iGaming

The island's largest buyer of identity verification, 315 licensed companies at end-2024, reaching about a tenth of Malta's economy.

Latest

Latest

Latest

Latest

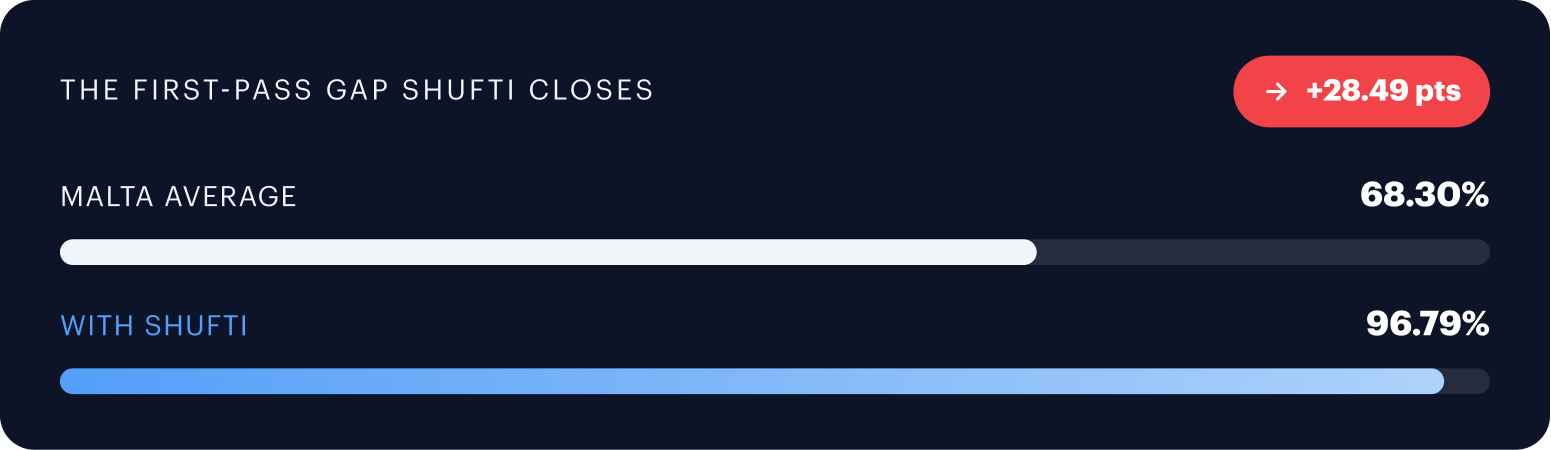

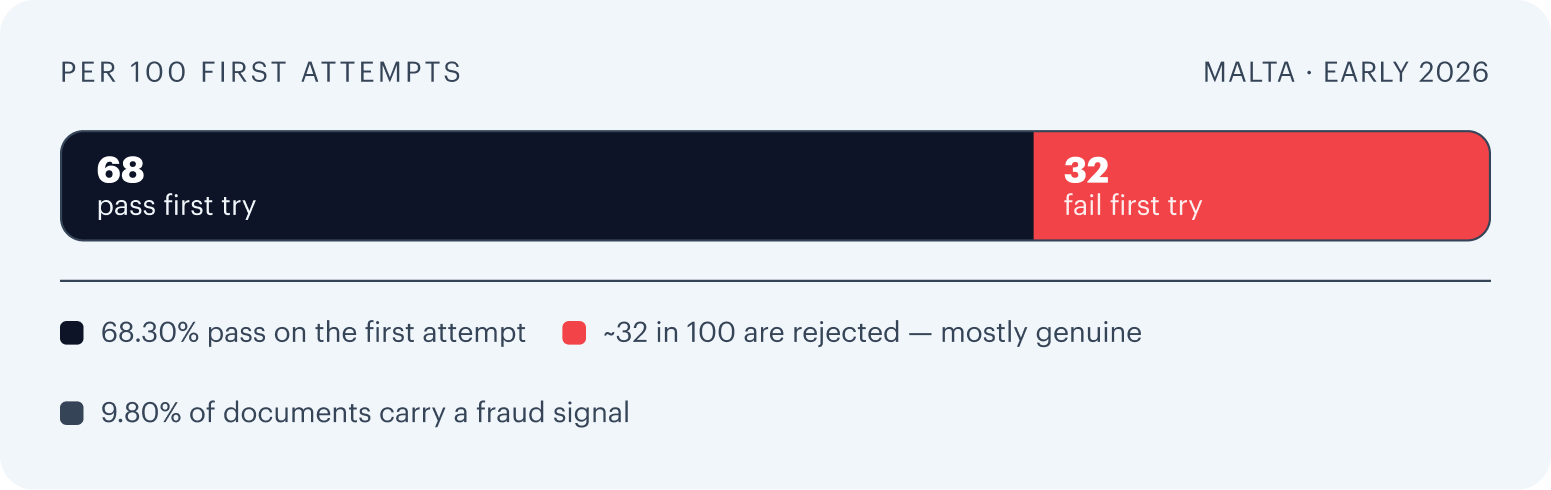

Nearly one in three identity checks in Malta fails on the first attempt. This playbook shows why Maltese e-ID, gaming, and fintech onboarding stalls, and the verification controls that move first-pass rates from 68% toward 97%.

Schedule a Demo

Overview

Malta clears fewer first-attempt verifications than its reputation as a digital-finance hub suggests. Across early 2026, fewer than seven in ten checks passed on the first try, and almost one in ten documents carried a fraud signal. The same data shows that gap is recoverable.

Regulatory context

Malta runs one of the strictest onboarding regimes in the EU because it has something to prove. In June 2021 it became the first EU member state placed on the FATF grey list, and it spent the following year rebuilding beneficial-ownership registers, financial-intelligence cooperation, and enforcement before the FATF removed it in June 2022. That episode reset expectations for every regulated business on the island.

