Gated Guide Financial Crime & Identity Risk

The Deepfake Detection Gap: How Many of Your Verified Customers Never Existed?

Deepfake-powered synthetic identities passed your verification checks years ago. They're still in your portfolio, maturing toward bust-out, moving illicit funds, and quietly distorting your loss provisioning. Routine KYC remediation was never built to find them. This guide shows what is.

Request A Blind Spot Audit01 The Problem

Some of your "defaults" were never real borrowers

When a loan goes bad, it gets filed as a default: a real customer who couldn't repay. But a growing share of credit losses don't fit that story. They aren't borrowers who failed to repay. They're borrowers who never existed.

These are synthetic identities: profiles assembled with AI-generated or deepfaked credentials that passed your KYC checks, behaved like real customers, and built a credit history. Then they walked away from exposure no one can ever collect on.

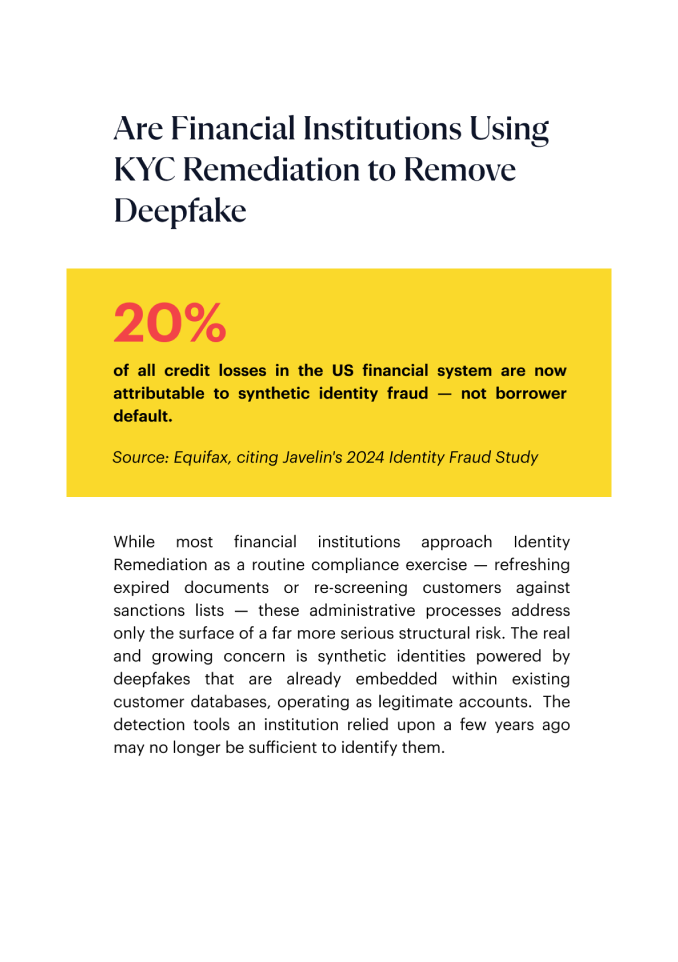

This is no longer a fringe problem. Synthetic identity fraud now accounts for 20% of credit losses in the U.S. financial system. In Javelin's 2024 Identity Fraud Study, 73% of financial institutions reported it rising, and US lender exposure reached a record $3.3 billion.

And the problem isn't only at the front door anymore. It's already inside the building.

20%

of credit losses in the U.S. financial system are now attributable to synthetic identity fraud. They are recorded not as fraud, but as ordinary default.

Equifax, citing Javelin's 2024 Identity Fraud Study

02 Misclassification

A default you can recover from. A ghost borrower you cannot.

Real borrower · unable to repay

There is someone to find

A genuine, verified individual who can't meet repayment obligations. There's a person to contact, a record to trace, assets to pursue. Collections and recovery proceedings are viable.

Partial recovery is possible.

A borrower who never existed

There is no one to find

A fabricated profile built on AI-generated or deepfaked credentials. No individual to pursue. No asset to trace. No one to locate. There was never anyone there.

