About one in six identity checks in Mexico fails on the first attempt. This handbook shows why document diversity, name-order ambiguity, and spoofed captures stall onboarding, and how compliance teams move pass rates from 83% to 99%.

About one in six identity checks in Mexico fails on the first attempt. This handbook shows why document diversity, name-order ambiguity, and spoofed captures stall onboarding, and how compliance teams move pass rates from 83% to 99%.

83.10%Mexico's average first-pass rate

98.95%First-pass rate with Shufti

7.50%Document fraud rate

The first-pass gap Shufti closes→ +15.85 pts

Mexico average83.10%

With Shufti98.95%

That gain of roughly 16 points pulls back the genuine applicants who used to drop out at onboarding. Each recovered check means faster onboarding, fewer manual reviews, and lower cost per verification.

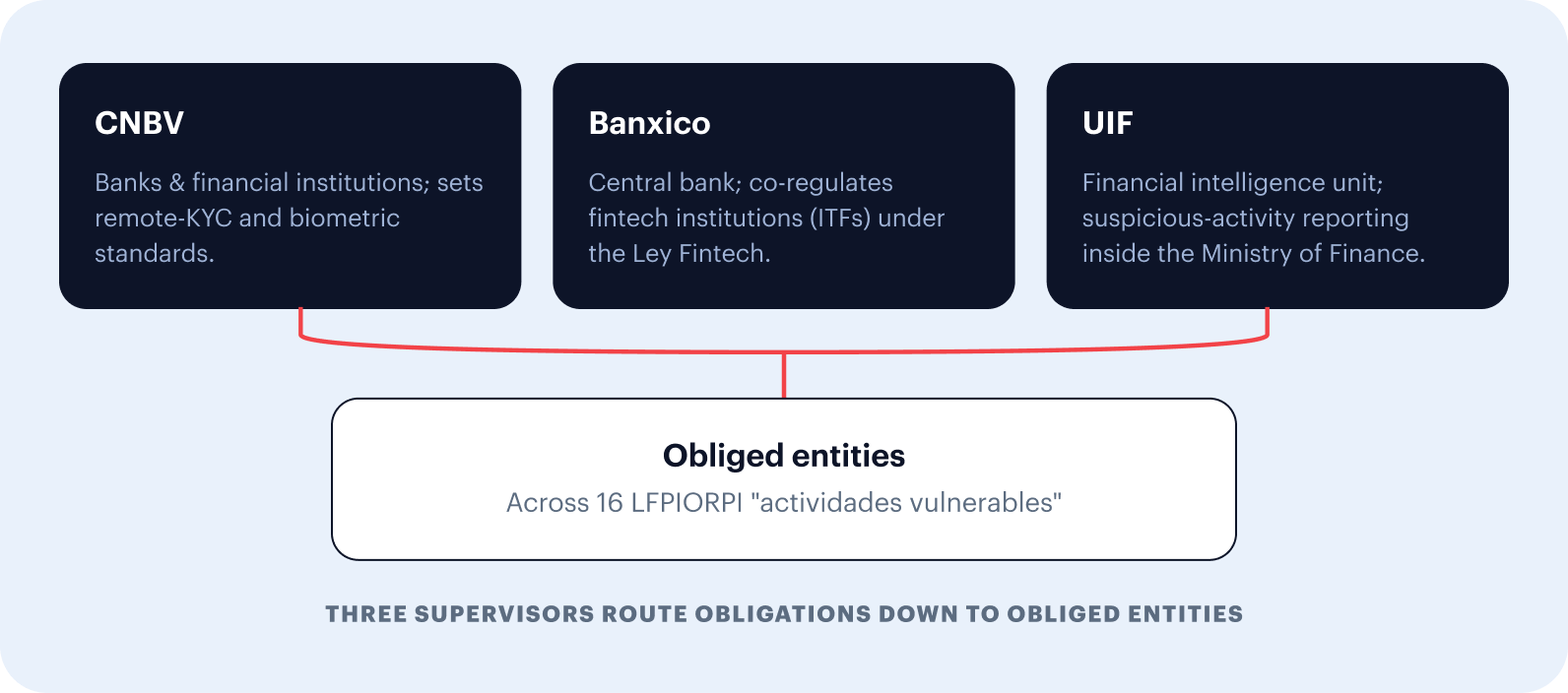

Regulatory Context

Why is Mexico's KYC bar higher than it looks?

