Face Verification

Face Verification

Address Verification

Address Verification

Document Verification

Document Verification

Age Verification

Age Verification

VideoIdent

VideoIdent

Fast ID

Fast ID

Docless Verification

Docless Verification

Consent Verification

Consent Verification

NFC Verification

NFC Verification

Business Verification

Business Verification

Due Diligence

Due Diligence

Investor Verification

Investor Verification

E-Signature

E-Signature

QES

QES

AML Screening

AML Screening

Transaction Monitoring

Transaction Monitoring

Adverse Media

Adverse Media

Business AML Screening

Business AML Screening

PEP & RCA

PEP & RCA

Sanctions

Sanctions

Watchlist

Watchlist

Behavioural Biometrics

Behavioural Biometrics

Device Fingerprinting

Device Fingerprinting

Biometric Face Authentication

Biometric Face Authentication

MFA

MFA

Fraud Hub

Fraud Hub

Onboarding

Onboarding

Ongoing Monitoring

Ongoing Monitoring

KYC

KYC

KYB

KYB

KYI

KYI

Age Assurance

Age Assurance

Identity Verification

Identity Verification

Workforce IAM

Workforce IAM

Candidate Verification

Candidate Verification

Compliance

Compliance

Fraud prevention

Fraud prevention

Trust & safety

Trust & safety

Global expansion

Global expansion

Product Managers

Product Managers

Compliance Officers

Compliance Officers

Fraud Analysts

Fraud Analysts

Developers

Developers

Deepfake Detection

Deepfake Detection

Bonus Abuse / Promotion Abuse

Bonus Abuse / Promotion Abuse

Account Takeover

Account Takeover

Synthetic Identity Fraud

Synthetic Identity Fraud

Document Fraud

Document Fraud

Impersonation Fraud

Impersonation Fraud

Multi-Accounting

Multi-Accounting

Fraud Networks

Fraud Networks

Chargeback Fraud

Chargeback Fraud

Money Mule Activity

Money Mule Activity

Party Fraud

Party Fraud

Regulatory & Compliance Risks

Regulatory & Compliance Risks

Fintech

Fintech

Crypto

Crypto

iGaming

iGaming

Forex

Forex

Social Network

Social Network

Marketplace

Marketplace

