Face Verification

Face Verification

Address Verification

Address Verification

Document Verification

Document Verification

Age Verification

Age Verification

VideoIdent

VideoIdent

Fast ID

Fast ID

Docless Verification

Docless Verification

Consent Verification

Consent Verification

NFC Verification

NFC Verification

Business Verification

Business Verification

Due Diligence

Due Diligence

Investor Verification

Investor Verification

E-Signature

E-Signature

QES

QES

AML Screening

AML Screening

Transaction Monitoring

Transaction Monitoring

Adverse Media

Adverse Media

Business AML Screening

Business AML Screening

PEP & RCA

PEP & RCA

Sanctions

Sanctions

Watchlist

Watchlist

Behavioural Biometrics

Behavioural Biometrics

Device Fingerprinting

Device Fingerprinting

Biometric Face Authentication

Biometric Face Authentication

MFA

MFA

Fraud Hub

Fraud Hub

Onboarding

Onboarding

Ongoing Monitoring

Ongoing Monitoring

KYC

KYC

KYB

KYB

KYI

KYI

Age Assurance

Age Assurance

Identity Verification

Identity Verification

Workforce IAM

Workforce IAM

Candidate Verification

Candidate Verification

Compliance

Compliance

Fraud prevention

Fraud prevention

Trust & safety

Trust & safety

Global expansion

Global expansion

Product Managers

Product Managers

Compliance Officers

Compliance Officers

Fraud Analysts

Fraud Analysts

Developers

Developers

Deepfake Detection

Deepfake Detection

Bonus Abuse / Promotion Abuse

Bonus Abuse / Promotion Abuse

Account Takeover

Account Takeover

Synthetic Identity Fraud

Synthetic Identity Fraud

Document Fraud

Document Fraud

Impersonation Fraud

Impersonation Fraud

Multi-Accounting

Multi-Accounting

Fraud Networks

Fraud Networks

Chargeback Fraud

Chargeback Fraud

Money Mule Activity

Money Mule Activity

Party Fraud

Party Fraud

Regulatory & Compliance Risks

Regulatory & Compliance Risks

Fintech

Fintech

Crypto

Crypto

iGaming

iGaming

Forex

Forex

Social Network

Social Network

Marketplace

Marketplace

Banking

Banking

Gig Economy

Gig Economy

Payments

Payments

Ride Hailing

Ride Hailing

Adult Content

Adult Content

Blind Spot Audit

Blind Spot Audit

Deepfake Detector

Deepfake Detector

Liveness Spoofs

Liveness Spoofs

Document Originality

Document Originality

Document Deepfake

Document Deepfake

Global Trust Platform

Global Trust Platform

Journey Builder

Journey Builder

Case Management

Case Management

Shufti AI

Shufti AI

Fraud Analytics

Fraud Analytics

Vendor Comparison

Vendor Comparison

Brand Personalisation

Brand Personalisation

AI Compliance Co-Pilot

AI Compliance Co-Pilot

OCR

OCR

Secure Capture

Secure Capture

Deployment Options

Deployment Options

Identity Methods

Identity Methods

API Documentation

API Documentation

Mobile SDKs

Mobile SDKs

Service Status

Service Status

Help Center

Help Center

Contact Us

