Face Verification

Face Verification

Address Verification

Address Verification

Document Verification

Document Verification

Age Verification

Age Verification

VideoIdent

VideoIdent

Fast ID

Fast ID

Docless Verification

Docless Verification

Consent Verification

Consent Verification

NFC Verification

NFC Verification

Business Verification

Business Verification

Due Diligence

Due Diligence

Investor Verification

Investor Verification

E-Signature

E-Signature

QES

QES

AML Screening

AML Screening

Transaction Monitoring

Transaction Monitoring

Adverse Media

Adverse Media

Business AML Screening

Business AML Screening

PEP & RCA

PEP & RCA

Sanctions

Sanctions

Watchlist

Watchlist

Behavioural Biometrics

Behavioural Biometrics

Device Fingerprinting

Device Fingerprinting

Biometric Face Authentication

Biometric Face Authentication

MFA

MFA

Fraud Hub

Fraud Hub

Onboarding

Onboarding

Ongoing Monitoring

Ongoing Monitoring

KYC

KYC

KYB

KYB

KYI

KYI

Age Assurance

Age Assurance

Identity Verification

Identity Verification

Workforce IAM

Workforce IAM

Candidate Verification

Candidate Verification

Compliance

Compliance

Fraud prevention

Fraud prevention

Trust & safety

Trust & safety

Global expansion

Global expansion

Product Managers

Product Managers

Compliance Officers

Compliance Officers

Fraud Analysts

Fraud Analysts

Developers

Developers

Deepfake Detection

Deepfake Detection

Bonus Abuse / Promotion Abuse

Bonus Abuse / Promotion Abuse

Account Takeover

Account Takeover

Synthetic Identity Fraud

Synthetic Identity Fraud

Document Fraud

Document Fraud

Impersonation Fraud

Impersonation Fraud

Multi-Accounting

Multi-Accounting

Fraud Networks

Fraud Networks

Chargeback Fraud

Chargeback Fraud

Money Mule Activity

Money Mule Activity

Party Fraud

Party Fraud

Regulatory & Compliance Risks

Regulatory & Compliance Risks

Fintech

Fintech

Crypto

Crypto

iGaming

iGaming

Forex

Forex

Social Network

Social Network

Marketplace

Marketplace

Banking

Banking

Gig Economy

Gig Economy

Payments

Payments

Ride Hailing

Ride Hailing

Adult Content

Adult Content

Blind Spot Audit

Blind Spot Audit

Deepfake Detector

Deepfake Detector

Liveness Spoofs

Liveness Spoofs

Document Originality

Document Originality

Document Deepfake

Document Deepfake

Global Trust Platform

Global Trust Platform

Journey Builder

Journey Builder

Case Management

Case Management

Shufti AI

Shufti AI

Fraud Analytics

Fraud Analytics

Vendor Comparison

Vendor Comparison

Brand Personalisation

Brand Personalisation

AI Compliance Co-Pilot

AI Compliance Co-Pilot

OCR

OCR

Secure Capture

Secure Capture

Deployment Options

Deployment Options

Identity Methods

Identity Methods

API Documentation

API Documentation

Mobile SDKs

Mobile SDKs

Service Status

Service Status

Help Center

Help Center

Contact Us

Contact Us

Technical Support

Technical Support

Supported Documents

Supported Documents

Supported Countries

Supported Countries

Content library

Content library

Blogs

Blogs

News

News

Reports

Reports

Insights