Banking

Banking

Gig Economy

Gig Economy

Payments

Payments

Ride Hailing

Ride Hailing

Adult Content

Adult Content

Blind Spot Audit

Blind Spot Audit

Deepfake Detector

Deepfake Detector

Liveness Spoofs

Liveness Spoofs

Document Originality

Document Originality

Document Deepfake

Document Deepfake

Global Trust Platform

Global Trust Platform

Journey Builder

Journey Builder

Case Management

Case Management

Shufti AI

Shufti AI

Fraud Analytics

Fraud Analytics

Vendor Comparison

Vendor Comparison

Brand Personalisation

Brand Personalisation

AI Compliance Co-Pilot

AI Compliance Co-Pilot

OCR

OCR

Secure Capture

Secure Capture

Deployment Options

Deployment Options

Identity Methods

Identity Methods

API Documentation

API Documentation

Mobile SDKs

Mobile SDKs

Service Status

Service Status

Help Center

Help Center

Contact Us

Contact Us

Technical Support

Technical Support

Supported Documents

Supported Documents

Supported Countries

Supported Countries

Content library

Content library

Blogs

Blogs

News

News

Reports

Reports

Insights

Insights

Knowledgebase

Knowledgebase

ROI calculator

ROI calculator

About

About

Career

Career

Press Release

Press Release

Certifications

Certifications

Partnership

Partnership

Awards

Awards

Events & Webinar

Events & Webinar

Interactive Demo

Interactive Demo

Podcast Studio

Podcast Studio

Spotlight Studio

Spotlight Studio

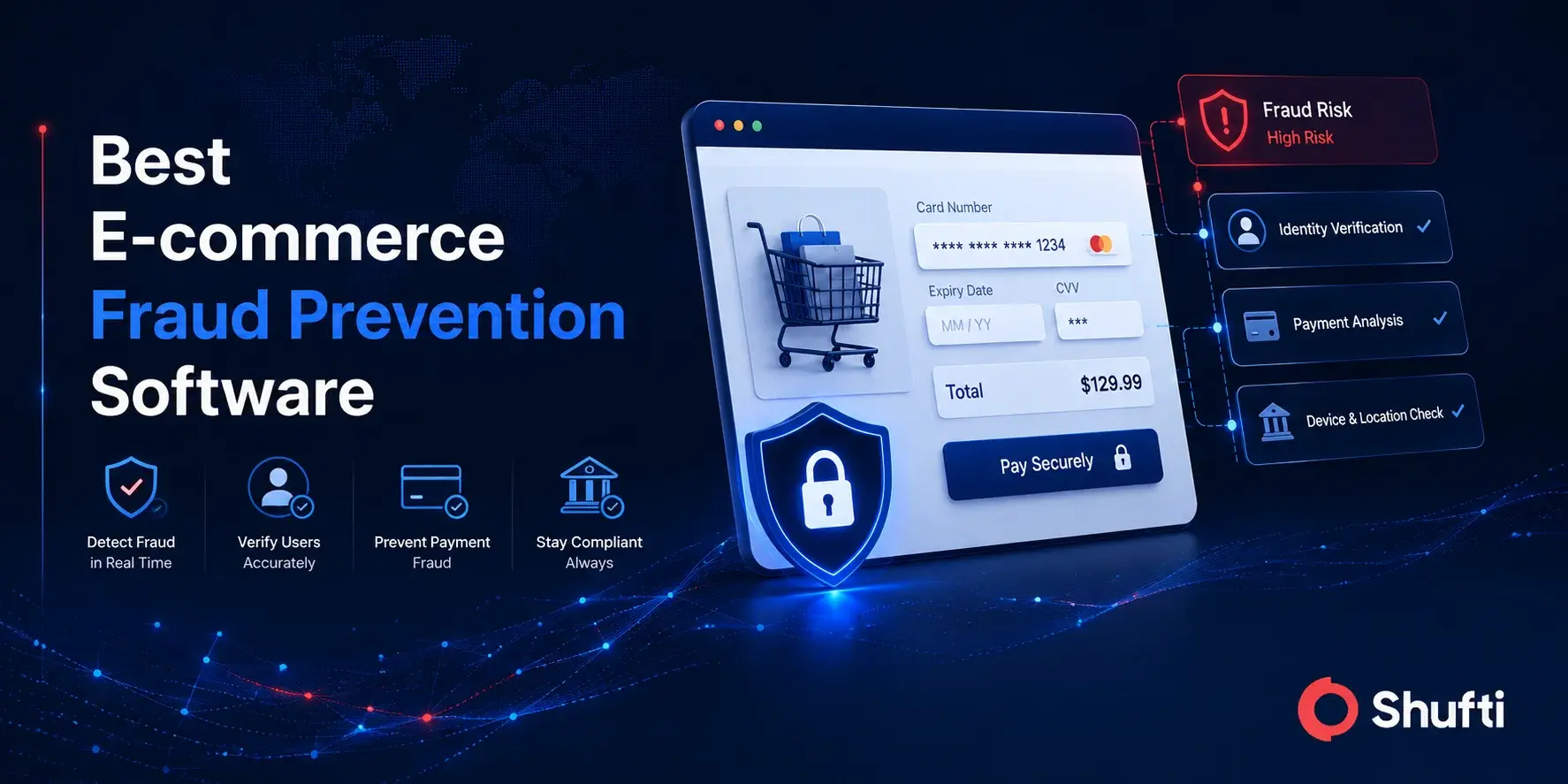

Best E-commerce Fraud Prevention Software in 2026

-

Add us as a Preferred Source

- 01 What to Look for in Ecommerce Fraud Prevention Software in 2026?

- 02 The 10 Best Ecommerce Fraud Prevention Tools in 2026

- 03 Ecommerce Fraud Prevention Software Comparison at a Glance

- 04 1. Shufti

- 05 2. ClearSale

- 06 3. Forter

- 07 4. Kount (an Equifax company)

- 08 5. NoFraud (now Wyllo)

- 09 6. Riskified

- 10 7. SEON

- 11 8. Sift

- 12 9. Signifyd

- 13 10. Stripe Radar

- 14 How to Choose the Right Ecommerce Fraud Prevention Software?