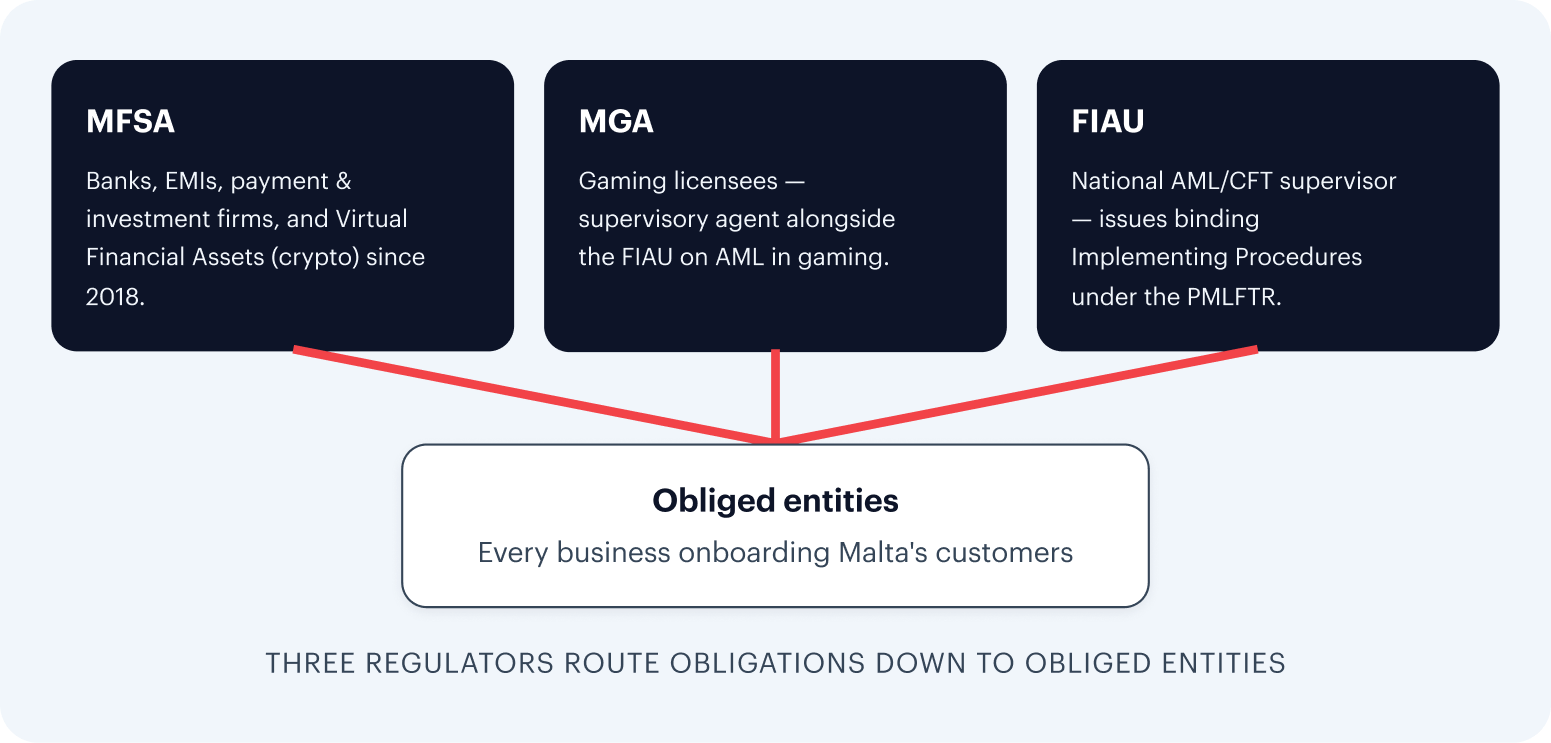

Three regulators now share that bar, and most Malta operators answer to at least one of them.

The pressure does not ease in 2026, it concentrates. Two hard deadlines now sit ahead of Malta's regulated firms.

For crypto firms the nearer cliff is MiCA: existing Malta providers must hold MFSA authorisation as a crypto-asset service provider by 1 July 2026. For the wider market, the EU's single AML rulebook applies from 10 July 2027, and the new EU Anti-Money Laundering Authority is already operating. Onboarding fixed in 2026 meets the harmonised standard early.

Scope

A Malta verification answers to three regulators and has to read the documents a small, heavily international economy puts in front of it. Knowing both is what separates a configured flow from a generic one.

The island's largest buyer of identity verification, 315 licensed companies at end-2024, reaching about a tenth of Malta's economy.

The most time-pressured group, existing providers must hold MFSA authorisation under MiCA by 1 July 2026 or stop serving the market.

Banks, EMIs and payment firms carry the same customer due-diligence bar under FIAU Implementing Procedures.