Mexican onboarding answers to three authorities and an AML law that governs sixteen “vulnerable activities”, and 2026 is tightening the rules on beneficial ownership and PEP checks.

The CNBV (Comisión Nacional Bancaria y de Valores) supervises Mexico's banks and financial institutions. Banxico, the central bank, co-regulates fintech institutions. The UIF (Unidad de Inteligencia Financiera), a unit inside the Ministry of Finance, runs financial intelligence and suspicious-activity reporting.

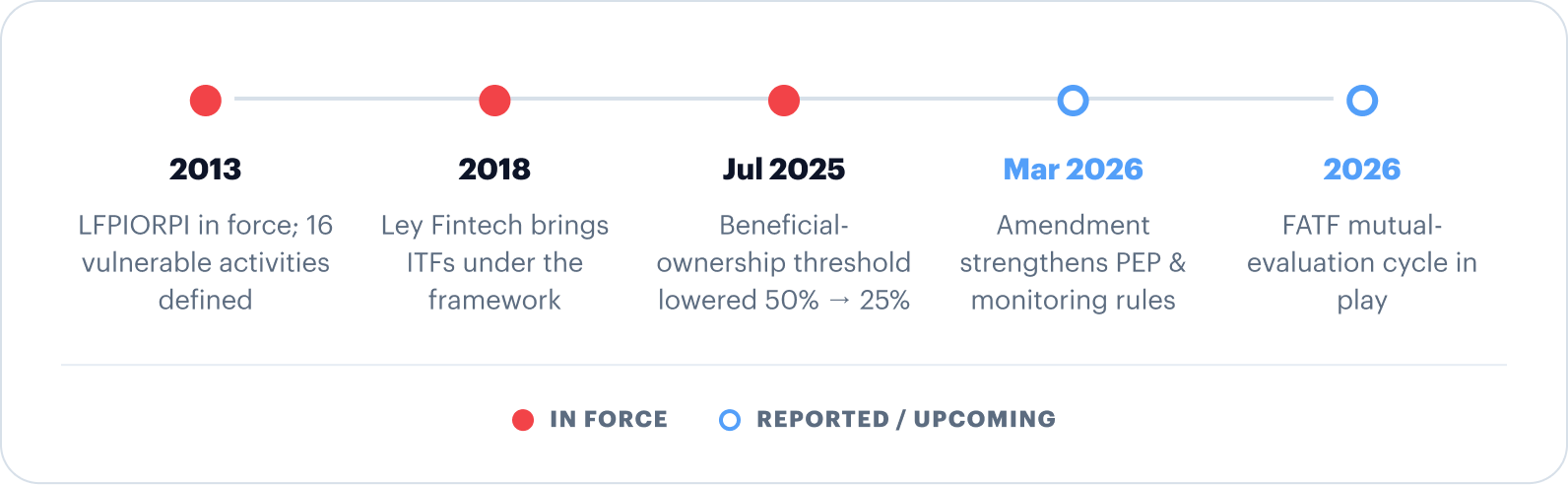

The backbone is the LFPIORPI, Mexico's AML law, enacted in 2012 and in force since 2013. It defines sixteen “actividades vulnerables”, from games and prepaid cards to real estate, virtual assets, and money transfer. Each one demands client identification, documentation, and screening.

The Ley Fintech (2018) brought fintech institutions (ITFs) under the same framework. Remote and biometric KYC is permitted under CNBV standards, including video identification, biometric matching, and liveness checks.

The bar is rising. A reported July 2025 LFPIORPI reform lowered the beneficial-ownership threshold from 50% to 25% (legal-firm analysis), and a March 2026 amendment is reported to have strengthened PEP and transaction-monitoring rules. With Mexico's 2026 FATF mutual-evaluation cycle in play, first-pass accuracy now carries real regulatory weight.