TL;DR

- The 10 best ecommerce fraud prevention software tools compared in this guide: Shufti, ClearSale, Forter, Kount (Equifax), NoFraud, Riskified, SEON, Sift, Signifyd, and Stripe Radar.

- Ecommerce fraud prevention software now spans two distinct jobs: stopping payment fraud and stopping identity fraud.

- Chargeback guarantee vendors absorb transaction liability; identity-led vendors stop account and onboarding fraud upstream.

- Most merchants need both layers, not one scoring engine doing everything.

- The right tool depends on your traffic, your markets, and your platform, not a leaderboard.

Most merchants do not lose sleep over the obvious stolen-card order. They lose sleep over the two failure modes in which scoring engines get wrong in opposite directions: the good customer who gets declined at checkout, and the fraudster who passes because the signal looks clean.

If you tighten the rules then conversion drops,if you loosen them then chargebacks climb up. Friendly fraud has made this worse, with card networks formalising how disputes get challenged.

Juniper Research, in a 2023 forecast, projected cumulative merchant losses from online payment fraud to exceed 362 billion dollars globally between 2023 and 2028. This guide breaks down what to evaluate, then compares the ten ecommerce fraud prevention software platforms worth a shortlist in 2026, with sourced ratings and an honest view of where each one actually fits.

What to Look for in Ecommerce Fraud Prevention Software in 2026?

The procurement question is not “which tool has the best AI”. It is which tool covers your specific fraud surface, with a liability model your finance team accepts, on the platform you already run. Six criteria separate the real contenders.

Owned technology versus orchestrated scoring stacks

The first question is whether the vendor builds its own detection technology or orchestrates third-party signals behind a risk score. Owned technology means one chain of custody for your data, one team accountable when a model misfires, and retraining on your own release timeline rather than a partner’s. Orchestrated stacks integrate faster and tap broad signal networks, but accountability fragments when a false decline traces back to a component the vendor licenses rather than controls. For high-volume merchants, that difference shows up in how quickly a vendor can adapt to a new attack pattern hitting your store specifically.

Identity fraud versus transaction fraud coverage

Ecommerce fraud detection covers two surfaces that many buyers conflate. Transaction fraud is the checkout decision: is this payment legitimate. Identity fraud is upstream: is this account real, or is it a synthetic identity, a stolen login in an account-takeover attempt, or a deepfake passing a verification step. Pure payment-scoring tools are strong on the former and thin on the latter. As account-takeover and synthetic identity attacks move earlier in the funnel, the account-opening and login stages need identity verification, not just a transaction score. The strongest programs cover both, either in one platform or by pairing an identity layer with a transaction layer.

Chargeback liability model

Chargeback prevention software splits into two commercial models, and the difference is financial, not technical. Guarantee vendors (Signifyd, Riskified, NoFraud, ClearSale) approve or decline orders and reimburse you for fraud chargebacks on orders they approved, transferring liability off your balance sheet. Score-only vendors (Sift, Kount, SEON, Stripe Radar) return a risk score or decision and leave the chargeback liability with you. Guarantees cost more and suit merchants who want predictable fraud expense; score-only models cost less and suit teams with the analyst capacity to act on signals themselves.

Cross-border and hard-market accuracy

A model trained mostly on US and Western European traffic degrades on documents, names, and behavioural patterns from emerging markets. If you sell into Latin America, the Gulf, Southeast Asia, or South Asia, ask how the vendor handles local payment methods, non-Latin scripts, and regional identity documents. This is where identity-led vendors with owned, regionally trained models pull ahead of payment-scoring engines tuned for North American card data.

Platform and Shopify integration depth

The best detection logic is worthless if it does not fit your stack. For Shopify fraud protection specifically, look for native apps that read order, customer, and fulfillment data without custom engineering, plus support for Shopify Plus checkout extensibility. Beyond Shopify, check for prebuilt connectors to your payment processor, your order management system, and major platforms like Magento, WooCommerce, and BigCommerce. Integration depth determines time-to-value more than any single accuracy metric.

Independent anti-spoofing conformance

As deepfakes and presentation attacks target identity steps, independent liveness testing separates marketing claims from verified capability. iBeta conformance under ISO/IEC 30107-3 is the recognised independent benchmark for presentation-attack detection. Level 3 is the highest published tier and, as of mid-2026, is held by only a small number of vendors globally. If your fraud surface includes selfie-based verification, account recovery, or high-value identity proofing, independent liveness conformance is a procurement requirement, not a nice-to-have.

