Asia-Pacific generates more of the world's growth than any other region. As digital-first businesses scale across these economies, synthetic identity fraud intensifies and KYC obligations tighten in step, yet most still run on identity verification infrastructure that cannot keep pace. Drawing on Shufti's internal verification data, this whitepaper maps that gap, including the finding that some of the region's most digitally developed economies record among the highest fraud rates, and sets out what it takes to close it.

Verification volume is increasing, but identity verification infrastructure is not keeping pace

APAC contributes nearly 60% of global growth. Social commerce is going mainstream, real-time payments are exploding, and population-scale digital public infrastructure like India's DigiLocker and Singapore's Singpass is putting verification at the centre of everyday life.

Every account opening, KYC refresh, age-gated purchase, payment authentication, and lending decision is a verification moment. It is the point where a business must decide, in milliseconds, whether the person on the other end is who they claim to be, and increasingly whether they are a person at all.

Two pressures are converging. Fraud is climbing fastest in the region's most digitally mature economies. As remote onboarding increases and the threat landscape evolves, the regulations governing remote onboarding and identity verification become equally stringent, and once-optional mandates are now legally binding.

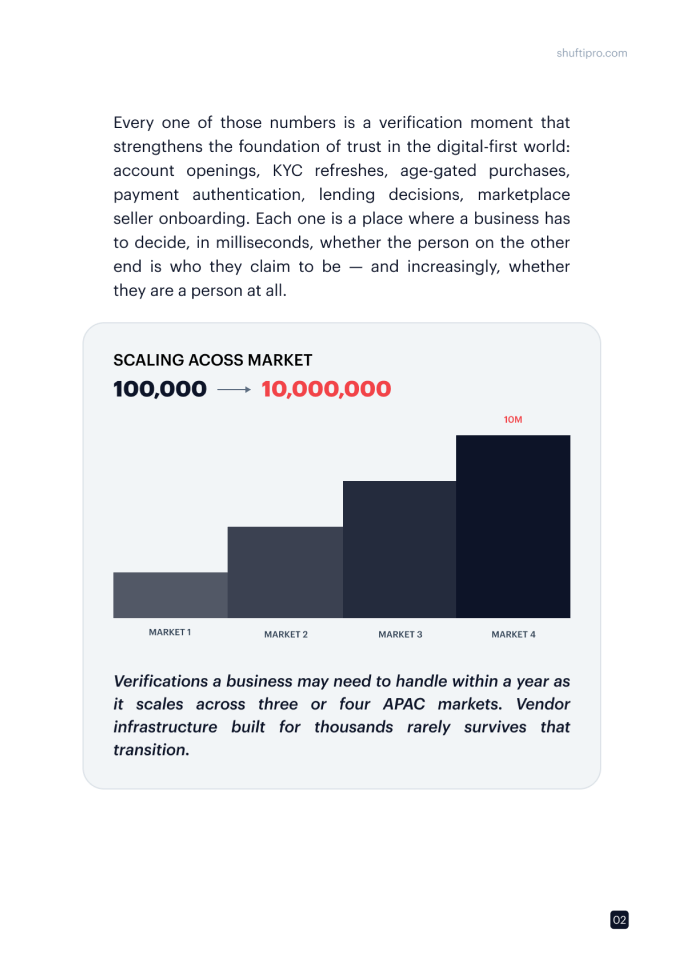

100K → 10M

As a business expands from one APAC market to the next, its verification volume can climb from 100K to 10 million, and the identity infrastructure beneath it must scale to match.