Insights

Knowledgebase

Knowledgebase

ROI calculator

ROI calculator

About

About

Career

Career

Press Release

Press Release

Certifications

Certifications

Partnership

Partnership

Awards

Awards

Events & Webinar

Events & Webinar

Interactive Demo

Interactive Demo

Podcast Studio

Podcast Studio

Spotlight Studio

Spotlight Studio

- Australia

- Austria

- Bangladesh

- Brazil

- Bulgaria

- Canada

- China

- Cyprus

- Egypt

- Estonia

- Eswatini

- Ethiopia

- France

- Germany

- Greece

- Haiti

- Hong Kong

- India

- Iraq

- Ireland

- Indonesia

- Italy

- Japan

- Jordan

- Kazakhstan

- Kenya

- Kosovo

- Kuwait

- Latvia

- Luxembourg

- Malaysia

- Malta

- Mauritius

- Mexico

- Micronesia

- Moldova

- Montenegro

- Morocco

- Mozambique

- Myanmar

- Namibia

- Nauru

- Nepal

- Nigeria

- Nicaragua

- Niue

- Norway

- Netherlands

- New Zealand

- Oman

- Pakistan

- Palau

- Palestine

- Panama

- Papua New Guinea

- Paraguay

- Peru

- Puerto Rico

- Philippines

- Portugal

- Portugal

- Qatar

- Republic of Congo

- Romania

- Russia

- Rwanda

- Samoa

- San Marino

- Senegal

- Serbia

- Seychelles

- Sierra Leone

- Singapore

- Slovakia

- Slovenia

- Somalia

- South Africa

- South Korea

- South Sudan

- Sri Lanka

- St Kitts and Nevis

- St Maarten

- St Lucia

- Sweden

- Switzerland `

- Syria

- Taiwan

- Tajikistan

- Tanzania

- Thailand

- Timor Leste

- Togo

- Tonga

- Trinidad and Tobago

- Turkey

- Turks and Caicos

- Turkmenistan

- Tunisia

- Tuvalu

- Uganda

- Ukraine

- UK

- Uruguay

- USA

- Uzbekistan

- Vatican City

- Vietnam

- Venezuela

- Vanuatu

Mauritius

Identity Verification & KYC For Mauritius

Shufti delivers identity verification Mauritius and AML screening for regulated entities. Mauritius KYC provider solutions support FSC and FIAMLA with audit-ready evidence.

Operational performance for Mauritius KYC

Our Numbers Speak Volumes

92.77%

Pass Rates

< 5 sec

Verification

Time

5

supported Mauritian

document types

Evidence-Ready Checks Across People & Businesses in Mauritius

Individual Documents We Verify

Shufti supports 5 Mauritian document types for KYC Mauritius compliance.

View All Supported DocumentsNational Identity Card

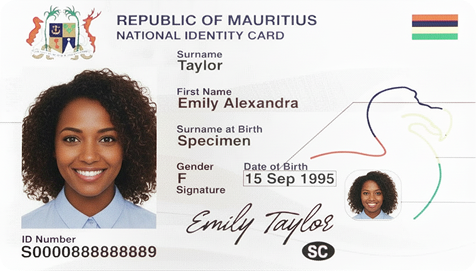

Government-issued photo identity card used as primary proof of identity for adults in Mauritius. Includes holder's name, date of birth, identification number, and photograph. Most commonly submitted document for individual KYC onboarding across financial services.

Passport

Official travel document issued by the Mauritian government, containing machine-readable zones (MRZ) for automated field extraction. Useful for non-face-to-face verification and cross-border transactions. Supports both standard and diplomatic passports issued by Mauritius.

Driver's Licence

Driving licence issued by the Traffic Branch of Mauritius Police Force. Contains holder's photograph, name, residential address, and licence category. Accepted as supplementary identity document and proof of address for KYC compliance and ongoing verification.