Contact Us

Technical Support

Technical Support

Supported Documents

Supported Documents

Supported Countries

Supported Countries

Content library

Content library

Blogs

Blogs

News

News

Reports

Reports

Knowledgebase

Knowledgebase

ROI calculator

ROI calculator

About

About

Career

Career

Press Release

Press Release

Certifications

Certifications

Partnership

Partnership

Awards

Awards

Events & Webinar

Events & Webinar

Interactive Demo

Interactive Demo

Podcast Studio

Podcast Studio

- Australia

- Austria

- Bangladesh

- Brazil

- Bulgaria

- Canada

- China

- Cyprus

- Egypt

- Estonia

- Eswatini

- Ethiopia

- France

- Germany

- Greece

- Haiti

- Hong Kong

- India

- Iraq

- Ireland

- Indonesia

- Italy

- Japan

- Jordan

- Kazakhstan

- Kenya

- Kosovo

- Kuwait

- Latvia

- Luxembourg

- Malaysia

- Malta

- Mauritius

- Mexico

- Micronesia

- Moldova

- Montenegro

- Morocco

- Mozambique

- Myanmar

- Namibia

- Nauru

- Nepal

- Nigeria

- Nicaragua

- Niue

- Norway

- Netherlands

- New Zealand

- Oman

- Pakistan

- Palau

- Palestine

- Panama

- Papua New Guinea

- Paraguay

- Peru

- Puerto Rico

- Philippines

- Portugal

- Portugal

- Qatar

- Republic of Congo

- Romania

- Russia

- Rwanda

- Samoa

- San Marino

- Senegal

- Serbia

- Seychelles

- Sierra Leone

- Singapore

- Slovakia

- Slovenia

- Somalia

- South Africa

- South Korea

- South Sudan

- Sri Lanka

- St Kitts and Nevis

- St Maarten

- St Lucia

- Sweden

- Switzerland `

- Syria

- Taiwan

- Tajikistan

- Tanzania

- Thailand

- Timor Leste

- Togo

- Tonga

- Trinidad and Tobago

- Turkey

- Turks and Caicos

- Turkmenistan

- Tunisia

- Tuvalu

- Uganda

- Ukraine

- UK

- Uruguay

- USA

- Uzbekistan

- Vatican City

- Vietnam

- Venezuela

- Vanuatu

Uganda

Identity Verification & KYC For Uganda

Shufti supports Know Your Customer, Know Your Business and Anti-Money Laundering compliance aligned to Uganda's Bank of Uganda, FIA and Anti-Money Laundering Act 2013 framework.

Operational performance for Uganda KYC

Our Numbers Speak Volumes

<5 sec

Verification Time

98.33%

Pass Rates

90%

eIDV Coverage

Evidence-Ready Checks Across People & Businesses

Individual Documents We Verify

Shufti supports 3 Ugandan document types.

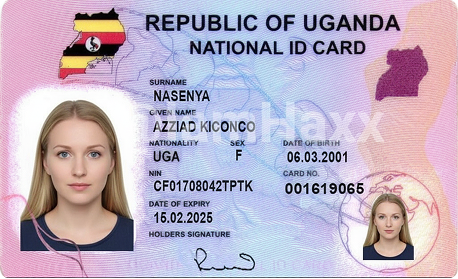

View All Supported DocumentsNational Identification Card

Biometric machine-readable card issued by NIRA to citizens aged 18+; contains fingerprint and facial recognition data; primary document for KYC verification.

Passport

Issued by the Directorate of Citizenship and Immigration Control, proof of citizenship and international travel is accepted for customer identity verification.

Driver's Licence

Issued by Uganda Driver Licensing System; mandatory for vehicle operation; contains name, address, date of birth and class; accepted fallback for KYC.