The 10 Best Ecommerce Fraud Prevention Tools in 2026

As the publisher of this guide, we list Shufti first for transparency. The remaining nine vendors are listed alphabetically and described on the same factual basis. Each entry includes an overview, key strengths, considerations, certifications, current public ratings, and the use case the vendor is best suited to. Product details are sourced from each vendor’s public website, public certification listings, and verified review platforms.

- Shufti

- ClearSale

- Forter

- Kount (an Equifax company)

- NoFraud

- Riskified

- SEON

- Sift

- Signifyd

- Stripe Radar

Ecommerce Fraud Prevention Software Comparison at a Glance

| Vendor | Primary approach | Chargeback guarantee | Identity / IDV depth | G2 rating | Best fit |

| Shufti | Owned full-stack identity and fraud | No (identity layer) | Deep (iBeta L3, 240+ countries) | 4.5/5 (64 reviews) | Global identity and onboarding fraud |

| ClearSale | ML plus human review | Yes | Moderate | 4.7/5 (206 reviews) | LatAm and low false-positive needs |

| Forter | Automated network decisions | No | Behavioural | 4.5/5 (29 reviews) | Enterprise real-time decisions |

| Kount (Equifax) | Identity-trust scoring | No | US identity data | 4.8/5 (116 reviews) | US policy-driven decisioning |

| NoFraud | Guaranteed decisions | Yes | Low | 4.7/5 (250 reviews) | SMB plug-and-play guarantee |

| Riskified | Approval-rate optimisation | Yes | Behavioural | 4.4/5 (200+ reviews) | Enterprise conversion plus guarantee |

| SEON | Digital footprint enrichment | No | Signal-based | 4.6/5 (381 reviews) | Self-serve, in-house fraud teams |

| Sift | Real-time event scoring | No | Behavioural | 4.6/5(610 reviews) | Multi-surface platforms |

| Signifyd | Network-backed guarantee | Yes | Low | 4.6/5 (352 reviews) | Mid-market and enterprise retail |

| Stripe Radar | Built-in payment scoring | No | Low | 4.4/5 (19 reviews) | Stripe-native businesses |

Sources: vendor public sites, Gartner Peer Insights, G2.com vendor profiles, Capterra, and Trustpilot. All data accurate as of June 2026; verify directly with each vendor before procurement.

1. Shufti

Shufti is a UK-headquartered identity verification and fraud prevention vendor built entirely on owned intellectual property: OCR, liveness detection, document intelligence, KYC, KYB, and proprietary AML, all developed and maintained in-house rather than licensed from partners. In the ecommerce context, Shufti sits at the identity-fraud layer, stopping synthetic identities, account-takeover attempts, and document and deepfake fraud at account opening and high-value verification steps, before a fraudulent order is ever placed. That ownership is what made Shufti a genuinely ‘Glocal’ vendor: the same architecture verifies a US driver’s licence with the same engineering control as a Vietnamese national ID, an Indonesian KTP, or a Saudi national ID, which is the architecture mainstream players turned to when their stacks struggled with non-Latin scripts.

Key strengths:

Shufti is trained on and actively verifying 10,000+ document types across 240+ countries and jurisdictions every month, not just listed in a lifetime catalogue. Its in-house OCR reaches 99.7% accuracy across 150+ languages and scripts and outperforms Google Vision on various non-latin scripts, which matters directly for cross-border ecommerce in emerging markets. It holds iBeta Level 3 conformance, the highest published independent presentation-attack detection standard, held by only three vendors globally, giving merchants a defensible posture against deepfake and spoofing attacks on identity steps. Its doc-less identity hub draws on 270+ authoritative data sources for passive checks across 95+ countries, plus 40+ active eID integrations including BankID, Singpass, MitID, and OneID, with three eIDV modes (Passive, Active, Biometrically Enriched) through a single API.

Considerations:

Shufti is an identity-fraud and onboarding-fraud platform, not a chargeback guarantee provider. Merchants who want fraud chargeback liability transferred off their balance sheet pair Shufti’s identity layer with a guarantee model, or select a guarantee vendor for that specific function. Commercial presence in North America is smaller than US-headquartered payment-fraud peers, a brand-awareness and contracting consideration, not a capability one. Pricing varies by deployment model and is not published per-transaction; enterprise and on-premises contracts are quoted directly.