Business Entity Identity

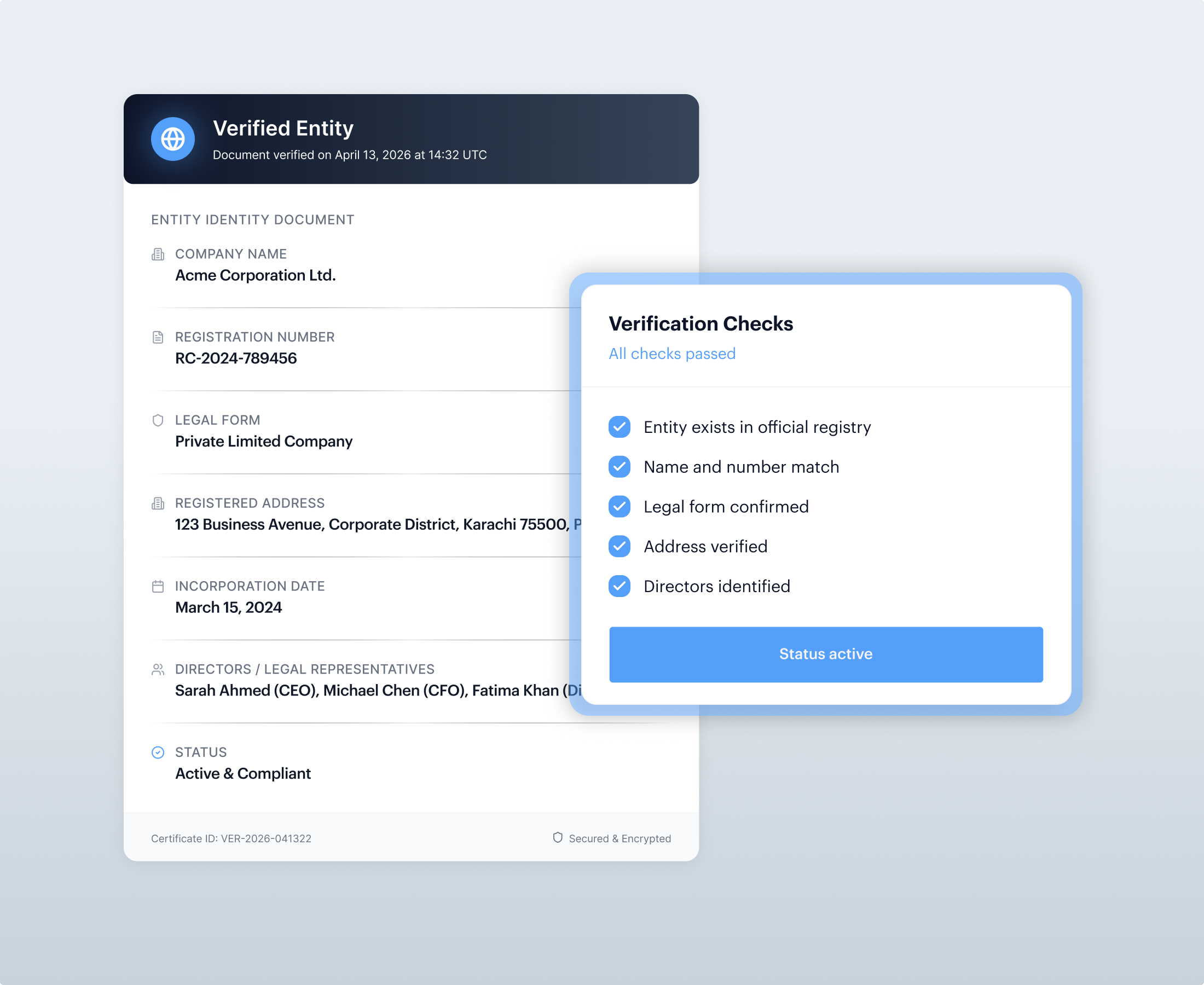

Certificate of Incorporation

Electronic record issued by Registrar confirming legal entity status, business registration number and incorporation date, required as primary evidence for corporate KYC baseline.

Business Registration Card

Official card issued by CBRD with Business Registration Number (BRN) confirming operational status and legitimacy for entity-level verification and ongoing compliance monitoring.