Business Entity Identity

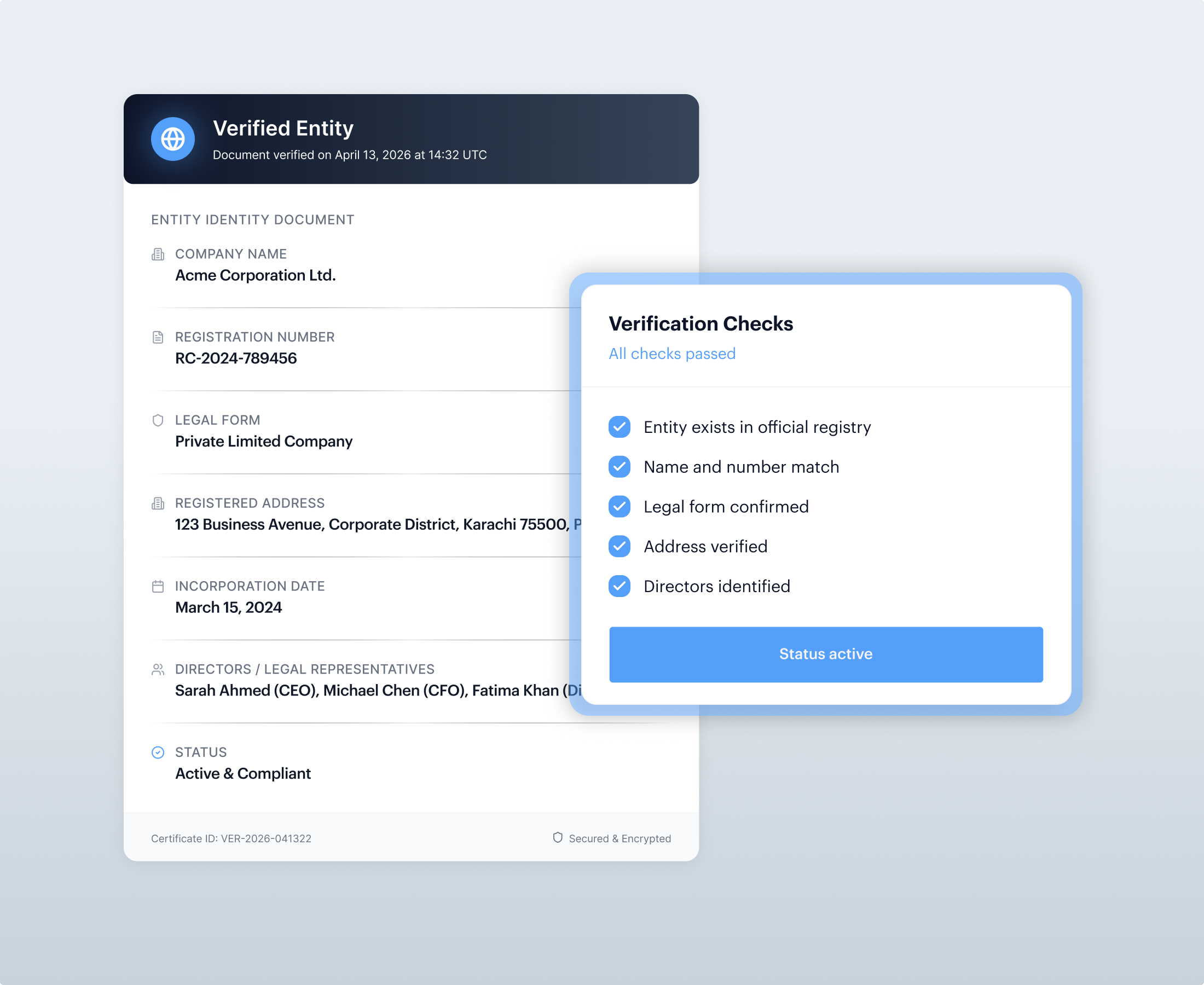

Certificate of Incorporation

Issued by Uganda Registration Services Bureau (URSB); specifies company name, place and date of incorporation; primary evidence of legal business entity status.

Memorandum and Articles of Association

Filed with URSB at incorporation; sets out company objectives, internal governance rules and share structure; required for business KYB verification.