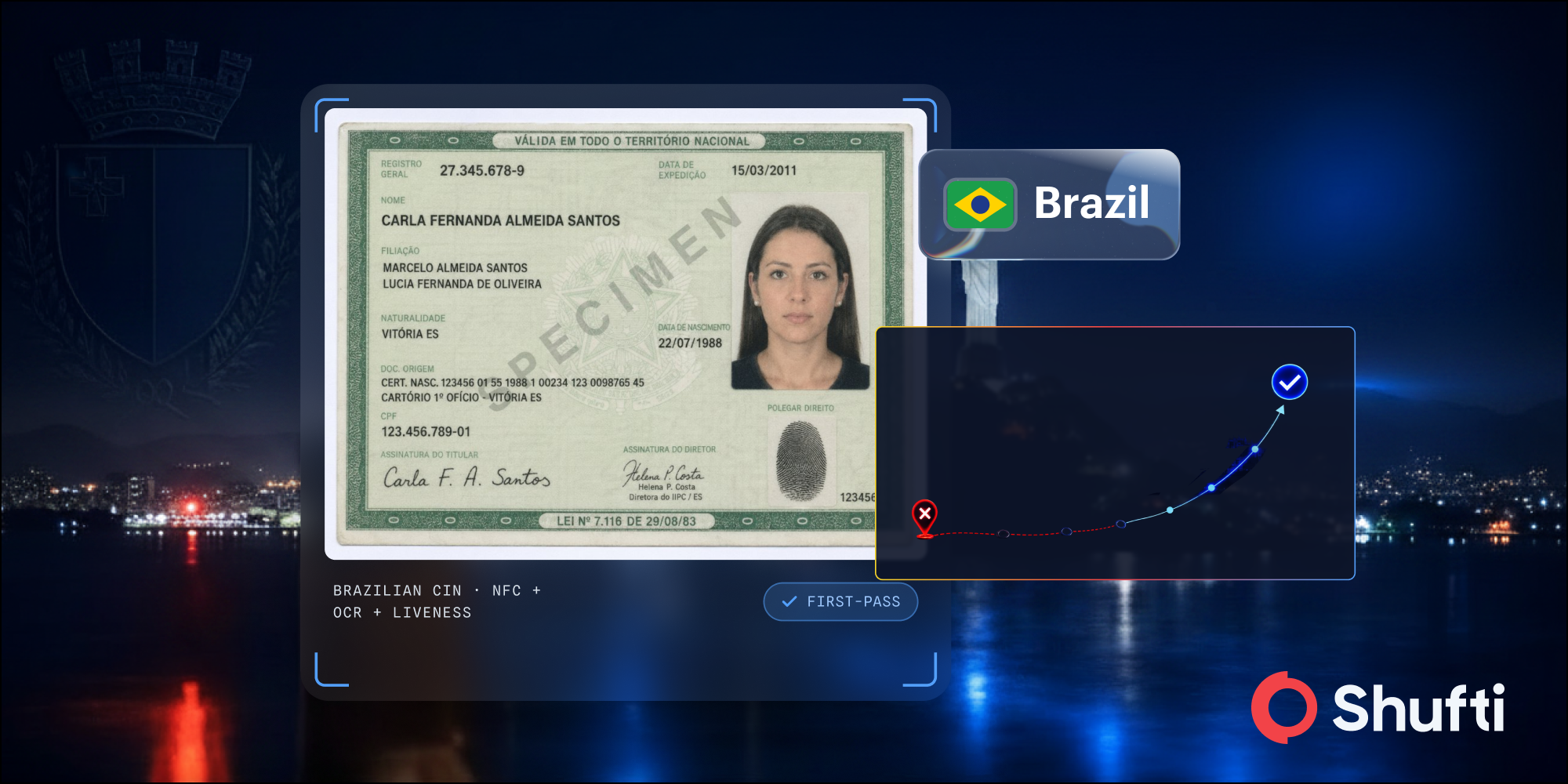

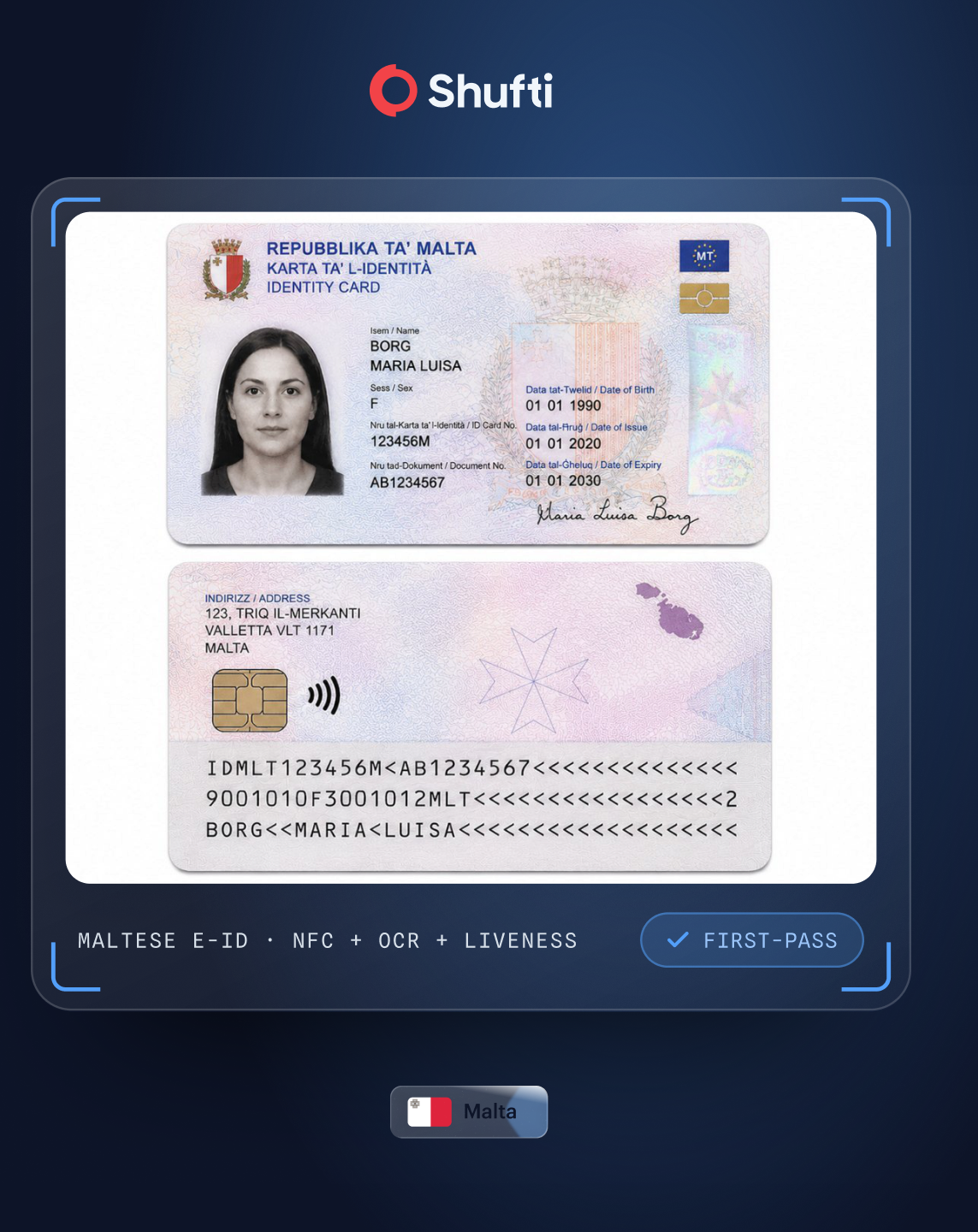

Maltese e-ID: a biometric card issued by Identità to citizens aged 14 and over, with a contactless chip and EU Regulation 2019/1157 security features.

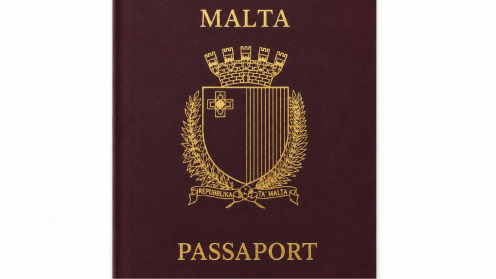

Maltese e-passport: carries an ICAO-standard chip that NFC verification can read for the highest assurance when a flow supports it.

Residence permits: appear regularly across the island's resident and expatriate population.

Foreign passports & national IDs: a constant stream, because Malta's platforms onboard customers worldwide.

Failure points

Most Malta verification failures are capture and document problems, not fraud. Close to 32 of every 100 first attempts fail, and the document fraud rate sits at 9.80%. The two most common rejection reasons are submitted screenshots and scanned copies and the Maltese e-ID adds two traps that generic OCR walks straight into.

The cost lands fast. MGA-licensed operators apply bank-grade KYC and onboard players from around the world, so every first-attempt failure either pushes a genuine customer toward a competitor or into a manual review queue. One configuration has to read a Maltese e-ID and the foreign passports and national IDs those players carry with equal accuracy.