Total, permanent, and usually misclassified as an ordinary default.

That misclassification compounds quietly. When ghost borrowers are counted as defaulters, provisioning models distort, risk ratings lose accuracy, and recovery teams spend months chasing people who were never real.

It also masks intent. Synthetic profiles are often nurtured deliberately, built up with credit history and believable behaviour over months or years, before a calculated "bust-out" maxes every line at once and disappears. Filed as a default, it looks like bad luck. It was a plan.

02 The Blind Spot

Why the risk is hiding in your historic database

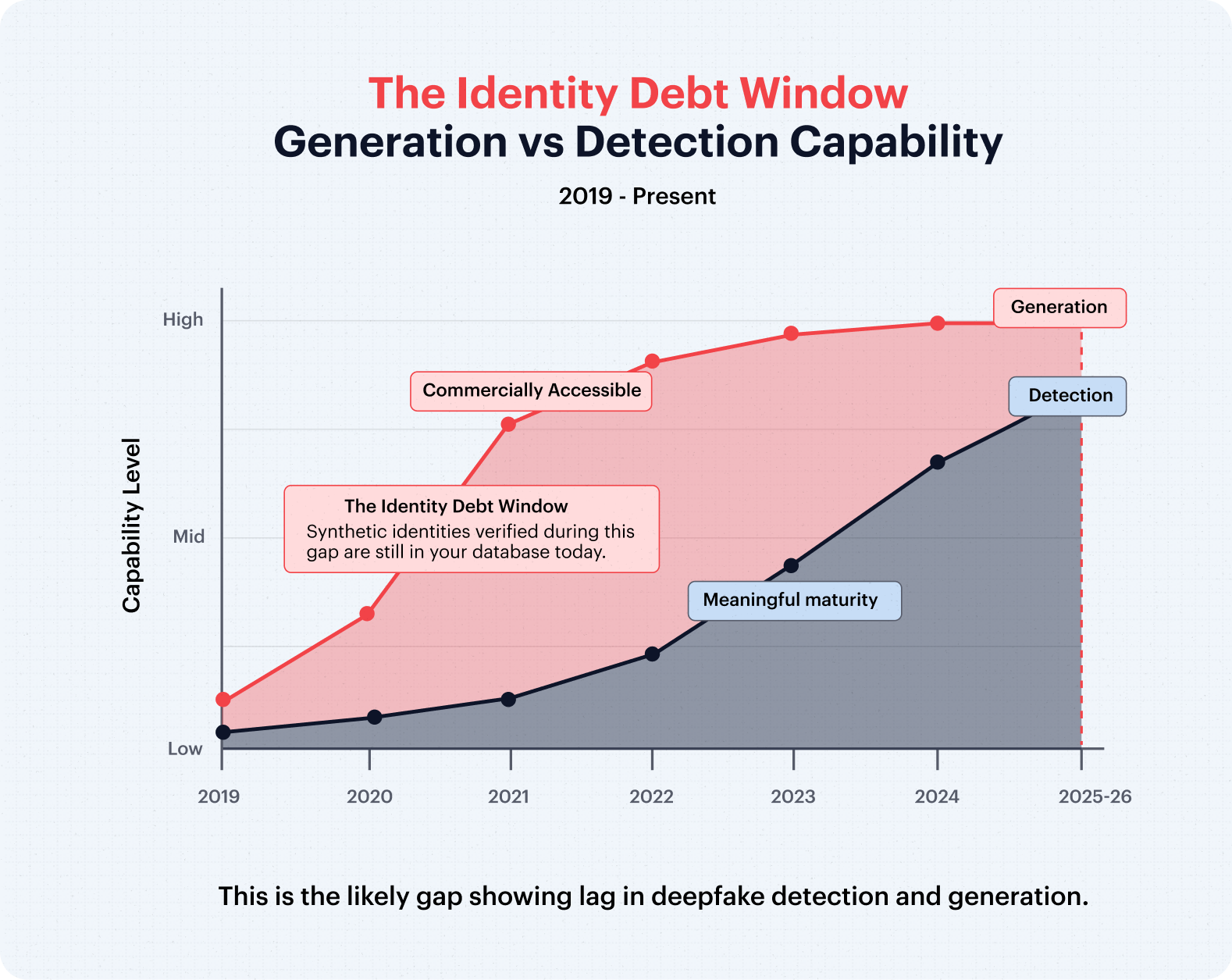

Most identity systems are being upgraded to catch deepfakes at onboarding. That's necessary work, but onboarding has never been airtight. By one estimate, 95% of synthetic identities go undetected at the onboarding stage. And the upgrades leave the harder question unanswered: what about the accounts verified before today's controls existed?

There was a window, still open for many institutions, when deepfake generation had already outpaced detection. Synthetic identities sophisticated enough to defeat live verification became viable well before detection tools could reliably catch them. Every account onboarded in that window passed verification against controls that, in hindsight, could not see what they were up against.

Those identities did not get caught later. They settled in. They are in your portfolio today, operating as legitimate accounts. Together they form a body of identity debt that routine KYC remediation is structurally not designed to find.

95%

of synthetic identities are estimated to go undetected during the onboarding process. That is exactly how they end up in your historic database.

Themis, 2025 Fraud Trends

Definition

Identity debt is the accumulated, unmeasured exposure created by synthetic and deepfake-powered identities that passed verification in the past and remain active in an institution's portfolio. Unlike a known default, identity debt is invisible on the balance sheet until it converts into credit loss, regulatory scrutiny, or reputational damage.