Business Tax Identity

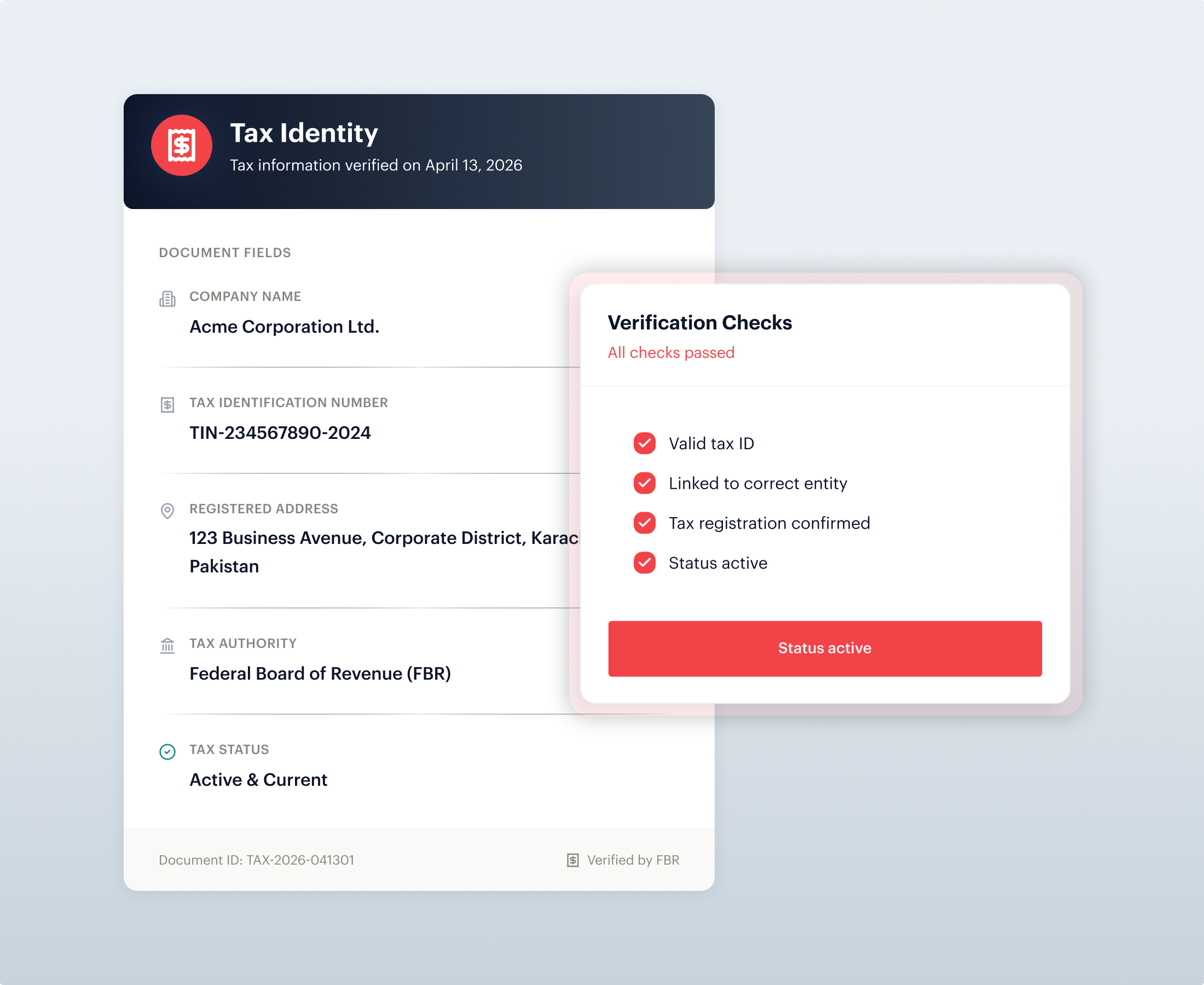

Tax Identification Number (TIN)

10-digit unique identifier issued by Uganda Revenue Authority; applies to companies and partnerships; required for tax administration and business verification.

VAT Registration Certificate

Issued by Uganda Revenue Authority to VAT-registered entities; confirms tax status and turnover threshold compliance; used in KYB to verify commercial scale.