Deployment Options:

- SaaS

- Cloud

- Local Cloud

- On-premise for data-residency compliance

Certifications and recognitions:

- iBeta Level 3 conformance under ISO/IEC 30107-3

- DHS RIVR 2025 Top Performer: 98.49% True Accept Rate, zero False Template Creation events in the U.S. Department of Homeland Security Remote Identity Validation Rally 2025

- SOC 2 Type II

- PCI DSS

- GDPR compliance, Cyber Essentials, Cyber Essentials Plus

Ratings (as of June 2026):

- Shufti Trustpilot Reviews: 4.8 / 5 (3,800+ reviews), the highest Trustpilot rating-and-volume combination among the vendors compared

- Shufti G2 Reviews: 4.5 / 5 (64 reviews)

Best for:

Online stores and marketplaces facing identity fraud, account-takeover, synthetic identity, and deepfake attacks, particularly those selling cross-border into emerging markets where document and behavioural accuracy degrade for models trained on Western data. Shufti is the identity-fraud layer that pairs with, or upgrades, a transaction-scoring tool. One platform. Fully owned technology. Global coverage with real local depth.

2. ClearSale

ClearSale is a Brazil-headquartered fraud prevention provider known for combining machine-learning risk scoring with a large human review operation, an approach suited to markets where manual analyst judgement on borderline orders reduces false declines. It operates a chargeback guarantee model for approved orders.

Key strengths:

ClearSale’s combination of automated scoring and human review targets one of ecommerce’s most expensive errors: rejecting legitimate customers. Reviewers on G2 frequently cite its ability to minimise false positives while approving genuine orders. Its Latin American roots give it strong regional fraud intelligence for merchants selling into Brazil and the wider region, and it offers a chargeback guarantee on approved transactions.

Considerations:

The human-review layer that improves accuracy on borderline orders can add latency compared with fully automated decisions, a trade-off for merchants needing instant approval at scale. Coverage and intelligence depth are strongest in the Americas; evaluate regional fit if your volume is concentrated elsewhere.

Certifications and recognitions:

- PCI DSS compliance

- SOC 2 (refer to clear.sale for current trust documentation)

Ratings (as of June 2026):

- Trustpilot: 3.8/5 (180 reviews)

- G2: rated across 226 reviews, reviewers report ease of setup and low false positives

Best for:

Mid-market and enterprise retailers selling into Latin America, or any merchant that values human-review accuracy on borderline orders and wants a chargeback guarantee rather than a score alone.

3. Forter

Forter is a US-headquartered enterprise fraud prevention platform that makes instant automated decisions on transactions using a large identity-and-behaviour network built across its merchant base. It positions around real-time, fully automated approve-or-decline responses at enterprise scale.

Key strengths:

Forter’s network effect, drawn from transactions across its merchant base, supports fast, fully automated decisions without manual review queues. It spans payment fraud, account takeover, and policy abuse, making it a fit for large merchants consolidating multiple fraud surfaces onto one platform.

Considerations:

Forter targets enterprise volumes and typically requires custom pricing and a sales-led onboarding process, which can be heavier than plug-and-play tools for smaller stores. Its strengths concentrate on transaction and behavioural fraud rather than document-based identity proofing.

Certifications and recognitions:

- PCI DSS compliance

- SOC 2 Type II

Ratings (as of June 2026):

- Trustpilot ( limited presence)

- G2 4.5/5 (26), reviewers cite reduced manual review workload and real-time approvals

Best for:

Large enterprise merchants and marketplaces want fully automated, real-time transaction decisions across multiple fraud surfaces, with the budget and volume to justify an enterprise contract.

4. Kount (an Equifax company)

Kount, an Equifax company, is a US-headquartered identity-trust and fraud prevention platform that scores transactions and interactions using AI plus Equifax identity data. It serves ecommerce, payments, and digital businesses with configurable risk policies.

Key strengths:

Kount’s link to Equifax identity data strengthens its US identity-trust signals, and its policy engine lets fraud teams tune decisions to their own risk appetite. It covers payment fraud, account takeover, and chargeback management, and reviewers on G2 praise its detection accuracy and review workflow.

