-validate the live face against the identity document.

Do KYC providers offer built-in deepfake detection?

Some do, but coverage depth varies across the market. Ask vendors to specify which attack vectors they cover and provide third-party certification data. Distinguish between PAD and IAD. A vendor that describes its liveness check as its deepfake detection layer is conflating two distinct controls, and that conflation is worth examining before a procurement decision.

: Meaning, Requirements, and When You Need One")