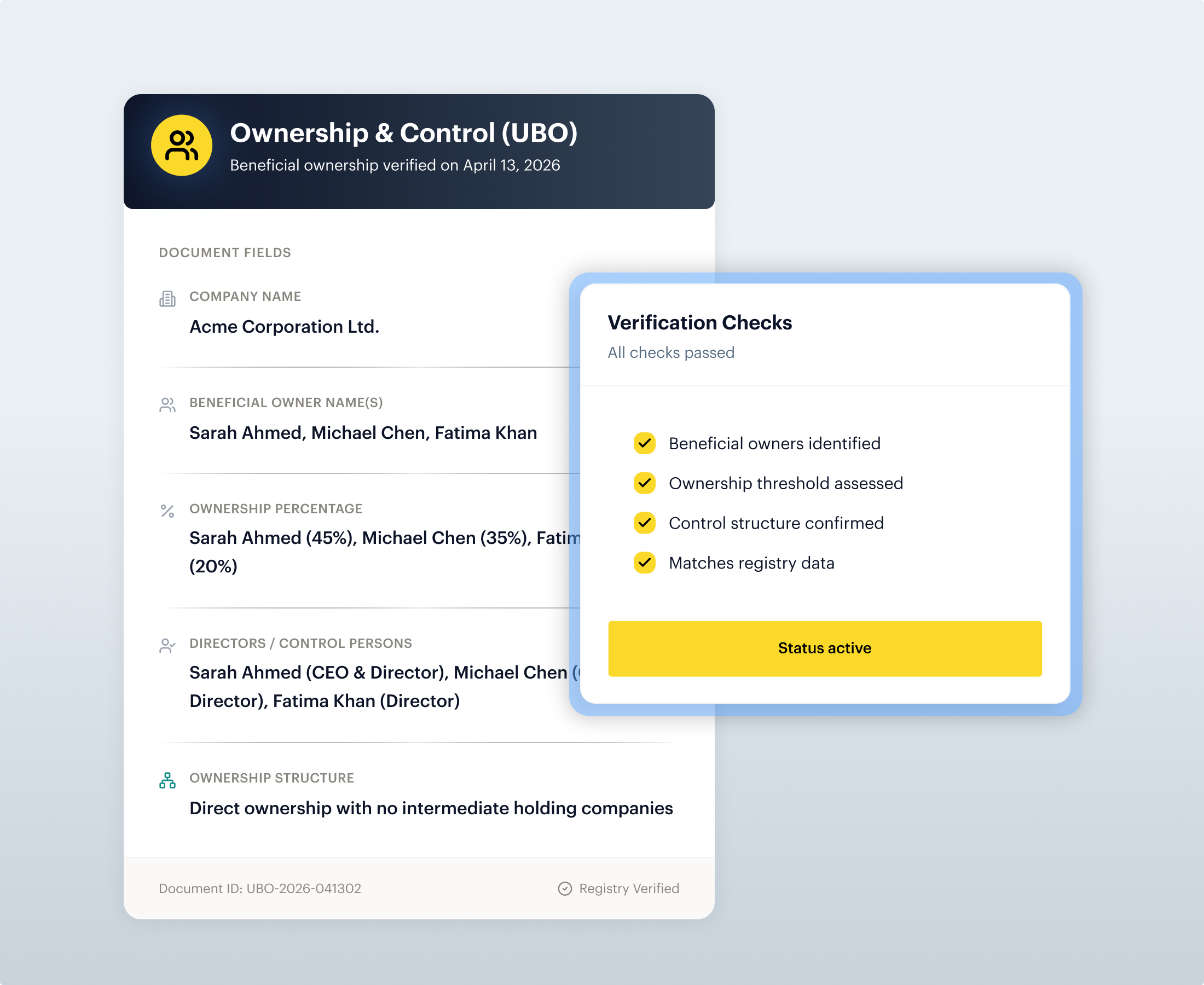

Ownership & Control (UBO)

Beneficial Ownership Register

Required by Companies (Amendment) Act 2022; filed with URSB within 30 days; discloses beneficial owner information, nature of ownership and control changes.

Register of Members

Maintained by every company under the Companies Act 2012; lists shareholders with share allocations and transfer history; used to confirm the ultimate ownership structure.

Languages We Cover

English-First Document Handling

Ugandan identity documents are issued in English. Shufti captures and stores structured data fields directly, eliminating translation friction in KYC workflows.

Name Matching With Luganda Support

Shufti handles Latin-script Luganda names alongside English to reduce false positives in sanctions and politically exposed persons (PEP) screening controls.

Evidence Consistency Across CDD Workflows

Identity data is reconciled across document inputs, beneficial ownership disclosures and screening outputs in one unified case file for audit compliance.

GOVERNANCE & CONTROLS

Audit-Ready Decisions, Lower Operational Drag

Fewer Avoidable Re-Submissions

Biometric National ID-first capture design reduces failure rates linked to Uganda's geographic identity access limitations in verification workflows.

Cleaner Audit Trails

Structured CDD case files meet Financial Intelligence Authority examination requirements and anti-money laundering recordkeeping standards comprehensively.

Better Name Matching Outcomes

Handles Luganda and English name variants, transliteration and diacritics to minimise false positives in sanctions and PEP screening controls.

One Workflow, One Back Office

KYC, KYB, sanctions screening and AML case management consolidated in one system with Bank of Uganda and FIA compliance mapped.