02 The Core Challenge

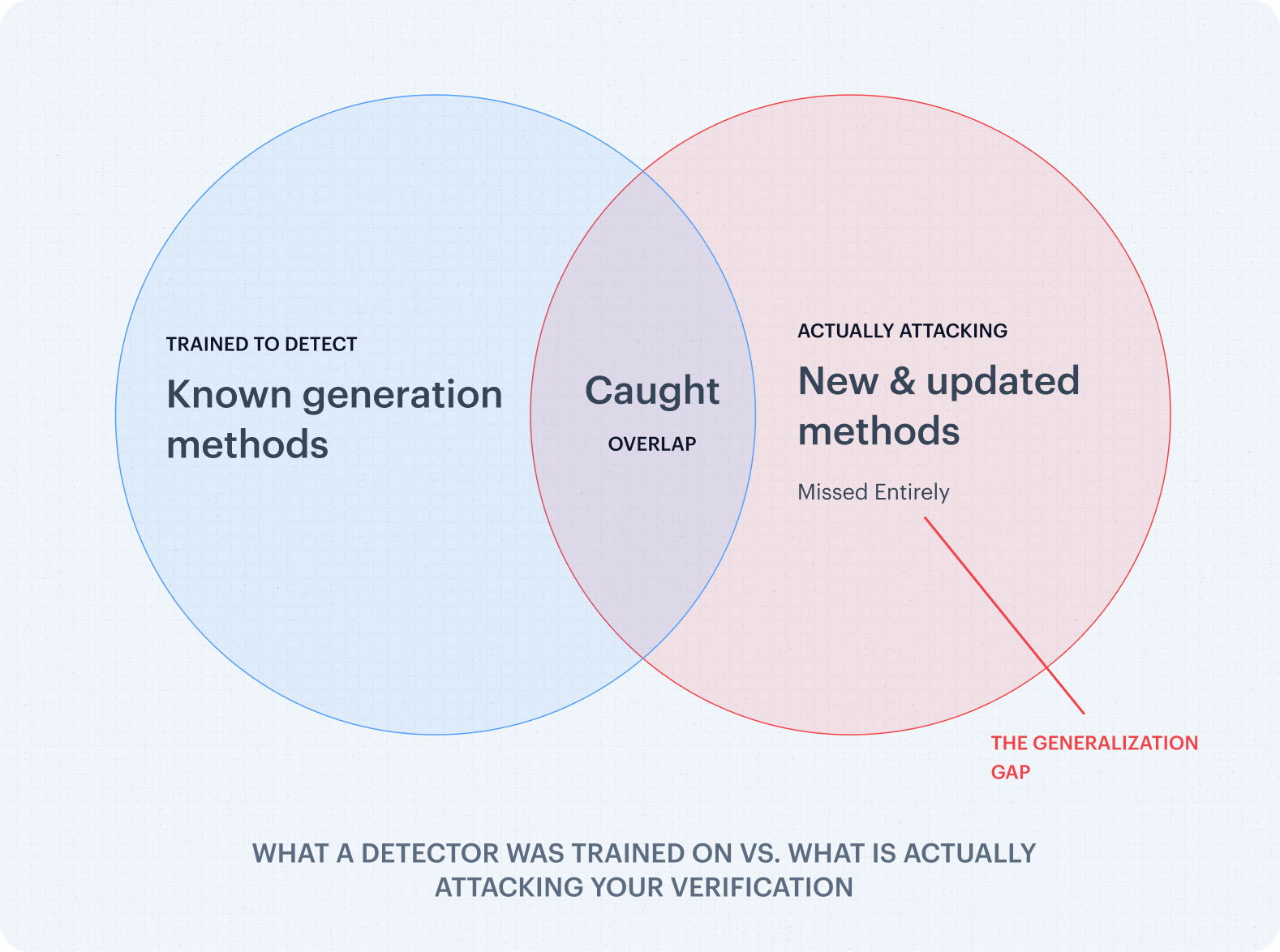

The Generalization Gap: why detection that worked then fails now

Definition

The Generalization Gap is the tendency of a deepfake detector to fail against generation methods it was never trained on. Detectors learn the digital artefacts left by known AI tools. When a new or updated model produces unfamiliar artefacts, the detector can still score well on familiar fakes while missing novel ones entirely.

This is not a marginal edge case. It is a structural limit on how detection works, and it has two consequences for financial institutions.

The first explains the historic risk. Detection models in use when many of your accounts were onboarded were trained against a narrower range of known threats. Actors using newer generation methods produced deepfakes that fell outside what those models had ever learned. Those identities passed verification not because any single control was weak in isolation, but because the controls were structurally incapable of recognising what they had never been trained to see.

The second consequence is that the problem is ongoing. A detector that is not continuously retrained against the newest generation methods is already partially obsolete, and any synthetic identity created with those newer methods can pass it today.

The research points the same way. Europol's Innovation Lab, in its report Facing Reality? Law Enforcement and the Challenge of Deepfakes, has noted that detection trained on known deepfakes offers limited assurance against fakes produced by unknown or updated models. A 2025 systematic analysis in the Journal of Sensor and Actuator Networks (Alawadhi et al.) reached a similar conclusion: keeping pace depends on detection methods that are robust and continuously adaptable. And the World Economic Forum's January 2026 report, Unmasking Cybercrime: Strengthening Digital Identity Verification against Deepfakes, tested commercial verification tools against real-world attack tools and concluded that identity systems must continuously adapt to remain resilient.

02 Why Routine Remediation Misses It

KYC remediation refreshes documents. It never asks if the identity was real.

Most KYC remediation programs do important but narrow work: refreshing expired ID documents, updating addresses, re-screening customers against sanctions lists, re-rating risk. Those are surface-level updates to a customer record, and they assume the identity behind that record was genuine to begin with.

The global standard actually supports going further. The FATF Interpretive Note to Recommendation 10 requires institutions to keep the data collected during customer due diligence up to date and relevant by reviewing existing records, particularly for higher-risk customers.

The same remediation framework, equipped with current detection, can forensically re-examine whether the identities verified in the past were genuine at the time they were verified.

From routine compliance to active risk reduction

That obligation was written for ongoing monitoring. But applied with current detection, it does something far more consequential: it lets you satisfy a regulatory requirement and remove synthetic profiles from your portfolio in the same pass.