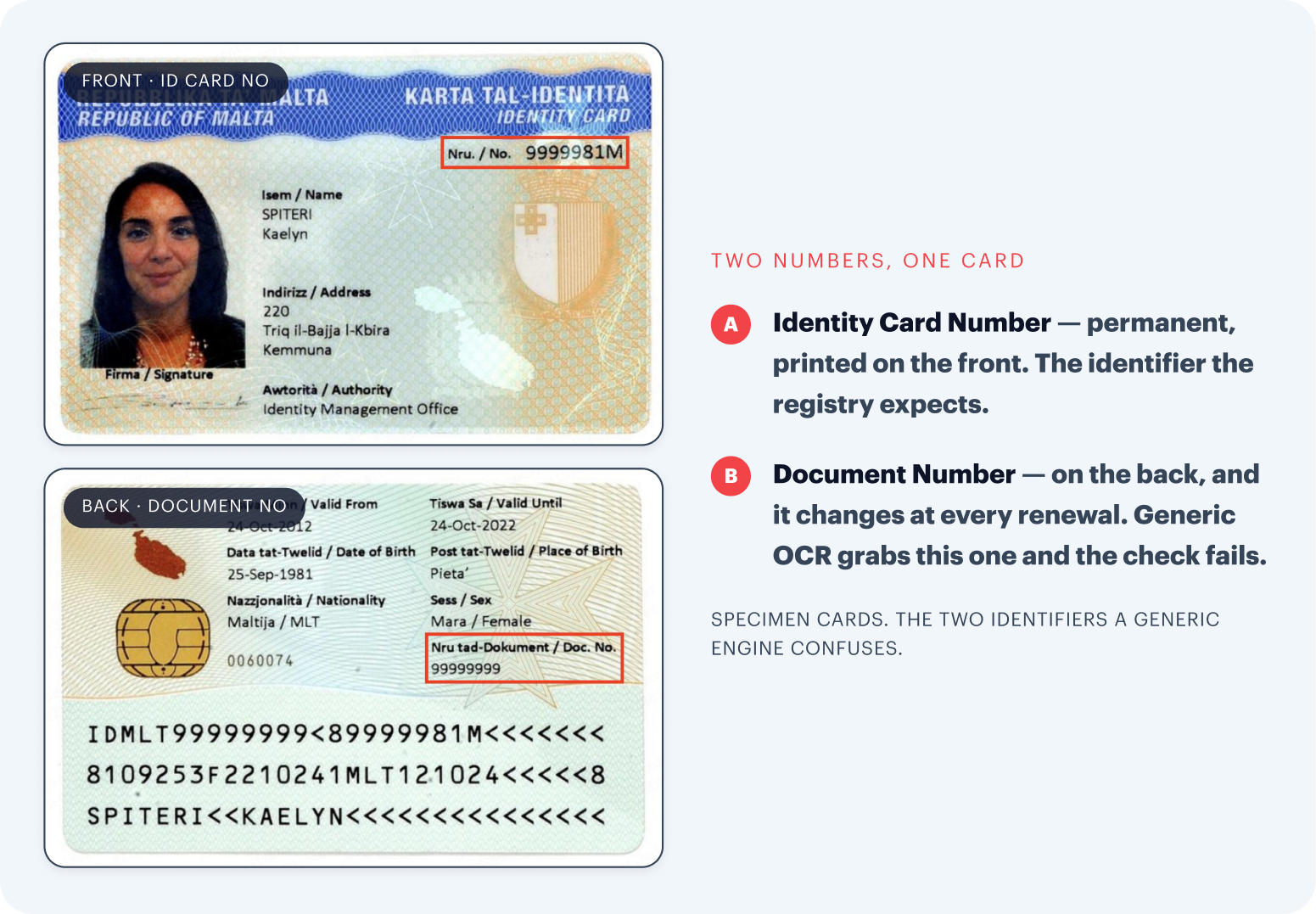

The Maltese e-ID prints a lifetime Identity Card Number and a separate Document Number that changes at every renewal. Generic OCR extracts the wrong one and the check fails against the government registry, and it recurs, because each renewal issues a new Document Number.