National ID-First Flow Design

Biometric National ID as primary verification pathway aligns with Uganda's digital identity infrastructure and regulatory compliance expectations.

Uganda IDV/KYC Challenges

Digital Identity Access Gap

A significant portion of Ugandans lack valid national IDs; geographic access to NIRA services is limited to 112 of 146 districts across the country.

Biometric Verification Limits

Banks cannot perform real-time facial verification against the NIRA database; live photo matching to national ID photo remains significantly constrained.

Rural Infrastructure Gap

Weak internet coverage in rural districts restricts access to online verification systems and real-time digital KYC platforms for customer onboarding.

Regulatory Interpretation Gap

Discrepancies exist between Bank of Uganda regulations and Anti-Money Laundering Regulations 2015; inconsistent fintech and money remitter onboarding standards.

Shufti’s IDV/KYC Solutions for Uganda

KYC Solutions

Face Verification

Reduces impersonation and synthetic identity fraud in customer onboarding; strengthens due diligence evidence against Uganda's documented fraud patterns.

.

Age Verification

Selfie-based age estimation with document verification fallback for regulated products; supports Uganda's risk-based customer due diligence framework.

.

Address Verification

Shufti can verify address-bearing documents, including Ugandan utility providers such as UEDCL (electricity), NWSC (water) and MTN Uganda; major banks.

.

Document Verification

Supports Uganda's primary identity documents, including biometric National ID with MRZ extraction, passports and driver's licences aligned to NIRA standards.

.KYB Solutions

Business Verification

Validates entity status through URSB registry data; corroborates TIN evidence; captures beneficial ownership disclosures per Companies Act compliance.

.")

Enhanced Due Diligence (EDD)

Structured escalation workflows for high-risk entities and politically exposed persons; produces reconstructable audit trails aligned with FIA standards.

.AML Screening

Business AML Screening

Screens entities and controlling persons against OFAC, UNSC sanctions lists and global politically exposed persons datasets per anti-money laundering.

.

Transaction Screening

Supports ongoing monitoring aligned to Uganda's goAML reporting platform obligations and suspicious activity monitoring in mobile money platform operations.

.Built to Fit Uganda's Compliance Landscape

Bank of Uganda (BoU)

Regulates banks and non-bank financial institutions; enforces KYC and AML/CTF compliance in the banking sector. Shufti outputs align with BoU examination standards.

Financial Intelligence Authority (FIA)

Uganda's primary AML authority receives, analyses, and disseminates financial intelligence via the goAML platform. Shufti supports FIA-compliant escalation.

Capital Markets Authority (CMA)

Regulates securities, capital markets and investment firms; licenses broker-dealers and fund managers; enforces AML. Shufti provides audit-ready CDD evidence.

Insurance Regulatory Authority (IRA)

Supervises insurers, reinsurers and brokers; enforces AML/CTF compliance in the insurance sector. Shufti supports customer verification for insurance operations.

Uganda Microfinance Regulatory Authority (UMRA)

Licences Tier-4 microfinance institutions and money lenders; promotes sound non-banking sector development. Shufti streamlines KYC for microfinance onboarding.

Uganda Revenue Authority (URA)

Enforces tax collection and administers TIN allocation and business formalisation requirements. Shufti validates TIN evidence and business registration.

Personal Data Protection Office (PDPO)

Data protection authority enforcing the Data Protection and Privacy Act 2019. Shufti logs consent and supports data subject access requests per PDPO requirements.

National Identification & Registration Authority (NIRA)

Issues biometric National ID Cards with fingerprint and facial recognition data. Shufti extracts MRZ and captures biometric fields per NIRA standards.

Deployment Choice

No major cloud provider operates data centres in Uganda; the closest infrastructure is in South Africa. Regulated entities typically require on-premise deployment.

Regulatory Alignment

Aligned to the Data Protection and Privacy Act 2019 and Anti-Money Laundering Act 2013 recordkeeping obligations and requirements enforced by PDPO and FIA.

Retention Controls

Minimum 10-year retention period mandated by the Anti-Money Laundering Act 2013 for account files, correspondence, customer due diligence and transaction records.