Scope

What does a Mexico verification actually have to read?

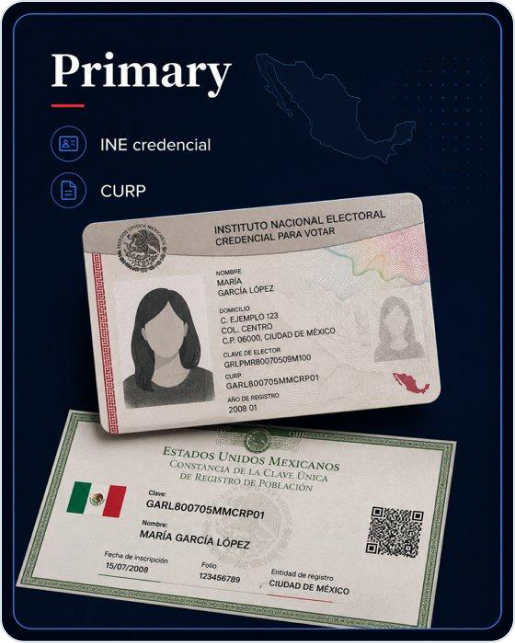

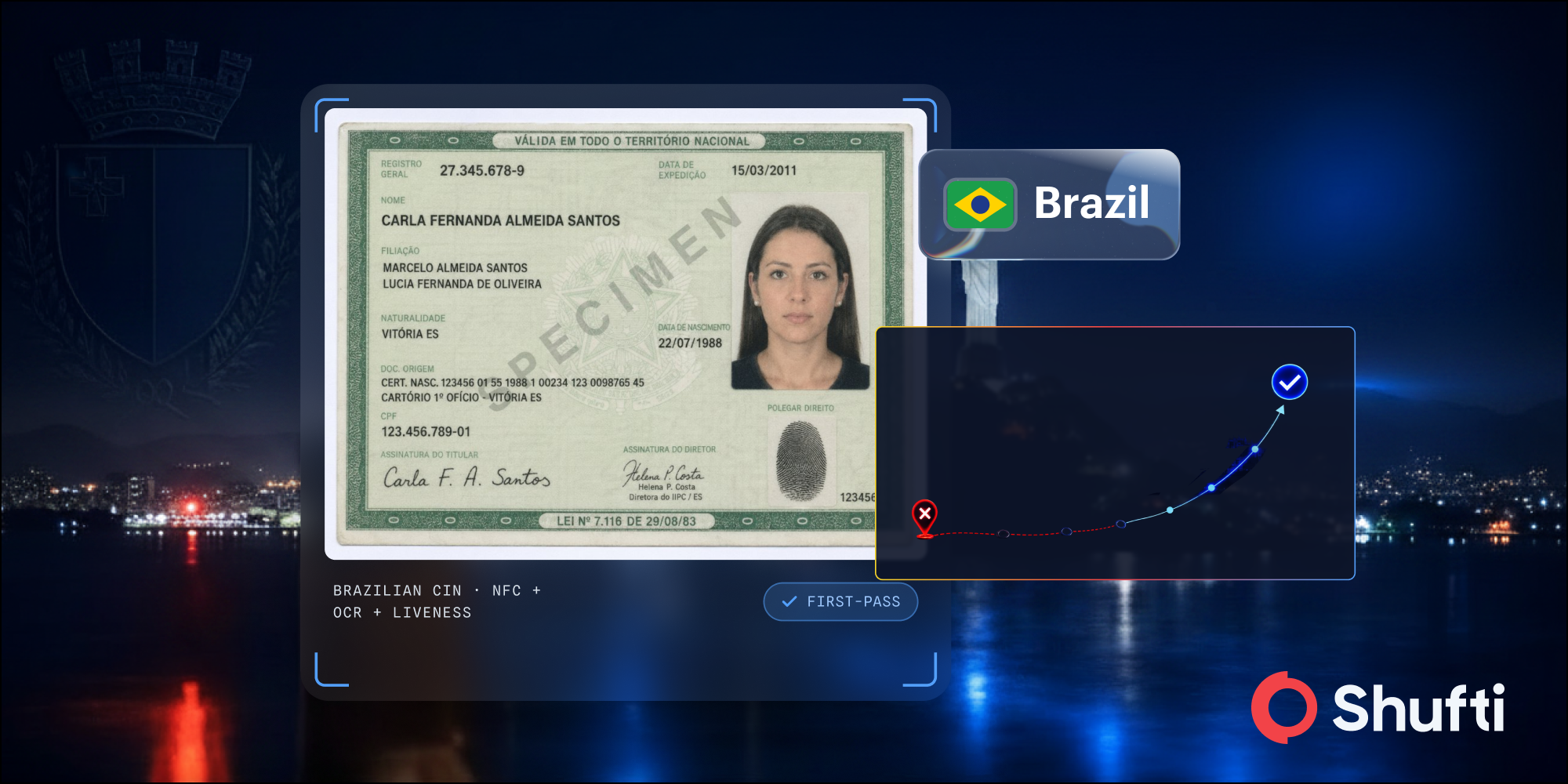

Mexico's de facto primary ID is the INE Credencial para Votar, but verification teams have to read across 57+ official document types issued at federal, state, and municipal levels.

The INE Credencial para Votar is the most widely accepted ID for KYC across banks, fintechs, and payment operators. It carries layered holographic security that protects the card but complicates the read.

Alongside it sits the CURP, Mexico's 18-character population registry code, administered by SEGOB through RENAPO. Both are foundational to identity in Mexico.

Beyond them, the framework recognises 57+ official IDs: Matrícula Consular, IMSS social-security cards, INM residence permits, SEGOB permanent-resident cards, passports, and state-by-state driving licences. The reader stack is not one template but dozens of variants, each with its own field positions, hologram placement, and graphic-heavy design. Generic, template-based verification struggles here.

Mexico's KYC document estate, grouped by type. Each issuer uses its own layout, fields, and security pattern.

Failure Modes

Why do first-pass rates drop in Mexico?

First-pass rates drop in Mexico because most rejections fall on genuine applicants, not fraudsters. A template-based engine stumbles on the country's document variety, inverts compound surnames, loses fields under holographic glare, and cannot separate a spoofed capture from a real one. Each problem is fixable; together they are the gap between 83% and 99%.

01

Document diversity and OCR layout chaos

Mexico recognises 57+ official identity documents, issued at federal, state, and municipal level, and the count keeps growing. Each state designs its own driving licence, so the name, CURP, and photo land in different places on every card. A template-based engine has to guess which field is which, and it guesses wrong on the variants it has never seen. The more document types you accept, the lower a template engine's pass rate falls, and every new state redesign quietly breaks it again.

Layouts shift across federal, state, and municipal issuers.