Considerations:

Reviewers note the configuration and tuning process can be complex and time-consuming to get right. Identity-data strengths are weighted toward the US market; evaluate coverage for non-US traffic.

Certifications and recognitions:

- PCI DSS Level 1

- SOC 2

Ratings (as of June 2026):

- Limited consumer Trustpilot presence (B2B platform)

- G2: 4.8 / 5 (120 reviews)

Best for:

US-focused ecommerce and payments businesses that want configurable, policy-driven risk decisioning backed by Equifax identity data, and have the team to tune it.

5. NoFraud (now Wyllo)

NoFraud is a US-headquartered fraud prevention provider focused on ecommerce, offering a chargeback guarantee with fast, mostly automated decisions and strong out-of-the-box integrations for small and mid-market stores.

On 19 March 2026 it rebranded as Wyllo, following its acquisition of post-purchase risk platform Yofi, repositioning from checkout fraud prevention toward a broader, customer-experience-first risk intelligence platform spanning the full commerce lifecycle.

Key strengths:

NoFraud ( Wyllo), is built for merchants who want a guarantee without an enterprise procurement cycle. It integrates natively with major ecommerce and payment platforms, and reviewers highlight accurate decisions, minimal chargebacks, and a clean analytics dashboard, with a guarantee model that transfers fraud chargeback liability on approved orders. The Yofi acquisition extends its signals beyond checkout into post-purchase risk, covering returns, refunds, and policy abuse across the customer journey.

Considerations:

NoFraud (Wyllo), concentrates on payment, chargeback, and post-purchase abuse for ecommerce; it is not a broad identity-proofing or KYC platform. Its sweet spot is small to mid-market merchants rather than the largest enterprise marketplaces. As a recently rebranded and recently merged platform, buyers should confirm current product packaging and integration scope directly during evaluation.

Certifications and Recognitions:

- PCI DSS compliance

- SOC 2

Ratings (as of June 2026):

- G2: 4.7/5 ( 259 reviews)

- Trustpilot: Limited Presence

Best for:

Small and mid-market online stores wanting a chargeback guarantee with fast setup, native ecommerce integrations, and minimal manual review overhead, now with added post-purchase abuse coverage under the Wyllo brand.

6. Riskified

Riskified is a US-and-Israel-based enterprise fraud prevention platform offering chargeback-guaranteed approve-or-decline decisions, with additional products for account protection, dynamic checkout, and payment authorisation optimisation aimed at lifting approval rates.

Key strengths:

Riskified frames fraud prevention as a revenue lever, optimising approval rates while guaranteeing approved orders against fraud chargebacks. Its conversion-focused product suite suits large merchants where a few points of approval rate move material revenue.

Considerations:

Riskified is enterprise-oriented with sales-led pricing, a heavier commitment than self-serve tools. As a transaction-decision platform, it focuses on payment and policy abuse rather than upstream document-based identity verification.

Certifications and recognitions:

- PCI DSS compliance

- SOC 2 Type II

Ratings (as of June 2026):

- Limited consumer Trustpilot presence (B2B platform)

- G2: 4.4 / 5 (200+ reviews)

Best for:

Large enterprise merchants prioritising approval-rate optimisation alongside a chargeback guarantee, where incremental conversion gains justify an enterprise contract.

7. SEON

SEON is a UK-headquartered fraud prevention platform known for real-time digital footprint analysis and data enrichment from email, phone, IP, and device signals, with transparent pricing and a self-serve onboarding path that appeals to fast-growing digital businesses.

Key strengths:

SEON’s enrichment approach builds a risk picture from open and digital-footprint signals without requiring heavy historical data, which suits newer merchants and high-velocity verticals. It is a recognised G2 Leader, and reviewers consistently praise its data enrichment, ease of use, and responsive support. Its API-first, configurable rules engine gives fraud teams direct control.

Considerations:

SEON is a score-and-signal platform, not a chargeback guarantee provider, so fraud liability remains with the merchant. Getting the most from its rules engine rewards teams with in-house fraud expertise to tune it.

Certifications and recognitions:

- ISO/IEC 27001

- SOC 2 Type II

- PSD2 SCA support

Ratings (as of June 2026):

- Trustpilot: 3.8/5 (38 Reviews)

- G2: 350+ reviews

Best for:

Fast-growing digital businesses, fintechs, and online stores want transparent, self-serve fraud detection with deep data enrichment and direct control over rules, where in-house teams can act on signals.