Encryption Posture

Data Protection and Privacy Act 2019 requires appropriate technical measures; compliance relies on industry-standard encryption practices and assessments.

Data Controls & Privacy for Uganda

Uganda AML Sources That Strengthen Decision

Parliament of Uganda

Uganda National Council for Science and Technology

Kabale District Local Government

Local Government of Napak District

Ministry of Local Government

New Vision

Daily Monitor

The Observer

Parliament of Uganda

Uganda National Council for Science and Technology

Kabale District Local Government

Local Government of Napak District

Ministry of Local Government

New Vision

Daily Monitor

The Observer

Parliament of Uganda

Uganda National Council for Science and Technology

Kabale District Local Government

Local Government of Napak District

Ministry of Local Government

New Vision

Daily Monitor

The Observer

Frequently Asked Questions

What are the KYC requirements for financial institutions in Uganda?

Financial institutions must conduct Customer Due Diligence (CDD) to verify customer identity using National ID, passport or driver's licence; assess beneficial ownership for companies; determine risk levels; and apply enhanced due diligence for high-risk customers and politically exposed persons under the Anti-Money Laundering Act 2013.

What is the role of the Financial Intelligence Authority (FIA) in Uganda's AML compliance?

The FIA is Uganda's primary authority for preventing and combating money laundering and terrorism financing. It receives, analyses and disseminates financial intelligence through the goAML platform and enforces compliance with the Anti-Money Laundering Act 2013 and Regulations 2015.

How do financial institutions in Uganda verify national identity cards for KYC purposes?

Financial institutions verify National ID cards using biometric data capture, machine-readable zone (MRZ) extraction and corroboration against NIRA records where access is authorised. Approximately 74 financial institutions currently access the NIRA database for digital KYC verification.

What are Uganda's Anti-Money Laundering Act requirements for beneficial ownership?

The Companies (Amendment) Act 2022 requires every company and limited liability partnership to maintain and file a Beneficial Ownership Register with URSB within 30 days of incorporation, disclosing beneficial owner information, nature of ownership and control changes.

What documents are accepted for identity verification in Uganda?

Primary documents are the National Identification Card, Passport and Driver's Licence issued by government authorities. Secondary documents include Voter's Card, Refugee ID and Certificate of Identity for KYC verification where primary documents are unavailable.

How long must financial institutions retain KYC and AML records in Uganda?

Financial institutions must maintain detailed KYC and AML records for a minimum of 10 years from the transaction date or account closure, as mandated by the Anti-Money Laundering Act 2013 for all account files and customer due diligence documentation.

What is eKYC (electronic Know Your Customer) and how is it implemented in Uganda?

Electronic KYC (eKYC) is remote digital customer verification using electronic methods rather than in-person onboarding. It is formally recognised under the Anti-Money Laundering Act 2013 amendments, enabling financial institutions to verify customers via NIRA database access and biometric document capture.

What are the penalties for non-compliance with Uganda's AML regulations?

Non-compliance with the Anti-Money Laundering Act 2013 can result in administrative fines, licence suspension, regulatory restrictions and criminal penalties, including imprisonment. Penalties vary based on violation severity and are enforced by FIA, Bank of Uganda and sectoral regulators.

How does customer due diligence (CDD) work in Uganda?

CDD requires financial institutions to identify and verify customer identity using reliable, independently sourced documents; assess beneficial ownership for companies; determine risk levels (low, medium, high); and apply enhanced due diligence measures for high-risk customers, politically exposed persons and cross-border exposure.

Build a Uganda-ready KYC, KYB & AML programme with Shufti

INDEPENDENTLY AUDITED. GLOBALLY CERTIFIED.

Certified to Global Standards

PROVEN WORKFLOWS

Use Cases for Regulated Growth in Uganda

Accelerate Growth, Eliminate Friction

Onboard users in seconds, not days. Deploy tiered address verification flows that maximise completion rates for genuine users while filtering out synthetic fraud.

Onboard Global Traders in Real-Time

Verify investors across 250+ countries & territories. Ensure compliance with international financial regulations while preventing identity theft and high-risk chargebacks.