02

Name misreading and surname-order ambiguity

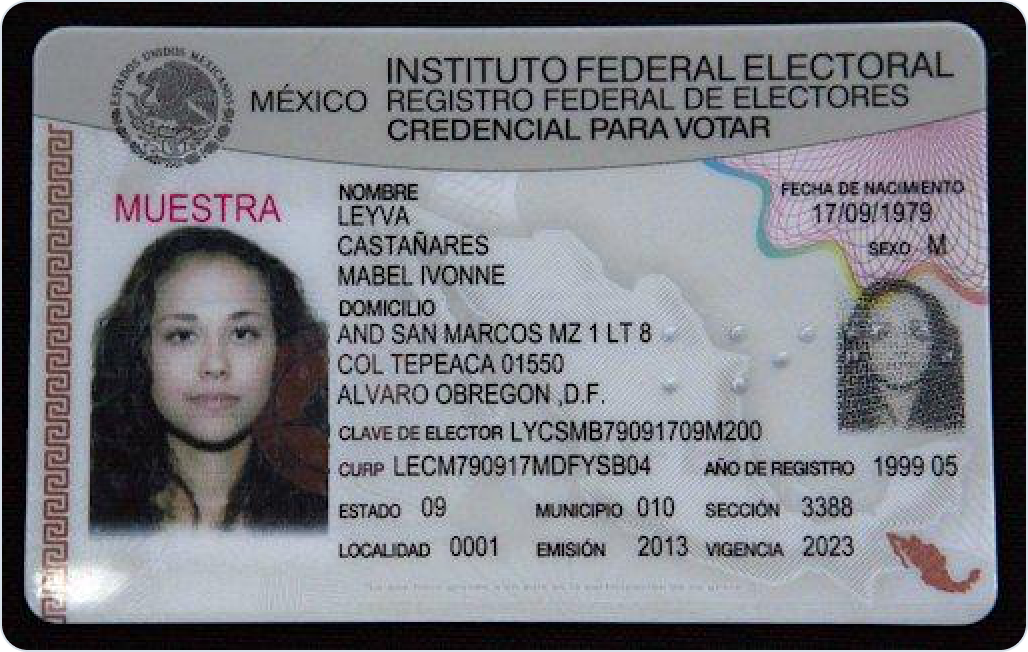

Mexican names carry a given name plus two surnames: the apellido paterno and the apellido materno. “LEYVA CASTAÑARES MABEL IVONNE” is the given name MABEL IVONNE with the compound surname LEYVA CASTAÑARES, but OCR with no local context reads LEYVA as the surname and the rest as first names.

That single inversion does double damage. It rejects a genuine applicant on a name mismatch, and it can fire a false sanctions or PEP hit that drags the case into manual review. A reported 2026 move toward flexible surname order only widens the gap.

The INE MUESTRA card: LEYVA CASTAÑARES MABEL IVONNE (compound surname + given names).

03

Holograms over key fields

For security, the INE credential and many state IDs print holographic overlays directly across the photo, the name, and the date fields. On a phone camera, flash and angle turn those overlays into glare that hides exactly the data the check needs.

A generic engine then returns blanks or garbled text for the date of birth or name, and the case is rejected or pushed to a human. The security feature meant to stop forgery ends up blocking genuine users.

Holographic overlays and wear sit over the data OCR needs.

04

Spoofed and manipulated captures

Most of Mexico's rejections are not clever forgeries; they are capture shortcuts and basic spoofs that an OCR-only flow cannot tell apart from the real thing. Five patterns dominate, in order of how often operators see them:

Colourcopy

A scan or photostat passed off as an original.

Screen-in-screen

A second screen displaying the document sits in the frame.

Altered document

Security features removed or data retouched.

Screenshot

A digital screenshot instead of a photo of the physical document.

5

Scanned document

A flat scan or PDF, losing the depth liveness needs.

Fix the gaps that stall Mexico onboarding

From INE and passport checks to liveness and continuous AML screening, see the coverage and onboarding detail Mexico operators need before they commit.

How does Shufti move Mexico onboarding from 83% to 99%?

Shufti raises Mexico's first-pass rate to 98.95% by reading the documents Mexico actually issues and rejecting the captures that should never count. It is the same checks, passing more genuine users on the first try.

Zero-shot OCR reads 57+ Mexican ID types, no per-template setup.

3

Parse

Context-aware parsing keeps apellido paterno & materno in order.

4

Match

3D face liveness at iBeta Level 3 confirms a real person.

5

Screen

AML & eIDV cover sanctions, PEP, adverse-media for UIF / LFPIORPI.

Reading the documents Mexico actually issues

Document Verification uses a proprietary zero-shot engine to read 10,000+ document types across 240+ actively processed countries in 150+ OCR languages, handling new INE designs and state-by-state licences with no per-template setup.

It reads through holographic glare using depth and texture, and applies Mexican civil-law name structure, so “LEYVA CASTAÑARES MABEL IVONNE” reaches screening in the right order rather than inverted.

Rejecting the captures that should never count

Face Verification runs at iBeta Level 3 conformance, the highest liveness standard, stopping screen-in-screen, screenshots, and altered captures in real time.