The second exposure: AML

The risk is not credit loss alone. A synthetic profile that has already passed KYC is a clean channel for layering illicit funds. It carries a verified identity, an established transaction history, and no flags. If regulators later determine that synthetic accounts in your portfolio were used to move illicit funds, the exposure extends well beyond the write-off into enforcement action, mandatory remediation, and reputational damage.

The Solution

The Shufti Blind Spot Audit

Shufti's Blind Spot Audit is a forensic framework built for exactly this remediation. It deploys as an Amazon Machine Image inside your own AWS environment, which means no personally identifiable information ever leaves your infrastructure. That single design decision removes the data-residency and privacy barrier that causes most institutions to defer forensic audits indefinitely.

Shufti's detection engines are continuously updated against new and emerging generation techniques, directly addressing the Generalization Gap. So the audit is not limited to surfacing what static tools missed years ago. It is built to catch what static detection deployed today would still miss.

That detection is independently validated. Shufti holds iBeta Level 1 and Level 2 presentation-attack-detection conformance and, in 2026, became the first European company to achieve iBeta Level 3 conformance, tested to the ISO/IEC 30107-3 standard across iOS and Android for passive liveness, with 0% error rates.

Runs in your AWS

Deploys entirely within your environment as an Amazon Machine Image. No PII leaves your infrastructure. No external data transfer.

Risk-based targeting

Focuses on high-value accounts and high-exposure onboarding windows. No need to reprocess your entire database.

Parallel detection engines

Multiple specialised engines for document, face, and manipulation analysis run across the selected cohort at once.

Findings you can act on

Actionable results delivered inside your own environment, ready for immediate remediation.

Available on AWS Marketplace, with no procurement commitment and no vendor access to your data.

Frequently Asked Questions

What is the deepfake detection gap?

The deepfake detection gap is the interval between when deepfake generation became sophisticated enough to defeat identity verification and when detection technology matured enough to reliably catch it. Synthetic identities verified during that gap passed KYC checks legitimately and remain active in institutional portfolios today.

What is synthetic identity fraud?

Synthetic identity fraud uses a fabricated identity, often built from a mix of real and AI-generated or deepfaked credentials, to pass verification and open genuine financial accounts. Because no real person sits behind the profile, losses from synthetic identities are typically total and unrecoverable.

Why can't routine KYC remediation catch synthetic identities?

Routine KYC remediation refreshes a customer record: expired documents, addresses, sanctions screening, and risk ratings. It assumes the underlying identity was genuine at onboarding. It is not designed to forensically re-examine whether that identity was ever real.

What is the Generalization Gap in deepfake detection?

The Generalization Gap is the tendency of a deepfake detector to fail against generation methods it was never trained on. Detectors learn artefacts from known AI tools, so newer or updated generation models can produce fakes the detector misses entirely, even while it still performs well on familiar ones.

How do you find synthetic identities already in a customer database?

By running a forensic audit: applying current, continuously updated deepfake and document-manipulation detection to historic verification records, prioritised by risk. This re-examines whether past identities were genuine at the time of verification, something the original onboarding process could not assess.

Does a forensic identity audit require sending customer data to a vendor?

It should not. Shufti's Blind Spot Audit deploys as an Amazon Machine Image inside your own AWS environment, so no personally identifiable information leaves your infrastructure. That removes the main data-residency and privacy barrier to forensic audits.

Do we have to re-verify our entire customer base?

No. A risk-based audit targets high-value accounts and high-exposure onboarding windows first, rather than reprocessing every record, which makes the audit faster and far less operationally disruptive.

Take the next step

Find out how many of your verified customers never existed

Every reporting period that synthetic identities go undetected is a period in which ghost borrowers keep maturing toward bust-out, illicit funds keep moving through clean-looking accounts, and regulatory exposure keeps accumulating without visibility. The Blind Spot Audit requires no procurement commitment, no PII transfer, and no disruption to current operations.