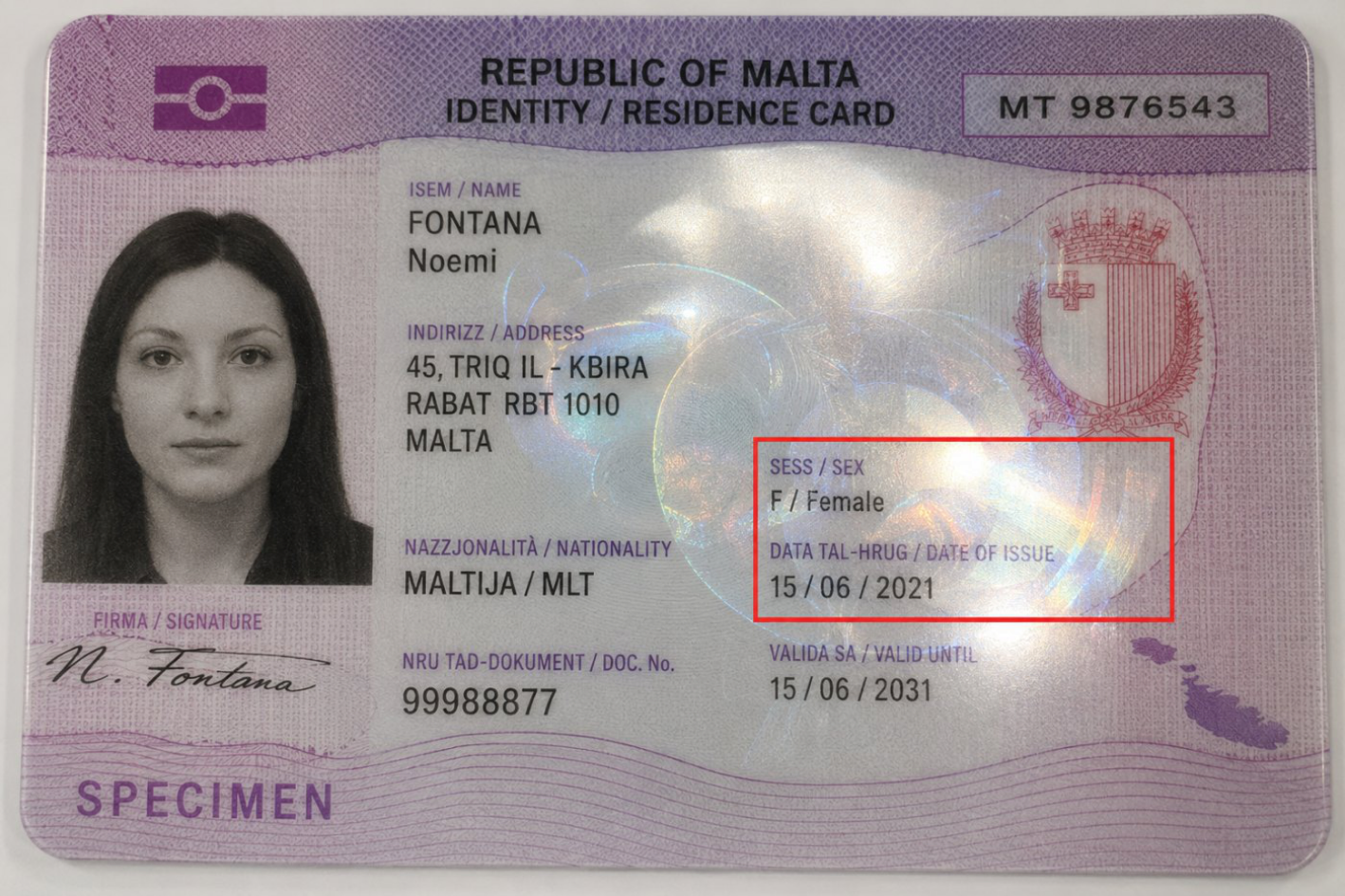

High-gloss polycarbonate throws glare on phone cameras, and Kinegram and transparent-window holograms sit directly over the Sex and Date of Issue fields. The same anti-forgery features that prove the card is genuine are what defeat a phone-camera read, often producing a poor document quality rejection.

Users submit a screenshot or photograph one screen with another device, so the engine sees a screen, not a document. A screen capture also fails liveness and authenticity, through moiré, screen glare, and the absence of depth, so even a perfectly legible screenshot is correctly refused.

Scanned or photocopied IDs strip out the security features an authenticity check depends on. A flat copy removes the optically variable features, holograms and OVI, that prove a card is real, so a genuine document fails the authenticity test, not only the OCR.

None of these are exotic. They are the everyday reality of verifying a small, document-modern, expat-heavy market through a phone camera.