8. Sift

Sift is a US-headquartered, AI-driven fraud prevention platform that scores user actions in real time across a large global events network, covering payment fraud, account takeover, and content abuse for online businesses.

Key strengths:

Sift processes a very large volume of events across its network, which feeds real-time risk scoring on payments and user actions. Reviewers rate its support and detection well. Its breadth across payment fraud, account abuse, and content moderation suits platforms with multiple fraud surfaces.

Considerations:

Sift returns scores and decisions but does not provide a chargeback guarantee, so liability stays with the merchant. Realising its accuracy depends on tuning models to your traffic, which rewards an analyst-equipped team.

Certifications and recognitions:

- PCI DSS compliance

- SOC 2 Type II

Ratings (as of June 2026):

- G2: 4.6 / 5 (600+ reviews)

- Limited consumer Trustpilot presence (B2B platform)

Best for:

Online platforms and marketplaces with multiple fraud surfaces (payments, accounts, content) that want a single real-time scoring engine and have the team to tune it, accepting that liability stays in-house.

9. Signifyd

Signifyd is a US-headquartered commerce protection platform offering chargeback-guaranteed decisions powered by a large merchant network, with a focus on recognising returning shoppers across stores to approve more orders.

Key strengths:

Signifyd’s merchant network lets it recognise a high share of returning shoppers, supporting high approval rates with a financial guarantee against fraud chargebacks on approved orders. It was named to G2’s Best Commerce Software Products of 2026 list. Its guarantee shifts fraud-chargeback liability off the merchant’s balance sheet.

Considerations:

Some reviewers cite false positives on legitimate orders and find the platform expensive for smaller businesses. Like other guarantee vendors, it focuses on transaction decisions rather than upstream document-based identity verification.

Certifications and recognitions:

- PCI DSS compliance

- SOC 2 Type II

Ratings (as of June 2026):

- Limited consumer Trustpilot presence (B2B platform)

Best for:

Mid-market and enterprise retailers want a chargeback guarantee and high approval rates from a large shopper-recognition network, with a budget that suits the guarantee model.

10. Stripe Radar

Stripe Radar is the fraud detection layer built into the Stripe payments platform, applying machine-learning risk scoring to transactions processed through Stripe, with configurable rules for teams already on Stripe’s stack.

Key Strengths:

For merchants already processing payments with Stripe, Radar adds fraud scoring with no separate integration, learning from Stripe’s network of transactions. It offers configurable rules and is straightforward to enable, making it the path of least resistance for Stripe-native businesses.

Considerations:

Stripe Radar is tied to the Stripe payments ecosystem, so it is not an option for merchants processing through other gateways, and it scores transactions rather than offering a chargeback guarantee, leaving fraud liability with the merchant.

Certifications and recognitions:

- PCI DSS Level 1 (via Stripe)

- SOC 2 (refer to stripe.com for current trust documentation)

Ratings (as of June 2026):

- Limited consumer TrustPilot Presence

Best for:

Businesses already on Stripe for payments that want built-in fraud scoring with zero added integration, and have the capacity to tune rules to their transaction mix.

How to Choose the Right Ecommerce Fraud Prevention Software?

The vendor that fits is the one that covers your actual fraud surface, under a liability model your finance team accepts, on the platform you already run. Most merchants fall into one of three procurement situations.

Scenario 1: Shopify and mid-market stores wanting plug-and-play chargeback protection

For a Shopify or mid-market store whose main exposure is stolen-card checkout fraud and the chargebacks that follow, the priority is a guarantee model with native integration and minimal tuning. This is genuinely the specialty of the guarantee vendors: Signifyd and NoFraud offer chargeback-guaranteed decisions with strong Shopify and ecommerce integrations, ClearSale adds human-review accuracy for low false positives, and Riskified suits larger merchants optimising approval rates. Shufti’s role here is the identity layer: if your fraud is increasingly account-takeover, synthetic accounts, or stolen logins rather than only card-not-present checkout, pair Shufti’s identity verification with a guarantee tool so you cover both the account and the transaction, not just the payment.