Digital Maturity & Fraud Exposure

The highest fraud signals show up where you'd least expect them

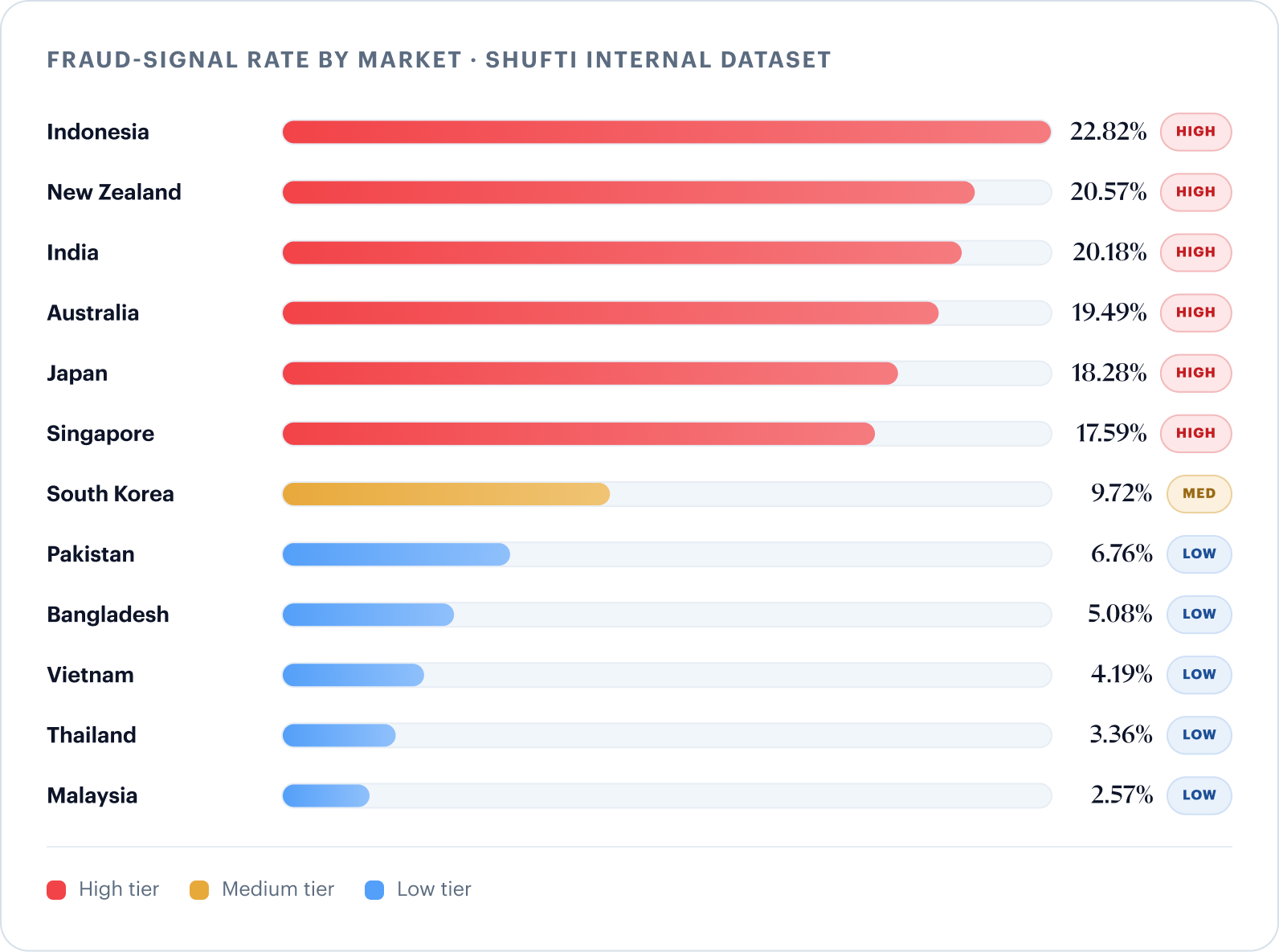

Across a sample of prominent APAC economies, the highest fraud-signal rates appear in the region's most digitally mature markets, not the ones most readers would expect.

The likely explanation is that digital maturity and the density of digital-first businesses scale together. More remote KYC means more attack surface, more attempts, and a higher share of fraud caught at the verification step.

Why Verification Breaks at Scale

Most IDV solutions are not trained on APAC scripts, so they fail on the region's documents

Most verification stacks assume a single national alphabet, two or three document formats, and one or two regulators per country. APAC breaks all of those at once.