Secure Trust at Every Transaction

Automate KYC and AML workflows to reduce manual onboarding costs. Strengthen residency checks while delivering the frictionless digital experience modern customers expect.

Power a Fair & Secure Player Experience

Reduce bonus abuse and multi-accounting rings at the door. Enforce location rules and trigger step-up checks without disrupting the player journey.

Build a Trusted, Verified Workforce

Screen freelancers and drivers at scale. Verify residency and reduce onboarding friction while maintaining trust between users.

Scale Your Exchange with Confidence

Balance anonymity with compliance. Instantly verify user jurisdiction to meet Travel Rule obligations and help stop abuse without slowing down legitimate trading volume.

Reduce fraud without blocking growth

Shufti supports marketplace integrity by verifying seller and buyer identities, enabling age-gated journeys where needed, and preserving evidence to support investigations, disputes and risk-led enforcement actions.

Accelerate Growth, Eliminate Friction

Onboard users in seconds, not days. Deploy tiered address verification flows that maximise completion rates for genuine users while filtering out synthetic fraud.

Onboard Global Traders in Real-Time

Verify investors across 250+ countries & territories. Ensure compliance with international financial regulations while preventing identity theft and high-risk chargebacks.

Secure Trust at Every Transaction

Automate KYC and AML workflows to reduce manual onboarding costs. Strengthen residency checks while delivering the frictionless digital experience modern customers expect.

Power a Fair & Secure Player Experience

Reduce bonus abuse and multi-accounting rings at the door. Enforce location rules and trigger step-up checks without disrupting the player journey.

Build a Trusted, Verified Workforce

Screen freelancers and drivers at scale. Verify residency and reduce onboarding friction while maintaining trust between users.

Scale Your Exchange with Confidence

Balance anonymity with compliance. Instantly verify user jurisdiction to meet Travel Rule obligations and help stop abuse without slowing down legitimate trading volume.

Reduce fraud without blocking growth

Shufti supports marketplace integrity by verifying seller and buyer identities, enabling age-gated journeys where needed, and preserving evidence to support investigations, disputes and risk-led enforcement actions.

Accelerate Growth, Eliminate Friction

Onboard users in seconds, not days. Deploy tiered address verification flows that maximise completion rates for genuine users while filtering out synthetic fraud.

Onboard Global Traders in Real-Time

Verify investors across 250+ countries & territories. Ensure compliance with international financial regulations while preventing identity theft and high-risk chargebacks.

Secure Trust at Every Transaction

Automate KYC and AML workflows to reduce manual onboarding costs. Strengthen residency checks while delivering the frictionless digital experience modern customers expect.

Power a Fair & Secure Player Experience

Reduce bonus abuse and multi-accounting rings at the door. Enforce location rules and trigger step-up checks without disrupting the player journey.

Build a Trusted, Verified Workforce

Screen freelancers and drivers at scale. Verify residency and reduce onboarding friction while maintaining trust between users.

Scale Your Exchange with Confidence

Balance anonymity with compliance. Instantly verify user jurisdiction to meet Travel Rule obligations and help stop abuse without slowing down legitimate trading volume.

Reduce fraud without blocking growth

Shufti supports marketplace integrity by verifying seller and buyer identities, enabling age-gated journeys where needed, and preserving evidence to support investigations, disputes and risk-led enforcement actions.

Let’s Tailor your journey

Just a few quick questions to guide your Shufti experience.

Shufti

Market Positioning and Commercial Assessment

Industry stands at 1.7rating

Best ID Verification Innovator

TOP 10 KYC Solution Provider

Best Client Onboarding Solution

Samer Al Tamimi@CEO of Safwa Bank

We take our client's privacy very seriously and always look for new innovative solutions to ensure a safe banking experience. Working with Shufti feels like a breath of fresh air, as their 100% in-house tech keeps our customer's data free from vulnerabilities and fully safe and protected.

PROVEN PLAYBOOKS

Explore Practical KYC & AML Resources

16 August, 2025

5 minutes read

How Much of What You’ve Verified Is Actually Real?

Shufti’s Deepfake Blindspot Audit now runs fully inside your AWS environment, auditing historic KYC for manipulation signals without moving sensitive data off-prem.

whitepapers