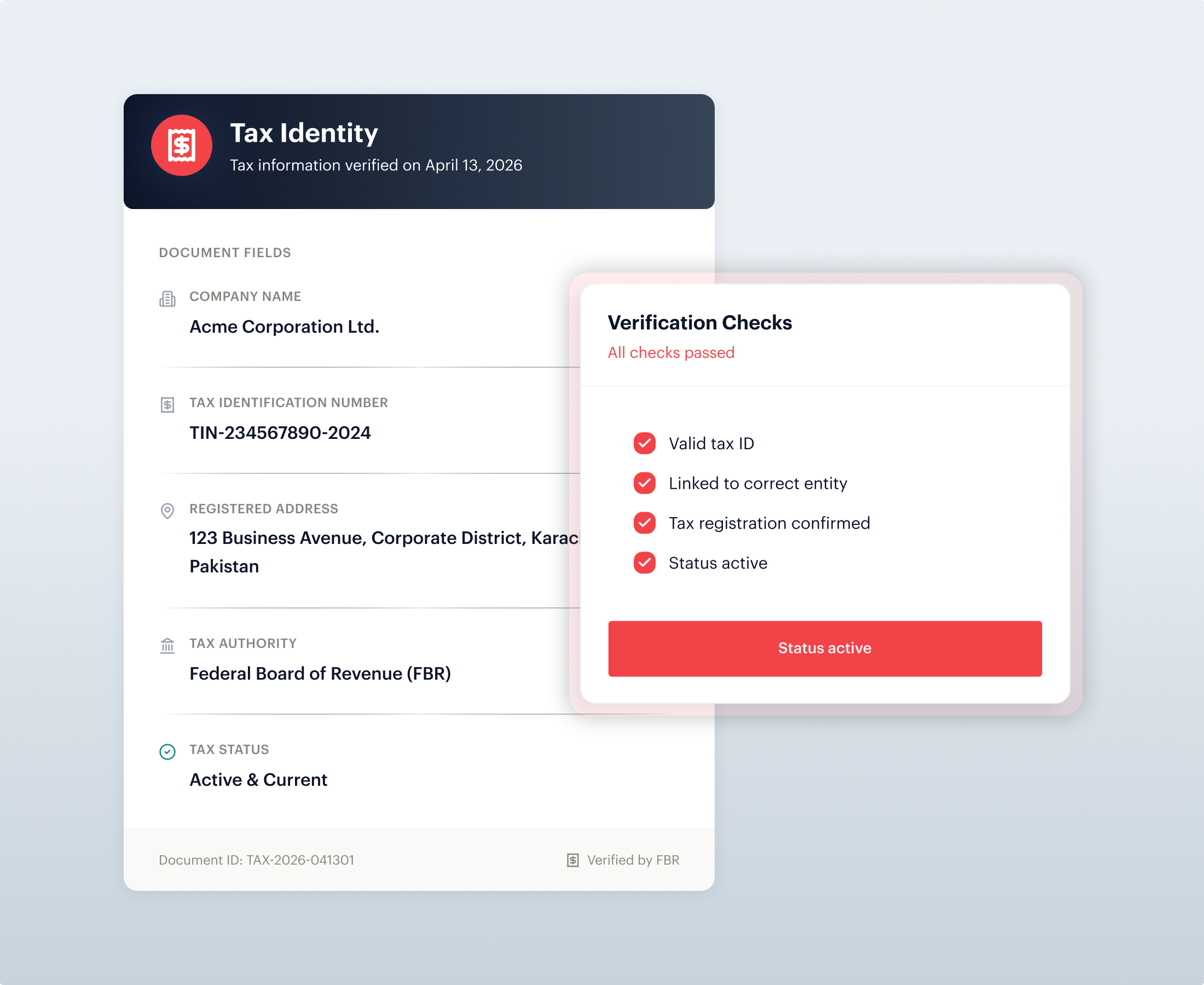

Business Tax Identity

Tax Account Number (TAN)

Official Tax Identification Number issued by Mauritius Revenue Authority (MRA); unique numeric identifier for all entities required for tax compliance and financial institution verification workflows.

VAT Registration Number

Separate identification for VAT-registered entities; demonstrates tax compliance status and revenue registration with MRA; collected for cross-validation during beneficial owner and entity verification.