Names appear in Latin, Devanagari, Khmer, Burmese, Tagalog, Vietnamese, Thai, Korean Hangul, simplified and traditional Chinese, Japanese (three concurrent scripts), Urdu, and Cyrillic. Thai and Khmer don't space between words, making OCR segmentation hard. Japanese dates may use imperial eras such as Showa, Heisei, or Reiwa instead of the Gregorian calendar. Korean names romanise inconsistently as Park, Pak, or Bak across systems, inflating false positives and negatives in screening.

The "frankenstack" problem. Most vendors answer APAC complexity by stitching together regional add-ons, using third-party OCR for one country, a liveness library for another, and a transliteration service for a third. A vendor that routes customer data through multiple sub-processors widens the breach surface and multiplies the privacy notices and data-processing agreements it must maintain. It also complicates the data-residency obligations that differ from market to market, leaving the buyer to account for a sub-processor chain it never designed.

The consequence is structural. It is not just friction on real customers or gaps for attackers, but a hard ceiling on expansion. An engine that can't reliably process APAC documents caps the markets a business can serve.

Evolving KYC Regulation

KYC regulations across APAC are growing fast

As remote identity verification becomes the norm across APAC, the laws governing it are evolving in step, raising the levels of assurance required, partly in response to deepfake-powered synthetic identity fraud and partly because legacy assurance levels no longer fit the remote onboarding that now defines financial services in the region.

India

RBI's Master Direction on KYC (updated August 2025) strengthened V-CIP expectations on spoof detection, liveness, and manipulation detection, moving beyond basic blink-and-smile toward deepfake-resistant controls.

Singapore

MAS' September 2025 Information Paper on deepfake cyber risks raises supervisory expectations on AI-generated identity fraud and non-face-to-face onboarding integrity.

Malaysia

Bank Negara's e-KYC Policy Document (revised April 2024) legally mandates liveness detection with prescribed FAR/FRR thresholds and independent assessment of document, biometric, and liveness modules.

Philippines

BSP's eKYC framework (Circular 1170) has accelerated remote onboarding, with biometric liveness and PhilSys integration central to higher-assurance workflows.

Hong Kong

A 30 May 2025 SFC circular expanded non-face-to-face onboarding, recognising iAM Smart and biometric ePassport verification for overseas onboarding.

China

The amended Anti-Money Laundering Law (effective 1 January 2025) introduces mandatory beneficial-ownership identification and widens the perimeter to more non-financial sectors.

Australia

The AML/CTF Amendment Act 2024 brings lawyers, accountants, and real-estate professionals into mandatory IDV from 1 July 2026, while existing reporting entities comply from 31 March 2026.

Vietnam

In APAC markets such as Vietnam, administrative reform compounds the challenge for remote identity verification. Vietnam's 1 July 2025 restructuring merged 63 provinces into 34 and abolished the district tier, invalidating address fields across millions of documents overnight. A vendor without in-house technology, or one dependent on third-party engines it does not control, cannot customise at this depth and will keep trailing what the region's regulators require.

The Evolving Fraud Threat

Regulation is also evolving in response to identity fraud threats

Deepfakes have become operational fraud infrastructure, and like other regions, Asia-Pacific is among the hardest hit.

+600%

Increase in deepfake-related content tied to criminal activity in Southeast Asia, H1 2024.

UNODC, October 2024

USD 25M

Transferred by an employee after a deepfake-enabled video call impersonating senior executives in the Hong Kong Arup case.

CNN, May 2024

USD 4B+

Estimated laundered via the Cambodia-based Huione Group, Aug 2021 to Jan 2025.

US Treasury / FinCEN, 2025

Dark-web marketplaces now sell ready-made synthetic identity kits, including AI-generated avatars, cloned voices, forged document templates and biometric artefacts built to defeat onboarding. These techniques evolve so quickly that liveness models regarded as state-of-the-art only months ago can already fail against newer presentation attacks and deepfake variants.

Different sectors face different threats. Fintechs deal with mule accounts and SIM-swap takeover, crypto platforms with synthetic identities and Travel Rule evasion, lenders with forged income proofs, dating and forex platforms with romance and investment scams, and iGaming with multi-account abuse and underage onboarding. The common thread is that many of these originate at the verification layer itself.