Document authenticity flags colourcopies and tampering at the moment of capture. For passports and advanced eIDs, NFC Verification reads the chip directly to confirm cryptographic authenticity.

Meeting Mexico's AML bar

AML Screening covers sanctions, PEP, and adverse-media watchlists for UIF and LFPIORPI obligations. Because names arrive correctly parsed, a surname-order slip no longer becomes a false match.

eIDV cross-checks the extracted data against government and financial sources to confirm the identity matches official records.

What higher pass rates are worth

Moving from 83.10% to 98.95% means roughly 16 in every 100 genuine applicants who used to fail now clear automatically. That is fewer manual reviews, faster onboarding, and lower cost per verification, with no control loosened.

The full stack is end-to-end proprietary, with no third-party aggregators, and runs as SaaS, Private Cloud, or fully on-premise for data-residency needs. Teams that prefer to configure and price without a sales call can do so at any tier via Shufti pricing.

Keep Reading

Your roadmap to a higher Mexico pass rate

See the verification path built for the documents Mexico actually issues, walk through INE, CURP, state licences, and the captures that should never pass with the Shufti team.

Raising Mexico's first-pass rate is not about relaxing checks; it is about reading each document correctly and rejecting only what truly should fail. Every issue above has one targeted control, and together they move first-pass approvals from 83.10% to 98.95%.

01

Document diversity: 57+ IDs across federal, state & municipal issuers

Control

Zero-shot OCR (10,000+ types, 150+ languages), no per-template setup.

Result

Every variant read on the first try, even new state designs.

Document authenticity, Face Verification at iBeta Level 3, and eIDV.

Result

Spoofs rejected at capture and genuine users pass, 83.10% to 98.95%.

Certifications

Independently audited and certified for enterprise-grade security and data protection.

Frequently Asked Questions

Mexico's average first-pass rate is about 83.10%, and with Shufti's full verification stack it reaches 98.95%. That is a gain of roughly 16 points. For every 100 genuine applicants, about 16 who would have failed on the first try now clear automatically.

Was This Content Helpful ?

KYC checks fail mainly for five reasons: colourcopies, screen-in-screen captures, altered documents, screenshots, and flat scans. Document diversity adds to this, because 57+ official ID types with different layouts and hologram placement overwhelm generic OCR. Surname-order misreads then push otherwise-clean applicants into AML mismatches.

Was This Content Helpful ?

Mexico's primary national ID is the INE Credencial para Votar. Teams also accept the CURP population registry code, plus 57+ official documents such as the Matrícula Consular, IMSS social-security cards, INM residence permits, passports, and state-issued driving licences.

Was This Content Helpful ?

The CNBV supervises banks and fintech institutions, and Banxico co-regulates ITFs under the Fintech Law. The UIF, inside the Ministry of Finance, handles financial intelligence. The AML backbone is the LFPIORPI, which governs sixteen vulnerable activities.

Was This Content Helpful ?

Mexico is reported to be working through an AML refresh in 2026: a July 2025 reform that lowered the beneficial-ownership threshold to 25%, a March 2026 amendment on PEP and monitoring rules, and its FATF mutual-evaluation cycle. The effect is tighter expectations on beneficial-owner checks, PEP screening, and name accuracy, so first-pass accuracy is now a compliance requirement, not just a cost lever.

Was This Content Helpful ?

Keep Reading the Mexico Handbook

Enter your email to continue, or close this and read on.

Take Your Mexico First-Pass Rate From 83% to 99%

Give genuine applicants the clean onboarding they expect, and give your team fewer manual reviews. See the verification path built for the documents Mexico actually issues.

Product Guide

Docless KYC Verification in APAC to Onboard More Genuine Users

Product Guide

EU AMLR Guide 2027: Requirements, Scope, Deadlines | Shufti

Product Guide

APAC Child Safety Age Verification Regulations

Product Guide

Docless Identity Verification in the Middle East

Product Guide

The Future of Docless Verification in Europe

Product Guide

Cyprus 2026 KYC Operators Guide to Improve First Pass Rate