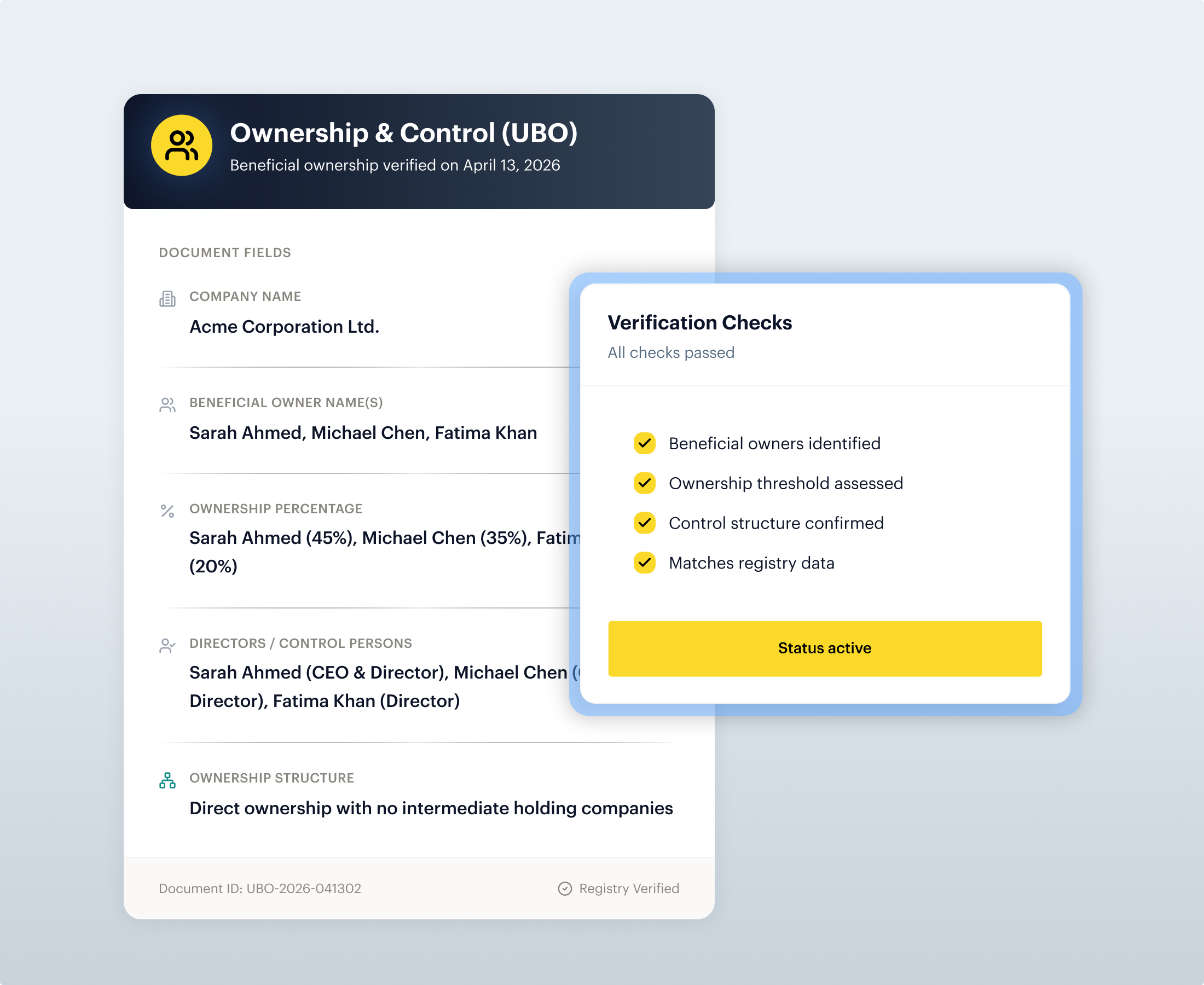

Ownership & Control (UBO)

Beneficial Ownership Register

Central register held by Registrar containing beneficial owner name, residential address and identity document details; legal foundation for UBO disclosure and 7-year retention obligations under Mauritius law.

Share Register

Company document disclosing ownership stakes and ultimate beneficial owners (threshold: 20% or more of voting rights); legal requirement under Companies Act with 7-year retention and Form 23 filing obligations.

Languages We Cover

Bilingual Document Handling

Mauritius government documents appear in English and French; Shufti's OCR and field extraction tolerate both script variants. Name matching controls account for French/English spelling variants and Latin transliteration inconsistencies common in official documents.

French And English Name Matching

Names in official documents may appear in French, English or mixed script. Shufti applies transliteration-aware rules and keeps extracted fields visible for audit and QA to reduce false mismatches where same person appears under variant spellings.

Evidence Consistency Controls

Shufti preserves extracted document data alongside matched customer records. Visibility of "what was extracted" versus "what was matched" supports audit trails, regulatory review and dispute resolution under FIAMLA recordkeeping and Data Protection Act 2017 requirements.

GOVERNANCE & CONTROLS

Audit-Ready Decisions, Lower Operational Drag

Fewer Re-Submissions

Quality gates reduce failed uploads and retries, improving completion rates and lowering verification costs.

Cleaner Audit Trails

Consistent outputs and evidence retention meet FSC and BoM audit requirements under FIAMLA regulations.

Better Name Matching

Transliteration-aware matching reduces false rejections on bilingual documents for faster verification.

One Workflow, One Back Office

Identity verification, KYB and screening in one view eliminates tool-switching and fragmentation.

National ID-First Flow Design

Prioritised National ID verification with quality gates ensures consistent handling of Mauritius document formats.

Mauritius IDV/KYC Challenges

Document Fraud Risk

Advanced forgery, altered MRZ data, and synthetic identity techniques pose verification challenges. Real-time liveness and facial biometrics required to block impersonation, CNIC misuse and high-risk account takeovers in digital onboarding.

Offshore Sector Complexity

Global Business Company structures, cross-border beneficial owner chains and nominee arrangements complicate UBO identification. Complex corporate hierarchies require enhanced verification and 7-year record retention under FIAMLA and Companies Act.

Address Proof Inconsistencies

National ID and passport "permanent" addresses may differ from current residence. Informal housing, shared utilities and addresses not matching customer records cause frequent proof-of-address failures during onboarding and ongoing monitoring cycles.