Whitepaper

Scale verification across APAC without rebuilding it in every market

A quick preview of the real challenges of verifying identity across APAC, and what getting it right actually takes. Get the whitepaper.

It usually comes back to three problems that feed each other

01 — They don’t own the core of what they sell

OCR is licensed from one company, face match from another, and liveness from a third. When India’s RBI tightens a liveness rule, the vendor cannot act until its supplier updates first. The market shifts in weeks, but the vendor catches up only in quarters.

02 — Their identity verification engines are not built to read the identity documents people carry in APAC

Most OCR is trained on the Roman alphabet and clean, standardised IDs. Devanagari, Thai, Khmer, Hangul, Nastaliq Urdu, and heavily-accented Vietnamese behave nothing like Latin text, so a generic engine quietly rejects valid IDs and pushes real people into manual review.

03 — They can’t adapt fast enough to keep up with fraud

Deepfake injection, synthetic identities, and forged templates keep evolving, yet many vendors run static detection engines they rarely retrain. A model tuned for last year quietly goes blind to this year’s attacks.

The Cost of Getting KYC Wrong

Four costs, absorbed concurrently

When identity verification fails, the cost lands in four distinct ways, and most APAC businesses absorb all four at once. The most visible is the regulatory penalty, and the largest is the revenue lost to customers who abandon a verification flow they cannot complete.

$27.45M

In composition penalties across nine financial institutions in 2025, following MAS action on Singapore’s 2023 money-laundering case involving more than SGD 3 billion in seized or frozen assets.

Monetary Authority of Singapore, 2025

Operational fraud loss is less visible but often larger. Mule accounts feed laundering, synthetic identities take out loans that default, and deepfake-impersonated accounts trigger wire transfers that cannot be recalled. Trust loss is the least measurable but most strategic. A bank whose customers learn their identities can be cloned loses something no compliance budget buys back. The flip side is measurable, because frictionless onboarding correlates with higher acquisition and retention.

Choosing the Right IDV Vendor for APAC

The problem isn’t solved by a longer feature list. It’s an architectural decision.

Choose a solution which has built the core capabilities in-house, controls the roadmap end to end, and is designed from day one for the scripts, formats, regulatory rhythms, and threats the region actually produces. Use this checklist when you evaluate an identity verification solution for the APAC market:

Does the solution own its tech stack, so it can adapt to new regulations, risks and fraud without bottlenecking growth?

Can it hold accuracy, speed and automation steady as verification volumes and fraud pressure both rise?

Can its OCR verify diverse APAC documents and non-Latin scripts, and normalise transliterated data for CRM consistency?

Does the solution offer doc-less and eIDV coverage across APAC that delivers higher conversion in regional flows?

Does the solution catch synthetic identity and organised fraud through multiple tools without blocking legitimate customers?

Does the solution provide higher-assurance authentication for high-risk and step-up scenarios?

Does the solution continuously adapt as threat typologies evolve?

Does the solution offer continuous identity verification to prevent fraud across the customer lifecycle?

Shufti's Approach

An in-house, end-to-end stack built for this region

Shufti was built on this principle. OCR, document authentication, biometric matching, liveness, and deepfake detection are all developed in-house, with capabilities that improve in step with the emerging needs and demands of digital-first businesses. The document library covers over 10,000 documents across more than 240 countries and territories, including the regional variants that decide whether APAC flows work. The fraud-detection layer trains continuously, and APAC signals feed back into the same models.

Case study · Vietnam

Administrative restructuring and the address-logic problem

When Vietnam moved to a two-tier administrative structure on 1 July 2025, identity documents still showed the old three-tier structure while government databases followed the new one. Vendors that hadn't updated their address logic kept checking against obsolete hierarchies, systematically rejecting legitimate addresses. During the transition, Shufti's OCR sustained high field-level accuracy on the new chip-based citizen ID, while a comparable third-party benchmark lagged by 14 points. For the lagging vendor, that meant thousands of additional rejected legitimate customers per month.