Scenario 2: Global and cross-border merchants facing identity fraud in high-risk markets

For merchants selling cross-border, especially into Latin America, the Gulf, Southeast Asia, and South Asia, Shufti is the structural fit. Its owned full stack is trained on and actively verifying 10,000+ document types across 240+ countries every month, with 99.7% OCR accuracy across 150+ languages where Western-trained models degrade, and a doc-less hub of 270+ authoritative data sources plus 40+ eID integrations for markets where document quality is uneven. Payment-scoring engines tuned for North American card data cannot match that regional identity depth. ClearSale is a narrower specialist where the priority is Latin American transaction review with a guarantee, and Trulioo-style data aggregation fits where only non-document verification is viable, but for owned, retrainable accuracy across many hard markets at once, Shufti is the broadest single answer.

Scenario 3: Enterprise marketplaces facing multi-vector fraud and deepfakes

For enterprise marketplaces facing account-takeover, synthetic identity, and deepfake attacks on identity steps, the deciding factor is defensible identity proofing. Shufti leads here on the strength of iBeta Level 3 conformance, the highest published presentation-attack detection standard held by only three vendors globally, combined with full-stack ownership that lets its team retrain defences on its own timeline as attacks evolve, validated by its DHS RIVR 2025 Top Performer result. For the transaction-decision layer alongside it, Forter and Sift are strong on real-time behavioural scoring, and AU10TIX-style tools specialise in synthetic-identity monitoring, but none of those provides independent Level 3 liveness conformance. The enterprise pattern is Shufti for the identity and anti-deepfake layer, paired with a transaction engine for payment decisions.

Marketing pages don’t reveal the right vendor. Fraud performance on your actual traffic does. The procurement question is which vendor’s structural advantages match your specific reality: where your customers live, which fraud vectors hit you hardest, whether you need liability transferred or signals to act on, and how exposed you are to AI-driven identity attacks. For merchants whose exposure runs through identity, account, and cross-border fraud, Shufti’s combination of full-stack ownership, iBeta Level 3 conformance, global document depth, and deployment flexibility is the broadest single-vendor answer, paired with a guarantee tool where chargeback liability transfer is the goal. The only way to confirm is a proof of concept on your own traffic.

Run a proof of concept on your hardest fraud cases, account-opening, cross-border, and deepfake scenarios and benchmark the result against any vendor on this list, through a live walkthrough with Shufti.

Frequently Asked Questions

What is e-commerce fraud prevention software?

Ecommerce fraud prevention software detects and blocks fraudulent activity across an online store, from account opening and login to checkout. It combines identity verification, behavioural and device signals, and machine-learning risk scoring to stop payment fraud, account takeover, synthetic identities, and chargebacks while approving legitimate customers.

What are the top ecommerce fraud prevention tools in 2026?

Leading options in 2026 include Shufti for identity and onboarding fraud, guarantee platforms Signifyd, Riskified, NoFraud, and ClearSale for chargeback protection, and score-based engines Sift, Kount, SEON, Forter, and Stripe Radar for transaction risk. The best choice depends on your fraud surface, markets, and platform.

How does AI improve ecommerce fraud detection in 2026?

AI improves ecommerce fraud detection by scoring thousands of signals per transaction in real time, learning new attack patterns faster than static rules, and reducing false declines that reject good customers. It also powers liveness and deepfake detection at identity steps, catching synthetic and spoofed identities rules-based systems miss.

Which fraud prevention software is best for Shopify stores?

For Shopify fraud protection, guarantee platforms like Signifyd and NoFraud offer native apps and transfer chargeback liability with minimal setup, while ClearSale suits low-false-positive needs. Stores also facing account-takeover or cross-border identity fraud should add an identity layer such as Shufti alongside a transaction tool.

What types of fraud does ecommerce fraud prevention stop?

It targets card-not-present payment fraud, chargebacks and friendly fraud, account takeover, synthetic and stolen identities, promotion and refund abuse, and deepfake or document fraud at verification steps. Transaction-scoring tools focus on payment and chargeback fraud; identity-led tools stop account-opening and impersonation fraud upstream.

How does chargeback prevention software work?

Chargeback prevention software scores each order for fraud risk and approves, declines, or flags it before fulfilment. Guarantee vendors approve or decline and reimburse fraud chargebacks on orders they approved, transferring liability. Score-only tools return a risk decision and leave chargeback liability with the merchant to manage.