Approval Process Delays

Account opening for Global Business Companies faces documented delays and compliance approval hurdles. Friction in international client onboarding increases operational burden and delays account activation.

Shufti's IDV/KYC Solutions for Mauritius

KYC Solutions

Face Verification

Stops identity fraud and mule sign-ups through liveness detection and facial biometrics matching selfie to document. Addresses Mauritius-specific risks including CNIC photo theft and impersonation in remote onboarding, reducing manual exceptions and re-verification cycles.

.

Age Verification

Estimates age from selfie-based analysis, then falls back to National ID or passport document verification when required. Blocks underage access whilst preserving onboarding speed for compliant Mauritius financial institutions and fintech platforms.

.

Address Verification

Online identity verification Mauritius through address documents issued in-country. Shufti supports utility bills from CEB (Central Electricity Board), CWA (Central Water Authority) and Mauritius Telecom, plus bank statements from MCB, SBM and AfrAsia Bank for full address confirmation.

.

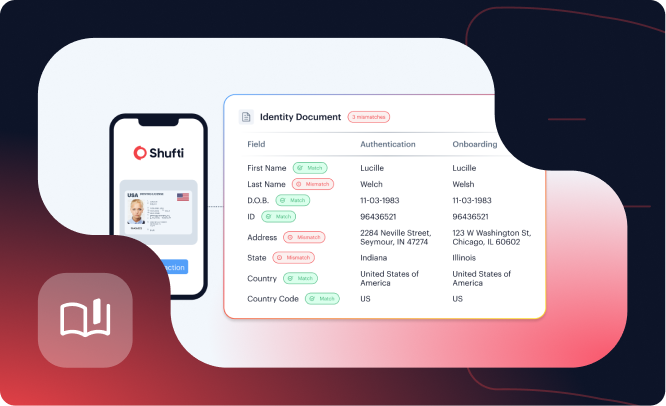

Document Verification

Detects tampered National ID, passport and driver's licence; extracts fields reliably across French and English variants. Reduces manual exceptions caused by poor captures and bilingual field inconsistencies, cutting re-submissions and fraud from corrupted document images.

.KYB Solutions

Business Verification

Identity verification Mauritius for businesses, directors and beneficial owners reduces shell-company onboarding risk. Checks entity registration via CBRD, validates Tax Account Numbers (TAN) and screens controllers against sanctions lists.

.

Enhanced Due Diligence (EDD)

Applies stricter verification for high-risk clients including PEPs, non-face-to-face relationships and entities previously rejected by other banks. Mandatory under FSC guidelines for complex ownership structures and Global Business Company clients requiring UBO documentation.

.AML Screening

Business AML Screening

Screens Mauritian entities and owners against UN Consolidated Sanctions List, EU sanctions, OFAC designations and National Sanctions Secretariat lists. Captures screening rationale and hit outcomes for goAML reporting to Financial Intelligence Unit (FIU) and audit compliance.

.

Transaction Screening

Monitors ongoing flows for structuring, mule activity and high-risk counterparties using threshold-based and pattern-based rules. Supports continuous AML controls under FIAMLA requirements with defensible logs and transaction monitoring records for regulatory review.

.Built to Fit Mauritius's Compliance Landscape

Financial Services Commission (FSC)

Integrated regulator for non-banking financial services, securities, investment funds and global business entities in Mauritius. Mandated to license, supervise and ensure AML/CFT compliance; Shufti supports FSC-aligned onboarding controls through structured KYC evidence and audit-ready decision trails. Official Website: https://www.fscmauritius.org/en

Bank of Mauritius (BoM)

Central bank responsible for monetary stability, financial system soundness and supervision of commercial banking institutions. Enforces AML/CFT compliance through banking guidelines and ongoing supervisory examination; Shufti preserves screening results and KYC evidence for BoM audit requirements. Official Website: https://www.bom.mu/

Financial Intelligence Unit (FIU)

Central agency receiving, analysing and disseminating financial intelligence on suspected money laundering and terrorist financing via goAML platform. Shufti strengthens FIU-readiness by preserving investigation-grade evidence packs supporting STR/CTR case preparation and reporting compliance. Official Website: https://www.fiumauritius.org/fiu/

Financial Crimes Commission (FCC)

Statutory authority established March 2024 consolidating anti-corruption, financial crime investigation and asset recovery functions. Conducts investigation and prosecution of money laundering, fraud and corruption; Shufti supports evidence preservation and compliance documentation for FCC referrals. Official Website: https://fcc.mu/