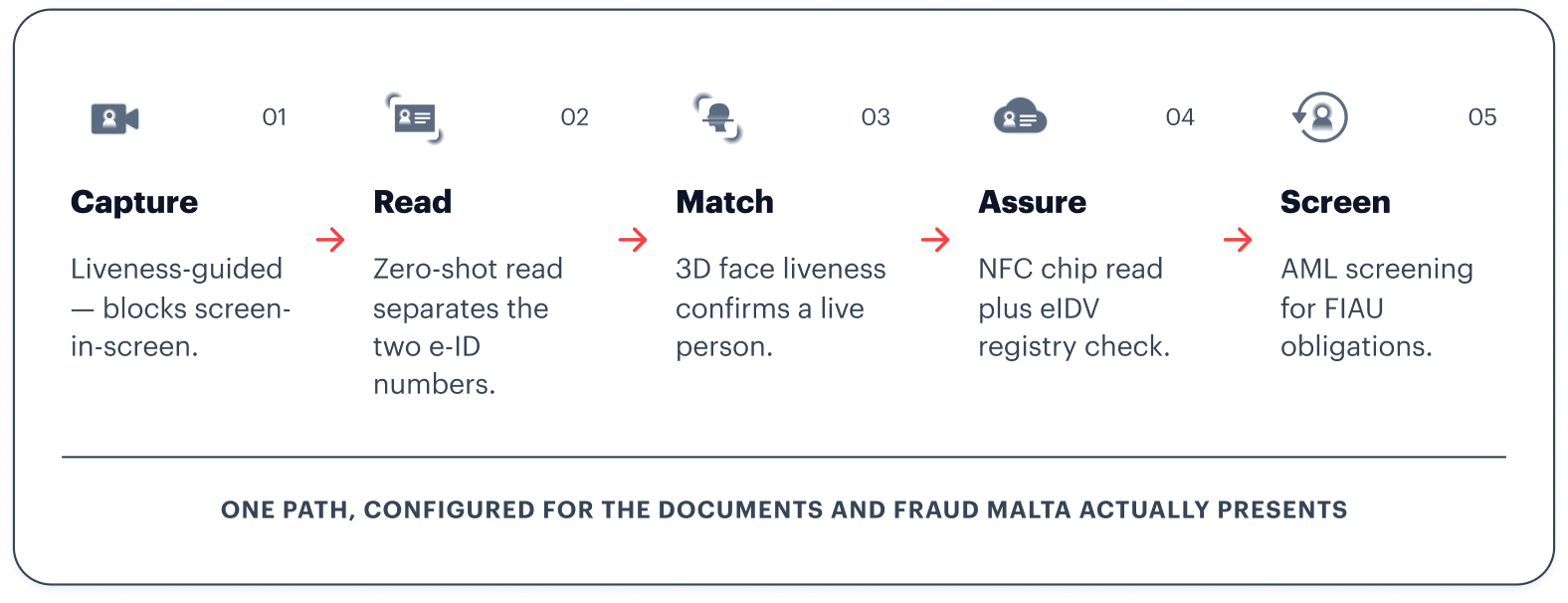

The failure points above map to specific controls. See how document verification, liveness detection and AML screening tie back to MGA and FIAU obligations on the Malta page..

Explore Shufti for MaltaThe fix

Shufti raises Malta's first-pass rate to 96.79% by reading the documents Malta actually issues and rejecting the captures that should never count. The gain is not a discount on standards, it is the same checks, passing more genuine users on the first try.

+28pts

Moving from 68.30% to 96.79% means roughly 28 in every 100 genuine applicants who used to drop out are now cleared automatically, fewer manual reviews, faster onboarding, and far less revenue lost at the front door. One configuration covers Maltese nationals and the island's large international player base.

Summary

Every failure point above maps to a control. This is the whole playbook on one screen.

| What fails | Why the check drops it | How it is solved |

|---|---|---|

| e-ID dual numbers | Wrong identifier sent to the registry | Zero-shot Document Verification separates the lifetime ID number from the renewal Document Number. |

| Polycarbonate glare & holograms | Data fields hidden under light and overlays | AI trained on holographic interference recovers the obscured fields. |

| Screenshots & screen-in-screen | A screen is captured, not a document | Liveness-guided capture and device signals reject it at the source. |

| Scans & colour copies | Security features stripped out | Authenticity checks flag the missing features before review. |

| Expatriate & foreign documents | Single-market engines miss the format | One configuration reads documents from 240+ countries. |

Teams that prefer to build and price a stack without a sales conversation can configure one directly at any tier.

See the verification path built for the documents Malta issues and the captures that should never pass.

Malta's average first-pass rate is 68.30%, meaning fewer than seven in ten identity checks clear on the first attempt, based on Shufti verification data for January to May 2026. With Shufti, the first-pass rate for the same market reaches 96.79%.