Shufti OCR accuracy96.79%

Comparable third-party benchmark82.36%

Case study · Japan

Multi-layer detection breaking a coordinated network

A criminal network targeting a leading Japan-based crypto exchange submitted multiple slightly altered originals of the same documents, each presented as a distinct customer. Traditional systems accepted each on its merits. Shufti's stack treated them as a connected set. While document and biometric layers flagged suspicion, the device-fingerprinting, IP-intelligence, and browser-behaviour layers traced the applications to a single originating device. What looked like independent onboardings was one coordinated attack, caught at the verification step rather than after accounts had opened.

Where it fits, doc-less eIDV removes the long forms, repeated requests, and upload failures that drive abandonment, already supporting Aadhaar via DigiLocker in India, Singpass in Singapore, ConnectID in Australia, and PhilSys in the Philippines, with the network expanding as new rails come online. Verifying against trusted identity databases and eIDs, backed by the higher assurance that iBeta Level 3 conformance brings to remote onboarding, lifts completion rates while holding fraud down, which is precisely what APAC businesses need in order to grow without identity verification becoming a bottleneck. Where eIDV isn't the right control, the biometric stack carries the assurance, independently assessed as iBeta PAD Level 3 conformant under ISO/IEC 30107-3, with 0% APCER and 0% BPCER on iOS and Android.

01 - 04

Certifications

Independently audited and certified for enterprise-grade security and data protection.

Frequently Asked Questions

Most verification stacks assume a single national alphabet, a few document formats, and one or two regulators per country. APAC breaks all of those at once. Names appear in Latin, Devanagari, Khmer, Burmese, Thai, Hangul, Chinese, Japanese, Urdu and Cyrillic scripts; date and address conventions vary; and regulators issue new technical mandates each quarter. A stack built for one market rarely survives expansion into three or four.

Was This Content Helpful ?

Recent moves include India's RBI Master Direction update (August 2025) strengthening V-CIP liveness and deepfake-resistance expectations; Singapore's MAS Information Paper on deepfake cyber risks (September 2025); Malaysia's Bank Negara e-KYC policy mandating liveness with FAR/FRR thresholds; the Philippines' BSP eKYC framework; Hong Kong's SFC recognition of iAM Smart; China's amended AML Law (effective January 2025); and Australia's AML/CTF Amendment Act 2024 extending IDV obligations from 2026.

Was This Content Helpful ?

A vendor that owns its core technology (OCR, document authentication, face matching, liveness, and deepfake detection on a single roadmap) so it can adapt within weeks of a regulatory change. Look for OCR proven on diverse APAC documents and non-Latin scripts, doc-less and eIDV coverage for higher conversion, layered detection of synthetic and organised fraud, and step-up assurance for high-risk scenarios.

Was This Content Helpful ?

eIDV verifies identity against an authoritative source of truth rather than a submitted document, removing the long forms, repeated information requests, and upload failures that cause onboarding abandonment. Shufti supports Aadhaar via DigiLocker in India, Singpass in Singapore, ConnectID in Australia, and PhilSys in the Philippines, with the network expanding as new national rails come online.

Was This Content Helpful ?

In Shufti's internal verification dataset, Indonesia shows the highest identity-fraud-signal rate among the APAC markets sampled, at 22.82%, ahead of New Zealand at 20.57% and India at 20.18%. The rates reflect documents flagged for failing authenticity, originality or integrity checks across client businesses.

Was This Content Helpful ?

The most digitally mature markets attract the most fraud, because higher verification volumes and digital-first onboarding give attackers a larger surface to target. In Shufti's data, developed economies such as New Zealand, Australia, Japan and Singapore sit in the high-fraud tier alongside Indonesia and India.

Was This Content Helpful ?

Deepfakes have become operational fraud infrastructure. Dark-web marketplaces sell ready-made synthetic identity kits, and liveness models can fail against newer presentation attacks, which is why APAC regulators including India's RBI and Singapore's MAS are moving towards deepfake-resistant liveness requirements for remote onboarding.

Was This Content Helpful ?

Form submitted successfully!

Thank you for your interest — your report is

loading now.

Scale verification across APAC without rebuilding it in every market

Get the full whitepaper: the fraud-exposure data, the regulation map, and the vendor checklist. Then talk to us about what clean APAC expansion actually looks like.

Back

Back