Data Protection Office (DPO)

Independent authority enforcing the Data Protection Act 2017, responsible for regulating personal data processing and issuing compliance certificates. Shufti ensures data handling aligns with DPA 2017 requirements through encryption, retention controls and access governance aligned to regulatory guidance. Official Website: https://dataprotection.govmu.org/SitePages/Index.aspx

Corporate and Business Registration Department (CBRD)

Government agency responsible for company incorporation, business registration, beneficial ownership register maintenance and corporate administration. Shufti verifies business legitimacy via CBRD registration, TAN validation and beneficial owner identification aligned to CBRD guidance. Official Website: https://companies.govmu.org/Pages/default.aspx

Mauritius Revenue Authority (MRA)

Revenue authority responsible for tax assessment, collection and enforcement; issues Tax Account Numbers (TAN) and manages VAT registration. Shufti validates TAN and VAT registration as part of business verification, confirming entity tax compliance and legitimacy for financial institution onboarding. Official Website: https://www.mra.mu/

Deployment Choice

No major cloud providers operate data centre regions physically in Mauritius. Regulated entities requiring in-country data residency must deploy on-premise or use Mauritius-based private cloud. Shufti supports private deployment options meeting FIAMLA localisation expectations for financial institutions.

Regulatory Alignment

Data Protection Act 2017 (Act No. 20 of 2017) is the primary personal data protection framework; enforced by Data Protection Office (DPO) issuing 3-year compliance certificates. FIAMLA requires 7-year AML financial record retention; DPA 2017 specifies retention periods determined by processing purpose and regulatory requirements.

Retention Controls

AML and financial records must be retained for minimum 7 years under FIAMLA 2002 and supporting regulations. Beneficial owner information must be retained for 7 years in share registers and company records. Shufti provides configurable retention and purge behaviour aligned to programme policy and audit obligations.

Encryption Posture

Mauritius does not specify general encryption standards in primary data protection or AML legislation. BFSI sector follows international best practice including TLS 1.2+ and AES-256 for sensitive data. FSC and BoM conduct supervisory review of encryption controls as part of ongoing compliance examination.

Data and Privacy Controls in Mauritius

Mauritius AML Sources That Strengthen Decision

National Assembly of Mauritius

Corporate and Business Registration Department

Mauritius Financial Services Commission

Mauritius Times

L'Express

The Mauritius Broadcasting Corporation

Frequently Asked Questions

What is KYC and why is it required in Mauritius?

KYC (Know Your Customer) is the process by which financial institutions verify the identity of customers before establishing business relationships in Mauritius. Under FSC and FIAMLA requirements, every bank, investment fund, fintech and financial institution must conduct KYC to combat money laundering, terrorist financing and fraud. Mauritius is rated Compliant by FATF for AML/CFT standards, making strict KYC implementation a core regulatory obligation.

What documents are required for KYC identity verification in Mauritius?

For individuals, KYC in Mauritius requires a valid government-issued identity document (National Identity Card, passport or driver's licence) with current permanent address details and recent photograph. For companies, documentation must include Certificate of Incorporation, beneficial owner declarations, director registrations, audited accounts and UBO identification forms. All documents must match existing ownership records and may require notarisation for foreign entities under FSC KYC regulations.

What is eKYC and how does online identity verification work in Mauritius?

eKYC (electronic Know Your Customer) is a digital identity verification process allowing financial institutions in Mauritius to complete customer onboarding in minutes rather than days. Using facial recognition, optical character recognition (OCR) and liveness detection, eKYC solutions verify government-issued identity documents in real-time. This method is legally compliant with FSC regulations and the Data Protection Act 2017, providing faster account opening and reduced fraud risk for banks, fintechs and investment funds.

Who is responsible for AML compliance and KYC oversight in Mauritius?

The Financial Services Commission (FSC) regulates non-banking financial institutions, investment funds and global business entities; the Bank of Mauritius (BoM) oversees commercial banks; the Financial Intelligence Unit (FIU) receives and analyses suspicious activity reports. The Financial Crimes Commission (established March 2024) conducts investigations into money laundering and financial crimes. All entities fall under FIAMLA and must report suspicious transactions to the FIU via the goAML system.

What is beneficial owner verification and when is it required in Mauritius?