The most common reasons are submitted screenshots and scanned copies, which strip out the features an authenticity check needs. Malta's e-ID adds two more: a card that carries both a lifetime Identity Card Number and a changing Document Number, and high-gloss polycarbonate with holograms that sit over data fields and blind generic OCR.

The primary document is the Maltese electronic identity card (e-ID), a biometric card issued by Identità to citizens aged 14 and over with a contactless chip. It shows a permanent Identity Card Number and a renewal-specific Document Number. Maltese e-passports and residence permits are also used, and Malta's international customer base means foreign passports and IDs appear often.

The Financial Intelligence Analysis Unit (FIAU) is the AML/CFT supervisor and issues binding Implementing Procedures. The Malta Financial Services Authority (MFSA) oversees banks, payment and investment firms, and Virtual Financial Assets, while the Malta Gaming Authority (MGA) supervises gaming licensees alongside the FIAU.

The EU's single rulebook, the AML Regulation, applies from 10 July 2027, and the new EU Anti-Money Laundering Authority is already operational. That makes 2026 the year for Malta-regulated businesses to bring onboarding and document checks up to standard before the harmonised rules take effect. Crypto firms face an earlier date: existing providers must hold MFSA authorisation as a crypto-asset service provider under MiCA by 1 July 2026.

Independently audited and certified for enterprise-grade security and data protection.

Form submitted successfully!

Thank you for your interest — your report is loading now.

Take the next steps to better security.

Get in touch with our experts. We'll help you find the perfect solution for your compliance and security needs.

Contact usStay ahead of the curve with fresh takes on the latest identity innovations.

Get in touch with our experts. We'll help you find the perfect solution for your compliance and security needs.

Contact us