Beneficial owner (UBO – Ultimate Beneficial Owner) verification is mandatory when a natural person owns 20% or more of a company's capital or voting rights. Under Mauritius KYC regulations, financial institutions must identify and verify beneficial owners to the same standard as customers. Information required includes full name, residential address, passport/NIC number and ownership percentage. This applies to corporate accounts, Global Business Companies and fund administration entities. UBO records must be retained for 7 years.

What is enhanced due diligence (EDD) and when must it be applied in Mauritius KYC?

Enhanced Due Diligence (EDD) is a stricter verification process required when conducting KYC for high-risk clients in Mauritius. EDD is mandatory for non-face-to-face business relationships, Politically Exposed Persons (PEPs), clients previously rejected by other banks and customers in high-risk jurisdictions. EDD steps include enhanced identity verification, source of funds/wealth documentation, ongoing transaction monitoring and more frequent compliance reviews. FSC guidelines require appropriate EDD measures proportionate to the client's risk profile and business model.

What are the sanctions screening and PEP identification requirements in Mauritius AML?

Financial institutions in Mauritius must screen all customers and transactions against the UN Consolidated Sanctions List, EU sanctions lists, OFAC designations and the National Sanctions Secretariat (NSSEC) list. Screening is required at account opening and periodically thereafter (frequency depends on business model and transaction volume). Politically Exposed Persons (PEPs) require identification and enhanced due diligence including source of wealth verification and ongoing monitoring. Licensees may use automated screening software or manual screening via publicly available lists.

How do KYC and AML compliance requirements differ for crypto and fintech in Mauritius?

Crypto and Virtual Asset Service Providers (VASPs) in Mauritius are regulated under the Virtual Asset and Initial Token Offering Services (VAITOS) Act 2021 and must comply with full AML/CFT and KYC requirements. VASPs must conduct Customer Due Diligence, verify beneficial owners, implement transaction monitoring and screen against sanctions lists before on-boarding customers. Recent updates (effective March 2025) require implementation of the Travel Rule for VASP-to-VASP transfers and participation in international data-sharing frameworks such as IVMS 101 for enhanced compliance.

Build a Mauritius-ready KYC, KYB & AML programme with Shufti

INDEPENDENTLY AUDITED. GLOBALLY CERTIFIED.

Certified to Global Standards

PROVEN WORKFLOWS

Use Cases for Regulated Growth in Mauritius

Reduce Fraud Without Blocking Growth

Shufti supports marketplace integrity by verifying seller and buyer identities, enabling age-gated journeys where needed, and preserving evidence to support investigations, disputes, and risk-led enforcement actions.

Secure Trust at Every Transaction

Automate KYC and AML workflows to reduce manual onboarding costs. Strengthen residency checks while delivering the frictionless digital experience modern customers expect.

Scale Your Exchange with Confidence

Balance anonymity with compliance. Instantly verify user jurisdiction to meet Travel Rule obligations and help stop abuse without slowing down legitimate trading volume.

Accelerate Growth, Eliminate Friction

Onboard users in seconds, not days. Deploy tiered address verification flows that maximise completion rates for genuine users while filtering out synthetic fraud.

Onboard Global Traders in Real-Time

Verify investors across 250+ countries & territories. Ensure compliance with international financial regulations while preventing identity theft and high-risk chargebacks.

Power a Fair & Secure Player Experience

Reduce bonus abuse and multi-accounting rings at the door. Enforce location rules and trigger step-up checks without disrupting the player journey.

Build a Trusted, Verified Workforce

Screen freelancers and drivers at scale. Verify residency and reduce onboarding friction while maintaining trust between users.

Let’s Tailor your journey

Just a few quick questions to guide your Shufti experience.

Shufti

Market Positioning and Commercial Assessment

Industry stands at 1.7rating

Best ID Verification Innovator

TOP 10 KYC Solution Provider

Best Client Onboarding Solution

Samer Al Tamimi@CEO of Safwa Bank

We take our client's privacy very seriously and always look for new innovative solutions to ensure a safe banking experience. Working with Shufti feels like a breath of fresh air, as their 100% in-house tech keeps our customer's data free from vulnerabilities and fully safe and protected.

PROVEN PLAYBOOKS

Explore Practical KYC & AML Resources

16 August, 2025

5 minutes read

How Much of What You’ve Verified Is Actually Real?

Shufti’s Deepfake Blindspot Audit now runs fully inside your AWS environment, auditing historic KYC for manipulation signals without moving sensitive data off-prem.

whitepapers